Quick Navigation

Market Overview

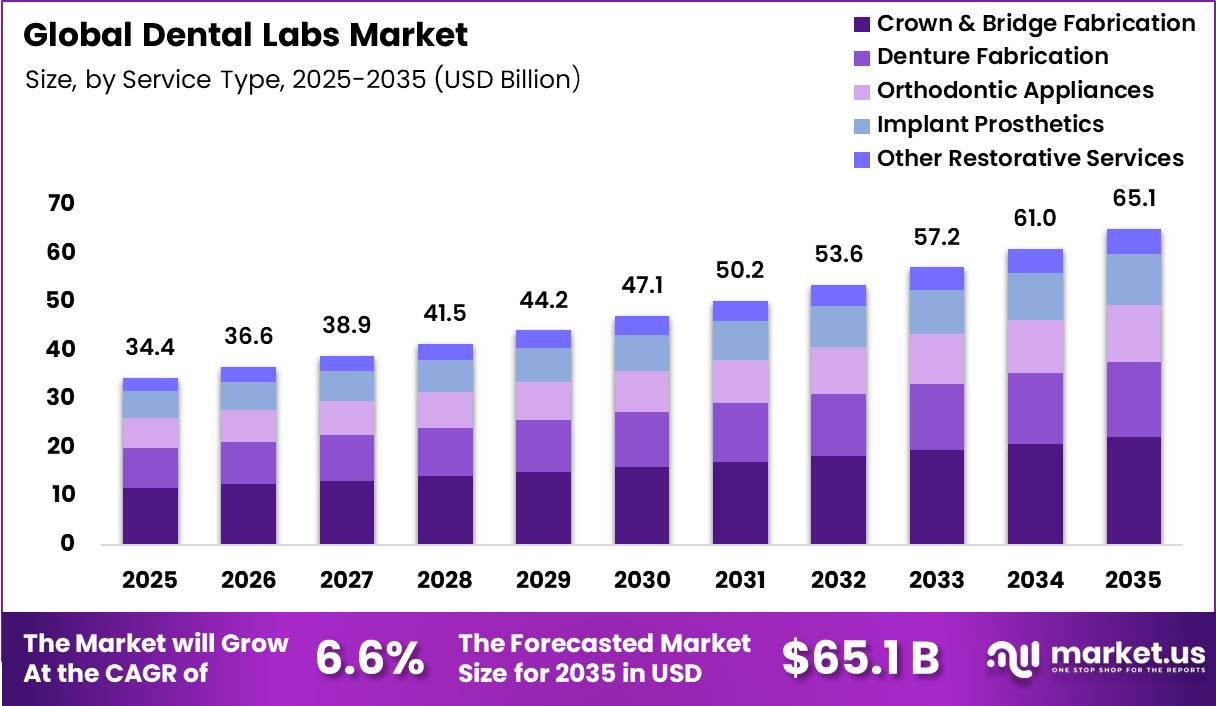

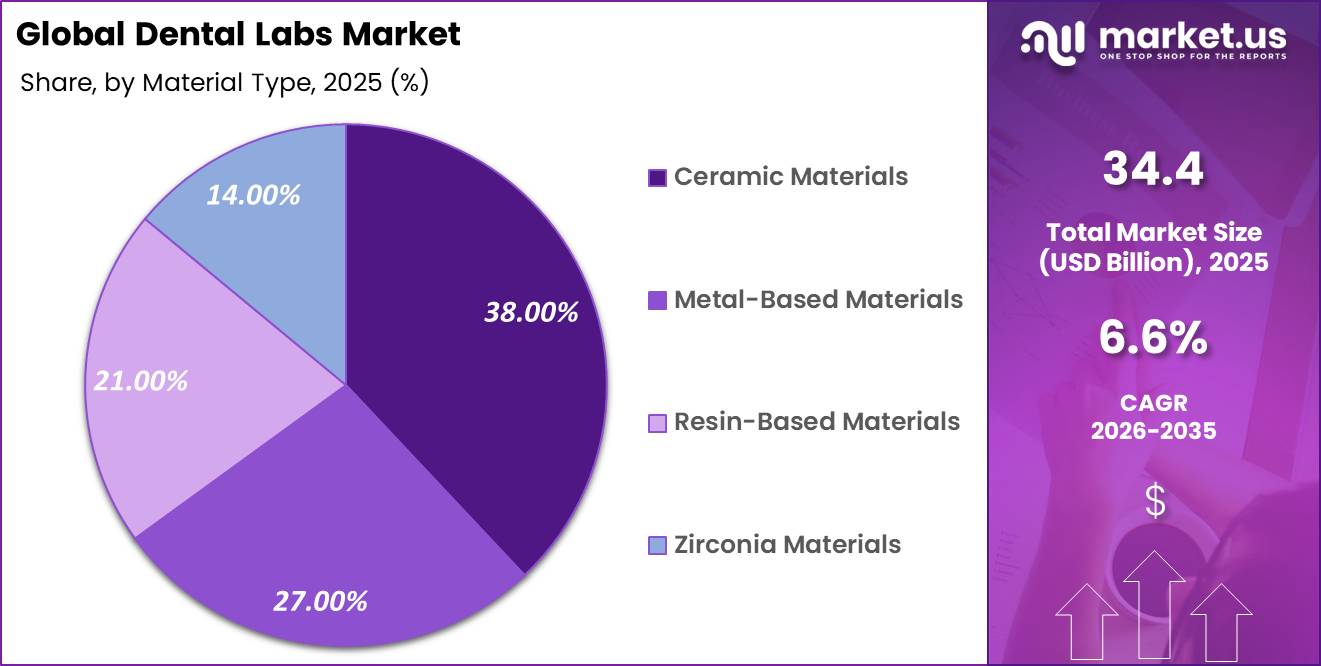

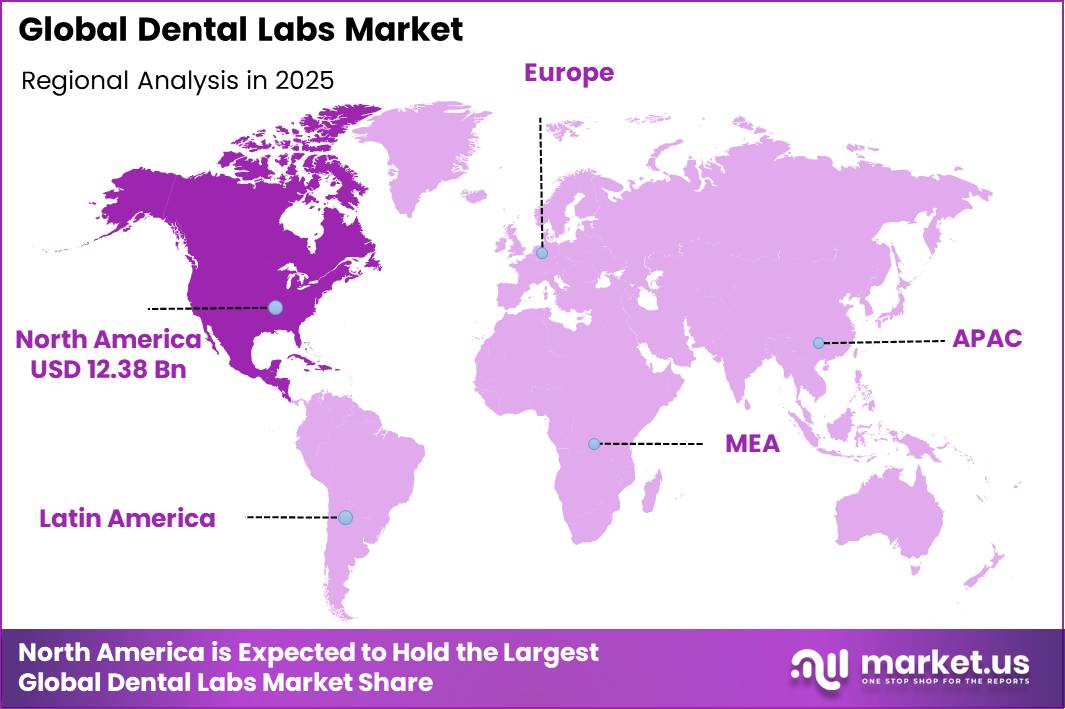

Global Dental Labs Market size is expected to be worth around US$ 65.1 Billion by 2035 from US$ 34.4 Billion in 2025, growing at a CAGR of 6.6% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 36.00% share with a revenue of US$ 12.38 Billion.

The Dental Labs Market plays a critical role in global oral health by manufacturing customised dental prosthetics, such as crowns, bridges, dentures, and orthodontic devices, based on a dentist’s prescription. These services support restorative and prosthetic dentistry, an essential part of dental care given the high burden of oral disease worldwide. Globally, oral diseases affect nearly 3.7 billion people, including widespread untreated cavities and periodontal disease, underscoring persistent dental care needs and prosthetic demand.

Dental laboratories are integral to indirect dental restorations, which are fabricated outside the mouth and later fitted by dentists, improving function, patient comfort, and aesthetics across age groups. Independent public health data from the Centres for Disease Control and Prevention show that dental conditions remain prevalent. 46% of U.S. children aged 2–19 years have untreated or restored caries, and over 20% of adults 65+ experience untreated decay, highlighting ongoing restorative needs met by dental labs.

National initiatives also reflect this need. In India, the National Oral Health Programme aims to expand integrated oral care services and awareness, addressing gaps in prevention and treatment across communities. Indirect restorations, such as custom-made crowns and dentures, remain foundational in modern dentistry, directly linking the dental labs sector to public health outcomes and patient quality of life as global oral disease burdens persist.

Key Takeaways

- Market Size: The Global Dental Labs Market size was US$ 34.4 billion in 2025. The market is estimated to grow to US$ 65.1 billion by 2035.

- Market Share: The Compound Annual Growth Rate (CAGR) of the market from 2026 to 2035 will be 6.6%.

- Service Type: Crown & Bridge Fabrication has the largest market share, accounting for 34% of total service type revenue.

- Material Type: Ceramic Materials leads the segment, accounting for 38% of total material type revenue.

- Technology: Conventional Laboratory Methods dominates the segment, accounting for 54% of total technology revenue.

- Application: Restorative Dentistry leads the segment, accounting for 42% of total application revenue.

- Lab Type: Independent Dental Laboratories dominates the segment, accounting for 58% of total lab type revenue.

- End User: Dental Clinics lead the segment, accounting for 67% of total end-user revenue.

- Regional: North America is the dominant regional market, accounting for 36% of global revenue.

Service Type Analysis

The Dental Labs Market is primarily segmented by service type into Crown & Bridge Fabrication, Denture Fabrication, Orthodontic Appliances, Implant Prosthetics, and Other Restorative Services. Crown & Bridge Fabrication dominates the market with a 34.00% share in 2025, driven by the rising prevalence of tooth decay, trauma cases, and ageing populations requiring fixed restorative solutions. These services remain the backbone of dental laboratories due to high procedural frequency and strong demand for aesthetic and functional restoration.

Denture Fabrication accounts for 24.00%, supported by increasing edentulism among elderly populations and growing demand for removable prosthetics. Orthodontic Appliances hold 18.00%, fueled by rising orthodontic treatments, especially among adolescents and adults seeking corrective and cosmetic alignment solutions.

Implant Prosthetics represent 16.00%, expanding rapidly due to increasing adoption of dental implants as a long-term replacement solution for missing teeth. Meanwhile, Other Restorative Services contribute 8.00%, including veneers, inlays, onlays, and custom prosthetic adjustments. The overall segmentation reflects a balanced demand between fixed and removable restorations, with crown and bridge solutions continuing to lead due to their cost-effectiveness and widespread clinical application across global dental practices.

Material Type Analysis

The Dental Labs Market by material type is segmented into Ceramic Materials, Metal-Based Materials, Resin-Based Materials, and Zirconia Materials. Ceramic Materials dominate the market with a 38.00% share in 2025, largely due to their superior aesthetics, biocompatibility, and natural tooth-like appearance, making them highly preferred for crowns, veneers, and bridges.

Metal-Based Materials account for 27.00%, driven by their exceptional strength, durability, and long-term performance in load-bearing restorations, particularly in posterior teeth applications. Resin-Based Materials hold a 21.00% share and are widely used in dentures, temporary restorations, and orthodontic appliances due to their flexibility, cost-effectiveness, and ease of processing.

Zirconia Materials represent 14.00% of the market and are experiencing rapid adoption owing to their high strength, fracture resistance, and improved aesthetic outcomes compared to traditional metals. The material segmentation highlights a shift toward advanced aesthetic solutions, particularly ceramics and zirconia, as patients increasingly demand natural-looking restorations.

However, metal-based and resin-based materials continue to play a crucial role in functional and economical dental solutions. Overall, material innovation is a key driver shaping laboratory workflows, with CAD/CAM compatibility further enhancing precision and efficiency across all material categories in modern dental labs.

Technology Analysis

The Dental Labs Market is segmented by technology into Conventional Laboratory Methods, CAD/CAM Systems, and 3D Printing Technology. Conventional Laboratory Methods dominate with a 54.00% share in 2025, as many dental labs, particularly in developing regions, continue to rely on traditional casting, moulding, and manual fabrication techniques due to lower setup costs and established workflows. However, this segment is gradually declining as digital transformation accelerates.

CAD/CAM Systems account for 31.00% of the market and are witnessing strong growth, driven by their ability to deliver high precision, faster turnaround times, and improved customisation in prosthetic design. These systems significantly reduce human error and material wastage, making them increasingly essential in modern dental laboratories.

3D Printing Technology holds a 15.00% share, but it is one of the fastest-growing segments due to its ability to produce complex dental structures with high accuracy and reduced production time. It is widely used in aligners, surgical guides, crowns, and models. The overall technological landscape reflects a transition from manual craftsmanship to digital dentistry, with hybrid workflows becoming common. This evolution is improving productivity, scalability, and patient-specific customisation in dental restorative solutions globally.

Application Analysis

The Dental Labs Market by application is segmented into Restorative Dentistry, Prosthodontics, Orthodontics, and Implantology. Restorative Dentistry dominates the market with a 42.00% share in 2025, driven by the high global burden of dental caries, trauma-related tooth damage, and the growing need for functional and aesthetic tooth restoration. This segment includes crowns, bridges, fillings, and other restorative procedures that form the core output of dental laboratories.

Prosthodontics accounts for 24.00%, supported by increasing demand for full and partial dentures, especially among ageing populations experiencing tooth loss. Orthodontics holds 19.00%, fueled by rising awareness of dental aesthetics, increased adoption of aligners, and expanding orthodontic treatments among both adolescents and adults.

Implantology represents 15.00% of the market and is expanding rapidly due to the growing preference for permanent tooth replacement solutions and advancements in implant-supported prosthetics. The segmentation highlights a strong emphasis on restorative and prosthetic solutions, which together account for the majority of dental lab demand. Increasing patient awareness, improved dental insurance coverage in several regions, and technological advancements are further strengthening application diversity within dental laboratories worldwide.

Lab Type Analysis

The Dental Labs Market by lab type is segmented into Independent Dental Laboratories, In-House Dental Clinic Labs, and Corporate Laboratory Networks. Independent Dental Laboratories dominate with a 58.00% market share in 2025, as they provide specialised, cost-effective, and flexible services to a wide range of dental clinics. These labs are particularly prevalent in developing regions where outsourcing remains the most economical model for prosthetic fabrication.

In-House Dental Clinic Labs account for 24.00%, driven by clinics seeking faster turnaround times, improved workflow integration, and greater control over customisation and patient-specific requirements. The adoption of digital dentistry tools such as CAD/CAM systems has significantly supported the growth of in-house labs.

Corporate Laboratory Networks hold 18.00% of the market and are expanding steadily due to consolidation trends, standardised production processes, and economies of scale. These networks often invest heavily in advanced technologies, automation, and centralised production facilities to serve large dental service organisations.

Overall, the segmentation reflects a hybrid operational structure where independent labs remain dominant, but in-house and corporate models are gaining traction due to technological advancement and increasing demand for faster, more precise dental restoration services.

End User Analysis

The Dental Labs Market by end user is segmented into Dental Clinics, Hospitals, and Academic & Research Institutes. Dental Clinics dominate the market with a 67.00% share in 2025, as they represent the primary point of service delivery for restorative and prosthetic dental procedures. Clinics frequently outsource dental laboratory work for crowns, bridges, dentures, and orthodontic appliances, making them the largest consumers of lab services globally.

Hospitals account for 18.00%, driven by the increasing integration of dental departments within multi-speciality healthcare systems and the growing demand for complex oral surgeries and implant-based restorations. Hospitals typically handle advanced cases requiring multidisciplinary care and high-precision prosthetic solutions.

Academic & Research Institutes represent 15.00% of the market, contributing through dental education, clinical training, and innovation in biomaterials and prosthetic technologies. These institutions also play a key role in advancing digital dentistry and developing new fabrication techniques.

Overall, the segmentation highlights the strong dependence of dental laboratories on outpatient clinical demand, while hospitals and academic institutions provide specialised and innovation-driven contributions. Rising oral health awareness, increasing dental tourism, and improved access to dental care are further strengthening demand across all end-user categories globally.

Key Market Segments

By Service Type

- Crown & Bridge Fabrication

- Denture Fabrication

- Orthodontic Appliances

- Implant Prosthetics

- Other Restorative Services

By Material Type

- Ceramic Materials

- Metal-Based Materials

- Resin-Based Materials

- Zirconia Materials

By Technology

- Conventional Laboratory Methods

- CAD/CAM Systems

- 3D Printing Technology

By Application

- Restorative Dentistry

- Prosthodontics

- Orthodontics

- Implantology

By Lab Type

- Independent Dental Laboratories

- In-House Dental Clinic Labs

- Corporate Laboratory Networks

By End User

- Dental Clinics

- Hospitals

- Academic & Research Institutes

Drivers

Digital workflow standardisation is a major driver for dental laboratories as it shifts production from manual, artisanal processes to scalable, software-enabled workflows. The FDI digital dentistry policy calls for standards that ensure quality, safety, effectiveness, interoperability, and consistency across digital dental systems. It also recommends integrating digital dentistry into undergraduate, postgraduate, and continuing professional education, reinforcing its role as core industry infrastructure.

Standardised workflows enable consistent management of file validation, bite registration, design approvals, and manufacturing processes across different scanners, CAD platforms, and production systems. This reduces manual errors and improves process reliability.

Laboratories benefit from lower remake rates, faster case turnaround, and improved production visibility. Standardisation also supports efficient multicenter operations and helps laboratories meet the demands of DSOs and other high-volume dental practices.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital workflow standardisation | +2.4% | North America, EU, Japan, Korea, ANZ | Medium term (2-4 years) |

| FDA-cleared printed restorations | +2.1% | North America core, EU spill-over, advanced APAC | Short term (≤ 2 years) |

| Intraoral scan-to-lab transfer | +1.9% | North America, EU, urban APAC, GCC | Short term (≤ 2 years) |

| CAD/CAM productivity scaling | +1.7% | Global digital dentistry corridors | Medium term (2-4 years) |

| Training-led technician upskilling | +1.5% | North America, EU, India, SEA, LATAM | Long term (≥ 4 years) |

| Secure data and interoperability demand | +1.4% | Global regulated digital markets | Long term (≥ 4 years) |

Challenges

Technician digital skills gaps remain a major challenge for dental laboratories as digital workflows become increasingly complex. Modern labs require expertise in CAD design, scanner-file interpretation, additive manufacturing workflows, materials processing, and digital quality assurance.

The FDI digital dentistry policy calls for comprehensive digital dentistry education across undergraduate, postgraduate, and professional training programs, while also noting that digital dentistry has not yet been fully integrated into many dental schools. This highlights an ongoing shortage of professionals with advanced digital-laboratory skills. Even with investments in scanners, mills, 3D printers, and software platforms, output quality still depends heavily on skilled technicians.

Critical tasks such as margin design, occlusion management, print orientation, post-processing, and case communication require specialised expertise. As a result, laboratories often invest in internal training programs, vendor certifications, and supervised workflows to maintain quality standards. The skills gap continues to limit productivity gains and can slow the conversion of technology investments into operational capacity growth.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Technician digital skills gap | -1.8% | North America, EU, India, SEA, LATAM | Long term (≥ 4 years) |

| Software interoperability friction | -1.6% | Global digital dentistry markets | Medium term (2-4 years) |

| 3D print validation burden | -1.5% | North America, EU, advanced APAC | Medium term (2-4 years) |

| Data governance complexity | -1.3% | EU, North America, and regulated APAC | Long term (≥ 4 years) |

| Remake risk in scan workflows | -1.2% | North America, EU, urban APAC | Short term (≤ 2 years) |

| High capex utilization pressure | -1.1% | Small and mid-sized labs globally | Medium term (2-4 years) |

Restraints

Print validation overhead is a significant restraint for dental laboratories adopting advanced 3D printing workflows. FDA guidance for 3D-printed medical devices outlines a complex process involving device design, software workflows, material controls, printing, post-processing, verification, testing, and process validation. The guidance also states that when critical functional characteristics, such as mechanical strength, cannot be inspected on every individual device, the manufacturing process itself must be validated before production.

For dental labs, this creates additional requirements for material traceability, build-orientation control, support-structure management, cure-cycle consistency, batch monitoring, and detailed documentation. New printed applications often require both destructive and non-destructive testing procedures to demonstrate reliability.

These validation activities demand specialised expertise, additional labour, and greater quality-management resources. As a result, many small and mid-sized laboratories may delay adopting new 3D-printed indications despite growing market demand, due to the operational and compliance burden associated with validation requirements.

| Restraint | Geographic Relevance | Impact Timeline |

|---|---|---|

| High digital capex burden | Global, strongest in small and mid-sized labs | Medium term (2-4 years) |

| Print validation overhead | North America, EU, advanced APAC | Medium term (2-4 years) |

| Interoperability lock-in | Global digital dentistry markets | Long term (≥ 4 years) |

| Data compliance cost load | EU, North America, and regulated APAC | Long term (≥ 4 years) |

| Uneven workforce readiness | North America, EU, India, SEA, LATAM | Long term (≥ 4 years) |

| Remake and rework erosion | North America, EU, urban APAC | Short term (≤ 2 years) |

Opportunity

Lab-as-a-service workflows represent a significant opportunity for dental laboratories to move beyond traditional manufacturing and become end-to-end digital workflow partners for clinics. The FDI digital dentistry policy highlights the need for user-friendly digital technologies, interoperable standards, secure data-management frameworks, and formal digital dentistry education, indicating that many practices still lack advanced workflow capabilities. This creates demand for laboratories that can manage scan validation, bite-data correction, case triage, digital design services, shade libraries, and production coordination.

By offering workflow management rather than only producing crowns, bridges, aligners, or prosthetics, labs can help clinics reduce administrative burden and improve treatment efficiency. Additional services such as remake analytics, turnaround-time guarantees, and design subscriptions can further strengthen clinic relationships.

These workflow platforms can increase customer retention by embedding laboratories more deeply into clinical operations. As a result, labs can generate recurring digital-service revenue while improving productivity and value capture from existing case volumes.

| Opportunity | Geographic Relevance | Execution Window |

|---|---|---|

| Lab-as-a-service workflows | North America, EU, Japan, Korea, ANZ | Short term (≤ 2 years) |

| Chairside-lab hybrid networks | North America core, EU, urban APAC | Medium term (2-4 years) |

| 3D printed speciality production | North America, EU, China, advanced APAC | Medium term (2-4 years) |

| Cloud design outsourcing hubs | India, SEA, Eastern Europe, LATAM | Short term (≤ 2 years) |

| Interoperability software monetisation | Global digital dentistry markets | Long term (≥ 4 years) |

| Roll-up of analogue independents | North America, the EU, and Japan | Long term (≥ 4 years) |

Regional Analysis

In 2025, North America led the market, achieving over 36.00% share with a revenue of US$ 12.38 billion. The global dental labs market shows distinct regional variations driven by healthcare infrastructure, reimbursement policies, ageing populations, and the adoption of digital dentistry technologies.

North America dominates the market due to strong dental insurance coverage, high awareness of oral health, and advanced adoption of CAD/CAM systems, 3D printing, and digital impression technologies. The United States leads the region with a large number of dental laboratories and high demand for cosmetic and restorative procedures, supported by an ageing population requiring crowns, bridges, and implants.

Europe holds a significant share, driven by well-established public healthcare systems, an increasing geriatric population, and strong regulatory standards for dental materials and prosthetics. Countries like Germany, the UK, and France are key contributors, with growing integration of digital workflows in dental labs.

Asia-Pacific is the fastest-growing region due to rising dental tourism, an expanding middle-class population, and increasing awareness of oral aesthetics. Countries such as China, India, Japan, and South Korea are witnessing rapid growth in dental clinics and lab outsourcing services.

Latin America shows steady growth, supported by improving healthcare access and rising demand for affordable dental prosthetics. Meanwhile, the Middle East & Africa region is gradually expanding, driven by healthcare investments, urbanisation, and increasing adoption of private dental services, particularly in Gulf countries.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Player Analysis

Suppliers in the global dental labs market seek a competitive advantage through digital fabrication technology investment encompassing CAD/CAM milling systems, 3D printing platforms, and intraoral scanning integration alongside a material portfolio breadth spanning ceramic, zirconia, resin, and metal-based restoration systems serving restorative, prosthetic, orthodontic, and implant applications.

Key strategic focus areas include automation-driven production efficiency improvement, digital workflow integration with dental clinic chairside scanning systems enabling same-day turnaround capabilities, and geographic network expansion through independent laboratory acquisitions, enabling corporate consolidation of fragmented regional markets.

Companies continue investing in certified dental technician training, ISO and FDA quality management compliance, and proprietary digital design software platforms to secure long-term supply agreements with dental clinic chains, hospital dental departments, and dental service organisation procurement programs globally.

The progressive shift from conventional manual methods toward fully digital CAD/CAM and additive manufacturing workflows is simultaneously improving production precision, reducing material waste, and enabling remote case design capabilities that allow laboratory networks to centralise fabrication while maintaining geographically distributed case reception and delivery infrastructure through the forecast period to 2035.

Top Key Players

- National Dentex Labs

- Envista Holdings Corporation

- Modern Dental Group Limited

- Glidewell Laboratories

- Dentsply Sirona

- Henry Schein Inc.

- Straumann Group

- 3M Oral Care

- Ivoclar Vivadent AG

- GC Corporation

- Kulzer GmbH

- VITA Zahnfabrik H. Rauter GmbH & Co. KG

- Shofu Inc.

- Argen Corporation

- DDS Lab

Recent Developments

- In January 2026, Dentsply Sirona expanded its CAD/CAM digital dentistry platform integration with major US dental service organisation networks, enabling same-day crown fabrication workflows across over 3,200 affiliated clinic locations.

- In February 2026, Straumann Group acquired a leading independent dental laboratory network in Germany, adding 12 fabrication centres to its European corporate laboratory operations, targeting growing implant prosthetics and zirconia restoration demand.

- In March 2026, Glidewell Laboratories launched its next-generation 3D printing-based denture fabrication platform across its North American production facilities, reducing denture manufacturing turnaround time by 40% while improving fit precision for institutional dental clinic buyers.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 34.4 Billion |

| Forecast Revenue (2035) | US$ 65.1 Billion |

| CAGR (2026-2035) | 6.6% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Service Type (Crown & Bridge Fabrication, Denture Fabrication, Orthodontic Appliances, Implant Prosthetics, Other Restorative Services), By Material Type (Ceramic Materials, Metal-Based Materials, Resin-Based Materials, Zirconia Materials), By Technology (Conventional Laboratory Methods, CAD/CAM Systems, 3D Printing Technology), By Application (Restorative Dentistry, Prosthodontics, Orthodontics, Implantology), By Lab Type (Independent Dental Laboratories, In-House Dental Clinic Labs, Corporate Laboratory Networks), By End User (Dental Clinics, Hospitals, Academic & Research Institutes) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | National Dentex Labs, Envista Holdings Corporation, Modern Dental Group Limited, Glidewell Laboratories, Dentsply Sirona, Henry Schein Inc., Straumann Group, 3M Oral Care, Ivoclar Vivadent AG, GC Corporation, Kulzer GmbH, VITA Zahnfabrik H. Rauter GmbH & Co. KG, Shofu Inc., Argen Corporation, DDS Lab, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |