Quick Navigation

Report Overview

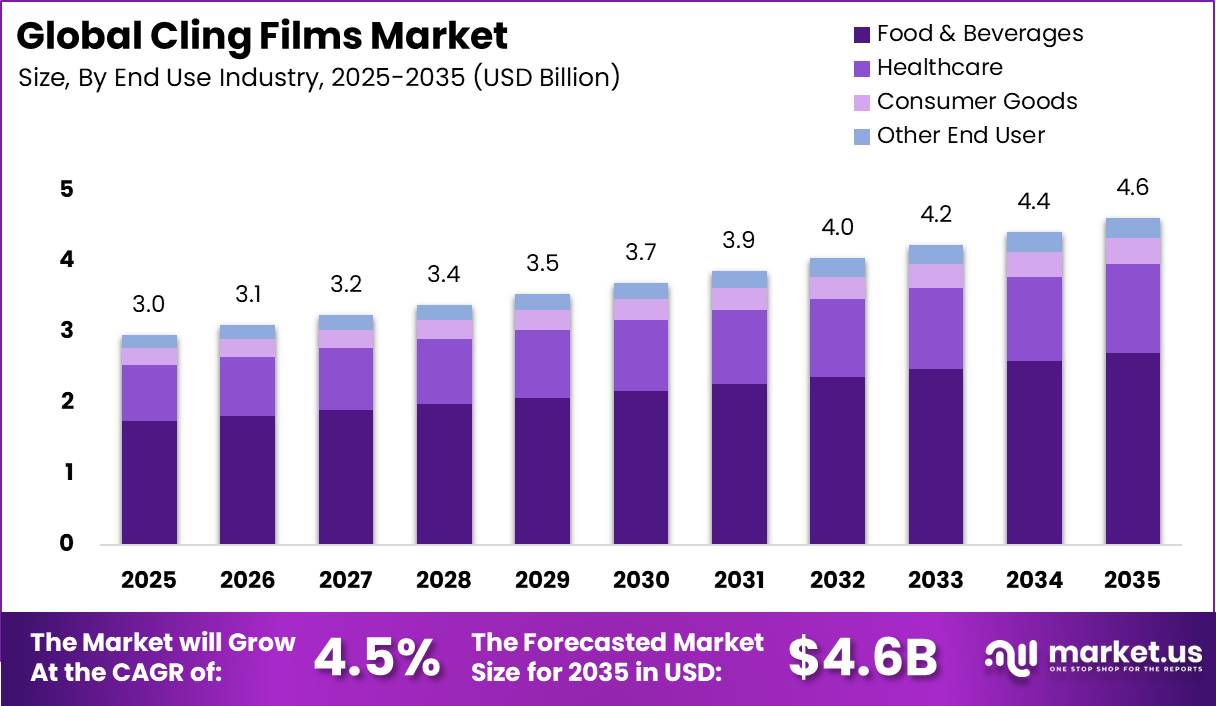

Global Cling Films Market size is expected to be worth around USD 4.6 Billion by 2035 from USD 3.0 Billion in 2025, growing at a CAGR of 4.5% during the forecast period 2026 to 2035.

The cling films market covers thin, stretchable plastic wrapping materials used to seal, protect, and preserve food, pharmaceutical products, and consumer goods. Manufacturers produce cling films primarily from polyethylene, PVC, polypropylene, and PVDC resins, distributing them through retail and institutional channels to households, food service operators, and industrial packagers. This reflects the breadth of end-use applications driving consistent baseline volume across both developed and developing economies.

Key Takeaways

- Market size in 2025: USD 3.0 Billion

- Market size in 2035: USD 4.6 Billion

- CAGR (2026 to 2035): 4.5%

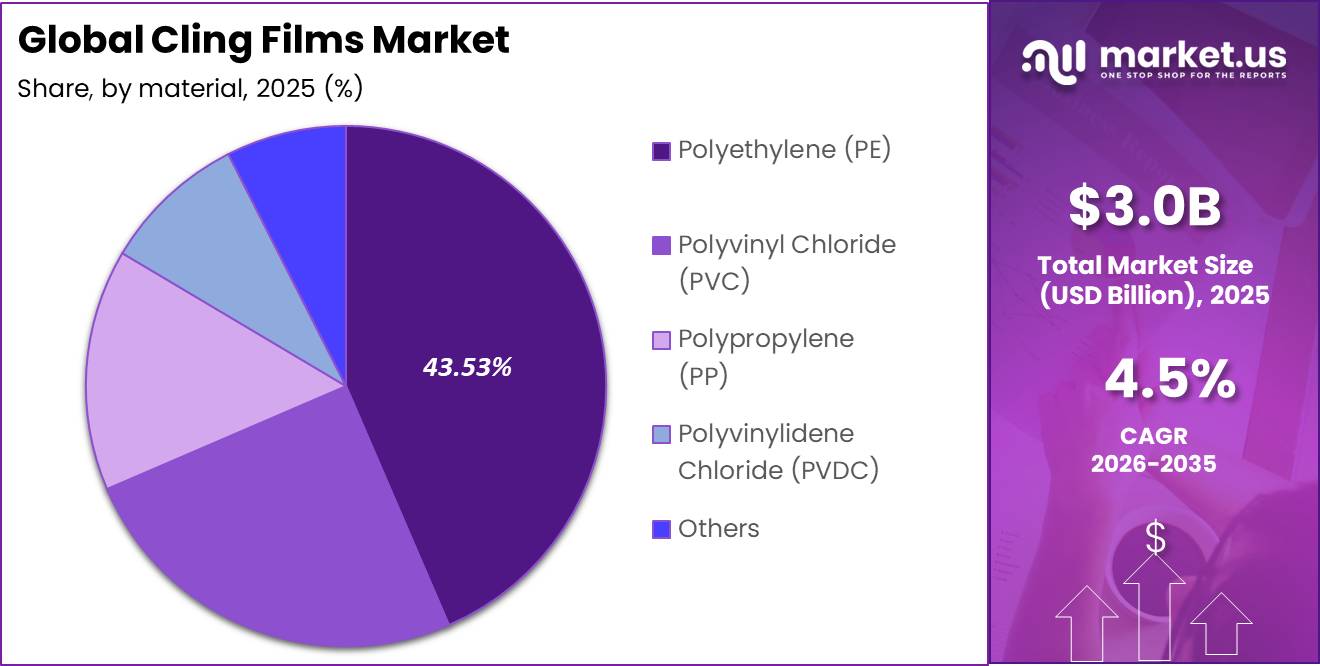

- Dominant material segment: Polyethylene (PE) with 43.53% share

- Dominant end use segment: Food and Beverages with 58.66% share

- Dominant distribution channel: Offline with 72.78% share

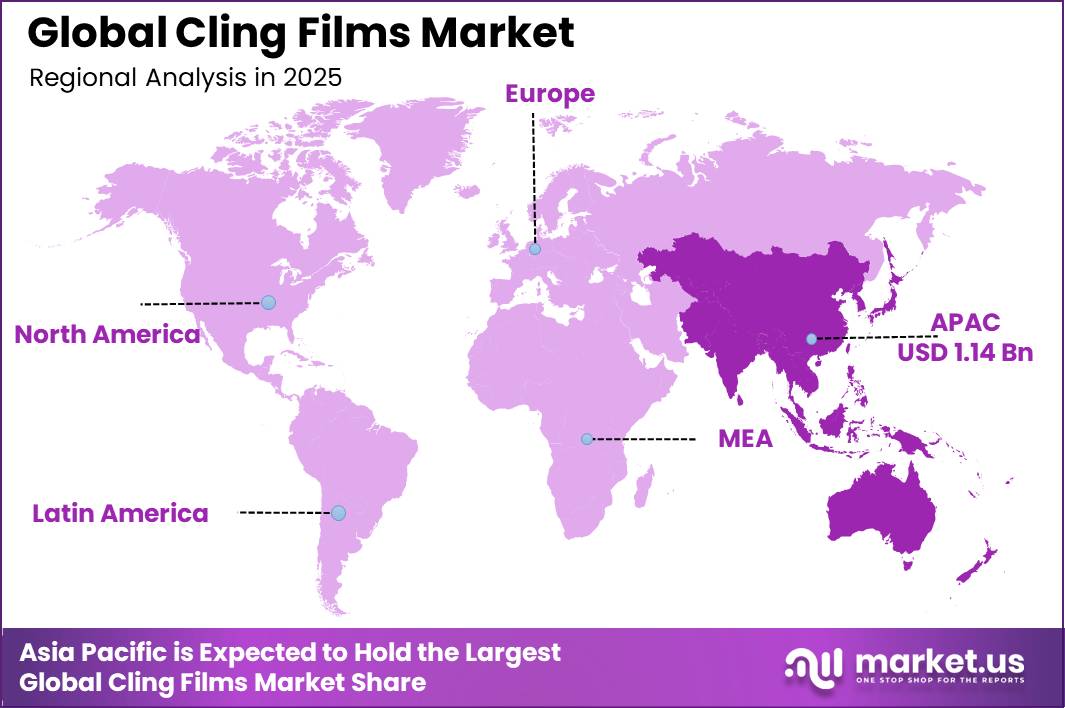

- Dominant region: Asia-Pacific with 38.56% share, valued at USD 1.14 Billion

Europe’s Packaging and Packaging Waste Regulation entered into force in February 2025 and begins applying from 12 August 2026. This regulation requires all packaging to achieve recyclability by 2030, restricts PFAS in food-contact packaging, and introduces recycled-content targets for non-PET plastics at 10% by 2030. Cling film suppliers serving EU retailers face direct pressure to reformulate PVC-heavy and multi-layer structures into mono-material polyethylene alternatives. Converters that meet these compliance thresholds gain first access to replacement demand across the region’s installed SKU base.

According to the U.S. Environmental Protection Agency, containers and packaging generate 82.2 million tons of municipal solid waste in the United States, equal to 28.1% of total MSW generation. This volume signals the scale of the packaging sector’s waste footprint and the commercial pressure building on manufacturers to adopt lighter, recyclable, or bio-based film formats. Brands and retailers that respond to this pressure early secure stronger shelf positioning with sustainability-focused procurement teams.

Data from the U.S. Environmental Protection Agency shows plastic containers and packaging alone account for 14.5 million tons of waste annually in the U.S. A public awareness study published by the National Institutes of Health, based on an online survey of 1,000 respondents across multiple European countries, found that citizens show high general awareness that plastic consumption directly affects human health. This consumer-level awareness accelerates retailer demands for sustainable packaging solutions, including recyclable and compostable cling film variants.

Material Analysis

Polyethylene (PE) dominates with 43.53% due to superior stretch properties and regulatory acceptance.

In 2025, Polyethylene held a dominant market position in the By Material segment of the Cling Films Market, with a 43.53% share. PE films offer superior cling strength, puncture resistance, and compatibility with food-contact regulations across major markets. Retailers and food service operators prefer PE over PVC alternatives as regulatory pressure on single-use plastics intensifies, making PE the structural backbone of flexible plastic packaging reformulation strategies globally.

Polyvinyl Chloride (PVC) has historically served as the standard material for household and commercial cling films due to its strong self-adhesion and low production cost. However, regulatory phase-outs under EU PFAS restrictions and plastic waste management frameworks are actively reducing PVC’s addressable market. Converters dependent on PVC-heavy product lines face SKU rationalization risk, particularly in EU-facing trade lanes where compliance timelines are tightest.

Polypropylene (PP) serves niche applications where heat resistance and stiffness are priorities, including microwave-compatible wraps and specialty food-service formats. PP commands a modest share within the material mix but holds competitive positioning as automated dispensing systems in commercial kitchens require films with consistent tension properties. This positions PP suppliers to benefit from the broader shift toward institutional and industrial wrapping formats.

Polyvinylidene Chloride (PVDC) targets high-barrier applications requiring oxygen and moisture resistance, primarily in pharmaceutical and premium food packaging. Others, including bio-based PLA films and starch-blend compostable wraps, represent the fastest growing sub-segment within the material category. Bio-based alternatives remain a small share today but attract investment as EU recyclability mandates and PFAS restrictions make conventional film formulations increasingly costly to maintain.

End Use Industry Analysis

Food and Beverages dominates with 58.66% due to high-frequency wrapping needs across retail and food service.

In 2025, Food and Beverages held a dominant market position in the By End Use Industry segment of the Cling Films Market, with a 58.66% share. As per the Food and Agriculture Organization of the United Nations, 14% of food is lost between harvest and retail due to inadequate cold-chain infrastructure for perishable products like meat and dairy. This food loss rate directly validates investment in protective wrapping solutions across retail, institutional, and cold-chain distribution formats.

Healthcare represents a structurally distinct demand stream within the end use mix. Hospitals, laboratories, and institutional catering operations require cling films that meet stricter hygiene and contamination standards than household or standard food-service grades. Antimicrobial-coated film formats and medical-grade wraps serve this segment, and suppliers that achieve relevant food-contact and pharmaceutical compliance certifications access a lower-churn, higher-margin customer base.

Consumer Goods applications include non-food household wrapping, retail product bundling, and e-commerce secondary packaging. As per our research, packaging accounts for approximately 44% of municipal solid plastic waste in some regions, reflecting its dominance in retail and pre-packaged product systems. This waste intensity is pushing consumer goods brands toward thinner, recyclable film formats, creating a direct reformulation pipeline for cling film suppliers serving private-label and branded retail programs. Other End Users, including industrial and logistics operators, hold the remaining share collectively.

Distribution Channel Analysis

Offline dominates with 72.78% due to established retail and institutional procurement networks.

In 2025, Offline held a dominant market position in the By Distribution Channel segment of the Cling Films Market, with a 72.78% share. Supermarkets, foodservice distributors, and institutional procurement desks drive the majority of cling film volume through direct supply agreements and in-store availability. This structural reliance on physical distribution reflects the bulk-purchase behavior of commercial kitchens, healthcare facilities, and large-format retailers that prioritize consistent supply over digital ordering convenience.

Online represents the fastest growing distribution channel within the cling films market. E-grocery expansion, direct-to-consumer packaging supply, and B2B procurement platforms are pulling volume toward digital channels. This shift creates a demand signal for cling film formats specifically optimized for last-mile fresh food packaging, where individual portion sizes, tamper-evident wrapping, and cold-chain compatibility are non-negotiable product attributes rather than optional features.

Key Market Segments

By Material

- Polyvinyl Chloride (PVC)

- Polyethylene (PE)

- Polypropylene (PP)

- Polyvinylidene Chloride (PVDC)

- Others

- Bio-based PLA films

- Starch-blend compostable wraps

By End Use Industry

- Food and Beverages

- Healthcare

- Consumer Goods

- Other End User

By Distribution Channel

- Offline

- Online

Regional Analysis

Asia-Pacific Dominates the Cling Films Market with a Market Share of 38.56%, Valued at USD 1.14 Billion

Asia-Pacific holds the largest regional share of the cling films market, driven by dense urban food retail networks in China, India, Japan, and Southeast Asia. Rapid growth of quick-service restaurants and cloud kitchen formats across the region generates consistent short-cycle wrapping volume. Cold-chain infrastructure investment in India and ASEAN markets is expanding institutional demand for high-barrier films across dairy, meat, and pharmaceutical distribution channels.

North America maintains a structurally strong position anchored by supermarket-led fresh produce pre-packaging and a mature foodservice sector with high per-capita cling film consumption. U.S. regulatory frameworks continue to shape material selection, with PPI data for coextruded single-web film at 183.285 in April 2026 signaling persistent input cost pressure on converters. Suppliers serving North American institutional buyers face margin discipline requirements that favor scale operators over smaller regional converters.

Europe is undergoing the most significant regulatory-driven restructuring among all regions. The EU Packaging and Packaging Waste Regulation, applying from 12 August 2026, compels all packaging to meet recyclability and recycled-content criteria, creating immediate replacement demand for non-compliant PVC and multi-layer cling films. Converters supplying EU retailers that achieve mono-material PE or PP compliance ahead of deadline capture 15 to 25% of at-risk regional revenue before competitors exit legacy SKUs.

Latin America and the Middle East and Africa represent developing volume markets where food packaging consumption is rising alongside urbanization and modern retail expansion. Cold-chain build-out in GCC countries and Brazil’s growing supermarket penetration are generating incremental cling film demand in both regions. However, price sensitivity in these markets favors cost-competitive commodity film formats over premium recyclable or bio-based alternatives in the near term.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Drivers

Europe’s Packaging and Packaging Waste Regulation entered into force in February 2025 and begins applying from 12 August 2026. This regulation requires all packaging to achieve recyclability by 2030, restricts PFAS in food-contact packaging with thresholds of 25 ppb for any individual PFAS and 250 ppb for the sum of targeted PFAS, and introduces mandatory recycled-content criteria. For cling film suppliers, this shifts revenue from commodity roll output toward reformulated PE-based films, downgauged structures, and compliance documentation services that EU retailers and exporters now require.

Beyond Europe, urban ready-to-eat meal penetration is driving high-frequency cling film usage across household and institutional wrapping cycles. Supermarket-led fresh produce pre-packaging models are standardizing cling film consumption at retail shelf level in North America and APAC urban corridors. Cold-chain distribution network expansion for dairy, meat, and pharmaceutical products is increasing demand for high-barrier wrapping films in markets where perishable goods transport is scaling faster than existing packaging infrastructure.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Packaged food throughput and fresh-produce wrap intensity | +1.2% | North America core, EU, APAC urban corridors | Short term (≤ 2 years) |

| Supermarket deli, foodservice, and institutional hygiene demand | +0.8% | North America core, EU, GCC, Japan, Australia | Short term (≤ 2 years) |

| EU PPWR compliance pushing redesign, downgauging, and recyclable-film substitution | +1.0% | EU core, UK spill-over, export-oriented Turkey and North Africa suppliers | Medium term (2-4 years) |

| Recycled-content and EPR rules accelerating mono-material PE film adoption | +0.7% | India, EU, selected ASEAN, North America spill-over | Medium term (2-4 years) |

| Bio-based and compostable niche premiumization in food-contact wraps | +0.5% | EU premium retail, Japan, South Korea, selected North America natural-food channels | Long term (≥ 4 years) |

| E-grocery, cold-chain, and secondary food handling expansion | +0.6% | China, India metros, Southeast Asia, North America, Western Europe | Medium term (2-4 years) |

Restraints

Cling film converters purchase PE, PVC, and related inputs on volatile resin price cycles, yet downstream contracts typically allow price resets only within 60-day notice periods and price-revision ceilings in the 3% to 7% range. The U.S. PPI for coextruded single-web film stood at 183.285 in April 2026, while Indian PP postings showed increases of INR 2,000 to 4,000 per metric ton. This mismatch forces converters to absorb sudden resin cost movements before passing them through, compressing working capital and delaying line upgrades.

Regulatory phase-outs of single-use PVC-based films under plastic waste management frameworks in major economies are directly removing addressable volume for legacy product lines. Multi-layer polyethylene cling films face limited recyclability due to contamination issues and insufficient mechanical recycling infrastructure in most markets. Converters that have not yet invested in mono-material reformulation face growing revenue exposure as EU compliance deadlines approach and major retail procurement teams tighten their supplier sustainability requirements.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU recyclability compliance | -1.4% | EU core, UK spillover, export-to-EU suppliers | Medium term (2-4 years) |

| PFAS and food-contact reformulation | -0.9% | EU, India watchlist, global food-pack exporters | Short term (≤ 2 years) |

| Mono-material substitution pressure | -1.2% | North America core, EU, developed APAC | Medium term (2-4 years) |

| Resin-price pass-through mismatch | -1.0% | North America core, India, ASEAN converters | Short term (≤ 2 years) |

| PVC scrutiny in fatty-food uses | -0.8% | EU, Nordic markets, premium retail chains | Medium term (2-4 years) |

| Freight and import-cost volatility | -0.7% | APAC export corridors, MENA, Europe importers | Short term (≤ 2 years) |

Challenges

Food-contact compliance for cling films has become a multi-layered regulatory burden for manufacturers. Companies must simultaneously navigate EU food contact regulations, U.S. FDA requirements, evolving PFAS restrictions, and retailer-driven positive list requirements. The EU PFAS thresholds of 25 parts per billion for individual PFAS and 50 parts per million for total PFAS, effective August 2026, are forcing extensive screening of legacy additives including slip agents, anti-fog compounds, and processing aids across active product portfolios.

For manufacturers managing 200 to 300 SKUs, roughly 20% to 25% of formulations may require reformulation or re-evaluation. Each migration study and compliance test costs tens of thousands of dollars and takes 3 to 6 months to complete. Medium-sized converters managing 30 to 40 parallel compliance projects over 2 to 3 years face lab capacity strain that directly delays product launches and compresses available revenue windows in regulated export markets.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Volatile polyolefin feedstock | -1.2% | Global; APAC and NA resin hubs | Medium term (2-4 years) |

| Tightening recyclability mandates | -1.0% | EU regulatory hubs; US coastal states | Long term (≥ 4 years) |

| Food-contact compliance complexity | -0.8% | EU, North America, high-standard APAC | Medium term (2-4 years) |

| Converter margin compression | -0.9% | Global, especially fragmented APAC/LatAm | Medium term (2-4 years) |

| Post-consumer resin (PCR) constraints | -0.7% | EU, UK, US, developed APAC | Long term (≥ 4 years) |

| Logistics and lead-time volatility | -0.6% | APAC–EU/NA trade lanes; MENA | Short term (≤ 2 years) |

Opportunities

The EU Packaging and Packaging Waste Regulation creates a direct share dislocation opportunity for suppliers that proactively redesign portfolios before lagging SKUs exit compliance under August 2026 rules. Food-contact packaging made from non-PET plastics faces a 10% recycled-content target by 2030, while all packaging must advance toward recyclability grades A to C. Suppliers converting PVC-heavy or multi-material cling ranges into mono-PE or mono-PP, APR-compatible structures can command 300 to 700 basis points of gross-margin premium above commodity roll pricing.

Early movers in mono-material PPWR upgrade films can protect 15% to 25% of at-risk EU revenue and access a reformulation replacement pool covering roughly 20% to 30% of the region’s installed cling film SKU base. Capturing even one-third of this substitution window translates into approximately +1.4 percentage points of incremental growth above baseline. Bio-based compostable films, healthcare-grade antimicrobial wraps, and cold-chain e-grocery formats represent additional high-margin opportunity pools with short-to-medium execution windows for companies that already hold food-contact compliance certifications in target regions.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Mono-material PPWR upgrade films | +1.4% | EU core, UK, premium export Asia | Short term (≤ 2 years) |

| Cold-chain e-grocery wrap systems | +1.2% | North America, EU, APAC urban | Short term (≤ 2 years) |

| Healthcare & lab consumables films | +0.9% | North America core, EU, Japan, Korea | Medium term (2-4 years) |

| Bio-based compostable premium niche | +0.7% | EU, Japan, premium urban APAC | Medium term (2-4 years) |

| Private-label converter roll-up | +1.0% | India, SEA, LATAM, Eastern Europe | Medium term (2-4 years) |

| Smart dispensing & B2B service models | +0.8% | North America, EU foodservice, GCC | Long term (≥ 4 years) |

Key Company Insights

Berry Global Inc. built its competitive position through broad-based flexible film manufacturing scale, serving food, healthcare, and consumer goods segments across North America and internationally. In March 2025, Berry Global received U.S. antitrust clearance for its combination with Amcor, enabling final regulatory approval. This transaction restructures the competitive hierarchy of the cling films market by merging two of its largest volume producers into a single entity with global distribution reach.

According to UNEP, packaging accounts for approximately 36% of total plastics demand globally, making it the primary target for bioplastic substitution strategies. Amcor plc completed its all-stock acquisition of Berry Global in April 2025, significantly expanding its flexible packaging and cling film portfolio. Plastics Pacts initiatives report improving the recyclability of plastic packaging by 23% among participating businesses. Amcor’s scale and compliance infrastructure position it to capture premium margin on recyclable mono-material cling film formats as EU PPWR enforcement tightens.

Key Players

- Berry Global Inc.

- Mitsubishi Chemical Group Corporation

- Amcor plc

- Sealed Air

- Sigma Plastics Group

- Anchor Packaging LLC

- IPG

- POLIFILM

- Reynolds Consumer Products

- Greendot Biopak

- Zhengzhou Eming Aluminium Industry Co., Ltd.

- PRAGYA FLEXIFILM INDUSTRIES

- Other Key Players

Recent Developments

- April 2025 – Amcor completed its all-stock acquisition of Berry Global, significantly expanding its flexible packaging and cling film portfolio and creating one of the largest flexible film producers globally.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 3.0 Billion |

| Forecast Revenue (2035) | USD 4.6 Billion |

| CAGR (2026-2035) | 4.5% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Material (Polyvinyl Chloride (PVC), Polyethylene (PE), Polypropylene (PP), Polyvinylidene Chloride (PVDC), Others including Bio-based PLA Films and Starch-blend Compostable Wraps); By End Use Industry (Food and Beverages, Healthcare, Consumer Goods, Other End User); By Distribution Channel (Offline, Online) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Berry Global Inc., Mitsubishi Chemical Group Corporation, Amcor plc, Sealed Air, Sigma Plastics Group, Anchor Packaging LLC, IPG, POLIFILM, Reynolds Consumer Products, Greendot Biopak, Zhengzhou Eming Aluminium Industry Co., Ltd., PRAGYA FLEXIFILM INDUSTRIES, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |