Quick Navigation

Report Overview

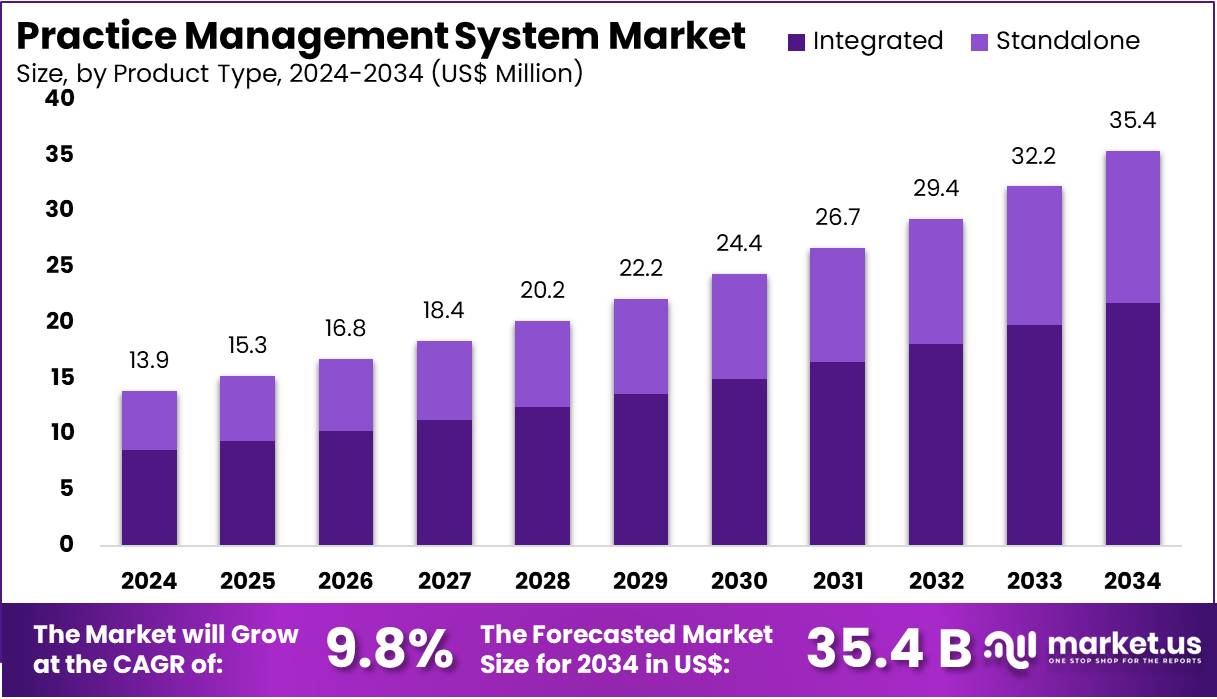

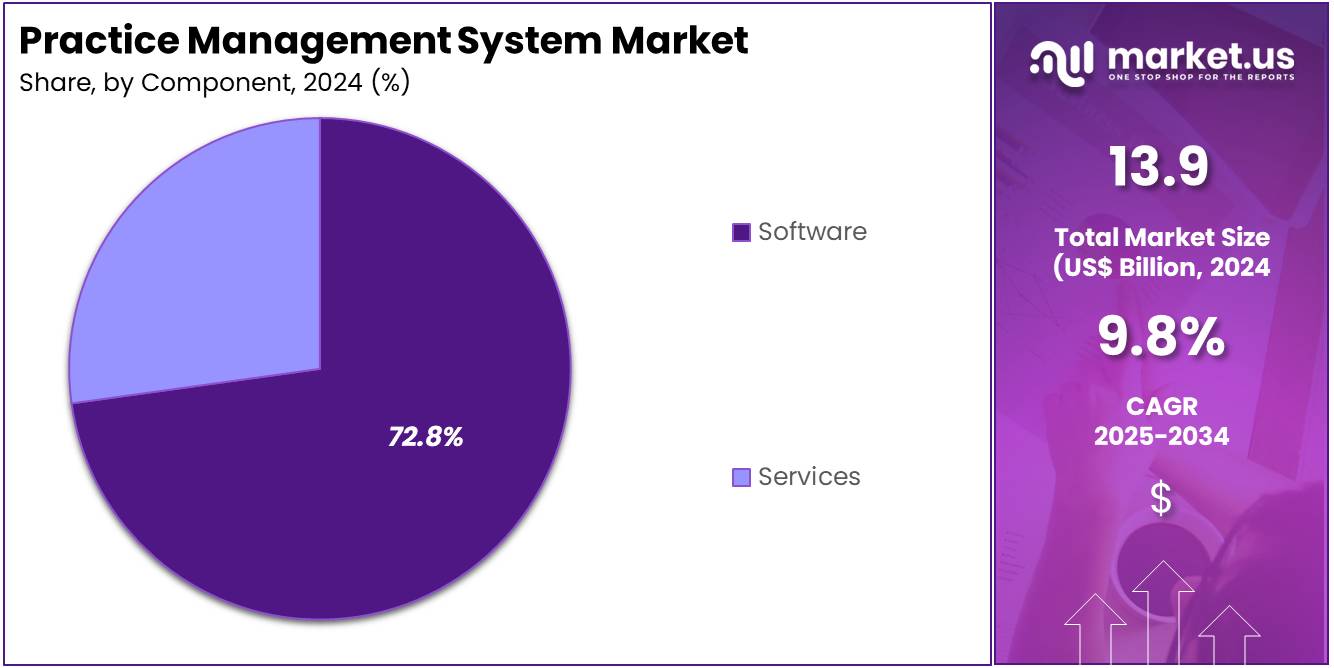

The Practice Management System Market size is expected to be worth around US$ 35.4 billion by 2034 from US$ 13.9 billion in 2024, growing at a CAGR of 9.8% during the forecast period 2025 to 2034.

Increasing demand for efficient and cost-effective healthcare solutions has driven the growth of the practice management system (PMS) market. Healthcare providers are seeking better ways to streamline administrative tasks such as scheduling, billing, and patient record management, which has resulted in the adoption of these systems. The ongoing push for improved patient care quality while controlling costs has made PMS an essential tool for medical practices.

Technological innovations have also played a significant role in this growth, with cloud-based systems gaining popularity due to their flexibility and accessibility. The rise of value-based care models has created further opportunities for PMS to assist in data analysis and performance measurement, ultimately supporting healthcare organizations in optimizing operations. As regulatory requirements for electronic health records (EHR) and patient data security continue to evolve, PMS solutions provide valuable support in maintaining compliance.

Additionally, the increased need for telehealth integration, particularly in light of the COVID-19 pandemic, has spurred the development of PMS systems that seamlessly incorporate virtual care solutions. An aging population and the growing prevalence of chronic diseases also contribute to the demand for more advanced practice management tools. According to the Centers for Disease Control and Prevention (CDC), as of 2021, 88.2% of office-based physicians in the United States were using any electronic medical record (EMR) or electronic health record (EHR) system, with 77.8% having a certified system.

Key Takeaways

- In 2024, the market for practice management system generated a revenue of US$ 13.9 billion, with a CAGR of 9.8%, and is expected to reach US$ 35.4 billion by the year 2034.

- The product type segment is divided into integrated and standalone, with integrated taking the lead in 2024 with a market share of 61.5%.

- Considering component, the market is divided into software and services. Among these, software held a significant share of 72.8%.

- Furthermore, concerning the delivery mode segment, the market is segregated into web-based, cloud-based, and on-premise. The web-based sector stands out as the dominant player, holding the largest revenue share of 56.7% in the practice management system market.

- The end-user segment is segregated into physician back office, pharmacies, diagnostic laboratories, and others, with the physician back office segment leading the market, holding a revenue share of 53.9%.

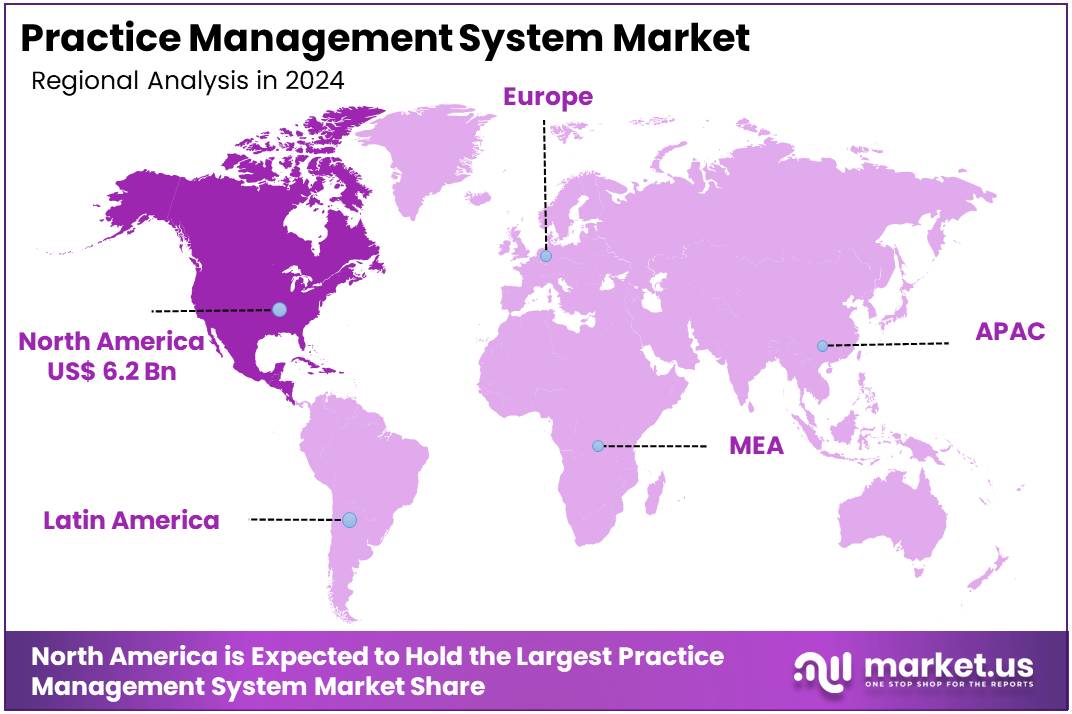

- North America led the market by securing a market share of 44.3% in 2024.

Product Type Analysis

The integrated segment led in 2024, claiming a market share of 61.5% owing to as healthcare providers increasingly adopt comprehensive solutions to streamline operations and improve patient care. Integrated systems that combine patient engagement tools, e-Rx, EHR/EMR, and other functionalities are anticipated to experience rising demand due to their ability to enhance workflow efficiency and ensure seamless data sharing across different healthcare providers.

The growing emphasis on reducing administrative burdens and improving the overall patient experience is likely to drive the adoption of integrated solutions. Additionally, as regulations around data sharing and interoperability become stricter, healthcare organizations are projected to seek integrated systems to comply with new standards. The integration of various features into a single platform is expected to provide cost-effective, user-friendly solutions that meet the evolving needs of healthcare providers, thereby accelerating the growth of this segment.

Component Analysis

The software held a significant share of 72.8% as healthcare organizations increasingly adopt digital solutions to optimize clinical and administrative functions. Software is expected to dominate the market due to its ability to facilitate patient scheduling, billing, coding, and record-keeping, which are crucial for efficient practice management. The growing need for better data management, improved patient outcomes, and the reduction of errors is likely to drive demand for practice management software solutions.

Additionally, the increasing focus on value-based care, which requires more streamlined patient data management and reporting, is anticipated to further contribute to the growth of the software segment. As software solutions continue to evolve with added functionalities, such as AI and predictive analytics, healthcare providers are expected to adopt these tools to enhance operational efficiency and patient care.

Delivery Mode Analysis

The web-based segment had a tremendous growth rate, with a revenue share of 56.7% owing to the increasing adoption of cloud-based technologies and the demand for flexible, scalable solutions. Web-based platforms provide healthcare providers with the ability to access their practice management systems remotely, enabling them to offer improved services and streamline operations, especially in multi-location practices.

The anticipated growth of this segment is driven by the rising need for efficient data sharing, real-time updates, and the ability to access patient records from anywhere. The shift towards web-based systems is also supported by the increasing use of mobile devices in healthcare, enabling practitioners to access information on-the-go. As the healthcare sector continues to prioritize flexibility, security, and cost-effectiveness, web-based solutions are projected to become more widely adopted.

End-user Analysis

The physician back office segment grew at a substantial rate, generating a revenue portion of 53.9% due to the increasing demand for efficient administrative and operational support in medical practices. The back office plays a crucial role in managing the business side of healthcare, including billing, insurance claims, scheduling, and patient records, all of which can be optimized through advanced practice management systems.

As the healthcare industry continues to shift towards value-based care models, the need for seamless coordination between clinical and administrative operations is projected to rise. Furthermore, the growing adoption of digital solutions to streamline workflow and reduce administrative costs is likely to drive the demand for practice management systems in physician back offices. As practices seek to improve patient service, reduce overheads, and enhance productivity, the physician back office segment is expected to see continued expansion.

Key Market Segments

By Product Type

- Integrated

- Patient engagement

- e-Rx

- EHR/EMR

- Others

- Standalone

By Component

- Software

- Services

By Delivery Mode

- Web-based

- Cloud-based

- On-premise

By End-user

- Physician Back Office

- Pharmacies

- Diagnostic Laboratories

- Others

Drivers

Technological Advancements are Driving the Market

The practice management system (PMS) market is experiencing significant growth due to continuous technological advancements. The integration of artificial intelligence (AI) and machine learning into PMS solutions has enhanced administrative efficiency, enabling automated scheduling, billing, and patient record management. For instance, AI-driven systems can predict patient no-shows and optimize appointment scheduling, reducing downtime for healthcare providers.

Additionally, the adoption of cloud-based PMS offers scalable solutions with real-time data access, facilitating seamless coordination among medical staff. These technological innovations not only streamline operations but also improve patient care by minimizing errors and expediting processes. As healthcare facilities increasingly prioritize digital transformation, the demand for advanced PMS is expected to rise, further propelling market expansion.

Restraints

High Implementation Costs are Restraining the Market

Despite the benefits, the high costs associated with implementing advanced practice management systems pose a significant barrier to market growth. The initial investment for purchasing and customizing PMS software can be substantial, especially for small to mid-sized healthcare practices. Beyond acquisition, expenses related to staff training, system maintenance, and periodic upgrades add to the financial burden.

For example, the average cost of a physician practice management software ranges from US$350 to US$1,000, excluding other services. These financial constraints may deter healthcare providers from adopting new systems, leading to continued reliance on outdated methods that could hinder operational efficiency. To mitigate this restraint, vendors are exploring flexible pricing models and offering scalable solutions to accommodate practices with limited budgets.

Opportunities

Integration of Telehealth Services is Creating Growth Opportunities

The integration of telehealth services into practice management systems presents a significant growth opportunity in the market. The COVID-19 pandemic accelerated the adoption of telemedicine, necessitating PMS platforms that can seamlessly incorporate virtual consultation functionalities. Systems equipped with telehealth capabilities enable healthcare providers to schedule, conduct, and document virtual visits within a unified interface.

This integration enhances patient accessibility to care, especially in remote areas, and optimizes the provider’s workflow by consolidating in-person and virtual appointments. As telehealth becomes a staple in healthcare delivery, PMS vendors offering robust telemedicine features are poised to attract a broader clientele. This trend indicates a shift towards more versatile and comprehensive practice management solutions, aligning with the evolving landscape of patient care.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors significantly influence the practice management system market. Economic downturns can lead to reduced healthcare budgets, limiting investments in new technologies and hindering the adoption of advanced PMS solutions. Conversely, economic growth facilitates increased spending on healthcare infrastructure, promoting the implementation of sophisticated management systems.

Geopolitical tensions may disrupt global supply chains, affecting the availability of necessary hardware components and delaying system deployments. Trade policies and international relations also impact the cost and accessibility of PMS software across different regions. However, supportive government initiatives aimed at healthcare digitization can mitigate negative effects, providing funding and incentives for technology adoption. For instance, programs that subsidize electronic health record implementation encourage practices to upgrade their management systems. Overall, while challenges persist, strategic planning and favorable policies can foster resilience and growth in the practice management system market.

Trends

Emphasis on Data Security is a Recent Trend

A notable trend in the practice management system market is the increasing emphasis on data security and compliance. With the digitization of patient records and administrative processes, safeguarding sensitive information against breaches has become paramount. Healthcare providers are now prioritizing PMS solutions that offer advanced security features, such as encryption, multi-factor authentication, and regular security audits.

Compliance with regulations like the Health Insurance Portability and Accountability Act (HIPAA) in the United States is also a critical consideration. Vendors are responding by enhancing their systems to meet stringent security standards, thereby building trust with users. This focus on data protection not only ensures legal compliance but also reinforces patient confidence in the confidentiality of their medical information.

Regional Analysis

North America is leading the Practice Management System Market

North America dominated the market with the highest revenue share of 44.3% owing to several key factors. The increasing adoption of electronic health records (EHR) and integrated healthcare solutions has streamlined administrative and clinical workflows, enhancing operational efficiency. The aging population in the United States, with approximately 16.5% of residents aged 65 and older in 2023, has increased the demand for healthcare services, thereby boosting the need for effective practice management systems.

Advancements in technology have led to the development of more sophisticated and user-friendly systems, improving patient care and satisfaction. Government initiatives, such as the EHR incentive programs offered by Medicaid and Medicare, have encouraged healthcare providers to adopt these systems, further driving market growth.

Additionally, the rising prevalence of chronic diseases has increased the patient load, necessitating efficient management solutions. The integration of telehealth services into practice management systems has expanded access to care, especially during the COVID-19 pandemic. The presence of key market players and well-established healthcare infrastructure in the region has also contributed to the market’s expansion. These factors collectively contributed to the robust growth of the practice management system market in North America in 2023.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to grow with the fastest CAGR owing to several key factors. The region’s aging population, with a significant increase in the number of individuals aged 65 and above, is anticipated to drive demand for healthcare services, including practice management solutions. For instance, the United Nations projects that by 2050, the number of older persons in Asia and the Pacific will reach 1.3 billion, up from 600 million in 2020.

Additionally, the rising prevalence of chronic diseases and disabilities is expected to increase the need for efficient management systems. Economic growth in countries like China and India is projected to enhance the purchasing power of the middle class, making healthcare services more accessible. Government initiatives aimed at improving healthcare infrastructure and providing support for the elderly are likely to further boost market growth.

The increasing awareness of the importance of efficient healthcare management in maintaining quality of care is expected to drive demand for practice management systems. These factors collectively contribute to the anticipated growth of the practice management system market in Asia Pacific during the forecast period.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the practice management system market focus on developing comprehensive, integrated solutions that streamline administrative tasks such as scheduling, billing, and patient records management. Companies invest in cloud-based platforms and artificial intelligence to enhance automation, improve data accuracy, and reduce operational costs for healthcare providers. Strategic partnerships with healthcare organizations and software developers help expand market presence and improve product offerings.

Many players emphasize user-friendly interfaces and mobile access to meet the needs of modern healthcare practices. Additionally, regulatory compliance and data security remain central to ensuring client trust and market growth. Athenahealth is a leading company in this market, offering cloud-based solutions for medical billing, scheduling, and practice management. The company focuses on simplifying healthcare workflows and improving financial performance for providers. Athenahealth’s commitment to innovation and customer service establishes it as a key player in the practice management industry.

Top Key Players in the Practice Management System Market

- Renaissance Physicians Partners

- McKesson Corporation

- GE Healthcare

- Epic Systems Corporation

- eClinicalWorks

- CoreCloud

- Cerner Corporation

- Athenahealth

Recent Developments

- In November 2023, Renaissance Physicians Partners (RPP), a physician-led network, partnered with Florence Health to oversee and manage its affiliated medical practices.

- In October 2023, GE HealthCare joined forces with University Hospitals to integrate enterprise digital solutions aimed at enhancing patient care and streamlining healthcare operations.

Report Scope

| Report Features | Description |

| Market Value (2024) | US$ 13.9 billion |

| Forecast Revenue (2034) | US$ 35.4 billion |

| CAGR (2025-2034) | 9.8% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Integrated (Patient Engagement, e-Rx, EHR/EMR, and Others), Standalone), By Component (Software and Services), By Delivery Mode (Web-based, Cloud-based, and On-premise), By End-user (Physician Back Office, Pharmacies, Diagnostic Laboratories, and Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Renaissance Physicians Partners, McKesson Corporation, GE Healthcare, Epic Systems Corporation, eClinicalWorks, CoreCloud, Cerner Corporation, and Athenahealth. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |