Quick Navigation

Report Overview

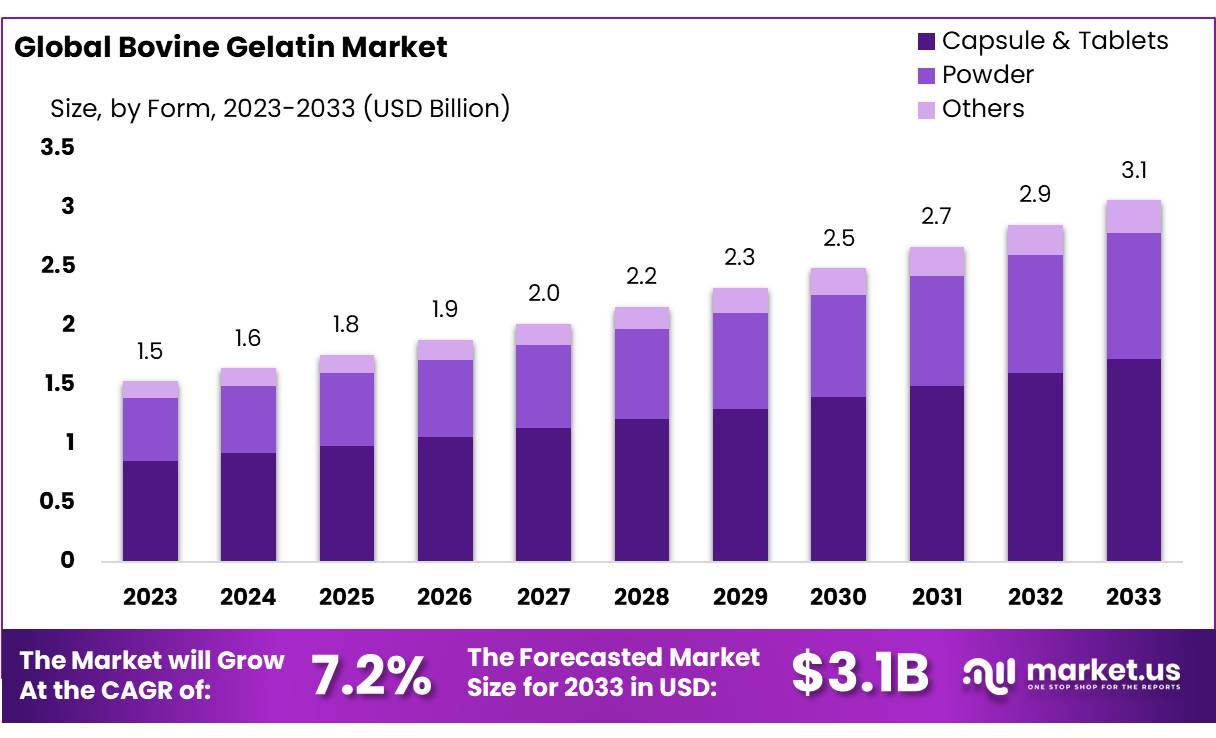

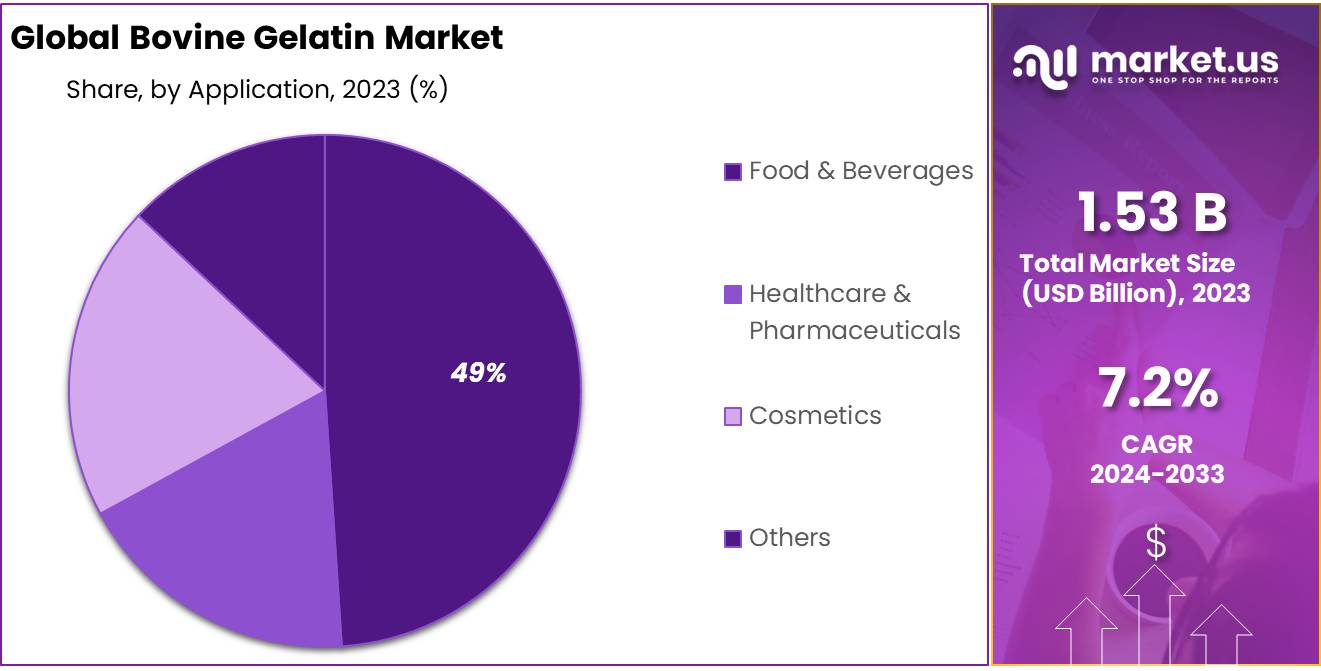

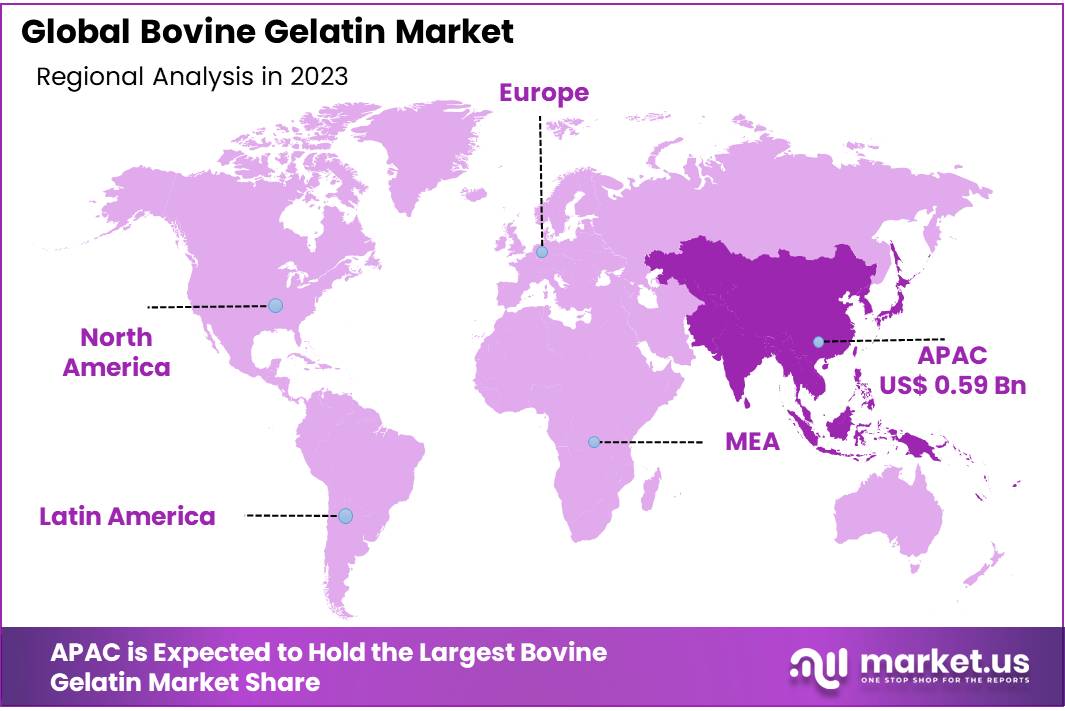

The Global Bovine Gelatin Market size is expected to be worth around USD 3.1 Bn by 2033, from USD 1.53 Bn in 2023, growing at a CAGR of 7.2% during the forecast period from 2024 to 2033. In 2023, Asia Pacific held a dominant position in the Government Cloud market, capturing over 38.7% of the market share, with revenues totaling USD 0.59 billion.

Bovine gelatin is a natural substance derived from the collagen found in the connective tissues, skin, and bones of cows (bovine species). It is commonly used in the food, pharmaceutical, and cosmetic industries due to its unique gelling, thickening, and stabilizing properties.

In food, bovine gelatin is often used in products like gummies, marshmallows, gelatin desserts, and as a stabilizer in dairy and meat products. It is also utilized in the pharmaceutical industry to make capsules, as well as in cosmetics for skincare products, due to its ability to enhance texture and improve moisture retention.

Bovine gelatin plays a significant role in various industries, including food, pharmaceuticals, and cosmetics, where it is used for its gelling and stabilizing properties. A key driver of this growth is the increasing demand for natural, plant-based ingredients in food and pharmaceuticals, as well as the expanding use of bovine gelatin in nutraceuticals and personal care products

The food and beverage sector remains the largest consumer of bovine gelatin, accounting for nearly 45% of the market share in 2023. This includes its use in confectioneries, dairy products, and processed foods. In 2023, gelatin-based products like gummies and marshmallows saw a demand increase of 5-7% annually in North America and Europe, regions where the trend for health-conscious, natural ingredients is particularly strong

Government regulations play a crucial role in the global bovine gelatin market, especially in regions like the European Union and the United States, where animal-based products are strictly monitored. For example, the EU mandates that bovine gelatin must be sourced from BSE-free regions, a regulation designed to prevent mad cow disease.

These safety standards have led to the development of stringent certification processes for gelatin manufacturers. As a result, in 2023, more than 70% of global bovine gelatin exports came from countries in North America and Latin America, with Brazil being one of the top exporters, sending over 60% of its bovine gelatin output to Europe and the U.S. annually

In terms of market dynamics, several partnerships and acquisitions have shaped the industry. For instance, in early 2023, Gelita, a leading gelatin producer, expanded its operations in Brazil, increasing production capacity by 30%, anticipating a rise in demand from the North American and European markets.

Similarly, PB Gelatins, another key player, has increased its R&D investments by 20% over the past two years, focusing on developing bovine gelatin alternatives and enhancing product applications for the growing nutraceutical and personal care sectors

Key Takeaways

- Bovine Gelatin Market size is expected to be worth around USD 3.1 Bn by 2033, from USD 1.53 Bn in 2023, growing at a CAGR of 7.2%.

- Capsule & Tablets held a dominant market position, capturing more than a 56.6% share of the global bovine gelatin market.

- Acid Cured held a dominant market position, capturing more than a 65.6% share.

- Conventional held a dominant market position, capturing more than a 78.7% share.

- Stabilizer held a dominant market position, capturing more than a 38.7% share of the global bovine gelatin market.

- Food & Beverages held a dominant market position, capturing more than a 49.7% share of the global bovine gelatin market.

- Supermarkets & Hypermarkets held a dominant market position, capturing more than a 39.5% share.

- Asia Pacific (APAC) dominates the global bovine gelatin market, accounting for 38.7% of the market share, valued at USD 0.59 billion.

Bovine Gelatin Business Environment Analysis

Regulations play a significant role in the production and distribution of bovine gelatin. Government authorities, such as the U.S. Food and Drug Administration (FDA) and the European Food Safety Authority (EFSA), have established strict guidelines to ensure the safety and quality of gelatin products.

These regulations encompass sourcing, processing, and labeling standards, which have led manufacturers to adopt advanced quality control systems. In regions like the Middle East, compliance with halal certifications is essential for market entry, adding another layer of regulatory consideration.

The rising demand for natural and functional ingredients has significantly impacted the bovine gelatin market. Gelatin is widely used in dietary supplements, functional foods, and pharmaceuticals due to its high protein content and health benefits, such as improved joint health and skin elasticity. According to the National Institutes of Health (NIH), the use of collagen-based supplements has grown by over 15% in 2023, reflecting consumer interest in wellness-oriented products.

Global trade in bovine gelatin is influenced by raw material availability and export-import regulations. Countries like Brazil, the United States, and India are leading producers, exporting significant volumes to Europe and Asia. In 2023, the export of bovine gelatin from Brazil grew by 12%, driven by strong demand from the food and pharmaceutical industries. Trade agreements have eased market entry, but geopolitical tensions and supply chain disruptions occasionally challenge the flow of goods.

Technological advancements in the processing of bovine gelatin have enabled manufacturers to improve efficiency and product quality. Innovations such as enzymatic hydrolysis and enhanced filtration techniques are being adopted to produce high-purity gelatin suitable for specialized applications like pharmaceuticals and cosmetics. Investments in R&D have surged, with companies allocating nearly 5-7% of their annual revenue to innovation in 2023.

The bovine gelatin market is highly competitive, with key players like Gelita AG, Darling Ingredients Inc., and Nitta Gelatin Inc. dominating the industry. These companies focus on strategic partnerships, mergers, and acquisitions to expand their market share. In 2023, Darling Ingredients Inc. announced a partnership with a biotechnology firm to enhance collagen extraction techniques, highlighting the industry’s commitment to innovation.

By Form

In 2023, Capsule & Tablets held a dominant market position, capturing more than a 56.6% share of the global bovine gelatin market. This segment’s strong performance can be attributed to the increasing demand for gelatin-based supplements, especially in the pharmaceutical and nutraceutical industries.

Bovine gelatin is often used in the production of softgel capsules and tablets due to its ability to improve bioavailability and support better absorption of active ingredients. Moreover, consumer preference for convenient and easy-to-consume forms of supplements further fueled the growth of capsules and tablets in the market.

As of 2024, the demand for Capsule & Tablets remains robust, continuing to represent a significant portion of the market. This form of gelatin remains preferred because of its consistent performance in both the dietary supplement and pharmaceutical sectors, where reliability and ease of use are critical factors. In addition, the expansion of the aging population and increasing health awareness are expected to sustain growth in this segment over the coming years.

The Powder form of bovine gelatin, while smaller in market share compared to capsules and tablets, has been gaining traction due to its versatility in food and beverage applications. In 2023, the Powder segment accounted for a significant portion of the market as it found applications in gummy candies, marshmallows, and even in skincare products.

Consumers’ interest in natural, customizable products has contributed to the rise of powdered gelatin, especially in the food processing industry. The versatility of powdered bovine gelatin allows it to be used in both industrial and home settings, where it serves as a key ingredient in the creation of various functional foods and beverages.

Other forms of bovine gelatin, which include products used in medical and cosmetic applications, held a smaller but steadily growing market share in 2023. The demand for gelatin in wound care, capsule coatings, and beauty products has been rising, supported by growing trends in self-care and health optimization. Although this segment remains niche, it shows potential for steady growth, especially as the demand for natural and sustainable ingredients continues to rise globally.

By Type

In 2023, Acid Cured held a dominant market position, capturing more than a 65.6% share of the global bovine gelatin market. This segment’s dominance is largely due to the high-quality gelatin produced through the acid curing process, which is widely used in the food, pharmaceutical, and nutraceutical industries. Acid-cured gelatin offers a superior texture, clarity, and stability, making it a preferred choice for applications like capsules, tablets, and confectionery products.

The growing demand for high-performance gelatin in food products such as gummy candies, marshmallows, and jellies has significantly boosted the acid-cured segment’s growth. Additionally, the increasing need for gelatin in the production of gelatin-based pharmaceuticals has played a key role in reinforcing this segment’s strong market position.

As we move into 2024, Acid Cured gelatin continues to maintain its leading market share, with demand remaining steady. The segment is expected to sustain its growth trajectory due to the continued expansion of the food and pharmaceutical industries, as well as ongoing trends in health and wellness. Consumers’ increasing interest in clean-label, natural ingredients has also contributed to the growth of acid-cured gelatin, which is perceived as a more natural and reliable option compared to alternatives.

On the other hand, the Alkaline Cured segment, though smaller in market share, has been steadily gaining traction. In 2023, Alkaline Cured gelatin accounted for a growing portion of the market, driven by its specific advantages in certain applications, particularly in the production of industrial products and certain types of capsules.

Alkaline-cured gelatin tends to be stronger and more resistant to thermal degradation, which makes it more suitable for specific uses, including in certain pharmaceutical applications and for coatings in softgel capsules. However, its use in food and beverage products is somewhat limited compared to acid-cured gelatin.

The Alkaline Cured segment is expected to see moderate growth, especially as industries continue to seek specialized gelatin solutions. This segment’s growth will likely be driven by technological advancements that make alkaline-cured gelatin more versatile and cost-effective for various applications. The segment is also benefiting from the growing use of gelatin in newer product formats like bio-based packaging and other sustainable materials, which are seeing increased demand as sustainability becomes a key concern in many industries.

By Nature

In 2023, Conventional held a dominant market position, capturing more than a 78.7% share of the global bovine gelatin market. This significant share can be attributed to the widespread use of conventional bovine gelatin across a variety of industries, including food, pharmaceuticals, and nutraceuticals. Conventional gelatin is more affordable and readily available compared to its organic counterpart, making it the preferred choice for large-scale manufacturing.

The demand for conventional gelatin is particularly strong in the production of capsules, tablets, gummy candies, and other processed food products, where its functionality and cost-effectiveness make it an ideal ingredient. As consumer demand for processed and packaged foods remains high, conventional bovine gelatin is expected to continue playing a major role in these sectors.

Looking ahead to 2024, conventional bovine gelatin is projected to maintain its dominant market share. The consistent demand for this form of gelatin in mass-produced food products, as well as its use in various pharmaceutical formulations, will likely support steady growth.

Additionally, the increasing adoption of gelatin-based solutions in emerging markets, where cost-sensitive production is a priority, further solidifies the position of conventional gelatin in the market. As the global food and beverage industry continues to expand, the demand for conventional gelatin is expected to remain strong, especially in regions where price sensitivity and availability are key factors.

In contrast, the Organic segment of the bovine gelatin market is smaller but growing steadily. In 2023, Organic gelatin accounted for a smaller portion of the market compared to conventional gelatin. The rise of organic products is being driven by a growing consumer preference for natural, sustainably sourced ingredients, particularly among health-conscious consumers and those seeking cleaner labels.

Organic bovine gelatin is increasingly used in premium food products, such as organic gummy supplements, natural cosmetics, and health-focused snacks, as well as in pharmaceutical applications that require certified organic ingredients.

In 2024, the Organic segment is expected to see continued growth as consumers become more aware of the benefits of organic and natural products. This growth will likely be driven by increasing demand in the health and wellness sectors, where organic products are often seen as safer and more beneficial. As organic certification becomes more accessible and production costs decrease, organic gelatin could capture a larger share of the market, particularly in North America and Europe, where organic trends are more pronounced.

By Function

In 2023, Stabilizer held a dominant market position, capturing more than a 38.7% share of the global bovine gelatin market. This strong market presence is largely driven by the widespread use of bovine gelatin as a stabilizing agent in a variety of food and beverage applications. Gelatin is a key ingredient in stabilizing products such as dairy items, desserts, and processed foods, where it helps to maintain texture and prevent separation.

Its ability to enhance the shelf life of products and improve the overall mouthfeel has made it a preferred choice in industries like confectionery, bakery, and dairy. The growing consumer demand for consistent product quality, especially in packaged foods, has significantly contributed to the continued dominance of the stabilizer segment.

Looking forward to 2024, the Stabilizer segment is expected to maintain its leading position in the bovine gelatin market. With the increasing production of convenience foods and ready-to-eat products, the demand for stabilizing agents is anticipated to remain strong.

Bovine gelatin’s versatility and effectiveness as a stabilizer in various formulations—ranging from sauces and dressings to ice creams and jellies—will continue to support its growth. Additionally, the trend towards clean-label products, where consumers are seeking fewer artificial additives, is likely to benefit the stabilizer segment, as gelatin is a natural ingredient that can replace synthetic stabilizers.

The Gelling Agent segment, while smaller in market share, also plays an important role in the bovine gelatin market. In 2023, this segment accounted for a significant portion of the market, particularly in the production of gummies, jellies, marshmallows, and other gel-based confectionery products.

The ability of bovine gelatin to form stable, reliable gels makes it the go-to ingredient for manufacturers in the candy and dessert sectors. With the continued growth of the global confectionery market, the demand for gelling agents is expected to grow steadily. In 2024, as new product innovations and healthier alternatives to traditional confectionery products emerge, the gelling agent segment is likely to see moderate growth, driven by consumer preferences for more functional and low-sugar options.

The Thickener segment is relatively smaller but continues to hold a steady position in the bovine gelatin market. In 2023, bovine gelatin was used as a thickening agent in products like soups, sauces, gravies, and beverages, where it helps achieve the desired viscosity and texture.

As the demand for clean-label, natural thickeners increases, the thickener segment is expected to grow slightly in 2024. Consumers’ increasing awareness of health and wellness trends, combined with the growing demand for natural and plant-based products, may create opportunities for gelatin to replace more synthetic thickening agents in various food applications.

By Application

In 2023, Food & Beverages held a dominant market position, capturing more than a 49.7% share of the global bovine gelatin market. This substantial share is largely driven by the widespread use of bovine gelatin in various food products, such as gummy candies, jellies, marshmallows, and dairy items. Gelatin’s ability to enhance texture, provide structure, and act as a stabilizer in food formulations has made it an essential ingredient in the food industry.

As consumer demand for convenience foods and processed snacks continues to rise, the Food & Beverages segment remains the largest contributor to the gelatin market. Additionally, the clean-label trend, with consumers seeking natural ingredients, has further boosted gelatin’s popularity in this sector, as it is often preferred over synthetic alternatives.

Looking ahead to 2024, the Food & Beverages segment is expected to maintain its dominant position, driven by the continued growth in the global confectionery and snack industries. The increasing demand for plant-based and low-sugar options is likely to further fuel the market for gelatin, as it can be used in healthier formulations without compromising on quality or taste. Additionally, the growing trend of functional foods, such as protein-enriched snacks and supplements, will continue to support the demand for bovine gelatin in food applications.

In 2023, the Healthcare & Pharmaceuticals segment also saw notable demand, accounting for a significant share of the bovine gelatin market. Gelatin is commonly used in the pharmaceutical industry to produce capsules, tablets, and other drug delivery systems due to its ability to enhance bioavailability and improve the ease of consumption.

This segment is expected to continue growing in 2024, driven by the increasing use of gelatin in the development of nutraceuticals, vitamins, and other supplements. With the aging global population and rising health consciousness, the demand for gelatin-based pharmaceutical products, including softgel capsules, is expected to remain strong.

The Cosmetics segment, although smaller in comparison to Food & Beverages and Healthcare & Pharmaceuticals, has been steadily growing. In 2023, bovine gelatin was increasingly used in skincare products, such as moisturizers, serums, and anti-aging formulations, due to its collagen content, which is beneficial for skin elasticity and hydration.

As the trend for natural and sustainable beauty products continues to gain momentum, the demand for bovine gelatin in cosmetics is expected to rise. In 2024, this segment is likely to see further growth, particularly with the increasing consumer preference for clean and organic beauty products.

By Distribution Channel

In 2023, Supermarkets & Hypermarkets held a dominant market position, capturing more than a 39.5% share of the global bovine gelatin market. This can be attributed to the widespread reach and convenience of large retail chains, which offer a broad range of products containing bovine gelatin, such as food items, dietary supplements, and personal care products.

Supermarkets and hypermarkets are the go-to shopping destinations for consumers seeking everyday products, including gelatin-based items like gummy candies, marshmallows, and even some pharmaceutical products. The extensive distribution networks of these retailers, along with their ability to offer competitive pricing and frequent promotions, continue to make them the largest sales channel for bovine gelatin products.

Looking into 2024, Supermarkets & Hypermarkets are expected to maintain their leading market position. With the ongoing demand for convenience and a broad variety of consumer goods under one roof, these retail formats will remain essential for the distribution of gelatin-based products. The increasing shift toward healthier food options and clean-label products, which often feature natural ingredients like gelatin, is likely to further strengthen the position of supermarkets and hypermarkets in the bovine gelatin market.

Specialty Stores, while accounting for a smaller portion of the market, have been steadily gaining traction, especially in sectors such as health and wellness, where consumers are looking for specific, high-quality gelatin products. In 2023, this segment saw growth, driven by the rising demand for gelatin-based dietary supplements, such as collagen peptides and joint health supplements, which are typically sold in health food stores and specialty retailers.

As consumer interest in personalized nutrition and natural wellness products continues to rise, specialty stores are expected to capture a larger share of the market in 2024. These stores cater to niche markets that are more focused on natural and organic ingredients, which include gelatin as a preferred choice for many health-conscious buyers.

Pharmacies & Drug Stores, which accounted for a significant portion of the bovine gelatin market in 2023, have been an important channel for the sale of gelatin-based health products, such as softgel capsules and dietary supplements.

With the increasing focus on health and wellness, more consumers are turning to pharmacies for their supplement needs, including those containing gelatin. The trend toward preventive health and the growing demand for nutraceuticals and vitamins is expected to keep this channel strong in 2024. Additionally, as the population ages, the demand for joint health supplements and other gelatin-based products in pharmacies is expected to rise, further supporting the growth of this distribution channel.

The E-commerce segment, while traditionally smaller, has been experiencing rapid growth. In 2023, the convenience of online shopping and the increasing preference for home delivery options led to a rise in the sale of gelatin-based products through online platforms. E-commerce provides a vast range of gelatin-containing products, from food and beverages to cosmetics and healthcare items, which can be easily compared and purchased by consumers from the comfort of their homes.

As more consumers turn to online shopping, especially post-pandemic, the E-commerce channel is expected to see significant growth in 2024. This trend is further accelerated by the growing popularity of subscription-based services for health and wellness products, which often include gelatin-based supplements.

Key Market Segments

By Form

- Capsule & Tablets

- Powder

- Others

By Type

- Acid Cured

- Alkaline Cured

By Nature

- Organic

- Conventional

By Function

- Stabilizer

- Thickener

- Gelling Agent

- Others

By Application

- Food & Beverages

- Healthcare & Pharmaceuticals

- Cosmetics

- Others

By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Stores

- Pharmacies & Drug Stores

- E-commerce

- Others

Drivers

Increasing Demand for Gelatin in the Food & Beverage Industry

One of the major driving factors for the growth of the bovine gelatin market is the rising demand for gelatin in the food and beverage industry. Gelatin plays a crucial role in food applications due to its versatility, natural origin, and functionality as a gelling agent, stabilizer, and thickener.

The global food industry continues to expand, with increasing consumption of confectionery products like gummies, marshmallows, and jellies, all of which heavily rely on gelatin for their texture and consistency.

According to the Food and Agriculture Organization (FAO), global food production is expected to increase by 70% by 2050, driven by population growth and dietary changes, particularly in emerging economies. As more consumers turn to processed foods for convenience and taste, the demand for gelatin-based ingredients is also expected to rise.

Moreover, consumer preferences are shifting towards clean-label products, which include natural ingredients like bovine gelatin rather than synthetic alternatives. This trend is evident in the growing popularity of gelatin-based snacks, dietary supplements, and functional foods.

The U.S. Department of Agriculture (USDA) projects that the global processed food market will continue to expand at a rate of 4% annually through 2025, with a particularly strong growth outlook for gelatin-based products such as gummy supplements and protein-rich snacks. Additionally, gelatin’s role in stabilizing emulsions and improving the shelf life of packaged food products makes it highly valued in the industry.

As food manufacturers seek natural alternatives to synthetic additives, the demand for bovine gelatin is expected to grow substantially. The global gelatin market in food applications alone is projected to exceed $4 billion by 2025, driven largely by its use in confectionery products, dairy, and other food categories. As a result, the food and beverage sector remains one of the largest and fastest-growing end-user industries for bovine gelatin, making it a key factor driving market expansion.

Restraints

Increasing Concerns Over Animal Welfare Limiting Bovine Gelatin Market Growth

According to data from the World Health Organization (WHO), over 40% of the global population is shifting towards plant-based diets in response to environmental and ethical concerns surrounding animal agriculture. This shift is most pronounced in developed countries like the United States and parts of Europe, where awareness of animal welfare and environmental sustainability is high.

A survey conducted by the Vegan Society in 2022 found that nearly 8 million people in the UK alone follow a plant-based diet, contributing to the increased demand for plant-based food ingredients over animal-derived ones. This cultural change is leading food manufacturers to explore alternatives to bovine gelatin, thus restricting the growth potential of the bovine gelatin market.

Moreover, there are regulatory and religious considerations that further limit the use of bovine gelatin in certain regions. For example, in Muslim-majority countries, bovine gelatin is often not permitted due to halal dietary restrictions. In countries like Saudi Arabia, approximately 20% of the population strictly adheres to halal dietary laws, leading manufacturers to look for gelatin alternatives that meet these religious requirements.

The same holds true in India, where religious beliefs significantly influence dietary choices, and 10%-15% of the population follows vegetarianism for ethical or religious reasons. These regions have seen a rise in demand for plant-based alternatives to bovine gelatin, such as agar-agar, which has led to a decrease in the use of animal-derived gelatin.

The ethical concerns surrounding animal-based ingredients are further reinforced by the impact of the Global Animal Partnership (GAP) and similar organizations that advocate for better animal welfare standards. These groups have raised awareness about the conditions under which livestock, including cattle used for gelatin production, are raised and slaughtered. As a result, the demand for more humane and sustainable gelatin alternatives is increasing.

Furthermore, some governments have started to implement regulations that encourage plant-based ingredients as part of their environmental and animal welfare policies. For instance, the European Union’s Farm to Fork Strategy, which aims to make food systems fair, healthy, and environmentally-friendly, is expected to further push the adoption of plant-based food alternatives, including gelatin substitutes.

According to a study published by the United Nations Environment Programme (UNEP), livestock production accounts for 14.5% of global greenhouse gas emissions, a factor that is driving demand for more sustainable, plant-based food ingredients. As the shift towards sustainability continues, the demand for bovine gelatin is expected to face increasing challenges from plant-based alternatives, which could further hinder its market growth.

Opportunity

Expansion of the Health and Wellness Sector Presents Growth Opportunities for Bovine Gelatin

The global dietary supplements market is projected to grow at a CAGR of 8.6% from 2023 to 2030, according to the National Institutes of Health (NIH). The increasing consumer demand for products that support joint health and skin rejuvenation has contributed to this growth.

Since bovine gelatin is a cost-effective and functional ingredient for these products, manufacturers are capitalizing on its ability to deliver the necessary collagen for both skin and joint benefits. For example, collagen supplements (which commonly include bovine gelatin as a key ingredient) have seen a market growth of approximately 10% annually in recent years, according to reports by the American College of Rheumatology.

The growth of the global organic food market, which is expected to reach USD 441 billion by 2026, also presents an opportunity for bovine gelatin. Many organic food products—especially those in the snack and confectionery sectors—are incorporating natural ingredients like bovine gelatin to meet consumer demand for clean-label, functional products. The U.S. Department of Agriculture (USDA) has reported an increase in organic food sales by 14% year-over-year, with a notable portion of these products containing gelatin for both texture and nutritional benefits.

Furthermore, the rising trend of personalized nutrition is another opportunity for bovine gelatin. As consumers seek more tailored dietary products, gelatin-based supplements that support specific health needs—such as joint support, skin hydration, and overall wellness—are becoming more in demand. According to a report by the International Food Information Council (IFIC), over 55% of consumers in the U.S. are interested in purchasing supplements or functional foods designed to meet their personal health goals.

To capitalize on these growth opportunities, manufacturers are also focusing on sustainable sourcing and quality improvements. The demand for high-quality bovine gelatin, derived from grass-fed and hormone-free cows, is expected to increase in response to consumer preference for ethically sourced ingredients. Initiatives like the Sustainable Beef Program in Australia aim to ensure that gelatin products meet sustainability and ethical sourcing standards, which can further drive consumer confidence and market growth.

Trends

Growing Popularity of Collagen-Based Products Driving Bovine Gelatin Demand

This growth is driven largely by the demand for collagen in both dietary supplements and functional foods, with bovine gelatin being one of the most commonly used sources due to its abundance and cost-effectiveness. The National Institute of Arthritis and Musculoskeletal and Skin Diseases (NIAMS) reports that over 10 million people in the United States suffer from joint issues, and as a result, collagen supplements have become increasingly popular as a way to help manage symptoms like joint pain and stiffness.

One of the latest trends is the integration of bovine gelatin into innovative formats such as collagen-infused beverages, snack bars, and gummies. These products are appealing to health-conscious consumers looking for convenient and tasty ways to boost their collagen intake.

Moreover, the European Food Safety Authority (EFSA) has officially recognized the benefits of collagen for joint and skin health, further supporting the demand for collagen-based foods and supplements. The increase in health claims around collagen, particularly for its role in reducing wrinkles and promoting joint mobility, is expected to lead to higher consumption of bovine gelatin in consumer products. This is further accelerated by the rise of e-commerce, which has allowed collagen-based products to reach a wider global audience.

In addition, with increasing concerns over animal welfare, some manufacturers are innovating by using more sustainable sourcing practices for bovine gelatin, such as using certified grass-fed and hormone-free cattle. This trend of more ethical sourcing is helping to mitigate some of the consumer resistance to animal-derived ingredients, broadening the appeal of bovine gelatin products.

As the demand for collagen continues to grow, bovine gelatin is positioned to benefit from this trend, both in terms of volume and market diversification. Companies in the food and supplement industries are already capitalizing on this trend by developing new products that target a wide range of health concerns, from skin aging to joint health.

The combination of increasing consumer interest in health and wellness, coupled with the benefits of collagen, ensures that bovine gelatin will remain a key ingredient in the functional food and supplement sectors.

Regional Analysis

Asia Pacific (APAC) dominates the global bovine gelatin market, accounting for 38.7% of the market share, valued at USD 0.59 billion. This dominance is primarily due to the region’s large population base, increased health awareness, and a strong demand for gelatin-based products, particularly in China, Japan, and India.

The growing popularity of collagen-based health supplements and functional foods is further fueling this market segment. APAC is also experiencing significant growth in the pharmaceutical and cosmetic industries, where bovine gelatin is used extensively in capsules and skincare products.

North America holds a substantial share of the market, driven by increasing consumer demand for dietary supplements and functional foods containing collagen. The U.S. is the leading contributor to the market, with consumers showing a keen interest in wellness and anti-aging products. The North American bovine gelatin market is valued at approximately USD 0.43 billion and is expected to grow steadily due to the high adoption of collagen-based products in the region’s health-conscious demographic.

Europe is another prominent market for bovine gelatin, driven by the growing demand for gelatin-based food and pharmaceutical products. With an emphasis on clean-label products, Europe accounts for 25% of the global market share. Countries like Germany, the U.K., and France are key contributors to this growth, supported by strong food safety regulations and a rising interest in natural and functional foods.

In Latin America and the Middle East & Africa, the market is smaller but is expected to grow steadily, driven by increasing urbanization, changing dietary habits, and the growing popularity of dietary supplements.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The bovine gelatin market is highly competitive, with several key players leading the industry through extensive product offerings and strategic initiatives. Gelita AG, a global leader in the production of gelatin, holds a strong market presence due to its diverse portfolio and innovation in collagen-based products.

Darling Ingredients Inc., another major player, benefits from its integrated supply chain and focuses on sustainable practices, making it a preferred choice for many customers in the food and pharmaceutical sectors. Additionally, Bernard Jansen Products Inc. and Nitta Gelatin, Inc. are prominent contributors, offering high-quality bovine gelatin used across various applications including food, supplements, and capsules.

Companies like Merck KGaA and Lonza Group are also significant players in the market, expanding their footprints through acquisitions and product innovations. Lonza specializes in providing high-quality gelatin for the pharmaceutical industry, particularly in capsule manufacturing. Gelatine and Jellice, both known for their robust presence in Europe and Asia, are continuously expanding their product offerings to meet the growing demand for collagen-based health products.

Moreover, Lapi Gelatine Spa, Trobas Gelatin, and Pioneer Europe B.V. are expanding their regional influence by focusing on emerging markets, offering both bovine and fish gelatin to cater to varying consumer preferences. Luoyang Leston Import and Export Trade Co., Ltd. has capitalized on its position in the Asia-Pacific region, where the demand for gelatin-based products is rapidly increasing due to rising health awareness. Together, these companies continue to strengthen their market position through strategic partnerships, product innovation, and geographic expansion.

Top Key Players

- Bernard Jansen Products Inc.

- Darling Ingredients Inc.

- Gelita AG

- Gelita

- Jellice

- Pioneer Europe B.V.

- Lapi Gelatine Spa

- Lonza Group

- Luoyang Leston Import and Export Trade Co., Ltd.

- Merck KGaA

- Nitta Gelatin, Inc.

- Nutra Food Ingredients LLC

- Pioneer Europe B.V.

- PV

- Trobas

- Gelatin

Recent Developments

In 2023 Bernard Jansen Products Inc. reported a 5% increase in its gelatin production capacity, with a particular focus on expanding its product line for the growing health and wellness industry.

In 2024, Darling Ingredients is expected to see an additional 4-5% growth in revenue, supported by its strategic initiatives to expand in emerging markets, especially in Asia Pacific and Latin America.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 1.5 Bn |

| Forecast Revenue (2033) | USD 3.1 Bn |

| CAGR (2024-2033) | 7.2% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Form (Capsule and Tablets, Powder, Others), By Type (Acid Cured, Alkaline Cured), By Nature (Organic, Conventional), By Function (Stabilizer, Thickener, Gelling Agent, Others), By Application (Food and Beverages, Healthcare and Pharmaceuticals, Cosmetics, Others), By Distribution Channel ( Supermarkets and Hypermarkets, Specialty Stores, Pharmacies and Drug Stores, E-commerce, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Bernard Jansen Products Inc., Darling Ingredients Inc., Gelita AG, Gelita, Jellice, Pioneer Europe B.V., Lapi Gelatine Spa, Lonza Group, Luoyang Leston Import and Export Trade Co., Ltd., Merck KGaA, Nitta Gelatin, Inc., Nutra Food Ingredients LLC, Pioneer Europe B.V., PV, Trobas, Gelatin |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |