Quick Navigation

Report Overview

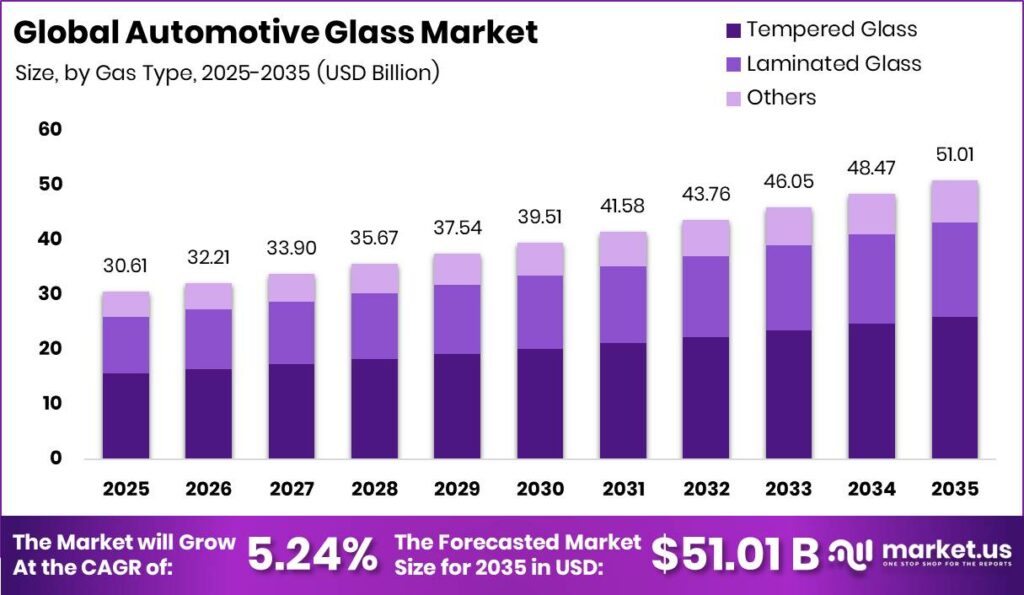

Global Automotive Glass Market size is expected to be worth around USD 51.01 Billion by 2035 from USD 30.61 Billion in 2025, growing at a CAGR of 5.24% during the forecast period 2026 to 2035. This steady expansion reflects rising glass content per vehicle and higher-value glazing formats. Suppliers gain a decade-long window to reprice product lines upward and lock in OEM programs.

Automotive glass covers windshields, side windows, rear glass, and roof panels fitted to passenger and commercial vehicles. The market splits across glass type, technology, application, vehicle type, and sales channel. Manufacturers serve two distinct buyers, factory OEM lines and the replacement aftermarket. This structure lets investors target either high-volume OEM contracts or higher-margin aftermarket demand with separate strategies.

Key Takeaways

- Global Automotive Glass Market will reach USD 51.01 Billion by 2035, up from USD 30.61 Billion in 2025.

- The market grows at a CAGR of 5.24% across the 2026 to 2035 forecast period.

- Tempered Glass leads the By Glass Type segment with a 51.10% share.

- Standard Glass holds 42.10% of the By Technology segment.

- Windshield leads By Application with a 37.20% share.

- Passenger Cars dominate By Vehicle Type with a 68.50% share.

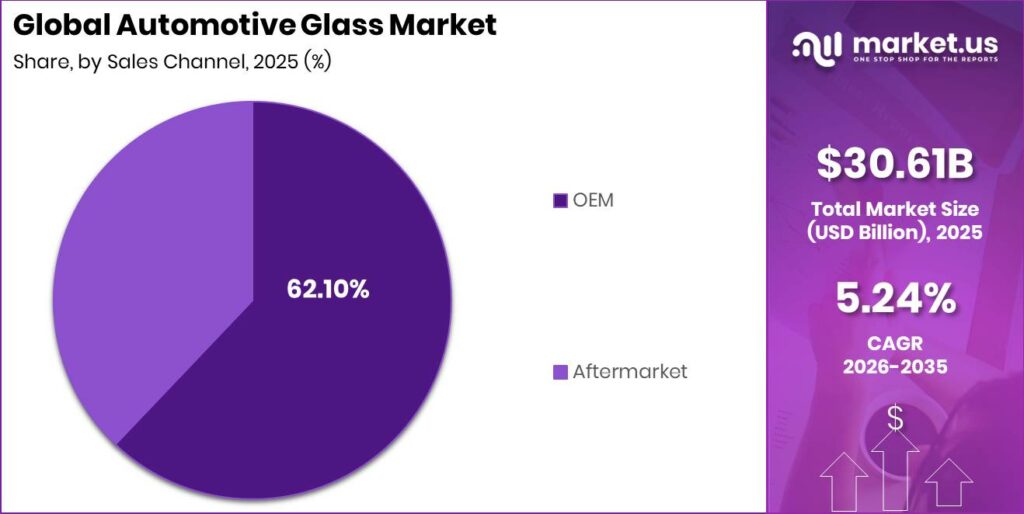

- OEM channels account for 62.10% of the By Sales Channel segment.

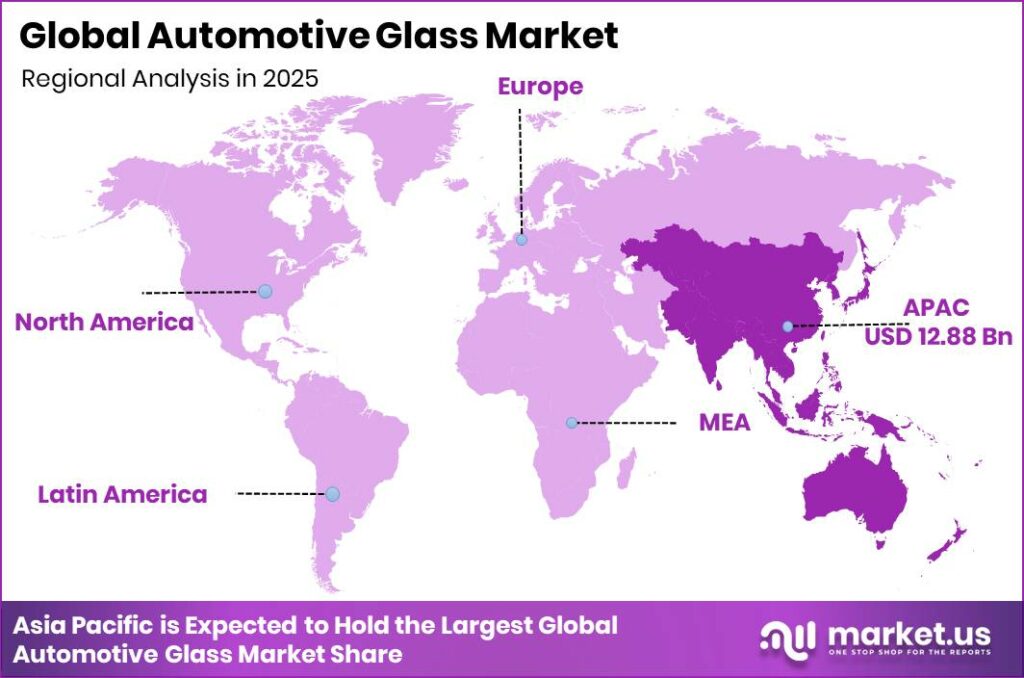

- Asia Pacific dominates with a 42.10% regional share, valued at USD 12.88 Billion.

Government policy now shapes glass demand as much as consumer taste. The EU General Safety Regulation forced advanced driver-assistance features onto new vehicles, lifting demand for sensor-ready windshields. India applies import tariffs on finished automotive glass panels to protect domestic producers. This means suppliers must plan capacity around regional rules, not just volume, to keep programs profitable and compliant.

Decarbonization mandates now push glassmakers toward low-carbon production. Saint-Gobain’s ORAÉ glass achieves a 42% reduction in embodied carbon versus standard European clear glass while holding equal technical performance. This lets OEMs cut supply-chain emissions without redesigning parts. Suppliers offering verified low-carbon glass will win preferred status on decarbonization-focused vehicle platforms and defend pricing. Explore adjacent demand through Automotive Interior Materials.

Recycled content strengthens this sustainability edge further. ORAÉ glass contains 64% recycled material, sharply cutting virgin raw-material consumption for advanced glass manufacturing. This reduces exposure to volatile soda ash and silica input costs. As a result, producers that build closed-loop recycling capacity gain both a cost buffer and a compliance advantage as circular-economy rules tighten across major automotive regions.

Glass Type Analysis

Tempered Glass dominates with 51.10% due to strength, safety, and low cost.

In 2025, Tempered Glass held a dominant market position in the By Glass Type segment of Automotive Glass Market, with a 51.10% share. This glass shatters into blunt fragments, meeting safety norms for side and rear windows. Its lower processing cost suits high-volume production lines. Suppliers scaling tempered output can defend volume contracts while funding investment in higher-margin laminated and smart glass formats.

Laminated Glass bonds two glass layers around a plastic interlayer, holding fragments in place after impact. This construction supports windshields and acoustic insulation duties. Regulators increasingly require laminated safety glass on side and rear windows across the European Union and India. This creates a clear upgrade path for suppliers to shift buyers from tempered to higher-value laminated products over the forecast period.

Other glass types cover specialty and coated variants serving niche vehicle and comfort needs. These formats round out supplier portfolios beyond mainstream tempered and laminated lines. Manufacturers use them to test premium features before mass rollout. This means investors should view the Others category as an innovation pipeline rather than a core volume driver in the near term.

Technology Analysis

Standard Glass dominates with 42.10% due to broad fitment and low unit cost.

In 2025, Standard Glass held a dominant market position in the By Technology segment of Automotive Glass Market, with a 42.10% share. This basic glazing serves entry and mid-range vehicles where cost control matters most. Its wide fitment keeps volumes high across every region. Suppliers should treat standard glass as a stable cash base that funds development of premium smart and solar-control formats.

Smart Glass and Electrochromic Glass let occupants dim windows electronically, replacing physical shades. This technology suits premium cabins and panoramic roofs. Fuyao Glass Industry Group advanced high-value glazing including panoramic sunroof and HUD-compatible glass to meet rising OEM demand in March 2025. This signals a shift toward feature-rich glazing that lets suppliers command higher prices per vehicle.

Solar Control Glass reflects heat to cut cabin temperature and cooling load. This feature helps electric vehicles preserve battery range. Buyers in hot climates value the comfort and efficiency gains directly. Manufacturers positioning solar control as an EV range enabler can attach premium pricing to a fast-growing vehicle segment across major markets. Compare adjacent demand via Automotive Tinting Film.

Acoustic Glass uses a sound-damping interlayer to reduce cabin noise at speed. This suits luxury vehicles and long-distance commercial fleets seeking comfort. Quieter cabins support premium brand positioning for automakers. This means acoustic glazing gives suppliers a clear feature to bundle with laminated products, lifting average selling prices without adding heavy production complexity.

Application Analysis

Windshield dominates with 37.20% due to safety mandates and sensor integration.

In 2025, Windshield held a dominant market position in the By Application segment of Automotive Glass Market, with a 37.20% share. Windshields carry cameras, sensors, and heating zones for advanced driver-assistance systems. This role converts a simple panel into a value-added assembly. Suppliers with camera-aperture and calibration expertise can charge premium prices and lock in long OEM co-development contracts.

Sidelite windows cover the side openings and increasingly must use laminated safety glass under new rules. This raises material content per vehicle beyond basic tempered panels. Regulators in the European Union and India drive this shift directly. As a result, suppliers gain incremental laminated volume as side-window mandates spread across more vehicle programs and regions.

Backlite, or rear glass, provides visibility and often carries defrost heating elements. This application supports both passenger and commercial vehicles. Emerging designs embed antennas and radar-transparent zones into rear windows. This creates room for suppliers to add electronic functions to a once-basic panel and raise per-unit value across the range.

Roof glass and panoramic sunroofs expand glazed surface area, especially on SUVs and electric vehicles. Others, including quarter glass and specialty panels, hold the remaining share collectively. These formats grow cabin brightness and premium appeal for buyers. This means suppliers investing in large-format roof glass capture rising glass area per vehicle.

Vehicle Type Analysis

Passenger Cars dominate with 68.50% due to high global production volumes.

In 2025, Passenger Cars held a dominant market position in the By Vehicle Type segment of Automotive Glass Market, with a 68.50% share. Passenger cars drive the bulk of global vehicle output and glass fitment. Their sheer volume anchors supplier revenue and factory utilization. Manufacturers that secure passenger-car OEM contracts gain the scale needed to fund premium glazing development across their portfolios.

Light Commercial Vehicles serve delivery and trade fleets that demand durability and low cost. This segment values reliable, easily replaced glass over premium features. Rising e-commerce logistics supports steady LCV output. This means suppliers can pursue stable, volume-based glass contracts with fleet operators seeking dependable replacement supply.

Heavy Commercial Vehicles use large windshields and specialized glazing built for tough duty cycles. These vehicles require thicker, more robust panels than passenger cars. Their long service life sustains aftermarket replacement demand. As a result, suppliers can build durable revenue from both original fitment and a steady stream of HCV glass replacements.

Electric Vehicles increasingly adopt panoramic roofs, solar control, and acoustic glazing to lift range and comfort. This raises glass value per vehicle well above conventional cars. EV makers treat glazing as a differentiation feature. This creates a high-value opportunity for suppliers that align smart and solar-control glass with the fast-expanding electric vehicle segment.

Sales Channel Analysis

OEM dominates with 62.10% due to factory fitment on new vehicles.

In 2025, OEM held a dominant market position in the By Sales Channel segment of Automotive Glass Market, with a 62.10% share. OEM channels supply glass directly to vehicle assembly lines under long-term contracts. This locks suppliers into stable, high-volume programs. Manufacturers winning OEM approval gain predictable revenue and early access to next-generation glazing specifications.

Aftermarket covers replacement glass sold after a vehicle leaves the factory, driven by damage and wear. This channel offers higher margins than OEM supply but faces calibration hurdles on ADAS glass. An expanding global vehicle parc sustains steady replacement demand. This means suppliers with recalibration capability can capture premium aftermarket revenue that rivals cannot easily serve.

Key Market Segments

By Glass Type

- Tempered Glass

- Laminated Glass

- Others

By Technology

- Standard Glass

- Smart Glass / Electrochromic Glass

- Solar Control Glass

- Acoustic Glass

By Application

- Windshield

- Sidelite (Side Windows)

- Backlite (Rear Glass)

- Roof Glass / Panoramic Sunroof

- Others

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- Electric Vehicles (EV)

By Sales Channel

- OEM

- Aftermarket

Regional Analysis

Asia Pacific Dominates the Automotive Glass Market with a Market Share of 42.10%, Valued at USD 12.88 Billion

Asia Pacific led the Automotive Glass Market in 2025 with a 42.10% share worth USD 12.88 Billion. China, India, and Southeast Asia drive this lead through high vehicle production and sales. Local factories keep glass supply close to assembly lines. This means suppliers building capacity in Asia Pacific gain proximity to the world’s largest and fastest-growing vehicle output base.

Asia Pacific also ranks as the fastest-growing region, powered by rising vehicle production across China, India, and Southeast Asia. Expanding middle-class demand lifts passenger-car sales year after year. Local content rules encourage domestic glass manufacturing. As a result, investors targeting organized OEM glass localization in India and ASEAN can capture new volume before competitors establish scale.

Europe and North America anchor demand for premium, sensor-integrated, and low-carbon glazing under strict safety and emissions rules. Guardian Glass introduced energy-efficient coated automotive glass to improve thermal comfort and support electric vehicle range in April 2025. Latin America and Middle East and Africa add aftermarket and replacement volume. This means suppliers can match product tiers to each region’s distinct regulatory and buyer profile.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Drivers

Safety regulators across Europe, the United States, and Japan now mandate advanced driver-assistance features on new vehicles. The EU General Safety Regulation required emergency braking, lane-keeping, and drowsiness detection on new light-duty approvals from July 2024. Each feature needs an optically qualified windshield with camera zones and sensor pads. This raises the average selling price of an ADAS windshield by an estimated 22–35% versus a standard laminated equivalent.

By 2025, over 90 million new vehicles carried at least one ADAS windshield technology, up from under 55 million in 2021. This fitment shift structurally reprices the entire OEM windshield segment upward. OEM supply deals now demand 24–36 month co-development cycles and recalibration documentation. As a result, suppliers convert a commodity part into a value-added assembly earning gross margins 8–14 percentage points above standard windshields. See Automotive Camera And Integrated Radar And Camera.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ADAS & Safety Regulation Mandates Driving Sensor-Integrated Windshields | +1.60% | Global — led by Europe, North America, Japan, South Korea | Short term (≤ 2 years) |

| Rising Vehicle Production & Sales in Asia Pacific | +1.20% | China, India, Southeast Asia | Short term (≤ 2 years) |

| SUV & Crossover Segment Growth Increasing Glass Surface Area per Vehicle | +0.85% | Global — most acute in China, North America, Middle East | Short term (≤ 2 years) |

| Laminated Safety Glass Regulatory Mandates for Side & Rear Windows | +0.65% | European Union, India, Brazil, ASEAN | Medium term (2–4 years) |

| Aftermarket Replacement Demand from Expanding Global Vehicle Parc | +0.55% | North America, Europe, Middle East & Africa | Short term (≤ 2 years) |

| Lightweight Acoustic & Thermal Glazing Adoption for Fuel Economy Compliance | +0.39% | Europe, Japan, North America | Medium term (2–4 years) |

Restraints

The U.S. administration’s 25% tariff on Canadian and Mexican goods took effect March 4, 2025, hitting automotive glass under HS Chapter 70. A windshield assembler in Canada exporting to a U.S. OEM now faces a landed-cost uplift of 15–20% on tariffed content. This category typically operates at 12–18% gross margin at Tier-1 level. This means some cross-border supply relationships turn loss-making at current contract prices.

India applies import tariffs of 15–20% on finished automotive glass panels, protecting domestic producers. This shields local makers but restricts imports of smart glass and ADAS-certified laminates needed for premium programs. Global suppliers with North American chains face forced CapEx reallocation. As a result, nearshoring investments demand 18–30 months of lead time while margin compression persists in the interim.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cross-Border Trade Tariffs Freezing Glass Component Import Economics | -1.10% | United States, Canada, European Union, India | Short term (≤ 2 years) |

| High Capital Intensity of Float Glass Furnace Investment Limiting New Entrants | -0.65% | Global — most restrictive in emerging markets | Long term (≥ 4 years) |

| OEM Platform Electrification Restructuring Glass Spec & Supply Pipelines | -0.45% | China, Europe, North America | Medium term (2–4 years) |

| Insurance & Repair Cost Escalation Suppressing Aftermarket Replacement Rates | -0.35% | North America, Western Europe | Short term (≤ 2 years) |

| Chinese Overcapacity-Driven Price Dumping Compressing Global ASPs | -0.29% | Southeast Asia, Middle East, Africa, Latin America | Short term (≤ 2 years) |

Challenges

A technical gap divides sophisticated ADAS windshields from the aftermarket network that must replace them. These windshields need refractive tolerances within ±0.5% and sensor alignment within 1–2 mm of OEM specification. As of 2025, fewer than 30–40% of independent glass shops had recalibration equipment costing USD 10,000–30,000 per bay. This gap blocks many shops from validating post-replacement system performance to OEM standards.

ADAS replacement jobs extend cycle times by 90–150 minutes versus standard work, and mis-calibrated installs raise warranty claims to 3–5× normal rates. Some owners delay replacements or choose non-certified glass, suppressing aftermarket revenue. Industry groups estimate a 4–6 year buildout for nationwide recalibration coverage. This creates a clear revenue stream for shops and suppliers that invest early in certified calibration infrastructure and technician training.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| ADAS Recalibration Complexity at Replacement | -0.70% | Global — most acute in North America & Europe aftermarket | Medium term (2–4 years) |

| Precision Optical-Grade Manufacturing Talent Gap | -0.55% | South Asia, Southeast Asia, Eastern Europe | Long term (≥ 4 years) |

| Automotive Glass End-of-Life Recycling Bottleneck | -0.45% | European Union, India, North America | Long term (≥ 4 years) |

| Soda Ash & Silica Input Price Volatility | -0.35% | Global — most acute in import-dependent emerging markets | Medium term (2–4 years) |

| OEM Multi-Platform SKU Proliferation Burden | -0.30% | Global — concentrated at Tier-1 glazing suppliers | Long term (≥ 4 years) |

Opportunities

Augmented reality windshields remain untapped white space at mass-market scale. As of 2025 to 2026, series-production AR deployments stayed confined to luxury programs, leaving vehicles priced between USD 25,000 and USD 55,000 almost fully un-penetrated. The technology laminates a transparent waveguide into the windshield, projecting navigation and hazard alerts at a 7–10 metre focal distance. This eliminates the separate HUD projector box and cuts cockpit integration cost by an estimated 15–20%.

The unit economics shift dramatically for glass makers. A conventional OEM laminated windshield sells at roughly USD 80–150, while an AR-integrated assembly commands USD 350–650, a 3–4× price uplift. As of 2025, the AR windshield market reached about USD 435–480 Million, growing above 11% CAGR yet under 1% of windshield volume. This means early movers in waveguide integration capture a sizable untapped commercial opportunity.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Augmented Reality & HUD Windshield Commercialization | +1.50% | North America, Europe, China, Japan, South Korea | Medium term (2–4 years) |

| Electrochromic & Smart Glass Scaling into Mass-Market Vehicles | +1.10% | China, Europe, North America | Medium term (2–4 years) |

| EV Panoramic Solar Roof Glass Integration | +0.80% | China, Europe, North America | Long term (≥ 4 years) |

| Closed-Loop Automotive Glass Recycling & Circular Economy Compliance | +0.55% | European Union, United Kingdom, Japan | Long term (≥ 4 years) |

| India & ASEAN Organized OEM Glass Manufacturing Localization | +0.45% | India, Vietnam, Indonesia, Thailand | Short term (≤ 2 years) |

Key Company Insights

AGC Inc. positions itself around premium functional glazing that protects occupants and interiors. According to AGC, its 2025 automotive laminated UV-cut glass blocks approximately 99% of ultraviolet radiation, reducing skin damage and interior material degradation. This gives AGC a clear comfort and durability selling point for premium and electric vehicle programs. This creates an advantage in winning OEM contracts where cabin quality and long-term material performance drive purchasing decisions.

Saint-Gobain S.A. anchors its strategy in verified low-carbon glass to meet OEM decarbonization goals. Data from Saint-Gobain shows its ORAÉ glass carries a footprint of only 6.64 kg CO₂e per square metre on a 4 mm substrate. The company expanded its sustainable mobility portfolio through low-carbon manufacturing investment in February 2025. This positions Saint-Gobain to win preferred supplier status, though rivals matching its recycled-content edge remain a competitive risk.

Key Players

- AGC Inc.

- Saint-Gobain S.A.

- Fuyao Glass Industry Group Co., Ltd.

- Nippon Sheet Glass Co., Ltd.

- Xinyi Glass Holdings Limited

- Guardian Industries Holdings, LLC

- Central Glass Co., Ltd.

- Sisecam Group

- Corning Incorporated

- Taiwan Glass Industry Corporation

- Vitro, S.A.B. de C.V.

- Pilkington (NSG Group)

Recent Developments

- January 2025 – AGC Inc. announced the commercialization of next-generation automotive glass solutions focused on improving lightweight performance and compatibility with advanced driver-assistance systems (ADAS), supporting smart vehicle glazing.

- May 2025 – NSG Group (Pilkington Automotive) strengthened its automotive glazing portfolio by advancing lightweight and high-performance glass technologies designed for connected and electric vehicles, with emphasis on optical quality and safety.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 30.61 Billion |

| Forecast Revenue (2035) | USD 51.01 Billion |

| CAGR (2026-2035) | 5.24% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Glass Type (Tempered Glass, Laminated Glass, Others), By Technology (Standard Glass, Smart Glass / Electrochromic Glass, Solar Control Glass, Acoustic Glass), By Application (Windshield, Sidelite (Side Windows), Backlite (Rear Glass), Roof Glass / Panoramic Sunroof, Others), By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCV), Heavy Commercial Vehicles (HCV), Electric Vehicles (EV)), By Sales Channel (OEM, Aftermarket) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | AGC Inc., Saint-Gobain S.A., Fuyao Glass Industry Group Co., Ltd., Nippon Sheet Glass Co., Ltd., Xinyi Glass Holdings Limited, Guardian Industries Holdings, LLC, Central Glass Co., Ltd., Sisecam Group, Corning Incorporated, Taiwan Glass Industry Corporation, Vitro, S.A.B. de C.V., Pilkington (NSG Group) |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |