Quick Navigation

- Report Overview

- Key Takeaways

- By Product Analysis

- By Antithrombotic and Anticoagulants Type Analysis

- By Application Analysis

- By End-user Analysis

- Key Market Segments

- Drivers

- Restraints

- Opportunities

- Impact of Macroeconomic / Geopolitical Factors

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

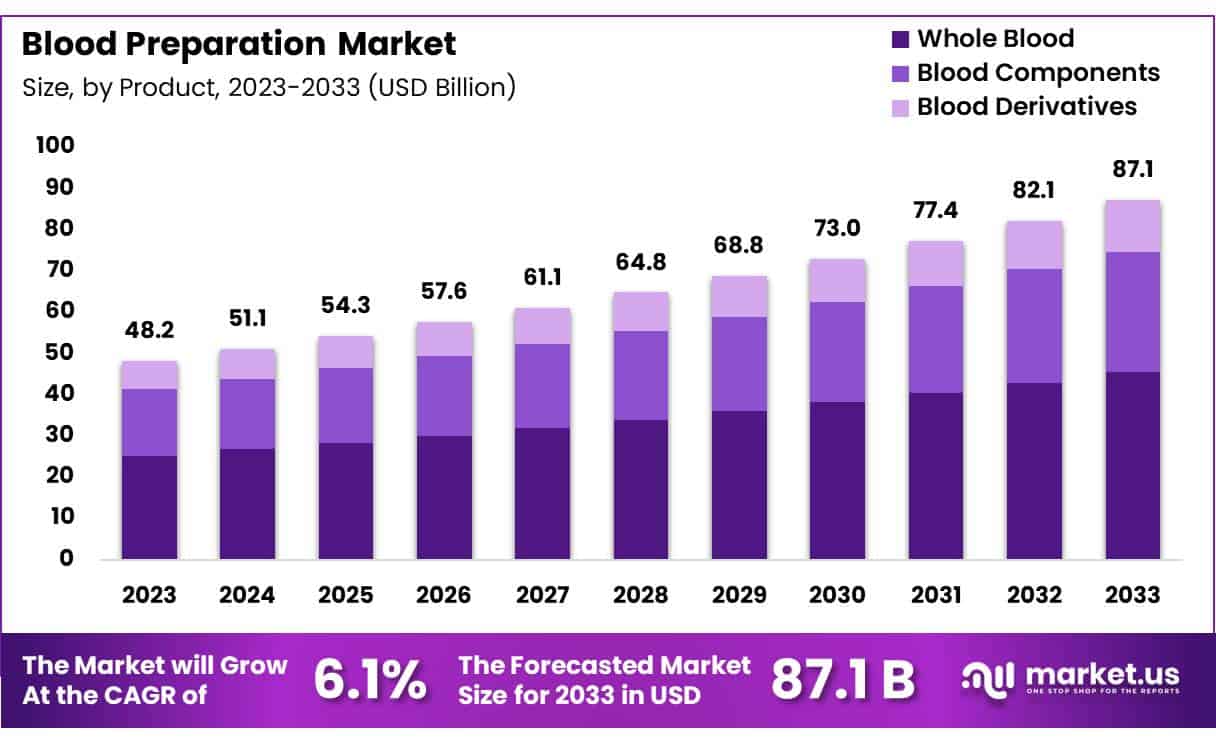

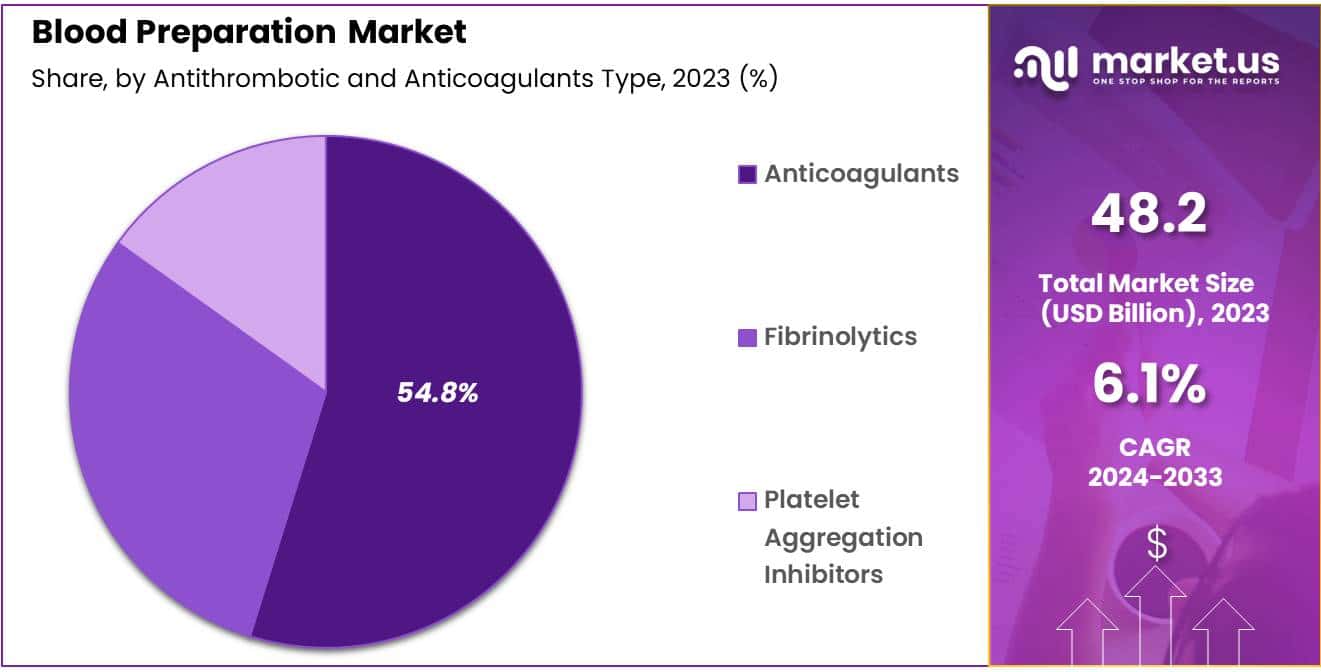

Global Blood Preparation Market size is expected to be worth around US$ 87.1 billion by 2033 from US$ 48.2 billion in 2023, growing at a CAGR of 6.1% during the forecast period 2024 to 2033.

Increasing awareness of the critical role blood preparation plays in healthcare drives significant growth in the market, particularly in applications such as transfusion medicine, surgical procedures, and emergency care. The demand for blood products, including red blood cells, platelets, and plasma, continues to rise, especially as healthcare providers emphasize the importance of safe and effective transfusions for various medical conditions.

According to the American National Red Cross, approximately 6.8 million individuals donate blood in the U.S., resulting in the collection of about 13.6 million units of red blood cells and whole blood each year. This robust donation framework highlights the importance of maintaining an adequate blood supply for patients in need.

In September 2021, the American Red Cross launched a national initiative aimed at increasing donor participation, particularly to enhance health outcomes for patients with sickle cell disease. This initiative reflects a growing focus on addressing specific health challenges through targeted blood donation campaigns.

Additionally, advancements in blood processing and storage technologies contribute to extended shelf life and improved safety of blood products, further enhancing their availability for clinical use. The rising prevalence of chronic diseases and an aging population also create opportunities for expanding blood preparation services. As the market continues to evolve, ongoing innovations and strategic initiatives will play a crucial role in meeting the increasing demand for blood products and improving patient care.

Key Takeaways

- Market Size: Global Blood Preparation Market size is expected to be worth around US$ 87.1 billion by 2033 from US$ 48.2 billion in 2023.

- Market Growth: The market growing at a CAGR of 6.1% during the forecast period 2024 to 2033.

- Product Analysis: The whole blood segment led in 2023, claiming a market share of 52.3% owing to the increasing demand for transfusions in critical care settings.

- Antithrombotic and Anticoagulants Type Analysis: The anticoagulants held a significant share of 54.8% as the prevalence of thromboembolic disorders continues to rise.

- Application Analysis: The thrombocytosis segment had a tremendous growth rate, with a revenue share of 40.8%

- End-Use Analysis: The hospitals segment grew at a substantial rate, generating a revenue portion of 60.7%

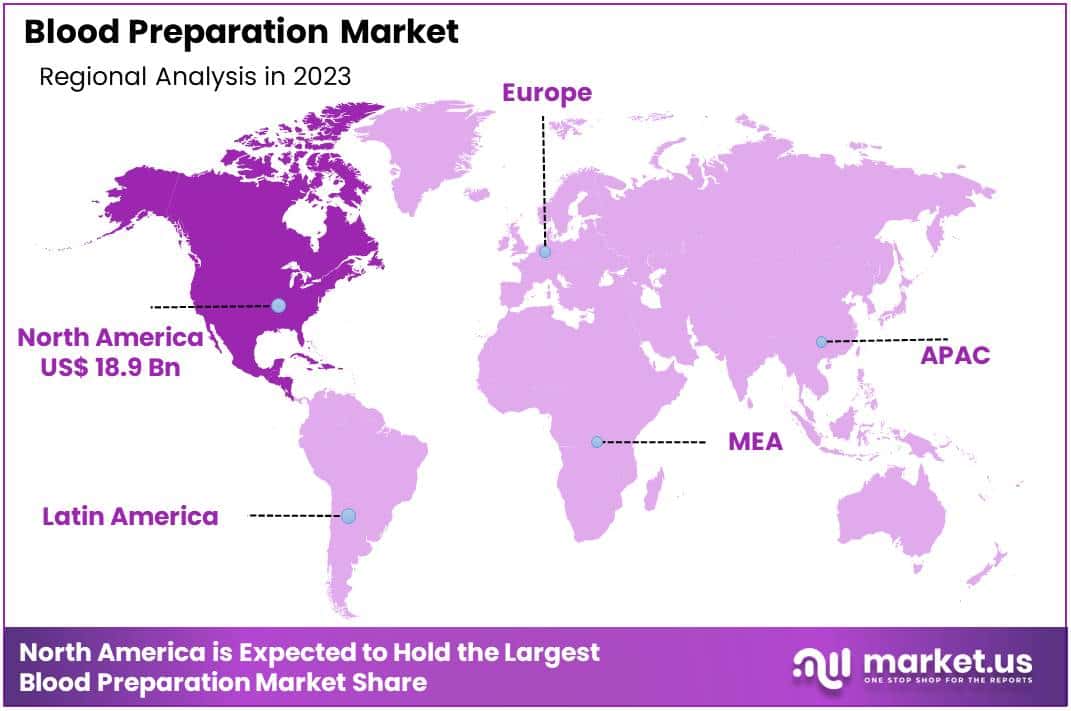

- Regional Analysis: North America dominated the market with the highest revenue share of 39.2%

By Product Analysis

The whole blood segment led in 2023, claiming a market share of 52.3% owing to the increasing demand for transfusions in critical care settings. Whole blood is crucial for patients undergoing major surgeries, trauma care, and treatment of various hematological disorders, making it an essential component in hospital protocols. The rising incidence of accidents and the growing prevalence of chronic diseases requiring frequent transfusions are likely to bolster the demand for whole blood products.

Additionally, advancements in blood collection and storage techniques are anticipated to improve the safety and availability of whole blood for transfusion. As awareness of the importance of timely blood supply in emergency situations grows, healthcare institutions are projected to enhance their blood donation drives, further promoting the whole blood segment. Consequently, the focus on comprehensive patient care is expected to solidify the position of whole blood within the overall blood preparation market.

By Antithrombotic and Anticoagulants Type Analysis

The anticoagulants held a significant share of 54.8% as the prevalence of thromboembolic disorders continues to rise. Anticoagulants play a critical role in preventing and treating conditions such as deep vein thrombosis, pulmonary embolism, and stroke, which are becoming increasingly common in aging populations.

The increasing adoption of anticoagulant therapies in clinical practice is likely to drive demand, particularly for novel anticoagulants that offer improved safety profiles and convenience over traditional options. Furthermore, ongoing research and development aimed at enhancing the efficacy of anticoagulants are expected to contribute to this segment’s growth.

The shift toward preventive care, where anticoagulants are used proactively to mitigate the risk of thrombotic events, is anticipated to further bolster market expansion. Overall, the anticoagulants segment is poised to play a vital role in the evolving landscape of blood preparation and management.

By Application Analysis

The thrombocytosis segment had a tremendous growth rate, with a revenue share of 40.8% owing to the increasing recognition of the condition’s impact on overall health. Thrombocytosis, characterized by elevated platelet levels, can lead to serious complications such as pulmonary embolism and cardiovascular issues, thereby raising the demand for effective treatment options. The rising prevalence of risk factors associated with thrombocytosis, including obesity and sedentary lifestyles, is likely to contribute to this trend.

Furthermore, advancements in diagnostic technologies are anticipated to enhance early detection and treatment of thrombocytosis, improving patient outcomes and increasing the demand for blood preparation products tailored to this condition. As healthcare providers continue to prioritize comprehensive management of thrombotic risks, the thrombocytosis segment is projected to play a critical role in the overall blood preparation market.

By End-user Analysis

The hospitals segment grew at a substantial rate, generating a revenue portion of 60.7% due to their critical role in patient care and management. Hospitals are expected to increasingly rely on blood components for various medical procedures, including surgeries, trauma care, and treatments for hematological disorders. The rising incidence of chronic diseases requiring regular transfusions and advanced therapies is likely to drive significant demand for blood preparation products within hospital settings.

Additionally, the growing emphasis on improving patient outcomes and reducing complications associated with blood transfusions will further solidify the importance of hospitals in this market. As healthcare facilities invest in enhancing their blood supply chains and transfusion protocols, the hospitals segment is anticipated to expand significantly.

Furthermore, collaborations between hospitals and blood banks are expected to streamline operations and ensure a consistent supply of blood products, reinforcing the hospitals’ position in the blood preparation market.

Key Market Segments

By Product

- Blood Components

- Whole Blood

- Blood Derivatives

By Antithrombotic Anticoagulants Type

- Fibrinolytics

- Platelet Aggregation Inhibitors

- Anticoagulants

By Application

- Thrombocytosis

- Pulmonary Embolism

- Renal Impairment

- Angina Blood Vessel Complications

- Others

By End-user

- Hospitals

- Research Labs

- Diagnostic Centers

- Blood Banks

Drivers

Growing Introduction of Blood and Cell-Based Therapies Drives Market Growth

Increasing introduction of new blood and cell-based therapies significantly drives the blood preparation market. Recent advancements in medical research and technology have led to innovative treatment options that utilize blood components for therapeutic purposes. In May 2023, NYBC Ventures launched as one of the first venture funds dedicated solely to advancing new blood and cell-based therapies, backed by a $50 million investment from the New York Blood Center.

This influx of funding is expected to foster the development of novel therapies, enhancing the efficacy and range of blood products available. As researchers and companies focus on creating targeted therapies that leverage the unique properties of blood and cell components, the demand for effective blood preparation processes will likely surge. Consequently, the market is anticipated to experience robust growth as healthcare providers increasingly adopt these advanced therapies to improve patient outcomes.

Restraints

Risk of Blood-Borne Infections Restraints Market Expansion

High levels of concern regarding the risk of blood-borne infections restrain the growth of the blood preparation market. Many patients express apprehension about the potential transmission of infections through blood products, which can lead to hesitance in accepting transfusions or therapies. This fear can impede the overall acceptance of blood-based treatments, as healthcare providers may be cautious in recommending these options to patients.

Additionally, regulatory bodies impose stringent safety standards and testing requirements for blood products, further complicating the preparation and distribution processes. The continuous risk of infections is expected to hamper the growth of the market, prompting manufacturers to invest in enhanced testing and purification technologies to ensure safety and boost consumer confidence in blood-derived therapies.

Opportunities

Rising Number of Heart Surgeries Creates Opportunities

Rising number of heart surgeries presents significant opportunities for the blood preparation market. The demand for blood products increases as surgical procedures involving the heart often require substantial transfusions to manage blood loss and maintain hemodynamic stability.

According to the German Heart Surgery Report 2022, the total number of heart surgical procedures rose from 92,838 in 2021 to 93,913 in 2022, reflecting a growing need for surgical interventions. As healthcare providers perform more heart surgeries, they will require reliable access to high-quality blood products and components to ensure optimal patient outcomes.

This trend is expected to drive demand for effective blood preparation solutions, enabling manufacturers to innovate and expand their offerings in response to the evolving needs of the cardiac care sector. As the volume of heart surgeries continues to rise, the blood preparation market is likely to thrive in parallel, bolstered by increasing clinical needs.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly impact the market for blood processing and storage solutions. Economic downturns often lead to budget cuts in healthcare spending, which can restrict access to essential blood products and technologies. Fluctuations in currency exchange rates may increase the costs associated with importing specialized equipment, further complicating supply chain logistics. Geopolitical tensions can disrupt international collaborations and trade, potentially leading to shortages in critical supplies.

However, rising awareness of the importance of blood safety and the increasing prevalence of chronic diseases create substantial demand for advanced blood preparation techniques. Additionally, government initiatives aimed at improving healthcare infrastructure contribute to market growth. Overall, despite the challenges posed by economic and geopolitical factors, the commitment to enhancing patient care through improved blood processing methods presents a positive outlook for the industry.

Latest Trends

Impact of Lab-Based Treatments on the Blood Preparation Market

Growing interest in lab-based treatments is projected to drive significant growth in the market for blood processing solutions. As researchers explore innovative techniques, the demand for advanced blood products increases, especially for unique medical applications. This trend encourages investment in research and development, leading to breakthroughs in blood preparation technologies.

For example, in November 2022, the NIHR Blood and Transplant Research Unit initiated the RESTORE clinical trial (REcovery and survival of STem cell Originated REd cells). Researchers noted that if this trial proves the effectiveness and safety of lab-grown red blood cells, it could revolutionize treatment options for individuals with rare blood types. As the market sees a surge in lab-based innovations, industry players are likely to expand their offerings and enhance the quality of blood products, ultimately improving patient outcomes.

Regional Analysis

North America is leading the Blood Preparation Market

North America dominated the market with the highest revenue share of 39.2% owing to a multitude of factors that underscore the critical demand for blood products. The increasing incidence of chronic diseases, traumatic injuries, and surgical procedures has heightened the need for blood transfusions. According to the American National Red Cross, a person in the United States requires blood or platelets every two seconds, necessitating around 29,000 units of red blood cells, 6,500 units of plasma, and 5,000 units of platelets daily.

This staggering demand translates to approximately 16 million blood components being transfused annually. Additionally, advancements in blood processing technologies have improved the safety, efficacy, and shelf life of blood products, enhancing the overall management of blood banks. The rising awareness about the importance of blood donations and various initiatives to encourage public participation have also contributed to an increase in available blood supply.

Furthermore, the growing emphasis on developing innovative blood substitutes and regenerative medicine is expected to bolster market growth. Collectively, these dynamics have created a thriving environment for the blood preparation market in North America.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

In the Asia Pacific region, the blood preparation market is projected to experience substantial growth during the forecast period. The rising demand for blood products is driven by an increasing incidence of chronic diseases, accidents, and a growing population that necessitates blood transfusions. In June 2023, the Indian Health Ministry reported that the country requires an average of 14.6 million blood units annually, highlighting the significant need for blood components.

According to the Press Information Bureau (PIB), someone in India requires blood every two seconds, with one in every three Indians likely to need blood at some point in their lives. This alarming trend underscores the urgent need for efficient blood collection and preparation systems.

Furthermore, improving healthcare infrastructure and increasing awareness about blood donation are anticipated to enhance blood availability in the region. As governments and organizations continue to focus on strengthening blood transfusion services and implementing advanced processing techniques, the blood preparation market in Asia Pacific is expected to flourish, driven by both demand and innovation in the sector.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The major players in the blood preparation market are actively engaged in the development and introduction of innovative products, as well as implementing strategic initiatives aimed at enhancing their competitive positioning. Key players in the blood preparation market focus on enhancing product quality and expanding their service offerings to drive growth. They invest in advanced technologies and processes, such as automated blood processing systems and pathogen reduction techniques, which improve safety and efficiency in blood handling.

Establishing strategic partnerships with hospitals and healthcare organizations enables them to broaden their distribution networks and ensure better access to their products. Companies actively pursue regulatory compliance and quality certifications to build trust and maintain a strong reputation within the industry. Additionally, they concentrate on geographic expansion into emerging markets, adapting their strategies to meet local healthcare demands and improve blood management practices.

Top Key Players

- Terumo Blood and Cell Technologies

- Sanofi

- Pfizer, Inc.

- Leo Pharma A/S

- GlaxoSmithKline PLC

- EryPharm

- Celgene Corp.

- Bristol-Myers Squibb Company

- Baxter International Inc

- AstraZeneca plc

Recent Developments

- In February 2023, Terumo Blood and Cell Technologies announced that its IMUGARD WB Platelet Pooling Set received FDA clearance and was officially launched. This innovative platelet pooling set extends the shelf life of whole blood-derived platelets from 5 to 7 days, making IMUGARD the first platelet pooling set approved for 7-day storage in the United States. This advancement is expected to significantly enhance the blood preparation market by increasing the availability and usability of platelets, ultimately improving patient outcomes in transfusion medicine.

- In April 2021, EryPharm introduced a medical device designed to manufacture cultured red blood cells in large quantities, aiming to create new sources of blood for transfusions. This innovative approach addresses the critical need for safe and sufficient blood supplies, supporting the growth of the blood preparation market by providing alternatives to traditional blood donation methods. The development of such technologies is essential for meeting increasing demand and enhancing the efficiency of blood preparation processes.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 48.2 billion |

| Forecast Revenue (2033) | USD 87.1 billion |

| CAGR (2024-2033) | 6.1% |

| Base Year for Estimation | 2023 |

| Historic Period | 2018-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Blood Components, Whole Blood, and Blood Derivatives), By Antithrombotic and Anticoagulants Type (Fibrinolytics, Platelet Aggregation Inhibitors, and Anticoagulants), By Application (Thrombocytosis, Pulmonary Embolism, Renal Impairment, Angina Blood Vessel Complications, and Others), By End-user (Hospitals, Research Labs, Diagnostic Centers, and Blood Banks) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Terumo Blood and Cell Technologies , Sanofi, Pfizer, Inc., Leo Pharma A/S, GlaxoSmithKline PLC, EryPharm , Celgene Corp., Bristol-Myers Squibb Company, Baxter International Inc, and AstraZeneca plc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |