Quick Navigation

Report Overview

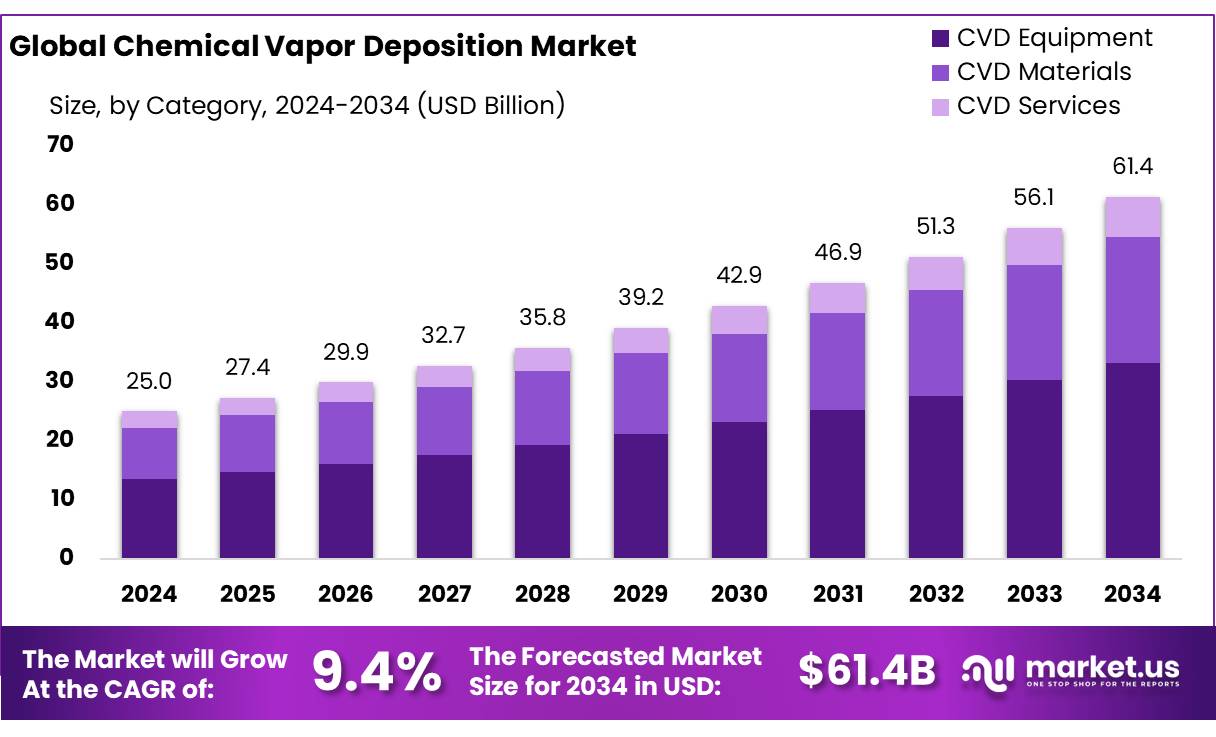

The Global Chemical vapor deposition Market size is expected to be worth around USD 61.4 Bn by 2034, from USD 25 Bn in 2024, growing at a CAGR of 9.4% during the forecast period from 2025 to 2034.

Chemical Vapor Deposition (CVD) is a widely used technique in material science and semiconductor industries to produce high-performance thin films, coatings, and advanced materials. The CVD process involves the chemical reaction of gaseous precursors in a vacuum chamber to form solid materials that are deposited onto a substrate. CVD is employed in a variety of applications, including semiconductor manufacturing, photovoltaic cells, coatings for industrial tools, and the production of carbon-based materials such as graphene and carbon nanotubes.

Growing investments in the semiconductor and electronics sectors are major contributors to the expansion of the CVD market. As the demand for smaller, faster, and more efficient electronic devices continues to rise, the need for advanced materials and coatings that can withstand increasingly demanding operational environments grows.

Another key driver for the growth of the CVD market is the increasing adoption of CVD in the production of coatings for aerospace, automotive, and industrial applications. CVD coatings are used to enhance the performance of critical components, such as turbine blades, automotive engine parts, and cutting tools. These coatings provide superior resistance to wear, corrosion, and high temperatures, making them ideal for industries where materials must perform under extreme conditions.

Several future growth factors are expected to influence the Chemical Vapor Deposition market. One of the most important factors is the continuous advancement in CVD technologies, such as the development of low-pressure and atomic layer deposition (ALD) techniques, which enable more precise control over material deposition and thickness. These advancements are likely to expand the range of applications for CVD, particularly in fields like nanotechnology and biotechnology, where high-precision material deposition is critical.

Key Takeaways

- Chemical vapor deposition Market size is expected to be worth around USD 61.4 Bn by 2034, from USD 25 Bn in 2024, growing at a CAGR of 9.4%.

- CVD Equipment held a dominant market position, capturing more than 53.4% of the global chemical vapor deposition (CVD) market share.

- Silicon Wafers held a dominant market position, capturing more than 47.5% of the global chemical vapor deposition (CVD) market share.

- Thermal CVD held a dominant market position, capturing more than 46.4% of the global chemical vapor deposition (CVD) market share.

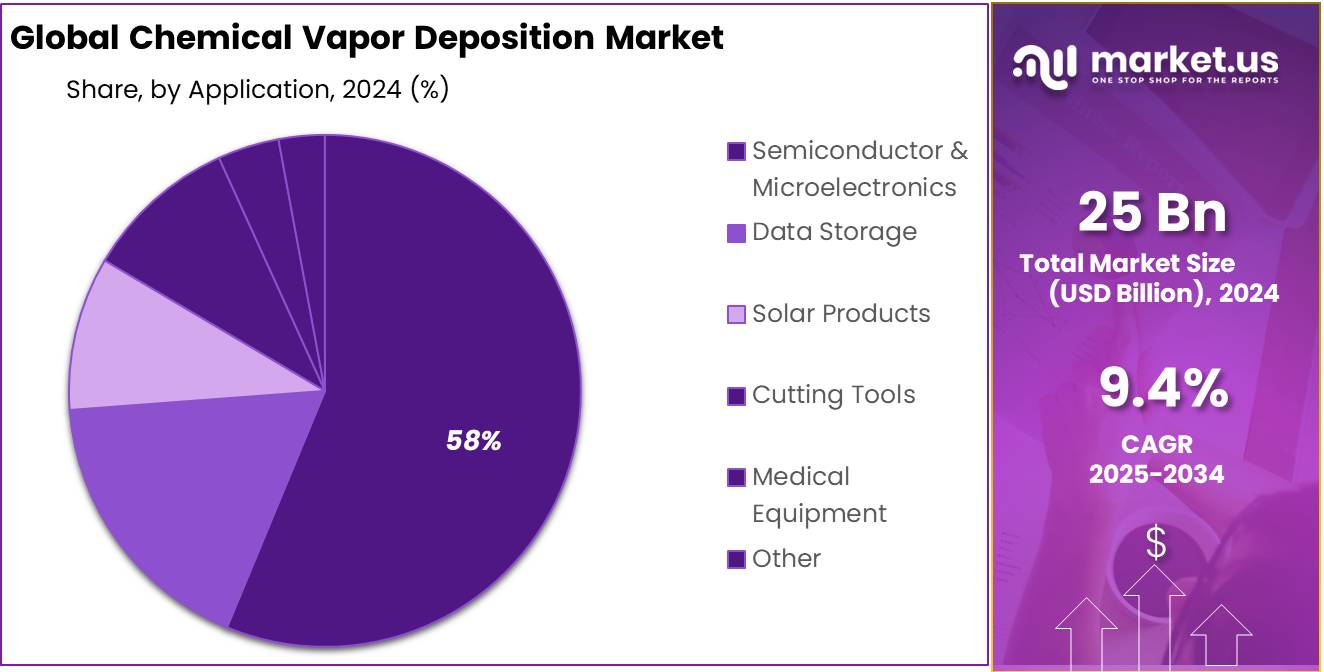

- Semiconductor & Microelectronics held a dominant market position, capturing more than 58.4% of the global chemical vapor deposition (CVD) market share.

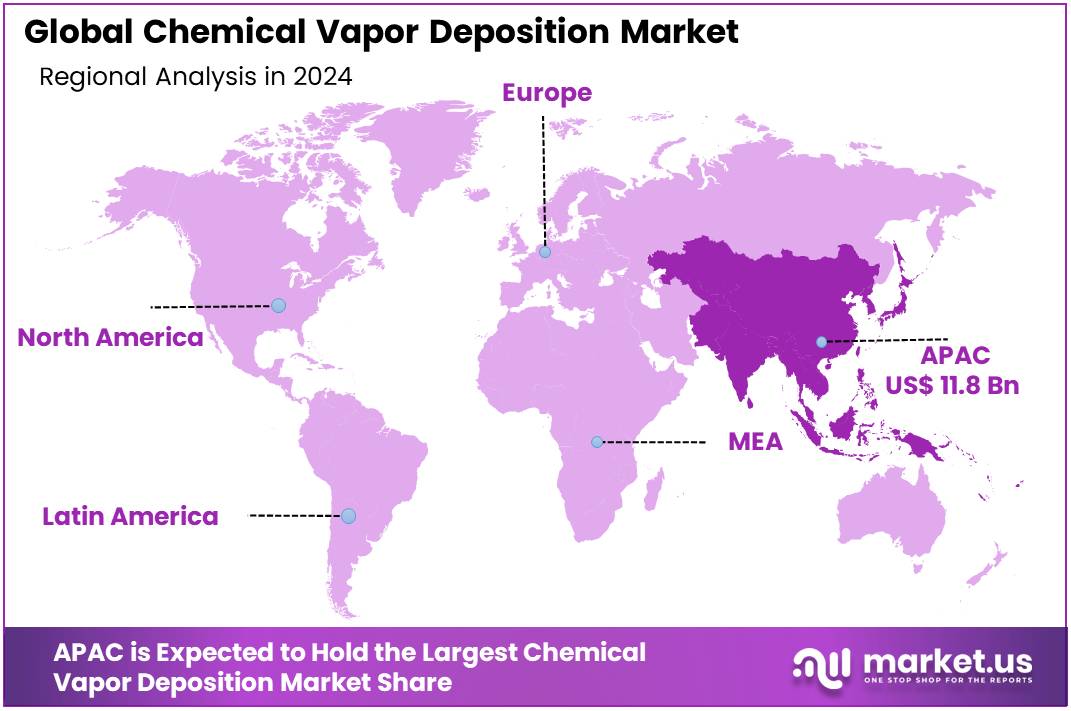

- Asia Pacific (APAC) holds a dominant position in the global Chemical Vapor Deposition (CVD) market, capturing more than 47.8% of the total market share, valued at approximately $11.8 billion.

By Category

In 2024, CVD Equipment held a dominant market position, capturing more than 53.4% of the global chemical vapor deposition (CVD) market share. This segment’s leading position is largely due to the growing demand for high-precision manufacturing equipment used in industries such as electronics, semiconductor production, and solar panels.

In the same year, CVD Materials are also expected to see steady growth, driven by the increasing application of these materials in electronics and energy sectors. However, the CVD Equipment segment continues to dominate due to its higher market share and the essential role it plays in the CVD process.

CVD Services, while crucial for specialized processes, occupies a smaller share in the market. These services are increasingly being outsourced to third-party providers that offer tailored CVD solutions for specific industrial needs.

By Type

In 2024, Silicon Wafers held a dominant market position, capturing more than 47.5% of the global chemical vapor deposition (CVD) market share. The high demand for silicon wafers is driven by their essential role in the semiconductor industry, where they are used in the manufacturing of integrated circuits (ICs) and other electronic components.

Following Silicon Wafers, Glass holds a significant portion of the market. The use of CVD to deposit thin films on glass is growing, particularly in applications related to solar panels, display technologies, and architectural glass coatings. The Glass segment is expected to continue expanding in 2024, driven by innovations in energy-efficient windows and displays, as well as the increasing deployment of solar photovoltaic cells, where glass plays a critical role.

Metals, Ceramics, and Polymers each contribute to the market in specific industrial applications, though at a smaller scale compared to silicon and glass. Metals are used in the aerospace, automotive, and electronics industries for coatings that provide improved wear resistance and conductivity. Ceramics are gaining traction in industries like automotive and power generation, where they are used for components that require high temperature and wear resistance.

By Technology

In 2024, Thermal CVD held a dominant market position, capturing more than 46.4% of the global chemical vapor deposition (CVD) market share. This technology remains the preferred method for producing thin films and coatings in industries such as semiconductors, solar energy, and automotive. Thermal CVD is valued for its simplicity and ability to produce high-quality films with excellent uniformity and control.

Plasma-Enhanced CVD (PECVD) is also experiencing significant growth. PECVD allows for lower processing temperatures and is widely used in applications where heat-sensitive materials are involved. It is increasingly being used in the production of thin films for solar cells, microelectronics, and MEMS (Microelectromechanical Systems). This technology is expected to see continued growth in 2024, particularly as the demand for flexible and lightweight electronics increases.

Metalorganic CVD (MOCVD) is gaining momentum as well, driven by its crucial role in the production of high-performance materials like gallium nitride (GaN) and indium phosphide (InP), which are used in LEDs, lasers, and power electronics.

Atomic Layer Deposition (ALD) and Molecular Beam Epitaxy (MBE) are more specialized technologies, with a focus on precision and nanoscale material deposition. While these technologies occupy a smaller share of the market, they are gaining traction in high-tech industries that require atomic-level control, such as in the production of advanced semiconductors and nanomaterials.

By Application

In 2024, Semiconductor & Microelectronics held a dominant market position, capturing more than 58.4% of the global chemical vapor deposition (CVD) market share. This sector continues to be the largest driver of CVD technology, primarily due to the critical role CVD plays in the fabrication of advanced semiconductors and microelectronic components.

Data Storage is also experiencing steady growth in 2024, driven by the increasing demand for high-performance storage devices. CVD technology is used to deposit films that improve the durability and efficiency of storage components, particularly in hard drives and solid-state drives (SSDs).

Solar Products are seeing a rise in CVD applications, as the demand for thin-film solar cells and other renewable energy technologies increases. The need for sustainable energy sources is pushing the market for solar products, where CVD is used to deposit materials like silicon for solar cells.

Cutting Tools and Medical Equipment are niche yet important sectors for CVD. In cutting tools, CVD coatings are essential for enhancing the durability and performance of industrial tools. In the medical equipment industry, CVD is used for coating surgical instruments, implants, and devices to improve their performance and biocompatibility.

Key Market Segments

By Category

- CVD Equipment

- CVD Materials

- CVD Services

By Type

- Silicon Wafers

- Glass

- Metals

- Ceramics

- Polymers

By Technology

- Thermal CVD

- Plasma-Enhanced CVD

- Metalorganic CVD

- Atomic Layer Deposition

- Molecular Beam Epitaxy

By Application

- Semiconductor & Microelectronics

- Data Storage

- Solar Products

- Cutting Tools

- Medical Equipment

- Others

Drivers

Growing Demand for Advanced Materials in the Food Packaging Industry

One of the major driving factors for the Chemical Vapor Deposition (CVD) market is the increasing demand for advanced materials in the food packaging industry. CVD is a process widely used to create thin films, coatings, and surface modifications on various materials, which is critical for food packaging. The need for improved food packaging solutions is growing as consumer preferences shift towards more sustainable, durable, and safe packaging options. The technology used in CVD allows manufacturers to apply coatings that enhance the barrier properties of packaging materials, improve shelf-life, and reduce spoilage, all of which are essential for food products.

The food packaging industry is heavily influenced by evolving consumer expectations for longer-lasting freshness and safer food. CVD coatings are used to enhance the strength and resistance of packaging materials to external factors like moisture, oxygen, and light. As per a report by the Food Packaging Forum (FPF), food packaging materials with advanced coatings can reduce waste by extending shelf life and improving the protection of the contents, thus contributing to sustainability goals. For instance, packaging with better moisture barriers can significantly reduce food wastage, a concern that is increasingly being recognized by both manufacturers and consumers.

According to the Food and Agriculture Organization (FAO), approximately one-third of all food produced globally is wasted, much of it due to inadequate packaging. By using CVD to improve packaging materials, companies can help mitigate this problem. The FAO and United Nations have emphasized the role of advanced materials in reducing food waste through improved packaging systems.

This growing focus on sustainable packaging, backed by government initiatives and industry collaboration, is propelling the adoption of CVD technologies in the food packaging sector, offering significant growth opportunities for businesses involved in this field.

Restraints

High Operational Costs Limiting Adoption of Chemical Vapor Deposition Technology

One of the significant restraining factors for the widespread adoption of Chemical Vapor Deposition (CVD) technology is its high operational costs. While CVD offers substantial benefits in creating high-performance coatings for a wide range of applications, the initial setup and ongoing operational costs can be prohibitive for smaller businesses and industries. The technology requires specialized equipment, high energy consumption, and strict environmental controls, all of which contribute to the overall expenses.

For example, the energy costs associated with running CVD reactors can be significant. According to a report by the International Energy Agency (IEA), industrial processes, including those that utilize CVD, account for around 30% of global industrial energy use, with certain high-temperature processes requiring even more energy to maintain the necessary reaction conditions. This has raised concerns among companies looking to adopt CVD technology, especially in sectors like food packaging and food processing, where cost-effectiveness is crucial to maintaining competitive pricing.

Additionally, the need for highly skilled personnel to operate and maintain CVD systems adds to the costs. The complex nature of the process means that manufacturers must invest in training or hire experts, further increasing operational expenses. A report from the U.S. Department of Energy highlights that the adoption of energy-efficient technologies in industries such as food production and packaging has been slower due to the initial capital investment required, even though these technologies can result in long-term savings.

While government initiatives are pushing for more sustainable practices, such as the U.S. Department of Agriculture (USDA) promoting energy efficiency in food manufacturing, the cost barrier remains a challenge. For instance, the USDA’s Energy Efficiency Improvement Program aims to reduce energy usage in food processing by up to 25% but does not fully offset the high costs associated with technologies like CVD.

Opportunity

Expansion in Sustainable Food Packaging Solutions

A major growth opportunity for the Chemical Vapor Deposition (CVD) market lies in the increasing demand for sustainable food packaging solutions. With the rising global awareness about environmental issues, industries are under growing pressure to reduce plastic waste and improve the sustainability of their operations. CVD technology can play a crucial role in meeting this demand by enabling the production of advanced, eco-friendly coatings for food packaging materials. These coatings improve the durability, barrier properties, and shelf life of packaging materials, all while reducing the need for excessive plastic use.

The global shift towards reducing plastic waste, especially in the food industry, has created significant opportunities for CVD applications. In fact, according to a report by the Food and Agriculture Organization (FAO), packaging accounts for about 15-20% of the total food waste, often due to inefficient packaging materials that fail to protect food products from external elements like moisture and air. By enhancing the barrier properties of packaging materials through CVD, manufacturers can significantly reduce food spoilage, thereby reducing waste and improving food security.

Additionally, initiatives like the European Union’s “Green Deal” and the U.S. Environmental Protection Agency’s (EPA) “Sustainable Materials Management” program are providing a regulatory push for industries to adopt more sustainable packaging solutions. These initiatives encourage the use of innovative technologies like CVD to create sustainable, recyclable, and biodegradable food packaging. The FAO also estimates that the food industry could cut packaging-related waste by up to 50% by using more advanced materials, potentially generating billions of dollars in savings.

As consumers continue to demand more eco-conscious packaging, and with government incentives driving the adoption of sustainable practices, CVD technology is poised for growth. This demand, combined with environmental regulations and sustainability goals, makes CVD an increasingly valuable tool in the food packaging industry.

Trends

Emergence of Eco-Friendly and Biodegradable Coatings in Food Packaging

A major trend currently shaping the Chemical Vapor Deposition (CVD) market is the growing focus on eco-friendly and biodegradable coatings, particularly in food packaging. As concerns about plastic pollution and environmental sustainability continue to rise, the food industry is increasingly turning to innovative materials that reduce waste and support sustainable practices. CVD technology is at the forefront of this shift, enabling the application of high-performance, biodegradable coatings that improve the functionality of packaging while being less harmful to the environment.

One of the driving forces behind this trend is the push for reducing plastic use in food packaging, which accounts for a significant portion of global plastic waste. According to the World Economic Forum (WEF), around 8 million tons of plastic enter the oceans every year, much of it from food and beverage packaging. In response, the European Union’s Green Deal aims to make all plastic packaging recyclable or reusable by 2030. This has led many food companies to explore CVD as a way to apply environmentally friendly coatings to packaging materials, such as paper, glass, and plant-based plastics, while maintaining their durability and shelf life.

CVD coatings used in food packaging are not only enhancing the materials’ resistance to moisture, oxygen, and light but also making them more biodegradable. These advancements contribute to reducing food spoilage and waste. For instance, the U.S. Department of Agriculture (USDA) reports that food packaging innovations could help reduce food waste, which is estimated at 30-40% of the total food supply. By extending shelf life with sustainable coatings, CVD helps lower both waste and environmental impact.

With government incentives like the USDA’s Sustainable Agriculture Research and Education (SARE) program promoting sustainability in food production and packaging, this trend is expected to accelerate. The continued development and adoption of CVD-based biodegradable coatings will play a key role in shaping the future of food packaging.

Regional Analysis

In 2024, Asia Pacific (APAC) holds a dominant position in the global Chemical Vapor Deposition (CVD) market, capturing more than 47.8% of the total market share, valued at approximately $11.8 billion. This region’s leadership is primarily driven by its robust semiconductor industry, with countries like China, South Korea, and Taiwan being key manufacturing hubs for electronic devices, microchips, and advanced materials.

In North America, the CVD market is experiencing steady growth, with the United States driving demand due to its well-established semiconductor and electronics manufacturing sectors. The increasing need for solar energy applications and advanced materials is further pushing market adoption. While North America holds a significant share of the market, its portion is relatively smaller compared to APAC, reflecting the region’s focus on research, development, and innovation rather than large-scale manufacturing.

Europe is also a notable player in the CVD market, with key countries like Germany and France driving technological advancements in semiconductors and solar technology. However, Europe holds a smaller market share than APAC and North America but is expected to see steady growth, driven by the increasing push for clean energy technologies and industry 4.0.

Middle East & Africa and Latin America are emerging markets for CVD technology, but their contribution remains limited due to less developed manufacturing sectors and lower adoption rates for advanced technologies compared to the other regions.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The Chemical Vapor Deposition (CVD) market is highly competitive, with several key players leading the industry in terms of innovation and market share. CVD Equipment Corporation is a prominent player known for its specialized equipment used in the deposition of thin films for semiconductors and solar cells. Similarly, Tokyo Electron Limited and Veeco Instruments Inc. are major contributors to the CVD equipment segment, focusing on the development of cutting-edge tools and technologies used in semiconductor manufacturing.

Plasma-Therm LLC and Applied Materials, Inc. are renowned for their role in the semiconductor and electronics sectors, providing specialized CVD equipment for the deposition of materials like silicon nitride and silicon carbide, which are critical for high-performance electronic devices. OC Oerlikon Management AG and ULVAC Inc. are key players in vacuum deposition systems, supporting the growing demand for advanced coatings and materials used in solar power and electronics applications.

Top Key Players

- CVD Equipment Corporation

- Tokyo Electron Limited.

- IHI Corporation

- Veeco Instruments Inc.

- ASM International N.V.

- Plasma-Therm LLC

- Applied Materials, Inc.

- OC Oerlikon Management AG

- voestalpine AG

- ULVAC Inc.

- Aixtron SE

- TAIYO NIPPON SANSO CORPORATION

- LPE

- Nuflare Technology Inc.

- RIBER

Recent Developments

Tokyo Electron’s systems are known for their precision, reliability, and ability to handle a wide range of materials such as silicon, gallium nitride, and silicon carbide, which are critical for producing high-performance semiconductor devices.

In 2024, IHI is expected to continue to enhance its market presence with a strong focus on CVD equipment used in semiconductor manufacturing, solar energy production, and advanced coatings.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 25.0 Bn |

| Forecast Revenue (2034) | USD 61.4 Bn |

| CAGR (2025-2034) | 9.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Category (CVD Equipment, CVD Materials, CVD Services), By Type (Silicon Wafers, Glass, Metals, Ceramics, Polymers), By Technology (Thermal CVD, Plasma-Enhanced CVD, Metalorganic CVD, Atomic Layer Deposition, Molecular Beam Epitaxy), By Application (Semiconductor and Microelectronics, Data Storage, Solar Products, Cutting Tools, Medical Equipment, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | CVD Equipment Corporation, Tokyo Electron Limited., IHI Corporation, Veeco Instruments Inc., ASM International N.V., Plasma-Therm LLC, Applied Materials, Inc., OC Oerlikon Management AG, voestalpine AG, ULVAC Inc., Aixtron SE, TAIYO NIPPON SANSO CORPORATION, LPE, Nuflare Technology Inc., RIBER |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |