Quick Navigation

Report Overview

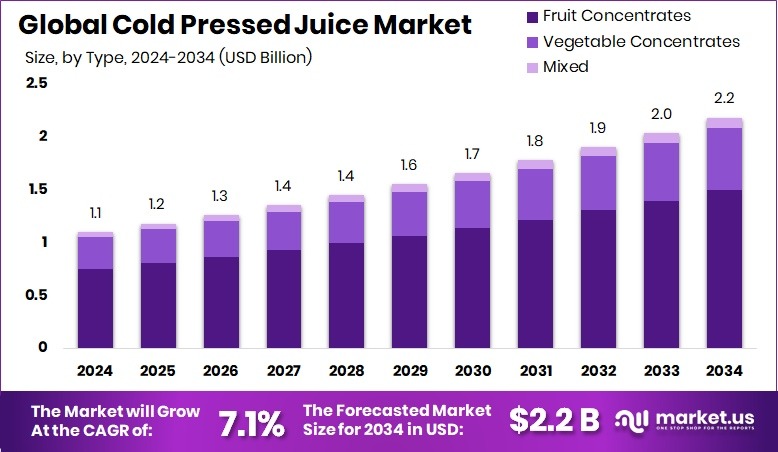

The Global Cold Pressed Juice Market is expected to be worth around USD 2.2 billion by 2034, up from USD 1.1 billion in 2024, and grow at a CAGR of 7.1% from 2025 to 2034. Rising health awareness in North America supported the USD 0.3 billion market growth.

Cold pressed juice is made by using a hydraulic press to extract juice from fruits and vegetables without heat. This method preserves the natural flavor, color, and nutrients, unlike traditional juicing, which can destroy enzymes and vitamins due to heat. The result is a raw, unpasteurized juice rich in antioxidants, minerals, and natural sugars, often favored by health-conscious consumers seeking clean, wholesome nutrition.

The cold-pressed juice market is steadily expanding as more people prioritize wellness and healthy lifestyles. Urban consumers are increasingly looking for fresh, minimally processed beverages, and cold-pressed juice fits that demand perfectly. Its appeal lies in transparency—short ingredient lists, no additives, and a focus on clean-label products. This is attracting millennials and Gen Z consumers, who often drive food and beverage trends.

One of the key growth factors is the rise of preventive healthcare. People want to support immunity and gut health naturally, and cold-pressed juice offers a convenient way to consume essential nutrients. The growing popularity of detox and cleansing routines also contributes to repeat purchases, especially among fitness enthusiasts.

Demand is also supported by changing eating habits and busy routines. Consumers want nutrition on the go, and ready-to-drink juices offer a fast, portable solution. With increasing awareness of the impact of diet on long-term health, demand is expected to remain strong. Florida’s Citrus Health Response Program received more than $20 million in funding for research and advertising in the fight against citrus greening.

Key Takeaways

- The Global Cold Pressed Juice Market is expected to be worth around USD 2.2 billion by 2034, up from USD 1.1 billion in 2024, and grow at a CAGR of 7.1% from 2025 to 2034.

- Fruit concentrates dominate the type segment with 68.50%, highlighting demand for natural and nutrient-rich juice bases.

- Conventional cold-pressed juices lead the category share at 67.30%, driven by affordability and wide-scale production methods.

- Bottled cold-pressed juices account for 74.20%, benefiting from convenience and consumer preference for ready-to-drink packaging.

- Glass packaging holds a 63.50% share, appealing to eco-conscious buyers seeking sustainable and premium beverage presentation.

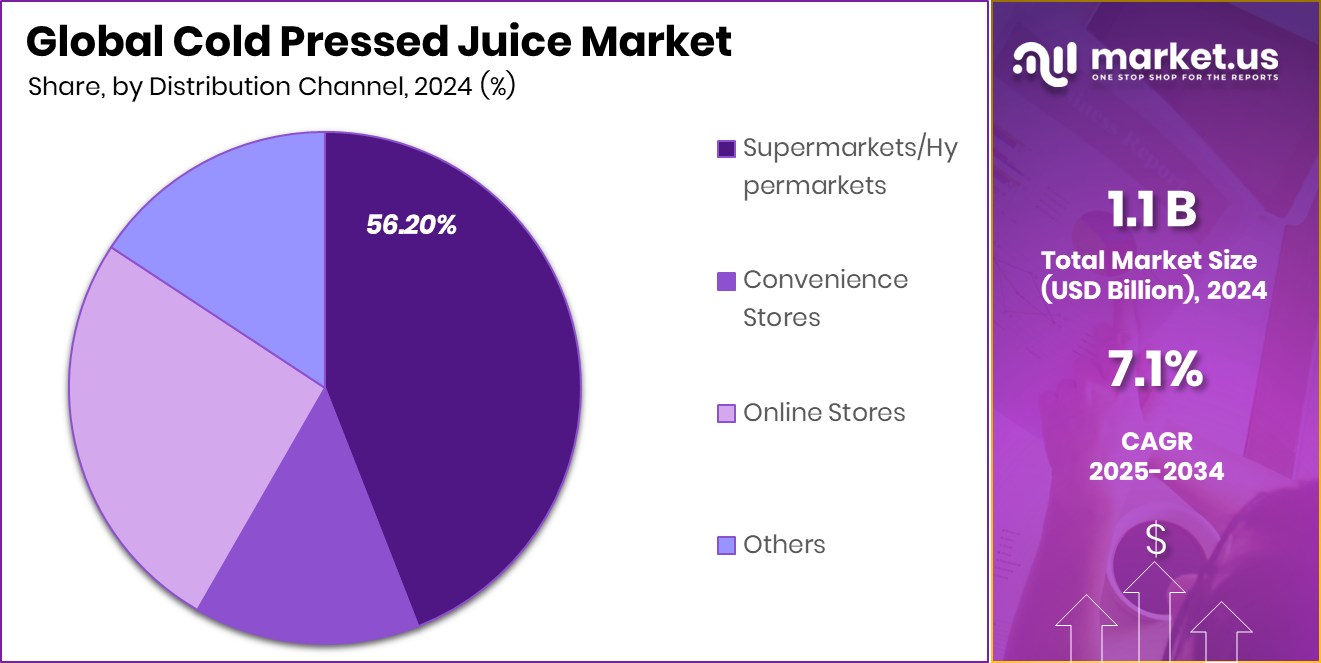

- Supermarkets and hypermarkets drive 56.20% of sales, offering visibility, variety, and ease of access to consumers.

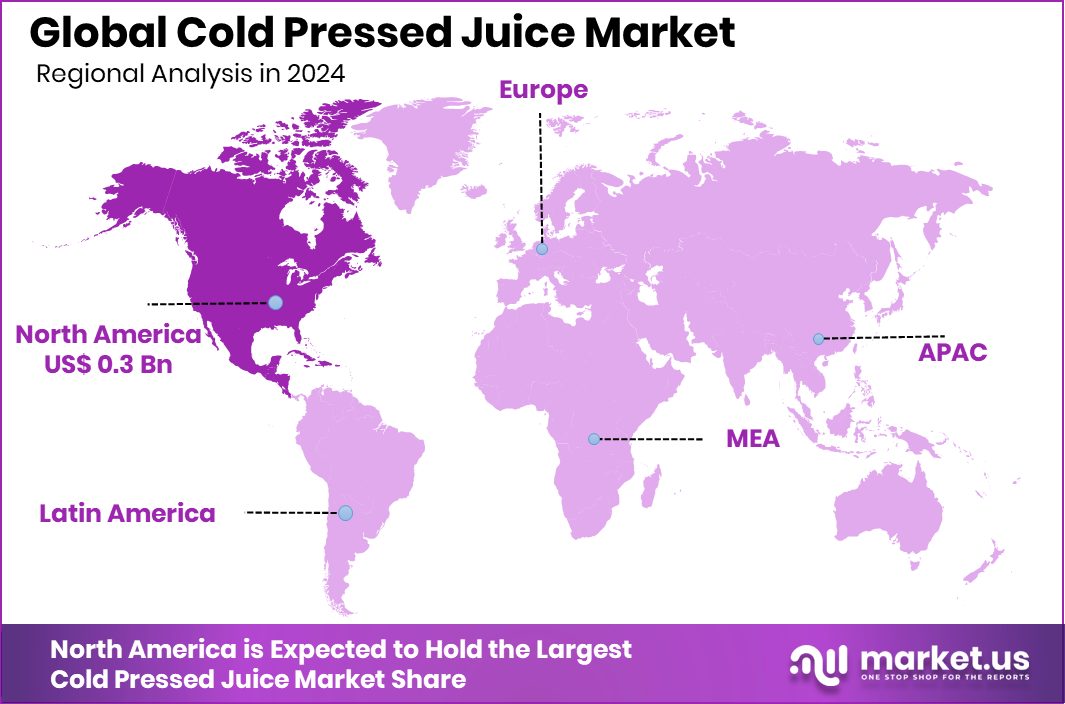

- The market in North America reached USD 0.3 billion in total value.

By Type Analysis

Fruit concentrates dominate cold cold-pressed juice market with a massive 68.50% type share.

In 2024, Fruit Concentrates held a dominant market position in the By Type segment of the Cold Pressed Juice Market, with a 68.50% share. This strong foothold was primarily driven by the widespread consumer preference for fruit-based beverages, owing to their natural sweetness, nutritional value, and refreshing taste.

The convenience of using fruit concentrates in large-scale production without compromising flavor or quality further enhanced their appeal among cold-pressed juice manufacturers. Additionally, fruit concentrates are easier to transport and store compared to fresh fruit juices, offering extended shelf life and cost efficiency, which favored their adoption by producers aiming to optimize logistics.

The high share was also supported by increased demand for juice blends made from apple, orange, pomegranate, and mixed berry concentrates, especially among health-conscious urban consumers. These concentrates are rich in essential nutrients like vitamins A and C, contributing to growing interest in immunity-boosting beverages post-pandemic.

The segment’s performance was also bolstered by the rising availability of organic and non-GMO concentrate options, aligning with the clean-label trend. With the fruit concentrate segment continuing to innovate through exotic blends and functional benefits, it maintained its leadership in the cold-pressed juice category, outperforming vegetable concentrates and mixed formulations in 2024.

By Category Analysis

Conventional products hold strong, capturing 67.30% of the cold-pressed juice category.

In 2024, Conventional held a dominant market position in the By Category segment of the Cold Pressed Juice Market, with a 68.50% share. This leadership was largely attributed to the cost-effectiveness and widespread availability of conventionally sourced fruits and vegetables used in juice production. Unlike organic variants, conventional cold-pressed juices are generally priced lower, making them more accessible to a broader consumer base, especially in emerging markets and among price-sensitive buyers.

The segment also benefited from strong retail penetration, with conventional juices occupying major shelf space across supermarkets, hypermarkets, and convenience stores. Large-scale manufacturers prefer conventional sourcing due to the stable supply chain, consistent quality, and higher yield per batch, which supports efficient large-volume production. Furthermore, the majority of new product launches and promotional campaigns during 2024 were targeted around conventional product lines, amplifying their visibility and consumer traction.

Additionally, consumer perception of conventional cold-pressed juices as nutritious and clean-label despite non-organic sourcing contributed to steady demand. While the organic category gained attention among niche health-focused groups, conventional juices continued to dominate in mainstream consumption due to affordability and availability, solidifying their position as the market leader in the category segment during the year.

By Packaging Analysis

Bottles are preferred by consumers, accounting for 74.20% of total packaging usage.

In 2024, Bottles held a dominant market position in the By Packaging segment of the Cold Pressed Juice Market, with a 74.20% share. This dominance was driven by their practicality, portability, and consumer familiarity, making them the preferred packaging format for both manufacturers and consumers. Bottles offer effective sealing and preservation of nutritional content, which is crucial for cold-pressed juices that contain no preservatives and require protection from oxidation and contamination.

The high adoption of bottles was also influenced by their compatibility with various materials, such as PET, glass, and recyclable plastics—each offering shelf appeal and extended shelf life. Bottled cold-pressed juices are highly favored in retail settings due to their visibility and ease of branding through labels, which aids product differentiation in a competitive landscape. Moreover, bottles cater well to on-the-go consumption, aligning with the fast-paced lifestyle of urban consumers, which further supported their market leadership.

In addition, manufacturers heavily invested in bottle-based packaging due to established infrastructure and lower operational changes compared to alternative formats. This ensured scalability and consistent product quality across distribution channels. With consumer trust and supply chain efficiency backing their usage, bottles firmly led the packaging segment of the cold-pressed juice market in 2024.

By Packaging Material Analysis

Glass packaging leads with a 63.50% share, reflecting premium positioning in the juice market.

In 2024, Glass held a dominant market position in the By Packaging Material segment of the Cold Pressed Juice Market, with a 63.50% share. This leading position was primarily due to the strong consumer perception of glass as a premium, sustainable, and non-reactive packaging material.

Glass preserves the freshness, flavor, and nutritional integrity of cold-pressed juices better than many alternatives, making it the top choice among brands targeting health-conscious and quality-focused customers.

The dominance of glass was also supported by its recyclability and eco-friendly appeal, which aligns with growing sustainability concerns among consumers. Premium juice brands widely adopted glass bottles to reinforce product positioning, enhance shelf appeal, and build brand trust. Moreover, the non-toxic and BPA-free nature of glass packaging attracted consumers wary of the chemical leaching associated with some plastic containers.

Retailers also preferred glass-packaged juices due to their visual clarity and premium aesthetic, which improved product visibility and consumer engagement in stores. Although glass packaging comes at a higher cost, its environmental benefits, product safety, and market positioning advantages enabled it to secure the majority share

By Distribution Channel Analysis

Supermarkets and hypermarkets distribute 56.20% of cold-pressed juices to wide-ranging consumers.

In 2024, Supermarkets/Hypermarkets held a dominant market position in the By Distribution Channel segment of the cold-pressed juice Market, with a 56.20% share. This leadership was largely driven by their widespread presence, extensive shelf space, and ability to offer a broad variety of cold-pressed juice brands and flavors under one roof. Consumers favored these outlets for their convenience, ease of access, and the opportunity to compare products in person before purchase.

The high share was also supported by promotional offers, bundle deals, and sampling campaigns frequently organized by brands within these retail spaces, which boosted impulse purchases and brand switching. Supermarkets and hypermarkets were especially effective in reaching urban and semi-urban populations, where health-focused beverage consumption is on the rise.

Moreover, cold pressed juice brands prioritized these channels for their strong footfall, consistent turnover, and reliability in supply chain logistics. Refrigeration infrastructure within supermarkets further ensured the safe handling of cold pressed juices, preserving quality and shelf life. As consumers increasingly sought transparency, clean-label products, and health-conscious options, supermarkets emerged as the most trusted and visible point of purchase.

Key Market Segments

By Type

- Fruit Concentrates

- Citrus Fruits

- Orange

- Lemon

- Grapefruit

- Berries

- Strawberry

- Others

- Tropical Fruits

- Mango

- Pineapple

- Banana

- Passion Fruit

- Others

- Vegetable Concentrates

- Carrot

- Tomato

- Beetroot

- Cucumber

- Others

- Mixed

By Category

- Conventional

- Organic

By Packaging

- Bottles

- Cartons

- Pouches

- Others

By Packaging Material

- Glass

- Plastic

- Others

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Stores

- Others

Driving Factors

Health Awareness Among Consumers Boosts Juice Demand

One of the top driving factors for the cold pressed juice market in 2024 is the growing health awareness among consumers. People are becoming more conscious about what they eat and drink, especially after the pandemic. Cold pressed juices are seen as a healthy choice because they are made without heat, helping to keep vitamins, enzymes, and nutrients intact.

Consumers prefer them over sugary or artificially flavored drinks. These juices are often promoted as natural, fresh, and packed with antioxidants, which appeals to fitness-focused and wellness-driven individuals. As more people shift toward clean-label and nutritious beverages, cold-pressed juices have become a go-to option, especially in urban areas with a rising demand for healthy lifestyles.

Restraining Factors

High Product Cost Limits Mass Market Reach

A major restraining factor in the cold-pressed juice market is its high price compared to regular juices. These juices are made using a special process that keeps nutrients intact, but it also increases production costs.

Cold pressed juices usually require fresh, high-quality fruits and vegetables, expensive cold press machinery, and careful handling due to a shorter shelf life. As a result, the final price is higher, which makes it less affordable for many consumers.

This limits the customer base mainly to health-conscious or high-income groups. In developing regions, where price sensitivity is higher, this becomes a major barrier to market growth and stops the product from reaching a broader, mass-market audience.

Growth Opportunity

Expanding Distribution Channels Enhance Market Reach

A significant growth opportunity for the cold pressed juice market lies in expanding distribution channels. By increasing availability in supermarkets, hypermarkets, convenience stores, and online platforms, companies can reach a broader consumer base.

Enhanced distribution not only improves product accessibility but also caters to the growing demand for health-focused beverages. Online retailing, in particular, offers convenience for busy consumers seeking nutritious options, while physical stores provide immediate purchase opportunities.

Strategic partnerships with retailers and investment in e-commerce platforms can further boost market penetration. As consumers increasingly prioritize health and wellness, ensuring widespread availability through diverse channels positions cold pressed juice brands to capitalize on this trend and drive sales growth.

Latest Trends

Innovative Flavor Combinations Attract Consumers

A notable trend in the cold pressed juice market is the introduction of innovative flavor combinations. Brands are blending unique fruits, vegetables, and superfoods to create distinctive and appealing juices. For instance, combinations like apple-beetroot-carrot or kale-pineapple-ginger offer both novel tastes and enhanced health benefits.

These creative mixes cater to adventurous consumers seeking variety and functional nutrition in their beverages. By continually experimenting with new ingredients and flavors, companies can differentiate their products, attract health-conscious customers, and stay competitive in the evolving market landscape.

Regional Analysis

In 2024, North America held a 34.20% cold-pressed juice Market share.

In 2024, North America dominated the Cold cold-pressed juice Market, accounting for 34.20% of the global share, with a market value of USD 0.3 billion. The region’s strong performance was driven by rising consumer awareness regarding health, wellness, and clean-label products, especially in the United States and Canada.

High demand for functional beverages and a growing fitness-oriented population further supported market growth in this region. Europe followed as another key region, where increasing preferences for organic and natural products shaped market dynamics.

Asia Pacific witnessed gradual growth, driven by emerging urban populations and increased health consciousness, though it still lagged in terms of volume compared to developed regions.

The Middle East & Africa and Latin America held comparatively smaller shares but showed potential for growth through expanding urban retail infrastructure and rising disposable incomes. Despite their current lower penetration, these regions are expected to attract market players aiming for long-term expansion.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

In 2024, the global cold-pressed juice market experienced significant growth, driven by increasing consumer demand for health-centric, natural beverages. Key players such as Suja Life LLC, Garden of Flavor, and Greenhouse Juice Co. have been instrumental in shaping this market landscape.

Suja Life LLC has solidified its position as a leader in the organic cold-pressed juice sector. The company’s commitment to offering a diverse range of cold-pressed, organic juices and wellness shots has resonated with health-conscious consumers. Suja’s products are known for their high-pressure processing (HPP) technique, which preserves nutrients and extends shelf life without the need for preservatives. This approach aligns with the growing consumer preference for clean-label products.

Garden of Flavor has distinguished itself through its dedication to producing small-batch, organic, cold-pressed juices. The company’s emphasis on using fresh vegetables, fruits, nuts, and berries, without heat or flash pasteurization, ensures the retention of natural flavors and nutrients. Garden of Flavor’s product line, featuring offerings like Mean Greens and Turmeric Tonic, caters to consumers seeking functional beverages that support overall wellness.

Greenhouse Juice Co., based in Toronto, has made significant strides in the cold-pressed juice market by focusing on organic, plant-based beverages bottled in sustainable glass packaging. The company’s commitment to environmental sustainability, combined with a diverse product portfolio that includes innovative flavors and wellness shots, has appealed to eco-conscious consumers.

Top Key Players in the Market

- 7-ELEVEN, Inc.

- Bolthouse Farms Inc.

- Evolution Fresh, Inc. (Starbucks Corporation)

- Suja Life, LLC.

- Garden of Flavor

- Greenhouse Juice Co.

- Juice Generation

- La Presserie

- Mama Juice

- Naked Juice Company (PepsiCo., Inc.)

- Pressed Juicery, Inc.

- Pulp & Press Juice Co.

- Pure Green

- Raw Pressery

- Suja Life, LLC

- The Juice Press LLC

Recent Developments

- In March 2025, 7-Eleven expanded its private-label beverage offerings by adding new energy drinks, hydration beverages, and prosecco wine lines and expanding its juice and tea options. This move reflects the company’s focus on diversifying its product range to cater to evolving consumer preferences.

- In May 2024, Bolthouse Farms separated into two entities: Bolthouse Fresh Foods, focusing on fresh carrots, and Generous Brands, encompassing beverages and dressings. This split aims to accelerate growth in each sector.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 1.1 Billion |

| Forecast Revenue (2034) | USD 2.2 Billion |

| CAGR (2025-2034) | 7.1% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Fruit Concentrates (Citrus Fruits, Orange, Lemon, Grapefruit, Berries, Strawberry, Others), Tropical Fruits (Mango, Pineapple, Banana, Passion Fruit, Others), Vegetable Concentrates (Carrot, Tomato, Beetroot, Cucumber, Others), Mixed), By Category (Conventional, Organi), By Packaging (Bottles, Cartons, Pouches, Others), By Packaging Material (Glass, Plastic, Others), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Online Stores, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | 7-ELEVEN, Inc., Bolthouse Farms Inc., Evolution Fresh, Inc. (Starbucks Corporation), Suja Life, LLC., Garden of Flavor, Greenhouse Juice Co., Juice Generation, La Presserie, Mama Juice, Naked Juice Company (PepsiCo., Inc.), Pressed Juicery, Inc., Pulp & Press Juice Co., Pure Green, Raw Pressery, Suja Life, LLC, The Juice Press LLC |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |