Quick Navigation

Market Overview

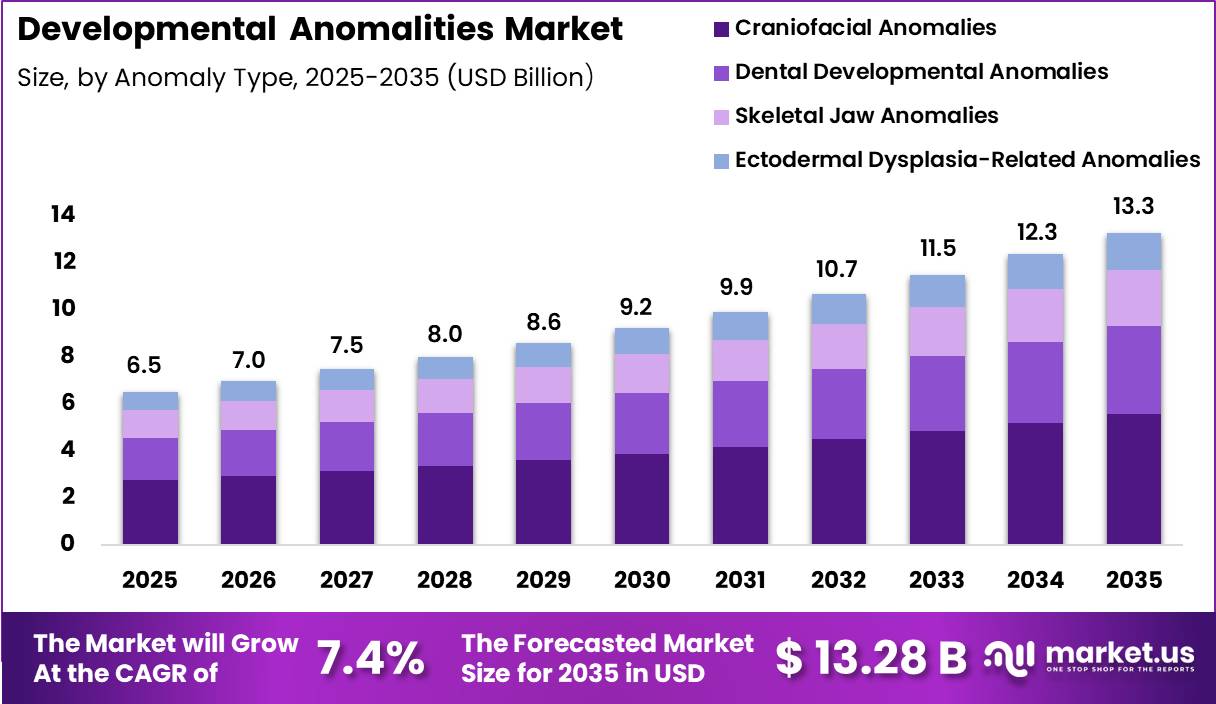

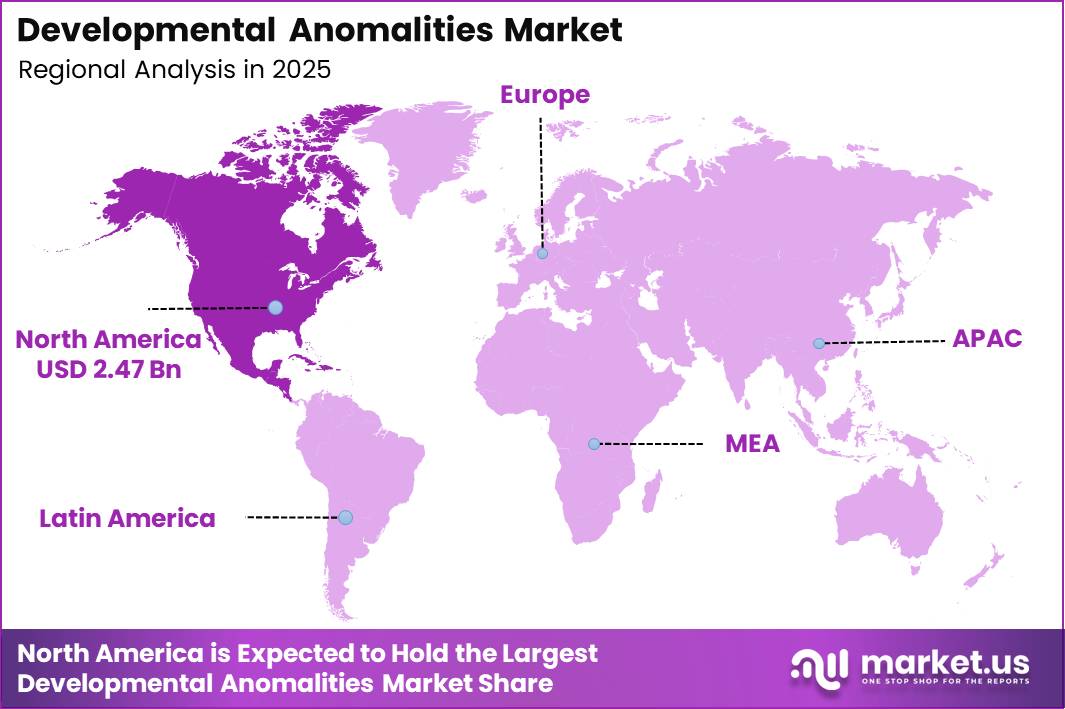

Global Developmental Anomalities Market size is expected to be worth around US$ 13.28 Billion by 2035 from US$ 6.50 Billion in 2025, growing at a CAGR of 7.4% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 38.00% share with a revenue of US$ 2.47 Billion.

Developmental anomalies, also referred to as congenital anomalies or birth defects, are structural or functional abnormalities that occur during fetal development and may be detected before birth, at delivery, or later in life.

The Developmental Anomalities Market is expanding as healthcare systems increase investment in prenatal screening, genetic diagnostics, neonatal intensive care, and corrective surgical procedures.

Growing awareness of early diagnosis, wider adoption of advanced ultrasound, fetal MRI, genomic sequencing, and newborn screening programs are improving the detection and management of congenital disorders. Public health initiatives promoting maternal nutrition, folic acid supplementation, vaccination, and prenatal care are also supporting demand for diagnostic and therapeutic solutions.

According to the World Health Organization (WHO), approximately 6% of babies worldwide are born with a congenital disorder, while an estimated 240,000 newborns die within the first 28 days of life each year due to congenital disorders, with an additional 170,000 deaths occurring between one month and five years of age.

WHO also reports that nearly 94% of severe congenital disorders occur in low- and middle-income countries, highlighting the need for improved access to screening and treatment services.

The market is further supported by technological advances in molecular diagnostics, fetal surgery, pediatric imaging, and multidisciplinary neonatal care. Healthcare providers are increasingly adopting precision medicine approaches to improve long-term outcomes for affected infants.

According to the U.S. Centers for Disease Control and Prevention (CDC), 1 in every 33 babies in the United States is born with a birth defect each year, and birth defects account for approximately 20% of all infant deaths in the country.

Updated CDC surveillance data also estimates around 1,251 annual cases of spina bifida, 758 cases of anencephaly, and 386 cases of encephalocele based on national birth-defect monitoring systems.

These statistics emphasize the continuing clinical and economic importance of developmental anomalies, driving innovation in prenatal diagnostics, surgical interventions, rehabilitation services, and long-term patient management.

Key Takeaways

- Market Size: Global Developmental Anomalities Market size is expected to be worth around US$ 13.28 Billion by 2035 from US$ 6.50 Billion in 2025.

- Market Share: The market is growing at a CAGR of 7.4% during the forecast period from 2026 to 2035.

- Anomaly Type: Craniofacial Anomalies (Cleft Lip & Palate) dominate the Developmental Anomalies Market with a 42.00% share in 2025.

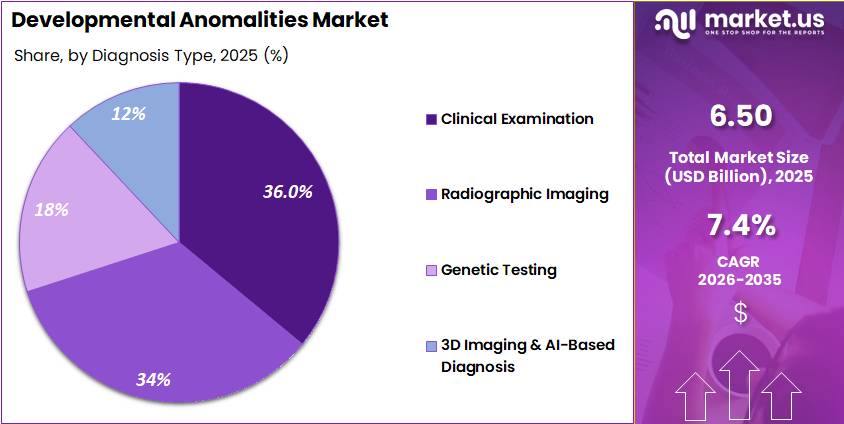

- Diagnosis Type: Clinical Examination dominates the Diagnosis Type segment with a 36.00% share in 2025.

- Treatment Type: The Surgical Correction segment dominated the Developmental Anomalities Market, accounting for 48.00% of total market revenue in 2025.

- End User: Hospitals dominate the End User segment with a 44.00% share in 2025.

- Age Group: Pediatric Patients dominate the Age Group segment with a 58.00% share in 2025.

- Distribution Channel: Hospital Pharmacies dominate the Distribution Channel segment with a 46.00% share in 2025.

- Regional Analysis: In 2025, North America led the market, achieving over 38.00% share with a revenue of US$ 2.47 Billion.

Anomaly Type Analysis

Craniofacial Conditions Lead Due to High Surgical Complexity and Early Diagnosis Demand.

Craniofacial Anomalies, particularly Cleft Lip & Palate, dominate the Developmental Anomalies Market with a 42.00% share in 2025, primarily due to their high global incidence and strong demand for early surgical and multidisciplinary intervention.

These conditions are often detected at birth or during prenatal screening, enabling early treatment planning and higher diagnosis rates. Dental Developmental Anomalies, including tooth agenesis and supernumerary teeth, account for 28.00% of the market, driven by increasing orthodontic consultations and rising aesthetic awareness.

Skeletal Jaw Anomalies hold an 18.00% share, supported by growing cases of maxillofacial deformities and trauma-related developmental disruptions requiring corrective surgery. Ectodermal Dysplasia-Related Anomalies contribute the remaining 12.00%, representing a niche but clinically complex segment involving hair, skin, and dental abnormalities.

Overall, craniofacial conditions dominate due to higher visibility, functional impairment, and availability of advanced surgical correction options. However, dental and skeletal anomalies are witnessing steady growth because of expanding orthodontic infrastructure and improved imaging diagnostics.

Increasing awareness programs and neonatal screening initiatives are further improving detection rates across all anomaly types, reinforcing structured treatment pathways and long-term patient management strategies in both developed and emerging healthcare systems.

Diagnosis Type Analysis

Clinical Examination Remains Core Diagnostic Backbone Despite Rapid Imaging Innovation.

Clinical Examination leads the Diagnosis Type segment in the Developmental Anomalies Market with a 36.00% share in 2025, as it remains the first-line, cost-effective, and widely accessible method for identifying structural and developmental abnormalities.

Radiographic Imaging follows closely with a 34.00% share, driven by increasing use of X-rays, CT scans, and panoramic imaging in orthodontic and maxillofacial diagnostics. Genetic Testing accounts for 18.00%, reflecting its growing importance in identifying hereditary syndromes and chromosomal abnormalities associated with developmental defects.

3D Imaging & AI-Based Diagnosis represents 12.00% of the market but is the fastest-growing segment, supported by advancements in digital dentistry, machine learning algorithms, and precision diagnostics. These technologies enhance early detection accuracy and treatment planning efficiency, especially in complex craniofacial cases.

Overall, diagnostic trends are shifting toward integrated approaches combining clinical evaluation with advanced imaging and genetic profiling. Hospitals and specialized dental centers increasingly adopt hybrid diagnostic workflows to improve accuracy and reduce misdiagnosis.

The rising availability of portable imaging systems and AI-assisted platforms is further strengthening diagnostic capabilities, particularly in urban healthcare settings, while gradual adoption in developing regions is expected to expand market penetration over the forecast period.

Treatment Type Analysis

Surgical Correction Dominates Due to High Clinical Necessity in Severe Developmental Cases.

Surgical Correction dominates the Treatment Type segment in the Developmental Anomalies Market with a 48.00% share in 2025, primarily due to the high necessity for reconstructive procedures in craniofacial and skeletal anomalies.

These interventions are often essential for restoring both function and aesthetics, particularly in cases such as cleft palate repair and jaw reconstruction. Orthodontic Treatment represents a significant complementary segment, focusing on alignment correction, bite adjustment, and long-term dental stabilization.

Prosthetic Rehabilitation is also gaining traction, especially for patients requiring functional restoration after surgical procedures or congenital deficiencies.

Regenerative & Tissue Engineering Approaches, although still emerging, are gradually expanding as research advances in stem cell therapy, biomaterials, and bioengineered bone grafting. These innovations aim to reduce surgical complexity and improve long-term outcomes.

Overall, the treatment landscape is evolving toward a multidisciplinary approach combining surgery, orthodontics, and regenerative medicine. Hospitals and specialized craniofacial centers are increasingly integrating these modalities to deliver personalized treatment plans.

Rising healthcare expenditure, improved surgical techniques, and better postoperative care infrastructure are further strengthening the dominance of surgical correction while supporting steady growth in non-invasive and regenerative alternatives.

End User Analysis

Hospitals Maintain Leadership Due to Integrated Multidisciplinary Treatment Infrastructure.

Hospitals dominate the End User segment in the Developmental Anomalies Market with a 44.00% share in 2025, primarily due to their comprehensive infrastructure, multidisciplinary teams, and advanced surgical capabilities.

They serve as the primary centers for complex craniofacial and skeletal anomaly treatments requiring coordinated surgical, orthodontic, and rehabilitative care. Dental Orthodontic Clinics represent the second-largest segment, driven by increasing demand for corrective dental procedures and early-stage anomaly management. These clinics play a crucial role in long-term orthodontic care and cosmetic correction procedures.

Academic & Research Institutes account for a smaller but strategically important share, focusing on innovation, clinical trials, and development of advanced diagnostic and treatment methodologies.

Overall, hospitals remain the central hub for high-acuity cases, while specialty clinics are expanding their role in outpatient and long-term care management. The growing collaboration between hospitals and dental clinics is improving referral systems and treatment continuity.

Increasing investment in specialized craniofacial centers and expansion of healthcare infrastructure in emerging economies are further strengthening hospital dominance while supporting gradual growth across specialized care settings.

Age Group Analysis

Pediatric Population Drives Market Demand Due to Early-Onset Nature of Developmental Anomalies.

Pediatric Patients dominate the Age Group segment in the Developmental Anomalies Market with a 58.00% share in 2025, as most developmental anomalies are congenital and identified during infancy or early childhood.

Early diagnosis and intervention are critical in this group to prevent long-term functional, structural, and psychological complications. Adolescents represent a significant secondary segment, as many dental and skeletal anomalies become more apparent during growth spurts, often requiring orthodontic or corrective surgical procedures.

Adults account for a smaller share but continue to represent ongoing demand for corrective surgeries, particularly for untreated congenital conditions or late-diagnosed anomalies. Increasing awareness and improved access to diagnostic services are enabling earlier detection across all age groups.

Overall, the dominance of pediatric patients is driven by neonatal screening programs, prenatal imaging advancements, and growing emphasis on early corrective interventions. Healthcare providers are increasingly focusing on integrated pediatric care pathways that combine surgery, orthodontics, and rehabilitation.

Meanwhile, rising cosmetic and functional correction demand among adolescents and adults is expanding the long-term treatment landscape, supporting sustained market growth across all age groups.

Distribution Channel Analysis

Hospital Pharmacies Lead Owing to Critical Role in Post-Surgical and Inpatient Care Delivery.

Hospital Pharmacies dominate the Distribution Channel segment in the Developmental Anomalies Market with a 46.00% share in 2025, primarily due to their direct integration with inpatient and surgical care services.

They ensure immediate availability of post-operative medications, antibiotics, and supportive therapies required after corrective procedures. Specialty Clinics & Centers represent a growing segment, driven by increasing patient preference for focused orthodontic and craniofacial care services. These centers often provide personalized treatment plans and long-term follow-up care.

Online Pharmacies are gradually expanding their presence, supported by rising digital healthcare adoption, improved logistics, and increasing demand for convenient medication access, particularly for routine prescriptions and maintenance therapies. The Others category includes small retail pharmacies and community-based dispensaries that serve localized patient populations.

Overall, hospital pharmacies continue to dominate due to their critical role in perioperative care and complex treatment management. However, the distribution landscape is gradually diversifying with the expansion of specialty care networks and digital platforms.

Increasing healthcare digitization, improved prescription tracking systems, and expanding outpatient care models are expected to further reshape distribution dynamics in the coming years.

Key Market Segments

Anomaly Type

- Craniofacial Anomalies (Cleft Lip & Palate)

- Dental Developmental Anomalies (Tooth agenesis, supernumerary teeth)

- Skeletal Jaw Anomalies

- Ectodermal Dysplasia-Related Anomalies

Diagnosis Type

- Clinical Examination

- Radiographic Imaging

- Genetic Testing

- 3D Imaging & AI-Based Diagnosis

Treatment Type

- Surgical Correction

- Orthodontic Treatment

- Prosthetic Rehabilitation

- Regenerative & Tissue Engineering Approaches

End User

- Hospitals

- Dental & Orthodontic Clinics

- Academic & Research Institutes

Age Group

- Pediatric Patients

- Adolescents

- Adults

Distribution Channel

- Hospital Pharmacies

- Specialty Clinics & Centers

- Online Pharmacies

- Others

Opportunity

Longitudinal registry monetization represents an emerging opportunity in congenital and developmental disorder care because most current systems focus on diagnosis and treatment rather than long-term data management. CDC birth-defects tracking programs collect information on defect occurrence, risk factors, referral needs, and healthcare resource utilization.

The Environmental Public Health Tracking Network also provides standardized metrics such as prevalence per 10,000 live births and average annual case counts across 12 monitored birth defects. These data frameworks create opportunities for advanced registry platforms that support care coordination, outcomes monitoring, and natural-history research.

Longitudinal registries can also enable real-world evidence generation, post-market surveillance, and clinical endpoint development for rare conditions. By connecting specialty centers, diagnostic providers, researchers, and therapy developers, registry platforms can become valuable healthcare infrastructure.

This creates potential for recurring enterprise services focused on analytics, patient tracking, and evidence generation rather than one-time clinical interactions alone.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Genomic first-line diagnostics | North America, EU, Japan, Korea, urban India | Medium term (2-4 years) | |

| LMIC congenital care networks | South Asia, Africa, LATAM, Southeast Asia | Long term (≥ 4 years) | |

| Longitudinal registry monetization | North America, EU, regulated APAC | Medium term (2-4 years) | |

| Maternal prevention platforms | India, Africa, LATAM, public EU systems | Short term (≤ 2 years) | |

| Rare-anomaly center roll-ups | North America, EU, GCC, advanced APAC | Long term (≥ 4 years) | |

| Transition-to-adult care services | North America, EU, Japan, Korea | Medium term (2-4 years) |

Drivers

Tertiary referral concentration is a key driver in the developmental anomalies market because many congenital and developmental conditions require highly specialized, multidisciplinary care. WHO identifies congenital disorders as a major cause of chronic illness and disability, often requiring long-term referral and support services.

Effective management typically involves coordinated care across pediatrics, genetics, imaging, surgery, rehabilitation, and care-coordination teams. CDC guidance also emphasizes the importance of linking affected children to appropriate specialist services and ongoing support networks.

This referral model channels patients toward specialized centers capable of delivering advanced diagnostics, complex interventions, and long-term follow-up care. Such centers benefit from higher patient volumes, stronger clinical expertise, and integrated treatment pathways.

As a result, center-of-excellence networks are becoming increasingly important for care delivery, referral capture, multidisciplinary service provision, and long-term patient management across the developmental-anomalies continuum.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance |

|---|---|---|

| High congenital disease burden | Global, strongest in LMICs | |

| Surveillance and tracking expansion | North America, EU, regulated APAC | |

| Prevention and prenatal screening push | North America, EU, India, LATAM, Africa | |

| Transition-to-adult care demand | North America, EU, Japan, Korea | |

| Tertiary referral concentration | North America core, EU hubs, GCC, urban APAC | |

| Genomic diagnostic integration | North America, EU, Japan, Korea, urban India |

Challenges

Etiologic and data uncertainty remains a significant challenge in the developmental anomalies market because the causes of many congenital conditions are not fully understood. WHO notes that congenital disorders can arise from genetic, infectious, nutritional, environmental, or multiple interacting factors, making precise cause identification difficult in many cases.

This limits the ability to develop highly targeted prevention and intervention strategies beyond broad public-health measures such as folate supplementation, vaccination, and diabetes management. CDC tracking systems collect data on the occurrence and distribution of birth defects, but standardized environmental tracking metrics currently cover only 12 monitored birth defects.

As a result, many conditions remain under-characterized in terms of geographic patterns and environmental exposures. These data gaps make it more difficult for healthcare systems, payers, and industry participants to prioritize resources and design condition-specific programs.

The lack of precise epidemiological information can also complicate forecasting, prevention planning, and targeted service development despite clear underlying clinical need.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| LMIC care-access gaps | -1.9% | Sub-Saharan Africa, South Asia, LMIC corridors | Long term (≥ 4 years) |

| Etiologic and data uncertainty | -1.7% | Global, stronger in emerging systems | Long term (≥ 4 years) |

| Fragmented screening pathways | -1.5% | Global, especially LMIC and mixed systems | Medium term (2-4 years) |

| Limited specialist workforce | -1.4% | LMICs, rural regions, second-tier cities | Long term (≥ 4 years) |

| Environmental risk complexity | -1.2% | Industrializing APAC, LATAM, Africa hubs | Long term (≥ 4 years) |

| Cross-lifecycle care coordination | -1.1% | North America, EU, advanced APAC | Medium term (2-4 years) |

Restraints

Severe care-access inequality restrains market growth because the highest burden of congenital disorders is concentrated in low- and middle-income countries where access to specialized diagnostics, surgery, neonatal intensive care, and pediatric specialists remains limited.

Although most children with serious congenital conditions are born in these regions, inadequate healthcare infrastructure leads to significantly higher mortality rates and reduced treatment access.

As a result, many patients die before reaching diagnosis, surgical intervention, or long-term management pathways. This creates a substantial gap between theoretical disease burden and actual healthcare utilization, reducing demand for diagnostic services, surgical procedures, medical devices, and follow-up care, particularly across Sub-Saharan Africa, South Asia, Latin America, and other underserved markets.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe care-access inequality | -2.1% | Sub-Saharan Africa, South Asia, LATAM, LMIC-wide | Long term (≥ 4 years) |

| Insurance coverage gaps and exclusions | -1.8% | India, LATAM, MENA, second-tier EU, APAC | Medium term (2-4 years) |

| Catastrophic financial burden on families | -1.6% | North America, high-cost EU, GCC, urban India | Medium term (2-4 years) |

| Surgical and specialist capacity shortfall | -1.5% | Sub-Saharan Africa, rural APAC, LATAM | Long term (≥ 4 years) |

| Unknown etiology limiting targeted care | -1.2% | Global | Long term (≥ 4 years) |

| Fragmented surveillance and registry gaps | -1.0% | LMIC-wide, rural North America, emerging APAC | Medium term (2-4 years) |

Regional Analysis

North America Dominates the Developmental Anomalies Market.

In 2025, North America led the Developmental Anomalies Market, accounting for over 38.00% share and generating revenue of US$ 2.47 Billion. The region’s dominance is driven by a well-established healthcare infrastructure, widespread adoption of advanced prenatal screening technologies, and strong presence of genetic testing laboratories and specialized pediatric care centers.

High awareness among healthcare professionals and expectant parents regarding early diagnosis of developmental disorders further strengthens regional demand. Continuous investments in research and development, along with supportive reimbursement frameworks, also contribute to the rapid uptake of innovative diagnostic solutions.

Leading hospitals and diagnostic centers in the United States and Canada are increasingly integrating AI-enabled imaging and non-invasive prenatal testing, improving diagnostic accuracy and early intervention outcomes.

Europe follows closely, supported by strong public healthcare systems, increasing focus on prenatal care, and rising adoption of advanced genetic testing. Countries such as Germany, the United Kingdom, and France invest in early screening programs and improved access to neonatal diagnostics.

Asia Pacific is emerging as the fastest-growing region due to expanding healthcare infrastructure, large patient population, and increasing awareness of congenital disorders. Latin America and Middle East and Africa show steady growth driven by improving diagnostics and maternal healthcare initiatives programs services expansion.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Player Analysis

The Developmental Anomalies Market is moderately consolidated, with a mix of global medical technology leaders and specialized dental and imaging companies competing intensely on innovation and early diagnosis solutions.

Large players such as Dentsply Sirona, Straumann Group, Zimmer Biomet, Envista Holdings, Align Technology, Medtronic, Carestream Dental, and Planmeca dominate through integrated diagnostic and treatment ecosystems. These companies focus on advanced imaging, digital orthodontics, and AI-supported diagnostic platforms to enhance early detection of developmental abnormalities.

Regional innovators like Vatech Co. and GC Corporation contribute strongly in imaging precision and biomaterials, while Ivoclar Vivadent and Shofu Inc. strengthen the materials and restorative segment. Overall competition is driven by technological differentiation, workflow efficiency, and increasing demand for minimally invasive and accurate diagnostic tools.

Competitive strategies across the market are heavily centered on R&D investment, strategic partnerships, and product innovation aimed at improving clinical outcomes. Companies such as Henry Schein Inc., Osstem Implant, and 3M Oral Care expand market reach through distribution strength, implant solutions, and advanced oral care products.

Integration of cloud-based platforms, digital dentistry workflows, and AI-assisted planning tools is becoming a key differentiator. Firms are also engaging in collaborations with hospitals, dental clinics, and research institutions to accelerate innovation pipelines.

Ecosystem-based competition is intensifying, where companies like Dentsply Sirona, Align Technology, and Envista Holdings build end-to-end digital treatment solutions, while others focus on niche advancements. This combined strategy of innovation, partnerships, and digital transformation is shaping a highly competitive and rapidly evolving market landscape.

Top Key Players

- Dentsply Sirona

- Straumann Group

- Zimmer Biomet

- Envista Holdings

- Align Technology

- GC Corporation

- Ivoclar Vivadent

- 3M Oral Care

- Medtronic

- Henry Schein Inc.

- Osstem Implant

- Planmeca

- Carestream Dental

- Vatech Co.

- Shofu Inc.

Recent Developments

- In July 2026, Zimmer Biomet unveiled a massive workforce and technological expansion plan to scale its global tech center in India. The company announced it will hire 500

highly specialized professionals over the next 3 years, dedicating the center’s focus entirely to advancing AI applications across data-driven robotics and automated

surgical planning frameworks via Reuters. - In May 2026, Dentsply Sirona Finalized an expanded regional distribution agreement with Atlanta Dental Supply to roll out its entire connected solutions portfolio, including Primescan 2 intraoral scanners andAxeos imaging suites, across the Southeast and Mid-Atlantic regions.

- In November 2025, Straumann Group, Executed the full financial takeover of Switzerland-based startup Mininavident AG, acquiring 100% of outstanding shares to secure their proprietary surgical guidance tech via Switzerland Global Enterprise. Straumann rebranded the highly precise, digitized 3D visualization and planning system to market it worldwide under the product name Straumann Falcon.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 6.50 Billion |

| Forecast Revenue (2035) | US$ 13.28 Billion |

| CAGR (2026-2035) | 7.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Anomaly Type (Craniofacial Anomalies (Cleft Lip & Palate), Dental Developmental Anomalies (Tooth agenesis, supernumerary teeth), Skeletal Jaw Anomalies, Ectodermal Dysplasia-Related Anomalies), By Diagnosis Type (Clinical Examination, Radiographic Imaging, Genetic Testing, 3D Imaging & AI-Based Diagnosis), By Treatment Type (Surgical Correction, Orthodontic Treatment, Prosthetic Rehabilitation, Regenerative & Tissue Engineering Approaches), By End User (Hospitals, Dental & Orthodontic Clinics, Academic & Research Institutes), By Age Group (Pediatric Patients, Adolescents, Adults), By Distribution Channel (Hospital Pharmacies, Specialty Clinics & Centers, Online Pharmacies, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Dentsply Sirona, Straumann Group, Zimmer Biomet, Envista Holdings, Align Technology, GC Corporation, Ivoclar Vivadent, 3M Oral Care, Medtronic, Henry Schein Inc., Osstem Implant, Planmeca, Carestream Dental, Vatech Co., Shofu Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |