Quick Navigation

Report Overview

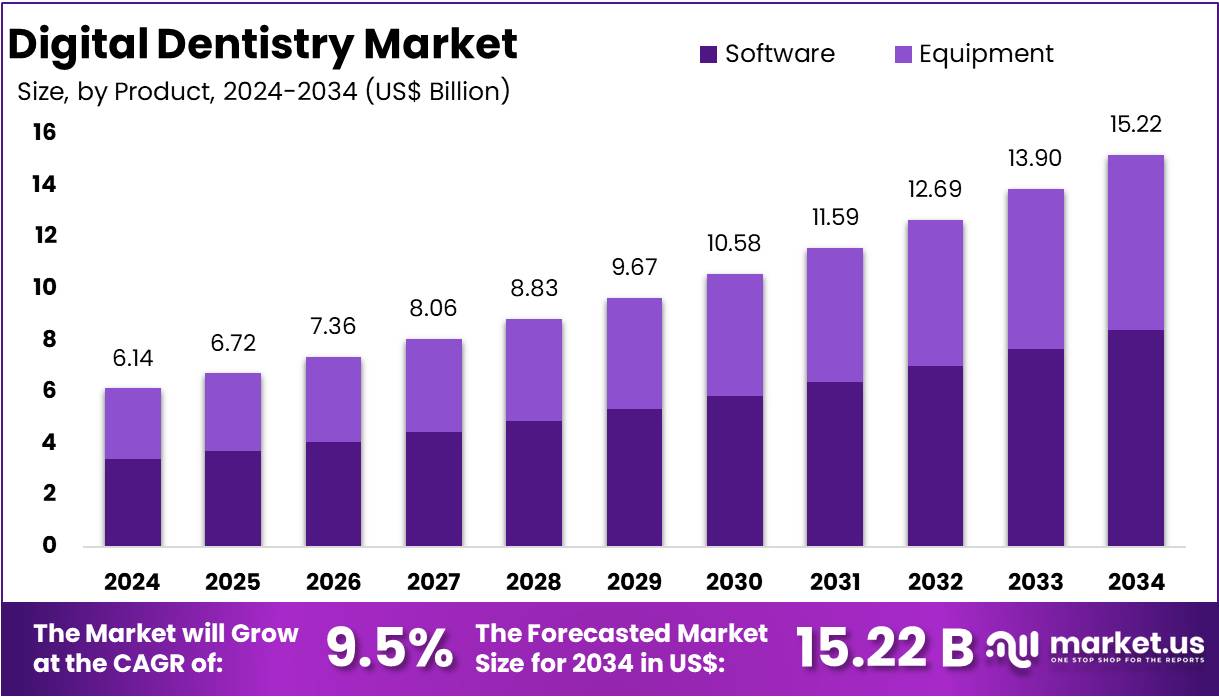

The Global Digital Dentistry Market Size is expected to be worth around US$ 15.22 Billion by 2034, from US$ 6.14 Billion in 2024, growing at a CAGR of 9.5% during the forecast period from 2025 to 2034. North America held a dominant market position, capturing more than a 39.2% share and holds US$ 2.40 Billion market value for the year.

Digital dentistry involves the integration of computer-aided and digital technologies into clinical practice to enhance treatment accuracy, efficiency, and patient outcomes. This approach utilizes advanced tools such as digital radiography, intraoral scanners, CAD/CAM systems, 3D printing, and AI-driven dental software, enabling precise diagnosis, customized treatment plans, and minimally invasive procedures.

The market growth is primarily driven by the rising demand for aesthetic and restorative dental procedures, increasing adoption of minimally invasive treatments, the growing prevalence of dental diseases, particularly among the aging population, advancements in AI-powered dental software and 3D printing technology, and improved patient experience due to reduced chair time and personalized treatment solutions.

However, the market faces certain challenges, including the high initial costs of digital equipment and technology adoption, the requirement for specialized training and technical expertise, and potential software and hardware integration issues that may impact workflow efficiency. Despite these challenges, digital dentistry continues to revolutionize the dental industry, offering solutions that streamline workflows and improve clinical outcomes.

Several recent developments highlight the industry’s momentum, such as Straumann Group’s acquisition of AlliedStar in September 2023, a Chinese provider of dental digital equipment and software. This strategic move strengthens Straumann’s presence in the China scanner market with a cost-effective and competitive solution, aligning with its long-term goal of expanding digital dentistry offerings.

Similarly, in September 2022, 3Shape introduced the TRIOS 5 Wireless intraoral scanner, designed to facilitate seamless digital workflows and enhance diagnostic accuracy, further advancing the transformation of digital dentistry. Additionally, in May 2022, Dentsply Sirona launched DS Core, a cloud-based digital dentistry platform developed in partnership with Google Cloud, aiming to improve collaboration between dentists, dental labs, and patients while optimizing treatment planning and workflow efficiency.

A survey conducted by the American Dental Association (ADA) in 2021 revealed that 91% of dental practices have transitioned to digital patient records; however, the adoption rates for advanced digital tools remain relatively lower, with intraoral scanners at 55.5% adoption and CAD/CAM systems at only 38%. This data highlights the market potential for further technological integration as more dental clinics and laboratories recognize the benefits of digitized workflows, precision diagnostics, and enhanced treatment customization.

The digital dentistry market is experiencing rapid technological advancements and increasing global adoption, driving the industry toward greater efficiency, cost-effectiveness, and improved patient outcomes. Despite certain challenges, the continued innovation in AI, cloud-based solutions, and 3D printing technologies is expected to propel market growth in the coming years.

Key Takeaways

- The Dental Dentistry market was valued at US$ 6.14 billion in 2024.

- Among product types segmented by software and equipment Software segment held the majority of the revenue share at 55.2%.

- Based Specialty Area, the market is bifurcated into Orthodontics, Prosthodontics, Implantology, and Others with orthodontics being the dominant segment covering 37.5% market share.

- Based on End User by dental Laboratories, dental hospitals and clinics, other end users, dental hospital and clinics accounted for the largest and fastest growing market share 66.8%.

- North America dominated the market which accounts for more than 39.2% market share.

Product Type Analysis

The software segment is expected to experience rapid growth and hold the majority share of 55.2% in the digital dentistry market due to several key factors. Software tools such as CAD (Computer-Aided Design) and CAM (Computer-Aided Manufacturing) systems, along with AI-powered diagnostic applications, significantly enhance treatment planning and execution, leading to greater accuracy and efficiency in dental procedures.

These digital solutions streamline dental workflows by integrating various aspects of dental practice—such as patient records, imaging, and treatment planning—into a unified system, facilitating the creation of highly customized solutions tailored to individual patient needs. Moreover, digital tools improve the overall patient experience by reducing chair time, providing visual aids for treatment explanations, and enabling more comfortable, precise procedures.

The continuous advancements in AI and machine learning technologies further accelerate the adoption of digital dentistry solutions. As these technologies evolve, they provide increasingly sophisticated tools that enhance diagnostic capabilities, treatment accuracy, and procedural efficiency. The integration of digital practice management software also plays a significant role, as it streamlines administrative tasks, enhances communication between dental team members, and improves patient record management. These innovations have not only improved the quality and efficiency of dental care but have also solidified the software segment’s dominant position in the digital dentistry market.

For example, CAD/CAM systems have revolutionized dental practices by enabling the precise design and manufacturing of dental prosthetics, including crowns, bridges, and dentures. AI-driven diagnostic tools, such as those used to analyze X-rays and 3D scans, provide highly accurate assessments of dental conditions, further enhancing treatment planning and outcomes.

Additionally, specialized algorithms have been developed and extensively trained to recognize specific medical conditions, assisting in the interpretation of laboratory results and improving diagnostic accuracy. Collectively, these advancements contribute to the ongoing expansion of the software segment, making it an indispensable component of modern dental practices.

Specialty Area Analysis

The orthodontics segment is anticipated to experience the highest growth rate in the digital dentistry market with 37.5% of total market share. Orthodontics plays a critical role in digital dentistry, offering significant benefits to both patients and practitioners. The use of advanced diagnostic tools, such as 3D imaging and cone beam computed tomography (CBCT), allows orthodontists to create precise and personalized treatment plans.

Digital models and virtual treatment simulations enhance patient communication, making it easier for patients to understand their treatment options and expected outcomes. The development of custom orthodontic appliances, like clear aligners and braces, has improved the accuracy and efficiency of treatments. Moreover, digital workflows streamline the treatment process, reducing chair time and ensuring a more comfortable experience for patients. Digital record-keeping has also simplified the storage, retrieval, and sharing of patient information, ensuring records remain up-to-date and easily accessible.

As a result, digital dentistry has significantly enhanced precision, efficiency, and the overall patient experience in orthodontic care, making it an indispensable element of modern dental practices. An example of innovation in the field is the FDA De Novo approval granted to Dental Monitoring for its AI-powered orthodontic remote monitoring system. This achievement represents a significant milestone in enhancing patient care and communication within orthodontic practices, further demonstrating the transformative potential of digital dentistry.

According to data from the British Orthodontic Society in 2023, the increased prevalence of online work, socializing, and video calls is influencing patient behavior, with 65% of orthodontists reporting it as a factor driving people to seek treatment. Additionally, more than a third (38%) of orthodontists note that their adult patients are influenced by social media influencers and celebrities.

Additionally, digital dentistry has made considerable advancements in implantology. The integration of digital tools such as CBCT, intraoral scanners, and CAD/CAM technology has revolutionized the planning and placement of dental implants. These digital workflows enable precise implant restoration planning, reducing complications and ensuring long-term success. By facilitating accurate diagnosis, scanning, designing, and prosthetic fabrication, digital tools enhance treatment accuracy, optimize clinical time, and reduce patient morbidity.

End-User Analysis

Dental hospitals and clinics dominated the digital dentistry market with 66.8% market share. These institutions play a central role in delivering comprehensive dental services, which is a key driver of their market leadership. Equipped with advanced technologies such as CAD/CAM systems, intraoral scanners, and 3D imaging tools, dental hospitals and clinics are crucial for diagnostics, treatment planning, and restorative procedures. By seamlessly integrating these digital technologies into their operations, they ensure streamlined workflows and deliver exceptional patient care.

Furthermore, dental hospitals and clinics address a wide range of dental needs, from routine check-ups to complex surgeries, making them well-suited to adopt and benefit from digital innovations. The increasing demand for aesthetic and customized dental treatments also contributes to the higher utilization of digital tools in these settings. Additionally, the presence of skilled professionals and access to resources enables effective implementation of cutting-edge technologies, further solidifying their dominant position in the market.

The combination of high patient volumes, comprehensive service offerings, access to funding, professional expertise, and strong patient trust makes dental hospitals and clinics the leading segment in the digital dentistry market. For example, a 2023 survey conducted by the American Dental Association Health Policy Institute (HPI) revealed that approximately 13.0% of the U.S. dentists were affiliated with a dental service organization, underscoring the increasing role of structured dental service models in adopting advanced dental technologies.

Key Market Segments

By Product

- Software

- Equipment

- CAD/CAM Systems

- Milling Machine

- 3D Printers

- Others

- Dental Imaging

- Extraoral Imaging

- Panoramic Systems

- Panoramic & Cephalometric Systems

- 3D CBCT Systems

- Intraoral Imaging

- X-ray Systems

- Intraoral Sensors

- Intraoral Photostimulable Phosphor Systems

- Intraoral Cameras

- Extraoral Imaging

- Intraoral Scanners

- Surgical Navigation Systems

- CAD/CAM Systems

Specialty Area

- Orthodontics

- Prosthodontics

- Implantology

- Others

By End-User

- Dental Laboratories

- Dental Hospitals and Clinics

- Others

Drivers

Technological Advancements in Digital Dentistry

Technological advancements are driving the rapid growth of the digital dentistry market. These innovations are transforming traditional dentistry into a more modern, efficient, and patient-friendly practice by enhancing precision, reducing treatment durations, and improving patient comfort. Modern dental technologies, including artificial intelligence (AI) and 3D printing, are making treatments more efficient, accurate, and comfortable.

Digital tools are increasingly being relied upon to detect and manage dental diseases, with robotics-assisted procedures enhancing precision in implant surgeries, reducing risks, and improving efficiency. Advancements such as CAD/CAM systems and 3D printing allow for the creation of highly accurate dental restorations, minimizing errors and improving outcomes.

Patients benefit from technologies like intraoral scanners, which replace the uncomfortable traditional molds, making procedures more convenient and less invasive. Innovations like CBCT imaging and AI-driven diagnostics enable early detection of dental issues, facilitating timely intervention and better prevention strategies. Minimally invasive techniques such as laser dentistry further reduce discomfort and recovery times. These advancements are improving the quality of dental care, making it more accessible, efficient, and patient-centered.

The increasing demand for aesthetic dentistry and the growing adoption of digital workflows are further fueling the expansion of the global digital dentistry market. For example, AI is helping to triage dental emergencies, determining which cases require immediate attention, while AI-powered intraoral scanners are enhancing diagnostic accuracy by creating detailed digital impressions and eliminating the discomfort of traditional molds.

These innovations not only improve efficiency in dental clinics but also enhance the overall patient experience. In March, 2025, Medit is set to introduce a new addition to its i900 intraoral scanner series. The Medit i900 Classic is designed to improve usability and efficiency, offering intuitive control, precise scanning, and seamless workflow integration, providing dental professionals around the world with enhanced options.

Restraints

High Initial Costs in Digital Dentistry

The cost of dental procedures using digital technology is significantly higher compared to traditional methods. The substantial initial investment required for adopting digital dental tools presents a major challenge for many practices. Technologies such as intraoral scanners, CAD/CAM systems, 3D printers, and compatible software come with high price tags. For instance, the cost of a 3D Intraoral Scanner is around US$ 3,700.

This significant upfront expenditure can be a barrier, especially for smaller practices or those located in developing regions. While digital tools and techniques promise enhanced efficiency, precision, and an improved patient experience, the costs of acquiring the necessary equipment, training staff, and maintaining software licenses can strain financial resources.

In addition to the initial purchase costs, practices must also account for ongoing expenses related to installation, maintenance, and training, further increasing the financial burden. Moreover, regulatory and compliance issues across different regions complicate the adoption process. Balancing the potential benefits of digital dentistry with the reality of these financial and logistical constraints remains a significant challenge, particularly for smaller practices.

Opportunities

The Potential use of digital dentistry in combination with Teledentistry

The integration of digital dentistry with teledentistry is transforming modern dental care. Digital dentistry includes intraoral scanners, 3D printing, and CAD/CAM restorations, improving precision and efficiency. These technologies enhance patient outcomes by enabling accurate digital impressions and AI-assisted diagnostics. When combined with teledentistry, remote consultations become more effective, allowing dentists to assess cases virtually. Additionally, 3D printing supports faster dental prosthetic production. This integration streamlines workflows, reduces costs, and expands access to quality dental care, particularly for patients in remote or underserved regions.

The growing adoption of teledentistry is driven by increasing patient demand for convenience. Remote consultations reduce travel time and allow dentists to reach patients who lack local dental services. The combination of digital tools and virtual care enhances treatment accessibility while ensuring high-quality care. Furthermore, it supports remote education for dental professionals, helping them stay updated on new advancements. As digital dentistry evolves, its integration with teledentistry will continue to reshape the future of dental care.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors play a pivotal role in shaping the digital dentistry market. Economic growth, increasing disposable incomes, and higher healthcare spending enable greater adoption of advanced dental technologies, driving market expansion. Additionally, rapid urbanization and evolving lifestyles contribute to rising demand for innovative dental solutions. Geopolitical elements, including trade policies, international regulations, and supply chain disruptions, can impact the availability and cost of digital dental equipment and raw materials.

Political stability and government initiatives promoting oral health further influence market growth by encouraging technological advancements and infrastructure development. However, global events such as pandemics can significantly disrupt supply chains, alter consumer demand, and challenge market stability, underscoring the need for a resilient and adaptive digital dentistry industry.

Latest Trends

Growing Adoption of Intraoral Scanners in Modern Dentistry

The growing adoption of intraoral scanners in modern dentistry is transforming clinical workflows, offering unparalleled precision, efficiency, and patient comfort. These advanced devices generate highly accurate 3D digital impressions, replacing traditional impression-taking methods and significantly improving the quality of dental restorations.

Innovations such as continuous image capture, AI-driven image processing, and real-time error correction enhance scanning accuracy and streamline workflows. A landmark study in collaboration with Semmelweis University in Hungary at the end of 2022 marked one of the largest international research efforts on intraoral scanners, shedding light on their clinical utility. A 2023 survey published in the International Dental Journal revealed that a significant 81.9% (n=878) of respondents believed that modern technology has enhanced the accuracy of intraoral scanners (IOS) over traditional casting methods, while 18.1% (n=194) still preferred traditional casting techniques.

The efficiency of intraoral scanners reduces chair time for patients while ensuring better-fitting restorations with minimal adjustments. Their seamless integration with CAD/CAM systems enables same-day restorations, making them indispensable in procedures such as crowns, bridges, implants, and orthodontic aligners. Patients also prefer digital impressions due to their comfort and non-invasive nature. With continuous technological advancements, intraoral scanners are poised to play an increasingly vital role in modern dentistry, driving precision, efficiency, and enhanced patient experiences.

Regional Analysis

North America is leading the Digital Dentistry Market

North America dominated the digital dentistry market with 39.2% market share, driven by its advanced healthcare infrastructure, high adoption rates of AI-powered dental technologies, and significant investments in research and development. The US alone accounts for a substantial portion of the global market share, reflecting strong technological advancements and increasing demand for precision-driven dental solutions. The region benefits from a well-established network of dental professionals and patients who prioritize efficiency, accuracy, and cutting-edge solutions in dental care.

Additionally, rising healthcare spending, supportive government policies, favorable reimbursement frameworks, and a strong presence of key market players contribute to its sustained growth. The rising demand for aesthetic dentistry, which requires highly accurate and customized treatments, further reinforces North America’s market dominance, ensuring continued expansion and technological innovation in digital dentistry. According to the American Dental Association, inflation-adjusted dental spending in 2023 increased by $4 billion, reflecting a 2.5% rise from 2022. This growth was primarily driven by a surge in Medicare dental expenditures.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

The Asia-Pacific region is poised for the highest CAGR in the digital dentistry market during the forecast period, driven by increasing demand for advanced dental care and aesthetic treatments. Rapid economic growth in countries like China and India has led to substantial investments in healthcare infrastructure and the widespread adoption of cutting-edge dental technologies. A growing middle-class population with rising disposable income is further fueling demand for modern, technology-driven dental solutions.

Additionally, the high prevalence of oral health issues in the region has intensified the need for more efficient and precise treatment options, making digital dentistry a preferred choice. Government initiatives supporting healthcare advancements and the integration of digital tools in dental practices are further accelerating market expansion. These factors collectively position Asia-Pacific as one of the fastest-growing regions in the global digital dentistry market, with significant potential for future innovation and adoption.

In January 2024, Fujitsu launched a large-scale health education initiative aimed at promoting oral and dental health among its approximately 70,000 employees in Japan. Running from January 26, 2024, the program encourages employees to take proactive steps toward maintaining and improving their dental well-being. As a global provider of digital services, the Fujitsu Group operates across various regions, including Japan, reinforcing its commitment to employee health and well-being worldwide.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Leading companies in the digital dentistry market are driving innovation by developing advanced solutions that enhance diagnostics, treatment planning, and restorative procedures. Significant investments in research and development have led to breakthroughs in CAD/CAM systems, AI-powered imaging software, and portable intraoral scanners, improving both accuracy and efficiency in dental care.

In addition to technological advancements, companies are prioritizing accessibility by creating user-friendly and cost-effective solutions, broadening the reach of digital dentistry. Strategic collaborations with dental organizations, educational institutions, and government bodies are further accelerating market growth by increasing awareness and promoting the widespread adoption of digital tools in dental practices. These combined efforts are positioning key players at the forefront of an evolving industry, shaping the future of modern dentistry.

Top Key Players in the Digital Dentistry Market

- 3Shape A/S

- Align Technology, Inc.

- Dentsply Sirona

- Envista Holdings Corporation

- Planmeca Oy

- Straumann Group

- Carestream Dental

- Ivoclar Vivadent

- Zimmer Biomet Dental

- Medit Corp.

- MORITA CORP.

- KaVo Dental

- Kuraray Noritake Dental Inc.

- Apteryx Imaging Inc.

- Kulzer GmbH

- Midmark Corporation

- Shofu Inc.

Recent Developments

- March 2025: Align Technology, Inc. introduced Align X-ray Insights, an advanced AI-powered computer-aided detection (CADe) software solution, across European Union countries and the United Kingdom. This innovative tool is designed to automatically analyze 2D radiographs, significantly enhancing diagnostic capabilities for dental professionals.

- October 2024: Dentsply Sirona launched CEREC Software 5.3, a major update that improves cloud-based dentistry workflows. This latest version offers enhanced integration with DS Core and the Primescan 2 intraoral scanner, providing greater workflow flexibility, smoother data transfers, and new opportunities for practice growth.

- December 2022: MBK Partners, a leading Asia-focused private equity firm, acquired Medit Corp., the world’s third-largest manufacturer of 3D dental scanners, for 2.45 trillion won ($2 billion). MBK secured a 99.5% stake in the South Korean digital dental equipment company from Unison Capital Korea through a share purchase agreement.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 6.14 billion |

| Forecast Revenue (2034) | US$ 15.22 billion |

| CAGR (2025-2034) | 9.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Software, Equipment), By Specialty Area (Orthodontics, Prosthodontics, Implantology, Others) By End User (Dental Laboratories, Dental Hospitals and Clinics, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | 3Shape A/S, Align Technology, Inc., Dentsply Sirona, Envista Holdings Corporation, Planmeca Oy, Straumann Group, Carestream Dental, Ivoclar Vivadent, Zimmer Biomet Dental, Medit Corp., J. MORITA CORP., KaVo Dental, Kuraray Noritake Dental Inc., Apteryx Imaging Inc., Kulzer GmbH, Midmark Corporation, Shofu Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |