Quick Navigation

Report Overview

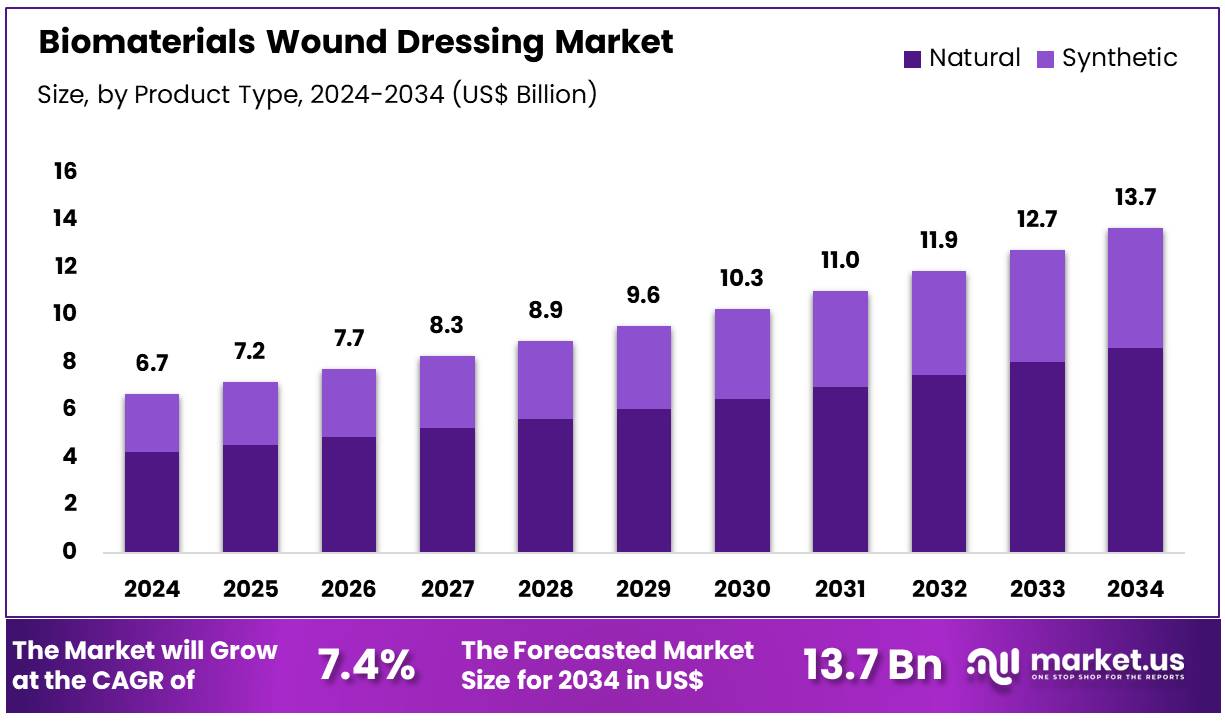

Global Biomaterial Wound Dressing Market is projected to experience significant growth, with an estimated market value reaching approximately USD 13.7 billion by 2034, up from USD 6.7 billion in 2024, reflecting a compound annual growth rate (CAGR) of 7.4% during the forecast period from 2025 to 2034.

This growth can be attributed to advancements in wound care technology, an increase in the prevalence of chronic wounds, and the growing demand for effective and efficient wound management solutions. Biomaterial-based wound dressings, which include both natural and synthetic materials, offer enhanced antimicrobial properties, improved moisture regulation, and promote tissue regeneration, creating an optimal environment for healing. The rising global geriatric population and an increase in surgical procedures worldwide are further driving demand, as healthcare providers seek dressings that facilitate quicker recovery and reduce infection risks.

Additionally, the increasing adoption of homecare wound management solutions has positively impacted market growth, as patients increasingly seek convenient and effective wound care options. Despite the market’s potential, challenges such as stringent regulatory approval processes, high costs, and limited reimbursement options may hinder its expansion. Nonetheless, innovations in wound dressing technologies and the growing incidence of chronic diseases are expected to fuel demand for biomaterial-based dressings.

A significant rise in chronic wounds and surgical procedures, along with the need for wound care solutions that enhance healing and minimize infection risks, has made biomaterial wound dressings increasingly popular. Furthermore, the widespread use of biomaterials such as alginate and chitosan in wound care due to their hydrophilic properties and adaptability in forming various dressing types, including hydrogels, beads, and electrospun scaffolds will continue to drive market growth.

For example, alginate-based wound dressings, derived from brown seaweed, are renowned for their high absorbency and biocompatibility. These dressings can absorb up to 20 times their weight in exudate, forming a gel that maintains a moist wound environment conducive to healing.

They are non-adherent, reducing pain during dressing changes, and can be left in place for up to 7 days, depending on the wound’s condition. Additionally, alginate dressings support tissue regeneration by promoting fibroblast proliferation and collagen synthesis. This research and funding are expected to unlock substantial growth opportunities in the market throughout the forecast period.

Key Takeaways

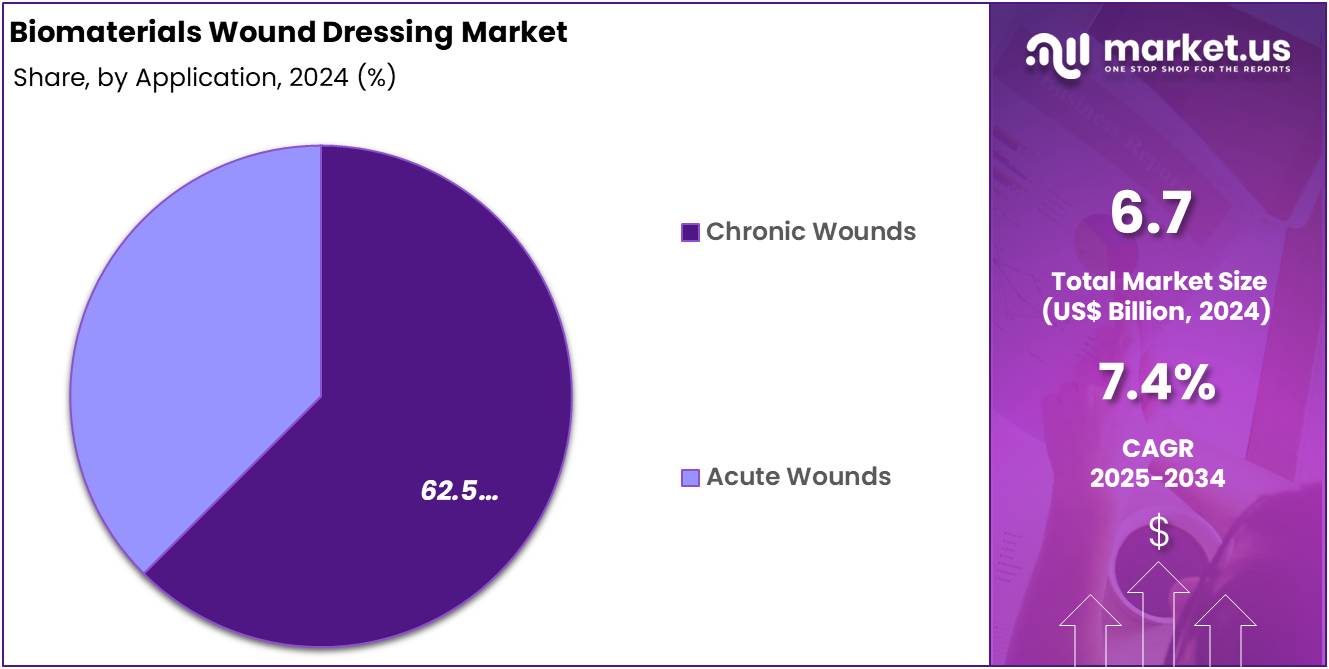

- In 2024, the market for biomaterials wound dressing market generated a revenue of US$ 6.7 billion, with a CAGR of 7.4%, and is expected to reach US$ 13.7 billion by the year 2033.

- By product type segment is divided into natural- alginate, collagen, chitosan, carboxymethyl cellulose (CMC), hydrocolloids, skin subtitles, honey, other natural materials, synthetic- polymeric, metallic, silicon, other. Natural biomaterials in which alginate taking the lead in 2024 with a market share of 63.2%.

- Considering channel, by application type segments is divided into chronic wounds- diabetic foot ulcers, pressure ulcers, venous leg ulcers, other chronic wounds and acute wounds- surgical & traumatic wounds, burn. Among these, chronic wound held a significant share of 62.5%.

- Based on end user hospitals, ambulatory surgical centers, home care settings, other end-users in which hospital accounted for the largest and fastest growing market share 43.3%.

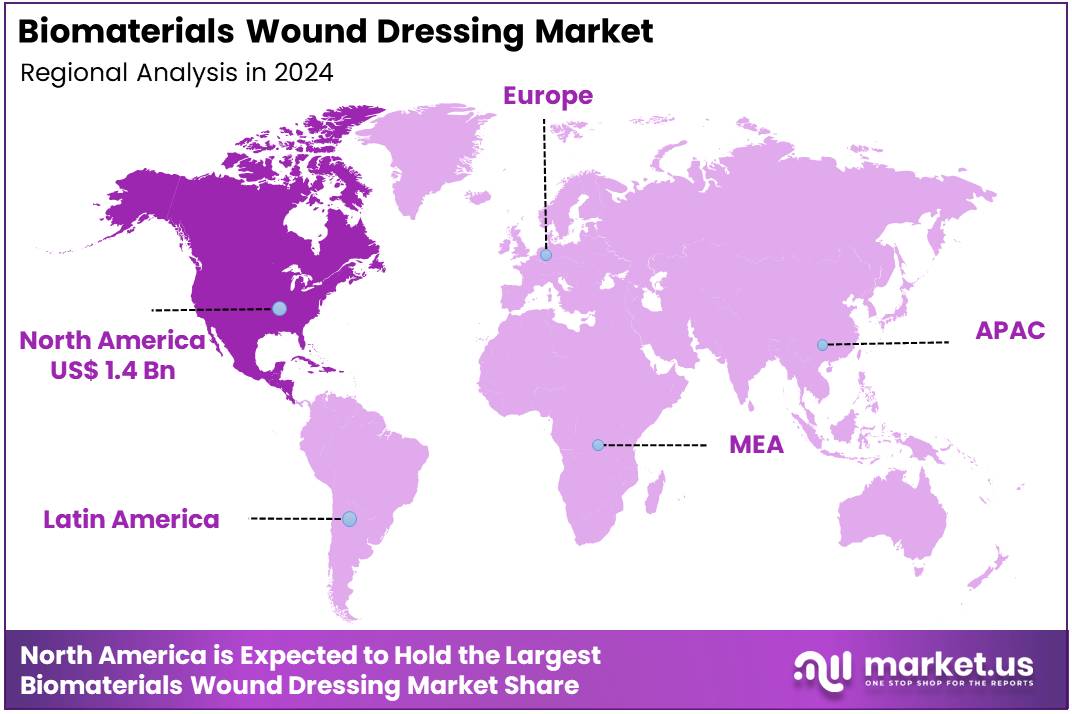

- North America led the market by securing a market share of 46.1% in 2024.

Product Type Analysis

In 2024, the biomaterial wound dressing market was primarily dominated by the natural segment with 63.2% share and within that alginate dressings captured substantial revenue driven by the growing preference for natural, plant-based wound care solutions. The demand for biocompatible and eco-friendly materials has significantly contributed to the rise of biomaterial dressings, which offer enhanced healing properties and a reduced risk of complications.

Alginate, a biopolymer known for its biocompatibility and non-toxic nature, is widely used in biomedical applications, particularly in wound healing. Its versatile nature allows it to be developed into various forms, including hydrogels, films, foams, wafers, and nanofibers, which enhances its adaptability in wound care. Alginate dressings are particularly effective for wounds with heavy exudate, such as ulcers and burns, as they provide excellent moisture management, maintain a moist healing environment, and possess antimicrobial properties.

Furthermore, the integration of antibacterial agents and nanoparticles enhances their therapeutic efficacy, helping to reduce infection risks and accelerate tissue regeneration. As concerns about traditional wound care solutions grow, the demand for natural, non-toxic, and biodegradable biomaterials like alginate continues to rise, solidifying its leadership in the biomaterial wound dressing market. These dressings not only help absorb excess wound fluid but also promote an optimal healing environment, especially for wounds with moderate to heavy exudation.

The therapeutic effectiveness of alginate dressings is influenced by factors such as the composition of polymers, cross-linking agents, and the incorporation of nanoparticles. The market’s shift toward innovative wound management solutions, focused on infection prevention and faster healing, further propels the growth of alginate-based dressings.

- A study published in the journal Personalized Medicine in September 2021 identified alginate as the most widely used and effective biomaterial for wound healing, surpassing other materials in terms of efficacy.

Application Type Analysis

The chronic wound segment of the biomaterial wound dressing market held a significant share of 62.5% in 2024, driven by the growing adoption of e-commerce platforms and the increasing demand for personalized care solutions tailored to managing chronic wounds. Chronic wounds, which can take years to heal and, in some cases, may never fully heal, result in considerable physical and emotional strain for patients while imposing substantial financial burdens on healthcare systems.

These wounds are a significant healthcare concern due to prolonged hospital stays, reduced quality of life for patients, and persistent challenges in dermatology. Chronic wounds are characterized by an extended and intense inflammatory phase that damages the extracellular matrix (ECM) and disrupts fibroblast function.

This prolonged inflammation can hinder the production and release of growth factors or lead to their excessive degradation by cellular or bacterial proteases, further delaying healing. The rising prevalence of chronic wounds presents a global health challenge, and efforts to reduce the prolonged inflammatory response have shown promise in enhancing healing rates.

Innovative biomaterial platforms that incorporate anti-inflammatory strategies are emerging as potential solutions to accelerate chronic wound repair. Statistics indicate that chronic wounds affect approximately 6.5 million patients annually, with associated wound care and management costs placing a significant financial strain on healthcare systems. In developing countries like India, challenges related to chronic wounds are compounded by factors such as low literacy rates, limited access to quality healthcare, reliance on imported medical equipment, affordability issues, and the lack of universal health insurance coverage.

By 2026, it is estimated that chronic wounds will impact approximately 20 – 60 million individuals worldwide, with long-term hospitalization placing additional pressure on healthcare systems due to the high costs of surgeries, advanced wound care products, and medical personnel resources, including physicians and nursing staff.

End User Type Analysis

The hospital segment is the dominant end-user category in the biomaterial wound dressing market, holding a significant market share due to the widespread use of wound dressings in hospital settings for a variety of wound types and surgical procedures.

Hospitals play a critical role in managing complex and severe wounds, such as chronic wounds, surgical wounds, and burns, and are equipped with advanced medical infrastructure and skilled healthcare professionals, making them the preferred choice for specialized wound care. In countries like India, hospitals are central to the advancement of wound care management, driven by their high demand for enhanced wound care solutions and their influence on treatment protocols.

As key healthcare centers, hospitals handle a wide range of wounds, including surgical incisions, diabetic ulcers, pressure sores, and traumatic injuries, among others. The availability of advanced biomaterial dressings and the ability to provide tailored care have strengthened hospitals’ position as the leading segment in the market.

Hospitals offer comprehensive wound care, with a particular focus on specialized treatment for chronic wounds, while addressing a diverse array of patient needs, from acute injuries to complex medical conditions. Understanding the varying needs of end-users some requiring highly specialized solutions and others seeking general-purpose applications is crucial for manufacturers and service providers, as it enables them to develop tailored products that address the distinct challenges of different industries.

- Based on a study conducted between 2021 and 2022 and published by NCBI, each year, five million patients are admitted to intensive care units. The prevalence of pressure ulcers varies significantly across different countries and healthcare systems. In European hospitals, the prevalence ranges from 3.8% to 23%, while in the US, it is reported at 12.3%. A systematic review in Iran found that the prevalence of pressure ulcers in healthcare settings, particularly in Iran, is approximately 19.59%.

Key Market Segments

Product Type

- Natural

- Alginate

- Collagen

- Chitosan

- Carboxymethyl cellulose (CMC)

- Hydrocolloids

- Skin subtitles

- Honey

- Others

- Synthetic

- Polymeric

- Metallic

- Silicon

- Others

Application

- Chronic Wounds

- Diabetic Foot Ulcers

- Pressure Ulcers

- Venous Leg Ulcers

- Other Chronic Wounds

- Acute Wounds

- Surgical & Traumatic Wounds

- Burn

End-user

- Hospitals

- Ambulatory surgical centers

- Home care settings

- Other end-users

Drivers

Rising Prevalence of Chronic Wounds

The increasing prevalence of chronic wounds, particularly diabetic foot ulcers (DFUs), is a significant concern, primarily driven by the rising global incidence of diabetes. As diabetes continues to affect millions worldwide, complications such as DFUs, which impact 15-25% of diabetic individuals, have become a major contributor to non-traumatic amputations. Factors such as poor blood circulation, high blood sugar levels, and neuropathy significantly impair the wound healing process in diabetic patients.

Additionally, the aging population is another key factor, as older individuals often experience reduced regenerative capacity and comorbidities, which further complicate wound healing. Chronic wounds are often stalled in one or more stages of the healing process due to pre-existing pathophysiological mechanisms, particularly in diabetic patients.

Pathological conditions in these individuals can delay wound recovery, but biomaterial wound dressings have shown promise in addressing these challenges. These dressings not only possess antiseptic properties but also carry biomolecules with anti-inflammatory, antimicrobial, and pro-angiogenic properties, which are particularly beneficial in treating diabetic wounds.

Despite ongoing innovations and increasing awareness of their benefits, challenges such as regulatory barriers and the lack of standardized protocols persist. However, the market for biomaterial wound dressings continues to grow, driven by the rising need for effective wound care solutions.

- As per the U.S. government projections, senior population is expected to surpass 77 million by 2060, suggesting that chronic wounds will become an increasingly prevalent issue in this demographic. Additionally, official data from the International Diabetes Federation projects that the number of diabetes patients in the UAE will rise to 1,325,800 by 2045, further highlighting the need for effective treatment solutions. As per NCBI, the lifetime risk of developing a foot ulcer in individuals with diabetes exceeds 33%. Diabetic foot ulcers lead to significant morbidity and are responsible for around two-thirds of all non-traumatic amputations in the US. These ulcers are the primary cause of non-traumatic lower-limb amputations in diabetic patients. Among hospitalized diabetic patients with foot ulcers, approximately 35.4% undergo lower extremity amputation.

Restraints

Regulatory Challenges

Regulatory challenges present significant barriers to the biomaterial wound dressing market, primarily due to the complexity of classification. Biomaterial wound dressings may fall under medical devices, medicinal products, or combination products, creating ambiguity in regulatory pathways.

Compliance with rigorous biocompatibility, safety, and efficacy standards further complicates the approval process, as these standards vary by region and demand extensive scientific validation. Manufacturers often struggle to provide sufficient evidence to support claims regarding the effectiveness and safety of innovative biomaterials, which can delay both product development and market entry.

Additionally, concerns regarding immune responses, where biomaterials could trigger adverse reactions, necessitate comprehensive testing and risk assessments. The emergence of antibiotic resistance in biomaterial-integrated wound care products compounds the regulatory burden, requiring specialized solutions and adherence to evolving guidelines.

Environmental concerns also remain, despite advances in biodegradable options, influencing perceptions of certain biomaterial wound dressings. These factors collectively hinder the growth and accessibility of biomaterial wound care products, underscoring the need for strategic solutions to navigate these challenges.

- In November 2023, the U.S. Food and Drug Administration (FDA) proposed a rule to reclassify certain wound dressings and liquid wound washes containing antimicrobials or other chemicals. If finalized, this rule would classify these products as Class II or III medical devices, subjecting them to more stringent regulatory requirements, including 510(k) submissions or premarket approval (PMA).

Opportunities

Rising Adoption in Homecare Settings

The increasing adoption of biomaterial wound dressings in homecare settings presents substantial opportunities, driven by the rising prevalence of chronic wounds and the growing need for convenient, cost-effective treatment options. As healthcare costs continue to rise, more patients with chronic diseases are opting for homecare solutions, which is expected to boost demand for active wound care products that help patients manage, diagnose, and monitor chronic and acute wounds from the comfort of their homes.

Patients with chronic wounds are often hesitant to travel long distances for medical care due to factors such as wound pain, limited mobility, or age, while also aiming to minimize their exposure to potential risks. Home wound care plays a crucial role in the overall management of chronic wound patients.

- In June 2023, a survey by the AARP Public Policy Research Institute found that around 35% of informal caregivers provide home-based wound care in Australia. Australia, up to 61% of wound patients receive care either from family caregivers or through self-care. This shift is anticipated to accelerate segment growth over the forecast period.

Additionally, the growing awareness of advanced wound care techniques, combined with a higher incidence of chronic wounds, is propelling the market for these products. Innovations in biomaterials designed to enhance healing, reduce infection risks, and provide increased patient comfort are contributing to the market’s expansion.

The use of biomaterial wound dressings in homecare is gaining momentum, especially with the increasing number of elderly individuals suffering from chronic wounds and a rising preference for home-based treatments. This demographic shift is poised to further drive the adoption of homecare wound management solutions.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic and geopolitical factors play a significant role in shaping the biomaterial wound dressing market. Rising healthcare costs and the increasing demand for personalized treatments are driving individuals toward advanced wound care solutions, including biomaterial dressings, as cost-effective and efficient alternatives.

Geopolitical factors, such as the integration of advanced wound care technologies into national healthcare systems, further support the growth of the biomaterial wound dressing market. However, challenges remain, including regulatory hurdles and the absence of standardized protocols for biomaterial wound dressings, which may hinder broader adoption, especially in countries with stringent medical regulations.

Despite these obstacles, the market is expected to experience steady growth, driven by the global recognition of the advantages of biomaterial-based solutions and increasing investments from both public and private sectors in research and development. Economic downturns and restricted healthcare budgets could potentially lead to reduced spending on non-essential medical products, such as premium wound care solutions.

Additionally, geopolitical instability, including trade disruptions and political tensions, may impact the supply of raw materials and escalate production costs, posing challenges to the market. After implementing aggressive tariffs on most of America’s trading partners, disrupting global markets, the US president announced on April 10, 2025, a 90-day pause on higher tariffs for most countries.

However, tariffs remain in effect for China, which supplies medical products used daily by hospitals. In fact, tariffs on Chinese imports have been raised to 125%. The hospital supplies sector is facing significant losses due to these tariffs. The tariffs are expected to impact up to 78% of all 510(k)-approved hospital supplies manufactured outside the U.S. More specifically, this will directly affect 66% of those supplies that are solely produced abroad.

Latest Trends

Bioactive Dressings for Enhanced Healing

The bioactive wound dressing market is experiencing significant growth, driven by strategic partnerships and collaborations among manufacturers, healthcare providers, and research institutions focused on developing innovative wound care solutions. Increasingly, wound care is being delivered in home settings, fueled by technological advancements and the growing demand for remote care. This shift is supported by innovations such as bioengineered skin substitutes, antimicrobial dressings, and negative pressure wound therapy, all of which contribute to better treatment outcomes and higher patient satisfaction.

The integration of digital health tools, telemedicine, and smart wound sensors is enabling personalized care and real-time monitoring, further enhancing the effectiveness of home-based wound care. Continuous advancements in bioactive wound care products, including bioengineered tissues, growth factors, and stem cell therapies, are significantly improving healing processes, reducing complications, and driving market growth.

Companies are increasingly combining traditional wound care approaches with modern biomaterial technologies to offer comprehensive, effective treatments. In particular, advanced wound care products such as hydrocolloids, hydrogels, and alginate dressings are gaining popularity for their superior effectiveness. Hydrocolloids, for example, create a gel that maintains a moist healing environment while providing protection against infections.

Emerging trends in this area include the use of hydrogels, bioadhesives, and cutting-edge fabrication techniques like 3D printing. The industry is also seeing the rise of smart materials, sensors, and personalized medicine, which are shaping the future of bioactive wound dressings. Hyaluronic acid dressings are especially effective in managing both acute and chronic wounds with low to moderate exudate, often used alongside secondary dressings.

Meanwhile, honey-based dressings are particularly beneficial for treating infected wounds, including those with antibiotic-resistant bacteria. Alginate hydrogels have been shown to enhance antibacterial activity and promote cell proliferation, while alginate films, which also possess strong antibiotic properties, support the re-epithelialization process, further highlighting the effectiveness of these advanced dressings.

Regional Analysis

North America is leading the Biomaterial Wound Dressing Market

North America is leading the biomaterial wound dressing market, held the highest revenue share due to growing demand for holistic wellness solutions and natural therapies. This trend reflects a strong preference for innovative, biocompatible wound care products that align with the region’s focus on sustainable and natural healthcare. Additionally, North America is home to major companies and research institutions that consistently invest in developing cutting-edge technologies such as bioactive and nanocomposite materials, which enhance the effectiveness of wound care products.

The high prevalence of diabetic ulcers in the US, largely driven by the growing number of individuals with diabetes, is contributing to the demand for advanced wound care solutions. Factors like poor diabetes management, prolonged disease duration, and complications such as peripheral neuropathy and peripheral artery disease increase the likelihood of developing diabetic foot ulcers. Lifestyle factors, including sedentary behaviors and unhealthy diets, also exacerbate the risk.

The biomaterial wound dressing market in North America is highly concentrated, with major industry players maintaining dominance. The region’s strong healthcare infrastructure, substantial healthcare spending, and ongoing research and development initiatives further solidify this leadership.

- For instance, in the U.S. about 1.6 million cases of DFUs occurred annually, with approximately half of these ulcers becoming infected. In about 20% of infected cases, amputation of part or all of the foot is required. In addition, the cost burden associated with surgical site infections (SSI) in the U.S. significantly impacts the biomaterial wound dressing market. In the US, SSIs lead to patients spending over 400,000 additional days in the hospital, resulting in an extra annual cost of US$ 900 million.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of Asia Pacific

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the biomaterial wound dressing market are increasingly focusing on expanding their product portfolios to meet the growing demand for advanced wound care solutions. Companies are making substantial investments in research and development to innovate biomaterials with enhanced properties, such as antimicrobial activity, moisture management, and tissue regeneration. Strategic partnerships with hospitals, clinics, and homecare providers are improving accessibility and bolstering market credibility.

Additionally, the integration of smart technologies, like sensors and drug delivery systems, is gaining momentum, offering more personalized and responsive care for patients. The use of digital health platforms is also becoming more common, enhancing patient engagement and streamlining the distribution of biomaterial wound dressings, particularly in remote areas. Many companies are also prioritizing sustainability by developing eco-friendly and biodegradable wound care products, aligning with environmental trends.

Moreover, obtaining regulatory approvals for evidence-based biomaterial solutions is fostering user trust and accelerating market adoption. These strategies collectively reflect the dynamic efforts by market leaders to address the evolving healthcare needs and drive innovation within the biomaterial wound dressing sector.

Top Key Players

- Smith & Nephew PLC

- Braun Melsungen AG

- 3M

- Mölnlycke Health Care AB

- URGO

- Integra LifeSciences

- Acelity

- ConvaTec Group PLC

- Coloplast Corp

- Medline Industries, Inc.

- DermaRite Industries LLC

- Medtronic plc.

Recent Developments

- In January 2024, 3M’s medical solutions division has been granted US$ 34.2 million by the U.S. Army Medical Research Acquisition Activity. The funding will support the development of new solutions for infection prevention, as well as wound management and healing. 3M will work in collaboration with the University of Minnesota Medical School, the 59th Medical Wing Science & Technology Office of the Chief Scientist (59MDW/ST), Naval Medical Research Unit-San Antonio (NAMRU-SA), and The University of Texas Health Science Center at San Antonio (UT Health San Antonio) on this initiative.

- In July 2023, Coloplast A/S expanded its wound care portfolio by entering into an agreement to acquire Kerecis, a company celebrated for its patented technology that uses intact fish skin for wound and burn treatment. This acquisition also prompted Coloplast to raise its long-term growth projections.

- In July 2021, Axio Biosolutions, a MedTech company, secured US$ 6 million in Series B2 equity funding, led by TrueScale Capital. The company plans to expand its commercial footprint in the US and EU, while also enhancing its operations in India. Axio’s groundbreaking products are currently being utilized in India, Europe, and more than 40 other countries. In February 2021, Axio received regulatory approval from the US FDA for Axiostat and the EU CE Mark for Maxiocel, enabling its use in advanced wound care applications.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 6.7 Bn |

| Forecast Revenue (2034) | US$ 13.7 Bn |

| CAGR (2025-2034) | 7.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Natural- Alginate, Collagen, Chitosan, Carboxymethyl Cellulose (CMC), Hydrocolloids, Skin Subtitles, Honey, Others; Synthetic- Polymeric, Metallic, Silicon, Others), By Application (Chronic Wounds- Diabetic Foot Ulcers, Pressure Ulcers, Venous Leg Ulcers, Other Chronic Wounds; Acute Wounds- Surgical & Traumatic Wounds, Burn), By End-User (Hospitals, Ambulatory Surgical Centers, Home Care Settings, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Smith & Nephew PLC, B. Braun Melsungen AG, 3M, Mölnlycke Health Care AB, URGO, Integra LifeSciences, Acelity, ConvaTec Group PLC, Coloplast Corp, Medline Industries, Inc., DermaRite Industries LLC, Medtronic plc |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |