Quick Navigation

Report Overview

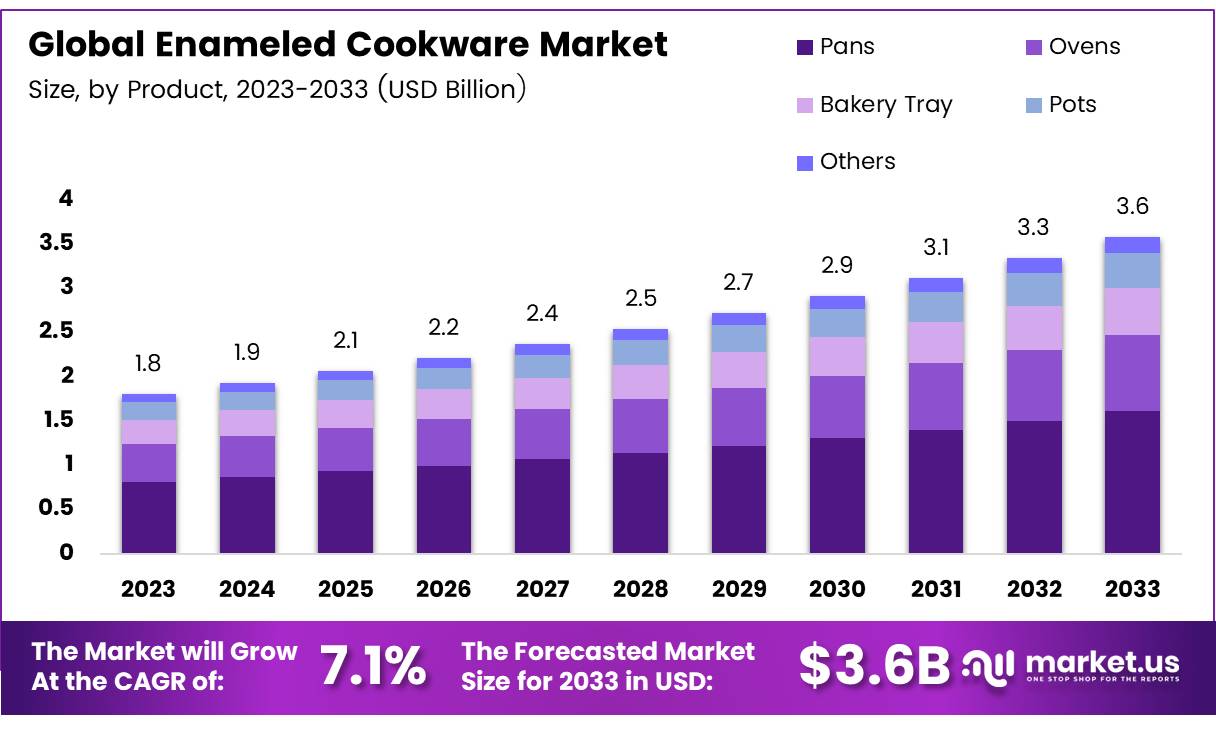

The Global Enameled Cookware Market size is expected to be worth around USD 3.6 Billion by 2033, from USD 1.8 Billion in 2023, growing at a CAGR of 7.1% during the forecast period from 2024 to 2033.

Enameled cookware refers to a category of cooking vessels, such as pots, pans, and baking dishes, that are coated with vitreous enamel. This enamel coating essentially involves fusing powdered glass to the cookware’s metal typically cast iron or heavy-gauge steel through a high-temperature baking process.

The market for enameled cookware represents a segment of the broader cookware industry that focuses on consumers seeking long-lasting, non-reactive, and aesthetically appealing cooking tools. It appeals to both gourmet chefs and home cooks who prioritize quality and health, given the non-reactive nature of the enamel that prevents the leaching of metals into food.

The market includes a variety of products ranging from basic pots and pans to high-end designer items, offered through multiple channels including retail stores, online platforms, and specialty boutiques.

From an analyst’s perspective, enameled cookware stands out due to its unique combination of durability and aesthetic appeal. The vitreous enamel coating provides a significant advantage over bare metal cookware by ensuring that no metallic tastes are imparted to the food, a crucial factor for culinary purity.

Furthermore, the robustness of the enamel coating reduces the need for frequent replacements, appealing to cost-conscious consumers looking for long-term kitchen investments. However, the production process for enameled cookware, which involves multiple stages of coating and firing, can be more resource-intensive than that for simpler metal cookware, potentially impacting manufacturing scalability and cost-effectiveness.

The enameled cookware market is currently experiencing growth driven by rising consumer awareness regarding health and wellness, which in turn fuels demand for non-toxic and safe cooking options. This trend is bolstered by the aesthetic versatility of enameled cookware, which makes it appealing to a broad demographic.

According to the National Center for Biotechnology Information (NCBI), while aluminum cookware dominated 62.33% of local shop sales in 2023, the demand for safer, high-quality alternatives is on the rise, notably among discerning consumers who are willing to invest in premium kitchenware.

The growth of the enameled cookware market can be attributed to several factors including increased consumer interest in high-quality kitchen tools and a growing inclination towards visually appealing cookware in home kitchens.

Opportunities for expansion into emerging markets exist, particularly as global incomes rise and standards of living improve. Governmental investment in safety regulations, as highlighted by the Consumer Product Safety Commission’s (CPSC) recall of 300 units of potentially hazardous cookware in 2023, underscores the market’s need for adherence to high production standards, thereby creating avenues for premium products.

Key Takeaways

- The global enameled cookware market is projected to reach USD 3.6 billion by 2033, growing at a CAGR of 7.1% from 2024 to 2033.

- Pans accounted for a 31.2% share in 2023, dominating the product segment due to their versatility in kitchens.

- The residential application segment led the market in 2023, driven by increased demand for durable and high-quality cookware for home use.

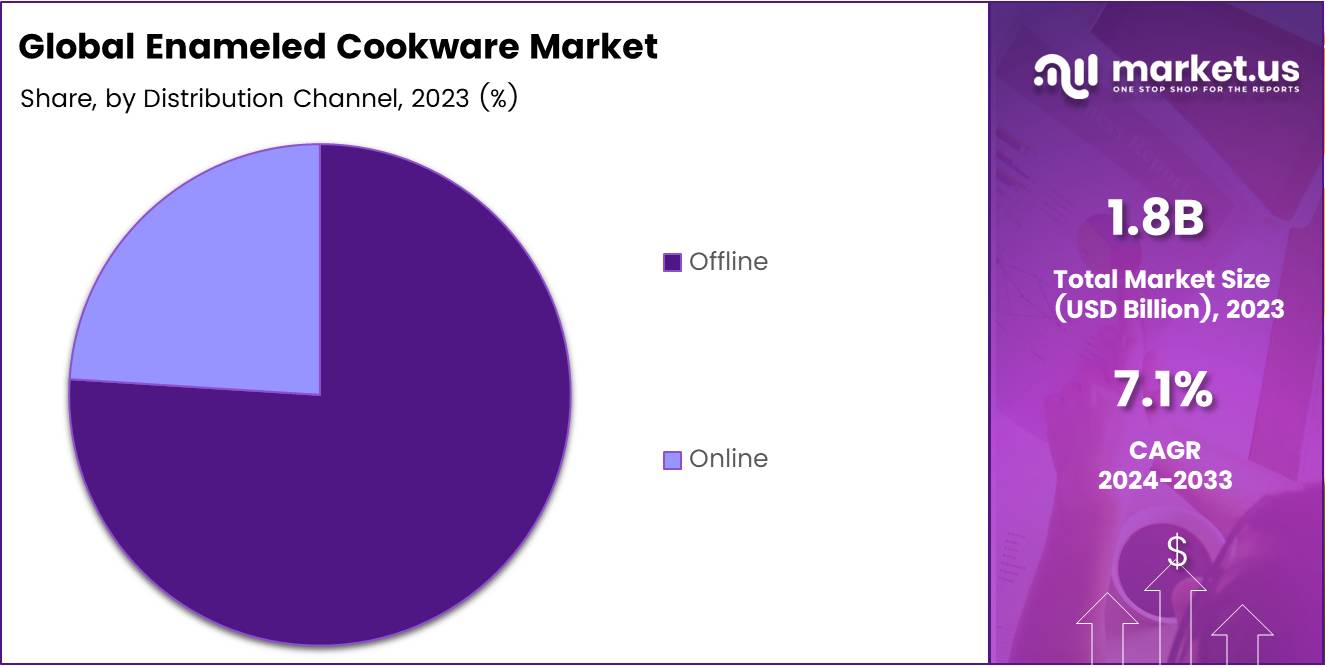

- Offline distribution channels dominated the market in 2023, reflecting consumer preference for hands-on evaluation before purchase.

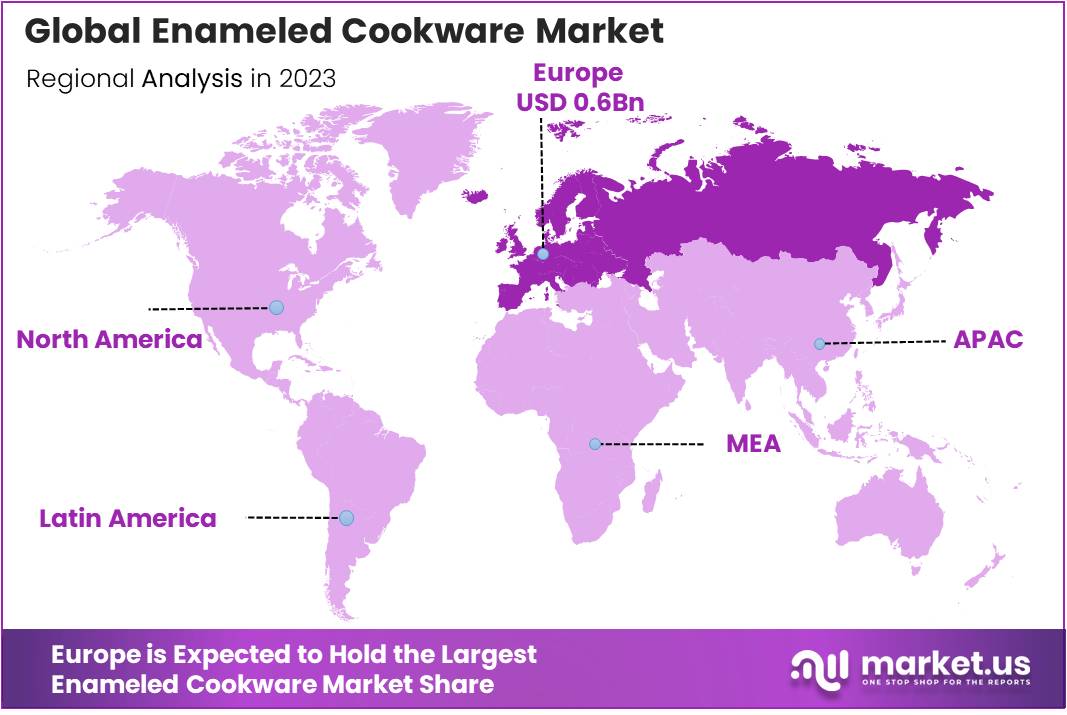

- Europe held a leading 37.5% market share in 2023, valued at USD 0.6 billion, driven by traditional cooking practices and eco-friendly preferences.

Product Analysis

Pans Lead Enameled Cookware Market in 2023 with 31.2% Share

In 2023, Pans held a dominant market position in the By Product Analysis segment of the Enameled Cookware Market, capturing a 31.2% share. This substantial market share underscores the robust demand for pans within the cookware sector, attributable to their versatility and widespread use in both household and commercial kitchens.

Following pans, ovens emerged as the second most significant category, reflecting a growing trend towards baked and healthy cooking methods. Bakery trays, although essential for specific baking needs, occupied a smaller segment of the market, indicative of their specialized application.

Pots maintained a steady market presence, benefiting from their fundamental role in diverse cooking practices. The category labeled Others, which includes various minor cookware products, collectively accounted for the remaining percentage of the market. This segment demonstrates a niche but essential part of the cookware landscape, catering to specialized culinary needs and innovative cooking technologies.

Overall, the distribution of market shares within the Enameled Cookware Market illustrates a clear preference for pans, suggesting a strong consumer focus on versatile and durable cooking solutions. The sustained popularity of these items is likely driven by ongoing innovations in cookware design and materials, enhancing their appeal and functionality across multiple cooking environments.

Application Analysis

Residential Sector Leads Enameled Cookware Market in 2023

In 2023, Residential held a dominant market position in the By Application Analysis segment of the Enameled Cookware Market. This sector’s leadership can be attributed to increasing consumer preferences for high-quality and durable cooking solutions in home kitchens.

The growing trend towards home cooking, amplified by ongoing global health concerns, has significantly driven the demand for enameled cookware, which is renowned for its longevity and ease of cleaning.

The commercial sector also shows a steady demand for enameled cookware, driven by the hospitality industry’s need for durable and aesthetically pleasing cookware in professional kitchens. However, the scale of growth in this sector pales in comparison to the residential segment. This disparity is largely due to the more frequent replacement and upgrade cycles in residential settings compared to commercial ones.

Market projections suggest that the residential segment will continue to expand its market share, supported by the increasing investments in home improvement and kitchen upgrades. The commercial segment is expected to witness moderate growth, contingent on the recovery of the hospitality sector and improvements in consumer spending in the post-pandemic economic landscape.

These trends underscore the significant influence of consumer behavior and economic conditions on the enameled cookware market dynamics.

Distribution Channel Analysis

Offline Dominates Enameled Cookware Distribution, But Online Channels Show Promise

In 2023, Offline held a dominant market position in the By Distribution Channel Analysis segment of the Enameled Cookware Market. This segment’s strength can be attributed to consumers’ preference for tangible evaluation of cookware’s quality and usability before purchase, a factor that significantly influences buyer decisions.

Brick-and-mortar stores offer the tactile experience that online platforms cannot, thus reinforcing the offline channels’ prominence.

However, the online distribution channel is rapidly gaining traction, fueled by the convenience of e-commerce and the expanding digital literacy among consumers. The rise in online shopping has been catalyzed by enhancements in digital marketing strategies and the robust development of e-commerce technology, which improve customer engagement and trust.

Data indicate a growing consumer inclination towards online purchases, which suggests a potential shift in the distribution dynamics over the coming years.

Online channels are expected to increase their market share by leveraging advanced analytics to personalize shopping experiences and by enhancing user interface designs to facilitate easier navigation and transaction processes.

This evolving landscape indicates a significant opportunity for market stakeholders to optimize their channel strategies to cater to shifting consumer preferences.

Key Market Segments

By Product

- Pans

- Ovens

- Bakery Tray

- Pots

- Others

By Application

- Residential

- Commercial

By Distribution Channel

- Offline

- Online

Drivers

Consumer Interest Fuels Demand for Enameled Cookware

The market for enameled cookware is driven by several key factors that resonate strongly with today’s health-conscious and aesthetically inclined consumers.

Firstly, enameled cookware’s non-reactive properties make it an ideal choice for health-centric cooking, especially when preparing acidic foods that could react with other metals. This non-toxic nature, devoid of chemicals such as PFOA, PFOS, and PTFE, appeals to consumers prioritizing safety in their cooking environments.

Additionally, the durability and longevity of enameled cookware stand out as significant advantages. Its resistance to wear, chipping, and scratching extends its lifespan, making it a cost-effective solution for long-term kitchen investments. The ease of cleaning, thanks to its smooth, non-porous surface, further enhances its appeal to those with busy lifestyles.

Moreover, the vibrant colors and designs available in enameled cookware meet the growing consumer demand for kitchenware that is both functional and stylish. These factors collectively drive the growth of the enameled cookware market, as they cater to both practical and aesthetic consumer needs.

Restraints

Limited High-Temperature Tolerance Limits Versatility

Enameled cookware’s suitability for diverse cooking methods faces significant constraints due to its limited high-temperature tolerance. This type of cookware is generally not recommended for high-temperature cooking techniques such as searing or broiling.

Such limitations reduce its versatility when compared to alternatives that can withstand higher temperatures. Additionally, the heavy weight of enameled cast iron cookware poses a challenge. This characteristic makes it less appealing for those who prefer lighter and more manageable kitchen tools, affecting its practicality and portability.

The combined effect of these factors may restrict the expansion of the enameled cookware market, as potential buyers might opt for more adaptable and easy-to-handle options available in the market.

Growth Factors

Expansion into Emerging Markets

The enameled cookware market presents a promising growth landscape, primarily fueled by expansion into emerging markets. Increased disposable incomes and a burgeoning middle class in regions such as Asia-Pacific, Latin America, and the Middle East are pivotal in amplifying demand for enameled cookware.

This demographic shift, coupled with heightened consumer awareness regarding the benefits of quality kitchenware, creates a fertile environment for market penetration and expansion.

Furthermore, leveraging product innovation, such as new designs, enhanced non-stick features, and a palette of color options, can significantly appeal to diverse consumer preferences.

Additionally, the escalating demand for eco-friendly and non-toxic products aligns with global sustainability trends, offering an avenue for differentiation and capturing a niche market segment.

The expansion of online sales channels also plays a crucial role, as the increasing prevalence of e-commerce platforms and direct-to-consumer sales strategies can broaden market reach and accessibility, thereby augmenting market growth potential in these dynamic regions.

Emerging Trends

Minimalist Kitchens Elevate Enameled Cookware’s Appeal

In the enameled cookware market, several trending factors are shaping consumer preferences and driving sales. The minimalist and clean aesthetic in kitchen designs is prominently boosting the appeal of stylish enameled cookware, which complements contemporary home decor.

Additionally, there is a notable resurgence in vintage and retro kitchen styles, where enameled cookware, especially cast iron varieties, offers a nostalgic touch to modern cooking spaces. This retro appeal taps into a broader desire for traditional cooking methods and old-fashioned design aesthetics.

Furthermore, the increasing popularity of slow cooking methods, such as braising, stewing, and baking, positions enameled cookware, particularly Dutch ovens, as essential tools for these techniques. This is due to their heat retention properties and versatility.

Finally, the shift towards sustainability is influencing consumer choices, with enameled cookware made from recyclable and durable materials gaining traction as an eco-friendly option. These factors collectively enhance the market attractiveness of enameled cookware, aligning well with both functional and ethical consumer expectations.

Regional Analysis

Europe Leads Enameled Cookware Market with 37.5% Share, Valued at $0.6 Billion Due to Strong Preference

Europe stands as the dominant region in the enameled cookware market, commanding a 37.5% share with a market value of USD 0.6 billion. This leadership can be attributed to traditional cooking practices that favor enameled cookware for its heat retention and non-reactive properties. European consumers also show a high preference for eco-friendly and health-conscious cookware solutions, further bolstering the market.

Regional Mentions:

In North America, the market is characterized by a strong preference for durable and aesthetically pleasing kitchenware, with the United States leading in terms of adoption rates. The demand in North America is driven by an increasing interest in home cooking and premium kitchen products. The region benefits from the presence of established manufacturers and a well-distributed retail sector that enhances product accessibility.

The Asia Pacific region is witnessing rapid growth in the enameled cookware market, driven by expanding middle-class populations and rising disposable incomes. Countries like China and India are major contributors to this growth, with local manufacturers expanding their reach and product offerings. The trend towards adopting Western cooking styles and the growing hospitality sector are significant growth factors in this region.

In the Middle East & Africa, the market is developing at a steady pace. The growing urbanization and the increasing number of expatriates along with the rising tourism sector, particularly in the UAE and Saudi Arabia, are contributing to the regional market expansion. The preference for luxurious and long-lasting cookware is expected to drive the demand for enameled cookware in this region.

Latin America shows potential for growth in the enameled cookware market, with Brazil and Mexico leading the way. The increase in urban households and the growing influence of European and North American cooking practices are expected to drive market growth in the region.

These regional dynamics highlight the diverse factors influencing the enameled cookware market globally, with Europe maintaining a significant lead due to its established consumer base and historical preference for enameled cookware.

Key Regions and Countries covered іn thе rероrt

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2023, the global enameled cookware market has witnessed considerable contributions from key players, notably enhancing the competitive landscape and consumer preferences within this sector. Le Creuset, with its premium positioning, continues to lead by leveraging its longstanding reputation for quality and durability. The brand’s ability to blend tradition with modern design appeals to both new and loyal customers, sustaining its market dominance.

The Coleman Company, Inc., recognized for its robust outdoor cookware, capitalizes on the growing trend of outdoor cooking and camping. Their products are designed to cater to rugged environments, thus expanding their customer base among outdoor enthusiasts. Staub, similar to Le Creuset, is revered for its high-quality cast iron cookware, which is prized for its heat retention properties, offering a distinctive choice for consumers seeking reliable and long-lasting cookware.

LODGE stands out for its cost-effective yet durable offerings, making enameled cookware accessible to a broader market segment. This strategic positioning helps in capturing value-conscious consumers without compromising on quality. Tramontina and Cuisinart also contribute significantly to the market through their diversified product ranges that cater to everyday cooking needs, blending functionality with affordability.

Country Door (Colony Brands) leverages its unique direct-to-consumer model to enhance customer engagement and satisfaction, offering personalized cookware solutions that resonate with home cooks. CAMP CHEF, specializing in outdoor cooking equipment, strengthens its market presence by addressing the niche segment of outdoor culinary activities.

WILLIAMS-SONOMA INC. and VERMICULAR emphasize innovation and luxury in cookware, with a focus on enhancing the culinary experience through advanced technologies and superior craftsmanship. Their products often serve as a benchmark for quality and innovation in the cookware market.

Overall, these key players are pivotal in driving growth and innovation within the global enameled cookware market, each employing distinct strategies to capture and sustain market share in an increasingly competitive environment. Their efforts are instrumental in shaping market dynamics and influencing consumer trends in 2023.

Top Key Players in the Market

- Le Creuset

- The Coleman Company, Inc.

- Staub

- LODGE

- Tramontina

- Cuisinart

- Country Door (Colony Brands)

- CAMP CHEF

- WILLIAMS-SONOMA INC.

- VERMICULAR

Recent Developments

- In October 2023, Titan Capital spearheaded the seed funding round for P-TAL, a brand specializing in kitchenware and home décor, successfully raising INR 4.33 crore along with contributions from other investors.

- In February 2024, the consumer houseware startup Basil successfully raised Rs 3.6 crore in seed funding to expand its product line and enhance market reach.

- In September 2024, Nestasia, a home décor and lifestyle brand, secured substantial growth capital amounting to $8.35 million, aimed at accelerating expansion and broadening its consumer base.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 1.8 Billion |

| Forecast Revenue (2033) | USD 3.6 Billion |

| CAGR (2024-2033) | 7.1% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Pans , Ovens, Bakery Tray, Pots, Others), By Application (Residential, Commercial), By Distribution Channel (Offline, Online) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Le Creuset, The Coleman Company, Inc., Staub, LODGE, Tramontina, Cuisinart, Country Door (Colony Brands), CAMP CHEF, WILLIAMS-SONOMA INC., VERMICULAR |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |