Global Canned Food Market Size, Share, And Business Benefits By Product (Canned Fruits and Vegetables, Canned Meat Products, Canned Fish/Seafoods, Canned Ready Meals, Canned Condiments, Others), By Type (Organic, Conventional), By Packaging Material (Metal, Plastic, Glass, Others), By Distribution Channel (Food Service, Retail (Hypermarkets and Supermarkets, Convenience Stores, Online, Others)), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends, and Forecast 2025-2034

- Published date: April 2025

- Report ID: 146007

- Number of Pages: 247

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

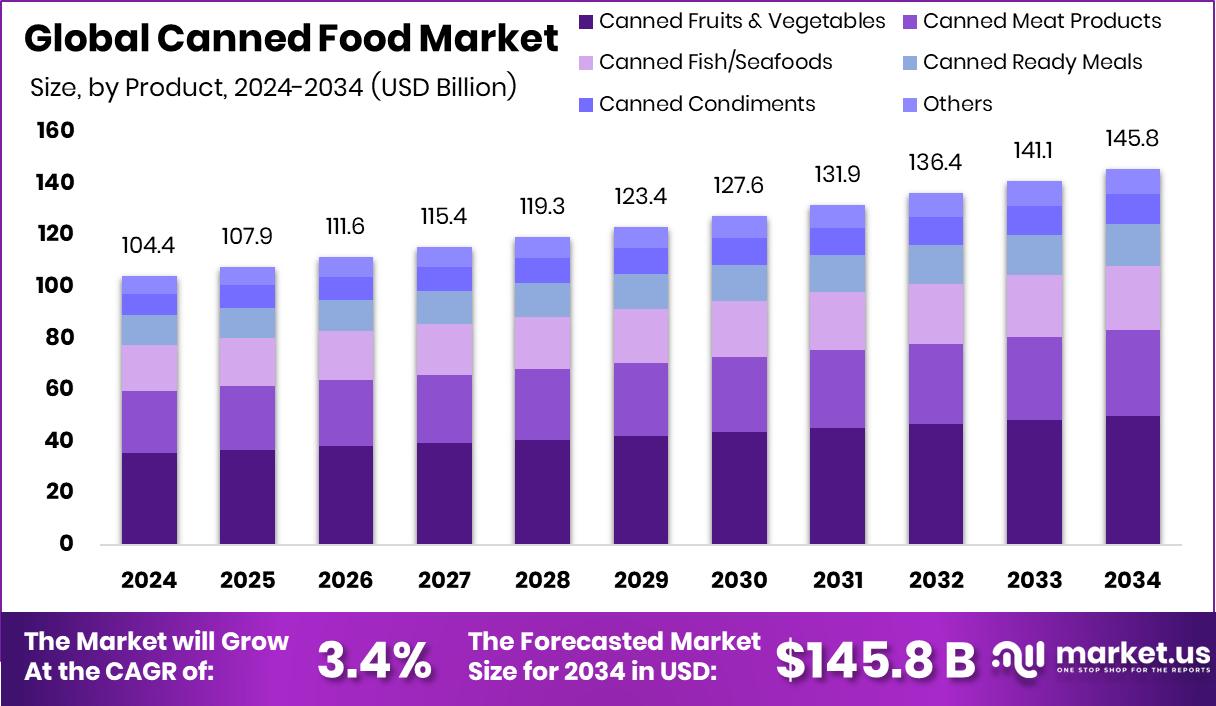

Global Canned Food Market is expected to be worth around USD 145.8 billion by 2034, up from USD 104.4 billion in 2024, and grow at a CAGR of 3.4% from 2025 to 2034. With USD 44 billion in revenue, Europe led the global canned food sector.

Canned food refers to edible items that are preserved and sealed in airtight containers, usually metal cans, to extend shelf life and prevent spoilage. This method of food preservation locks in taste, nutrients, and freshness, allowing products like vegetables, fruits, meats, beans, and ready-to-eat meals to remain consumable for months or even years. It’s a popular choice for convenience, especially among consumers with busy lifestyles or limited access to fresh produce.

The canned food market includes the global trade and retail of sealed, long-lasting food items distributed through supermarkets, convenience stores, online platforms, and food service outlets. This market serves both households and institutional buyers, driven by consumer demand for ready-to-use products, longer storage options, and affordable meal solutions. It covers various product segments, such as canned seafood, soups, fruits, vegetables, and meat-based meals, and operates in developed and developing regions.

Urbanization, changing dietary habits, and the increasing participation of women in the workforce have spurred growth in canned food consumption. Consumers prefer time-saving meals that require minimal preparation. Additionally, improvements in canning technology and food safety regulations have enhanced product appeal and shelf stability, further supporting market expansion across income groups.

The demand for canned food is steadily rising, especially in regions with limited access to fresh food year-round. Emergency preparedness, military consumption, and on-the-go lifestyles contribute to its continued popularity. Canned proteins and vegetables, particular, have witnessed strong demand in both household and commercial settings due to their affordability and availability.

The Ministry of Food Processing Industries (MoFPI) offers subsidies ranging from 35% to 50% for food processing units, including canned food production. The subsidy is capped at ₹5 crore, depending on the project type and location. Additionally, NABARD supports such initiatives through term loans under a ₹2,000 crore fund aimed at food processing units within designated Food Parks.

These loans cover up to 95% of project costs for government-promoted entities and up to 75% for other organizations. Furthermore, the scheme has allocated ₹6,000 crore for developing agro-processing clusters, offering grants up to 35% for eligible projects. These grants focus on critical areas such as sorting, grading, cold storage, and branding support for processed foods, including canned items.

Key Takeaways

- Global Canned Food Market is expected to be worth around USD 145.8 billion by 2034, up from USD 104.4 billion in 2024, and grow at a CAGR of 3.4% from 2025 to 2034.

- In 2024, canned fruits and vegetables held a 34.2% share in the product-wise canned food market.

- Conventional canned food products dominated with an 87.3% market share, reflecting consumer preference for traditional options.

- Metal packaging remained the top choice, accounting for 67.4% of the canned food market packaging material.

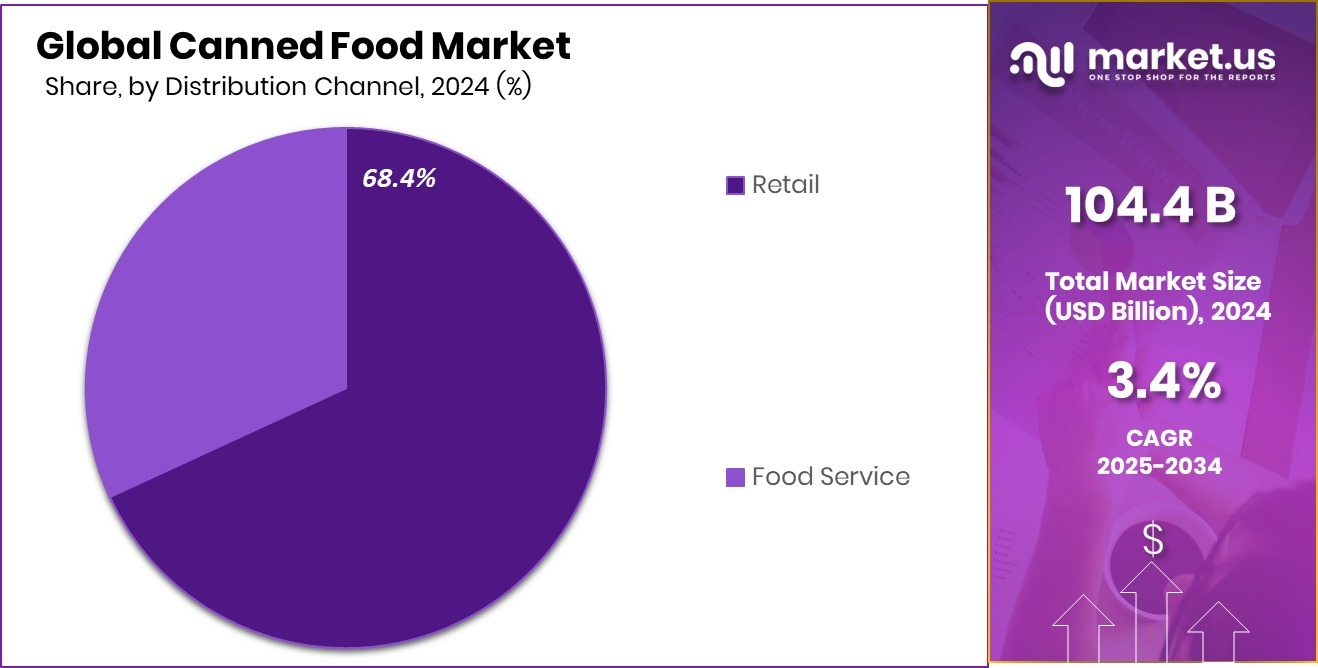

- Retail distribution led the market with a 68.4% share, driven by strong supermarket and grocery store sales.

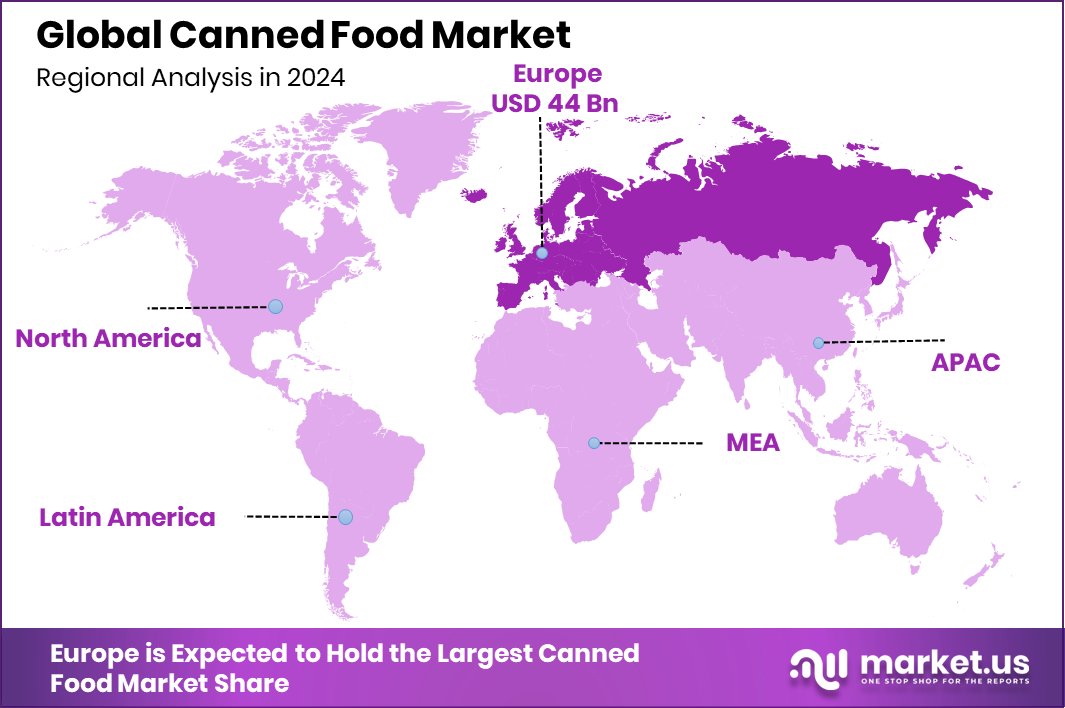

- Europe’s canned food grew steadily, securing 42.20% of the global market value.

By Product Analysis

In 2024, canned fruits and vegetables led with a 34.2% market share.

In 2024, Canned Fruits and Vegetables held a dominant market position in the By-Product segment of the Canned Food Market, with a 34.2% share. This segment led the market due to the rising demand for affordable, long-lasting produce options that do not require refrigeration.

Consumers in both urban and semi-urban areas increasingly turned to canned fruits and vegetables as a reliable alternative to fresh items, particularly in regions facing seasonal supply gaps or inconsistent cold chain infrastructure.

Busy households and working individuals favored these products for their convenience, extended shelf life, and reduced food wastage. Canned vegetables such as sweet corn, peas, and beans, along with fruits like peaches and pineapples, saw consistent consumption patterns in daily meals and quick recipes. Government food support programs and institutional use in schools and hospitals also contributed to stable demand.

Moreover, the segment benefited from a strong retail presence, with prominent visibility across supermarkets, small stores, and online platforms. The adaptability of canned produce in various cuisines and its suitability for bulk storage further reinforced its market leadership.

By Type Analysis

Conventional canned food types held a dominant 87.3% share in global sales.

In 2024, Conventional held a dominant market position in the By Type segment of the Canned Food Market, with a 34.2% share. This segment led the market owing to its affordability, wide availability, and established consumer acceptance. Conventional canned food continues to be a staple in many households due to its cost-effective nature and ease of storage, especially in regions where refrigeration or fresh supply is limited.

The dominance of conventional products is further supported by large-scale production and distribution networks that cater to both urban and rural markets. Consumers rely on these offerings for basic meals, emergency food kits, and pantry stocking. Traditional varieties such as canned tuna, beans, soups, and fruits remain high in volume sales across retail and institutional buyers.

Bulk purchasing for schools, catering services, and government food relief programs has also contributed to the segment’s performance. While there is a growing interest in organic and premium canned alternatives, conventional canned food maintains its strong position due to price sensitivity and consistent taste preferences.

By Packaging Material Analysis

Metal packaging remained the top choice, accounting for 67.4% market preference.

In 2024, Metal held a dominant market position in the By Packaging Material segment of the Canned Food Market, with a 67.4% share. This strong lead is attributed to metal’s durability, excellent barrier properties, and long-established use in food preservation. Metal cans, especially tin-plated steel and aluminum, are widely preferred for packaging various canned products, including vegetables, meats, seafood, and soups, due to their resistance to contamination and extended shelf life.

The dominance of metal packaging is also driven by its compatibility with high-heat sterilization, essential for ensuring product safety during long storage periods. Its tamper-proof nature adds to consumer confidence, especially in mass-produced goods. Metal packaging supports large-scale logistics and storage needs, making it a preferred choice for both retail and institutional supply chains.

Recyclability and established collection systems for metal waste have further supported its continued usage despite the emergence of alternative packaging formats. With the growing demand for safe, shelf-stable, and bulk food products, metal packaging remains integral to meeting consumer and commercial requirements.

By Distribution Channel Analysis

Retail outlets dominated distribution, capturing a 68.4% share in the canned food market.

In 2024, Retail held a dominant market position in the By Distribution Channel segment of the Canned Food Market, with a 68.4% share. This leading position reflects the strong consumer preference for purchasing canned food through supermarkets, hypermarkets, convenience stores, and grocery outlets. Retail channels offer extensive product visibility, easy accessibility, and frequent promotional deals that attract budget-conscious and impulse buyers alike.

The dominance of retail is also supported by the wide shelf presence of canned fruits, vegetables, meats, and ready-to-eat meals in physical stores. Consumers value the ability to inspect packaging, compare brands, and buy in bulk for household stocking. Retail stores continue to be the go-to option for both planned shopping and emergency purchases, particularly in urban and semi-urban areas.

Additionally, the growth of private-label canned goods through retail outlets has helped reinforce loyalty and affordability, increasing the segment’s overall volume. While online grocery platforms are growing, physical retail remains the most trusted and widely used channel for canned food purchases. The strategic placement of canned products near checkout lanes and high-traffic store sections further boosts consumer engagement.

Key Market Segments

By Product

- Canned Fruits and Vegetables

- Canned Meat Products

- Canned Fish/Seafoods

- Canned Ready Meals

- Canned Condiments

- Others

By Type

- Organic

- Conventional

By Packaging Material

- Metal

- Plastic

- Glass

- Others

By Distribution Channel

- Food Service

- Retail

- Hypermarkets and Supermarkets

- Convenience Stores

- Online

- Others

Driving Factors

Rising Urban Lifestyles Drive Convenient Food Choices

One of the major driving factors of the canned food market is the fast-paced urban lifestyle. As more people live in cities and work longer hours, they are looking for quick and easy meal solutions. Canned food offers ready-to-use options that save time on cooking and meal preparation. It is also easy to store and does not spoil quickly, making it ideal for busy individuals and families.

With the increasing number of working professionals, dual-income households, and students living independently, the demand for shelf-stable, convenient foods continues to rise. This shift in lifestyle patterns is significantly contributing to the growing popularity and consistent sales of canned food across both developed and developing regions.

Restraining Factors

Health Concerns Over Preservatives Limit Market Growth

One key restraining factor for the canned food market is growing health concerns related to preservatives and additives. Many consumers are becoming more aware of the ingredients in packaged foods and are actively avoiding items with high sodium, sugar, or artificial chemicals.

Canned foods often use preservatives to extend shelf life, which can raise red flags among health-conscious buyers. Additionally, concerns about Bisphenol A (BPA) in metal can linings have made some shoppers hesitant to choose canned products.

As demand for fresh, organic, and minimally processed foods increases, this negative perception can impact sales. Health trends are pushing consumers to explore other packaging formats and fresher alternatives, which may challenge the long-term growth of canned food products.

Growth Opportunity

Growing Demand for Organic and Healthy Canned Options

A significant growth opportunity in the canned food market lies in the increasing consumer demand for organic and healthier products. As more people become health-conscious, there’s a noticeable shift toward foods that are free from synthetic additives and preservatives. Canned food manufacturers are responding by introducing organic varieties that cater to this preference. These products not only meet the desire for healthier options but also align with the convenience that canned foods offer.

The combination of health benefits and ease of use makes organic canned foods particularly appealing to busy individuals and families. As this trend continues, it presents a substantial opportunity for growth within the canned food sector, encouraging innovation and expansion in product offerings.

Latest Trends

Eco-Friendly Packaging Is Gaining Big Attention

In 2024, one of the biggest trends in the canned food market is eco-friendly packaging. More companies are shifting to recyclable cans and BPA-free linings to attract health-conscious and environmentally aware consumers.

With growing pressure from governments and environmental groups, brands are now investing in sustainable materials like aluminum and biodegradable labels. This change not only helps the planet but also makes the brand look responsible, which boosts customer trust.

Many shoppers today check labels for environmental claims before buying. This trend is especially strong in Europe and North America, where green packaging is often linked to premium quality. Overall, sustainability is not just a bonus anymore—it’s becoming a key factor in canned food purchases.

Regional Analysis

In Europe, the canned food market reached USD 44 billion, capturing a 42.20% share.

In 2024, Europe held the dominant position in the global canned food market, accounting for 42.20% of the total market share, with an estimated valuation of USD 44 billion. This growth is driven by a strong demand for convenient, shelf-stable food options across countries like Germany, France, and the UK.

Consumers in Europe are increasingly favoring ready-to-eat meals due to fast-paced lifestyles and growing urban populations. North America also maintained a steady position in the global canned food industry, backed by consistent consumption across the U.S. and Canada. In the Asia Pacific region, the market showed signs of gradual expansion, particularly in countries like Japan and South Korea, where the preference for long-lasting packaged meals is increasing.

Middle East & Africa demonstrated moderate growth, supported by rising retail infrastructure and a growing working-class population. Latin America showed emerging potential, especially in urban centers across Brazil and Mexico, where demand for preserved food is growing in response to affordability and convenience.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, the global canned food market continues to be shaped by key players like Ayam Sarl, Bonduelle SA, and Bumble Bee Foods, each leveraging their unique strengths to navigate evolving consumer preferences and market dynamics.

Ayam Sarl has maintained its strong presence in Asia, offering a diverse range of canned products, including sardines, mackerel, tuna, baked beans, and coconut-based items. The brand’s commitment to quality, with products free from preservatives and certified halal, resonates well with health-conscious consumers. Its extensive distribution across over 30 countries, including Malaysia, Singapore, Japan, and parts of Europe, underscores its robust market penetration and adaptability to regional tastes.

Bonduelle SA, a French multinational, continues to lead in the plant-based food segment, specializing in canned, frozen, and fresh processed vegetables. With operations in over 100 countries and a portfolio of brands like Bonduelle, Cassegrain, and Arctic Gardens, the company emphasizes sustainable agriculture and innovation. Its strategic focus on ready-to-eat and convenience products aligns with the growing demand for healthy and quick meal solutions.

Bumble Bee Foods, headquartered in San Diego, California, remains a significant player in the canned seafood sector. Offering a wide array of products under brands such as Bumble Bee, Brunswick, and Clover Leaf, the company caters to a broad consumer base across North America and beyond. Its emphasis on sustainability and commitment to providing nutritious, protein-rich seafood options position it favorably amid increasing consumer awareness about health and environmental impact.

Top Key Players in the Market

- Ayam Sarl

- Bonduelle SA

- Bumble Bee Foods

- Campbell Soup Company

- CHB Group

- Conagra Brands, Inc.

- Del Monte Foods, Inc.

- Dole Food Company, Inc.

- Hormel Foods Corporation

- JBS S.A.

- Kraft Heinz Company

- Nestlé S.A

- Mitsubishi

- Thai Union Group PCL

- The Bolton Group

Recent Developments

- In August 2024, Bonduelle announced plans to sell its packaged salad business in France to Les Crudettes, a company of the LSDH Group. This decision was made in response to a decline in salad consumption in France and Germany, exacerbated by inflation and increased competition from private labels. The move is part of Bonduelle’s strategy to focus more on its canned and frozen food markets.

- In March 2024, Campbell Soup Company completed the acquisition of Sovos Brands, Inc. for approximately $2.7 billion. This acquisition added premium brands like Rao’s (pasta sauces), Michael Angelo’s (frozen Italian meals), and Noosa (yogurt) to Campbell’s portfolio. To support the growth of these brands, Campbell established a new business unit called “Distinctive Brands,” which also includes Pacific Foods

Report Scope

Report Features Description Market Value (2024) USD 104.4 Billion Forecast Revenue (2034) USD 145.8 Billion CAGR (2025-2034) 3.4% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product (Canned Fruits and Vegetables, Canned Meat Products, Canned Fish/Seafoods, Canned Ready Meals, Canned Condiments, Others), By Type (Organic, Conventional), By Packaging Material (Metal, Plastic, Glass, Others), By Distribution Channel (Food Service, Retail (Hypermarkets and Supermarkets, Convenience Stores, Online, Others)) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Ayam Sarl, Bonduelle SA, Bumble Bee Foods, Campbell Soup Company, CHB Group, Conagra Brands, Inc., Del Monte Foods, Inc., Dole Food Company, Inc., Hormel Foods Corporation, JBS S.A., Kraft Heinz Company, Nestlé S.A, Mitsubishi, Thai Union Group PCL, The Bolton Group Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Ayam Sarl

- Bonduelle SA

- Bumble Bee Foods

- Campbell Soup Company

- CHB Group

- Conagra Brands, Inc.

- Del Monte Foods, Inc.

- Dole Food Company, Inc.

- Hormel Foods Corporation

- JBS S.A.

- Kraft Heinz Company

- Nestlé S.A

- Mitsubishi

- Thai Union Group PCL

- The Bolton Group

Our Clients

- 146007

- April 2025