Quick Navigation

Report Overview

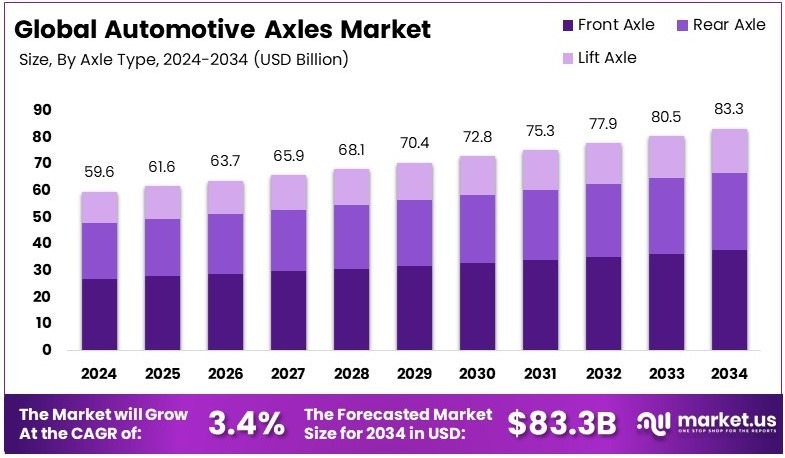

The Global Automotive Axles Market size is expected to be worth around USD 83.3 Billion by 2034, from USD 59.6 Billion in 2024, growing at a CAGR of 3.4% during the forecast period from 2025 to 2034.

Automotive axles are key components in a vehicle that connect the wheels and help them rotate. They also support the weight of the vehicle. Axles play a role in driving, braking, and steering. Strong and durable axles are important for vehicle stability, load handling, and overall driving performance.

The automotive axles market refers to the global business of producing and selling axles for vehicles. This includes axles for cars, trucks, buses, and off-road vehicles. The market tracks demand, innovation, and sales trends. Growth depends on vehicle production, technology upgrades, and demand for durable, fuel-efficient mobility solutions.

Automotive axles are essential components that support vehicle weight, connect the wheels, and help deliver engine power. Their demand has grown alongside rising vehicle production and stricter efficiency standards.

According to the International Organization of Motor Vehicle Manufacturers (OICA), global passenger car production reached 65.3 million units in 2023, highlighting strong demand for axle systems worldwide. This demand is further boosted by growing car ownership in emerging markets and rising investments in advanced mobility solutions.

To illustrate, the increasing adoption of electric vehicles is reshaping the axle market. Electric vehicles require lighter and more efficient axle systems to manage battery loads and enhance performance. Consequently, automotive suppliers are investing in innovation to meet new vehicle architectures.

For example, American Axle & Manufacturing made a strategic move in January 2025, acquiring British auto parts maker Dowlais for £1.2 billion. According to Reuters, this acquisition aims to strengthen its EV component capabilities and global reach. Such moves reflect how companies are preparing for the future of mobility.

In addition, regulatory policies are pushing manufacturers to adapt. In the United States, the Environmental Protection Agency (EPA) has introduced fuel economy standards requiring a fleet average of 40.4 miles per gallon by 2026. These policies are prompting automakers to integrate lightweight and energy-efficient components like advanced axles. As a result, both traditional and electric vehicle models are being redesigned with efficiency in mind.

Meanwhile, government support is playing a key role in sustaining supplier competitiveness. According to a White House press release, the U.S. government launched a $1 billion Drive Forward Fund to help small and medium-sized auto suppliers shift toward EV production. This funding aims to preserve jobs and stabilize the domestic supply chain during the industry’s electrification phase.

On the other hand, market conditions vary by region. Developed markets like North America and Europe show signs of saturation, with intense competition among established players. However, countries in Asia-Pacific, such as India and China, still offer room for growth due to increasing vehicle demand and infrastructure development. Therefore, many companies are shifting focus to these high-potential markets to maintain long-term growth.

Key Takeaways

- The Automotive Axles Market was valued at USD 59.6 billion in 2024 and is expected to reach USD 83.3 billion by 2034, with a CAGR of 3.4%. Rising vehicle production and demand for lightweight axles drive market growth.

- In 2024, Front Axle dominated with 45.2%, as it plays a critical role in steering and load distribution in vehicles.

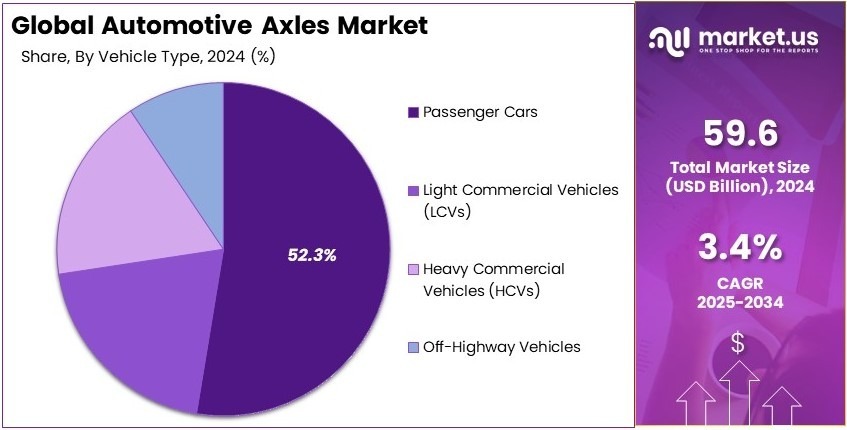

- In 2024, Passenger Cars led the market with 52.3%, driven by increasing consumer demand for fuel efficiency and vehicle stability.

- In 2024, Rear Axles remained a key segment, supporting vehicle load distribution and power transmission for improved performance and durability.

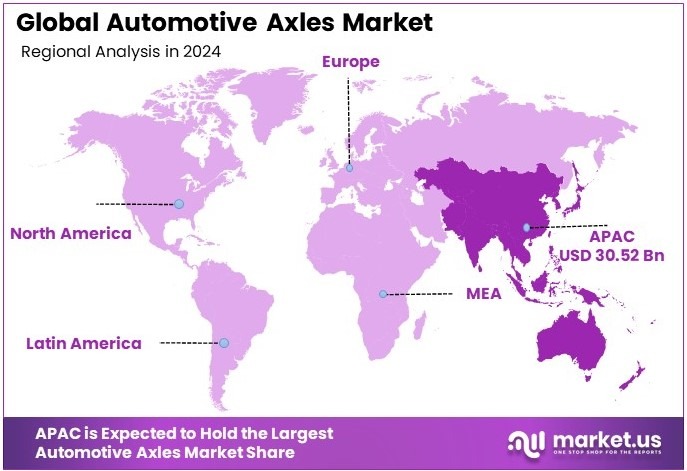

- In 2024, Asia Pacific dominated with 51.2% with valuation of USD 30.52 billion, due to strong automotive manufacturing and demand in China and India.

Type Analysis

Front axle dominates with 45.2% due to its critical role in vehicle steering and stability.

The automotive axles market can be segmented into front axle, rear axle, and lift axle. The front axle stands out significantly as it not only supports the weight of the front part of the vehicle but also plays a crucial role in steering and handling stability.

This segment’s dominance, representing approximately 45.2% of the market, is primarily driven by the increasing demand for vehicles that offer enhanced safety and driving dynamics, particularly in emerging markets where robust vehicle architecture is essential.

The rear axle, which facilitates power transfer from the transmission to the wheels in rear-wheel-drive vehicles, contributes to vehicle performance by improving traction control and load management. Its strategic importance is reflected in its substantial role within the market.

Lastly, the lift axle technology, which allows axles to be raised or lowered depending on the vehicle load, enhances the efficiency of commercial vehicles. It plays a vital role in improving fuel efficiency and reducing wear, thereby supporting operational flexibility and cost savings across the logistics and transportation industry.

Vehicle Type Analysis

Passenger cars dominate with 52.3% due to their high volume in global vehicle sales.

Among the vehicle types in the automotive axles market, passenger cars, light commercial vehicles (LCVs), heavy commercial vehicles (HCVs), and off-highway vehicles are key segments. The passenger cars segment leads with an impressive 52.3%, spurred by high global sales volumes and a marked preference for personal vehicles over public transport, particularly in the post-pandemic era.

Light commercial vehicles (LCVs) are increasingly crucial in urban logistics, particularly for last-mile delivery services driven by the surge in e-commerce. This segment’s growth underscores the need for efficient delivery systems in response to rising consumer demand.

Heavy commercial vehicles (HCVs) are indispensable for transporting heavy loads over long distances, with their utility spanning across construction, mining, and logistics sectors. Their substantial role in these industries highlights their importance in sustaining economic activities.

Off-highway vehicles cater specifically to agricultural and construction tasks, capable of operating in rugged environments. The demand for these vehicles is supported by ongoing infrastructure development and increased agricultural output, driving growth in this sub-segment.

Key Market Segments

By Axle Type

- Front Axle

- Rear Axle

- Lift Axle

By Vehicle Type

- Passenger Cars

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

- Off-Highway Vehicles

Driving Factors

Efficiency and Global Expansion Drives Market Growth

The automotive axles market is experiencing steady growth, largely driven by multiple supportive factors that are reshaping the industry. One of the most prominent contributors is the integration of lightweight materials into axle design. Using materials such as aluminum and advanced composites helps reduce the overall weight of the vehicle. This, in turn, boosts fuel efficiency and aligns with global emission regulations. Manufacturers are increasingly focused on meeting these environmental goals while also cutting operational costs.

In parallel, the rise of the e-commerce and logistics industry has significantly increased demand for commercial vehicles. With more delivery trucks and vans on the road, there is a growing need for durable and high-performance axles that can handle long distances and varied terrain. As consumers expect faster delivery times, logistics companies are expanding their fleets, which fuels axle demand.

Furthermore, the adoption of multi-axle vehicles in off-road and heavy-duty applications is on the rise. These vehicles, often used in construction, mining, and agriculture, require strong axles that can support heavy loads and rough terrain.

Lastly, increased vehicle export and global trade activities open new opportunities for axle manufacturers. As automotive companies enter new international markets, the demand for reliable axle systems grows, driving further market expansion.

Restraining Factors

Cost and Regulatory Pressures Restraints Market Growth

Despite promising growth prospects, several limiting factors are putting downward pressure on the automotive axles market. A key concern is the high cost of advanced axle technologies. Modern axle systems often include electronic sensors, lightweight alloys, and enhanced structural designs, all of which increase production expenses. For many small manufacturers and budget-conscious buyers, these costs can be a barrier to adoption.

Another issue is supply chain disruption, particularly in sourcing raw materials like steel, aluminum, and specialty metals. Events such as geopolitical conflicts, pandemics, or trade disputes have interrupted global supply lines, leading to delays in manufacturing and price fluctuations.

In addition, the market faces limited penetration in low-income economies. Many of these regions lack the infrastructure or purchasing power needed to adopt technologically advanced vehicles, including modern axle systems. The preference in these markets leans toward affordable, basic vehicle models that often use conventional components.

Strict import regulations and tariffs also limit the smooth flow of automotive components across borders. Countries often impose duties on imported axles to protect domestic industries, but this makes international trade more complex and costly. These combined challenges slow down the market’s potential and demand a strategic response from both manufacturers and regulators.

Growth Opportunities

Technological Advancements Provides Opportunities

The automotive axles market is entering a new era of innovation, with several emerging opportunities creating fresh avenues for growth. One of the most significant is the rapid rise of electric and hybrid commercial vehicles. These vehicles require specialized axle systems designed to support electric drivetrains and battery placement. This shift is driving manufacturers to redesign axle platforms that are lighter, more compact, and better integrated with electronic systems.

The development of modular axle platforms presents another major opportunity. These platforms allow for the easy customization of axle designs across different vehicle types, from small delivery vans to heavy trucks. Modular systems reduce production costs and shorten time-to-market, making them an attractive option for both OEMs and aftermarket suppliers.

Moreover, rural and Tier-II markets are emerging as high-potential regions. With increasing road connectivity and income levels, consumers in these areas are seeking durable, affordable vehicles. Automotive companies that tailor axle designs to these conditions can capture market share in previously underdeveloped areas.

Strategic collaborations with OEMs are also unlocking new possibilities. Through joint ventures and design partnerships, axle manufacturers can gain direct access to vehicle platforms in development, ensuring their components are integrated from the ground up, leading to higher product relevance and profitability.

Emerging Trends

Digital Innovations Are Latest Trending Factor

Several digital and technological trends are actively shaping the future of the automotive axles market. One of the most impactful is the shift toward electrified drivetrains. As electric vehicles (EVs) and hybrid models become more common, traditional axle systems are being replaced or reconfigured to match the needs of electric powertrains. Axles now must accommodate electric motors, regenerative braking, and compact battery layouts, leading to entirely new design approaches.

Predictive maintenance is another major trend transforming the axle market. By using sensors and data analytics, manufacturers can now monitor axle conditions in real-time. This allows for early detection of wear and tear, reducing the risk of failure and improving vehicle safety. Fleet managers also benefit from reduced downtime and lower maintenance costs.

The adoption of 3D printing in axle prototyping is also gaining momentum. This technology enables faster and cheaper production of test models, speeding up the innovation cycle. Manufacturers can experiment with multiple design iterations without investing in expensive tooling.

Finally, advancements in noise, vibration, and harshness (NVH) control are enhancing the driving experience. New axle designs are being engineered to minimize these issues, especially in luxury and commercial vehicles where comfort and stability are top priorities. These innovations reflect a clear trend toward smarter, more responsive axle systems.

Regional Analysis

Asia Pacific Dominates with 51.2% Market Share in the Automotive Axles Market

Asia Pacific leads the Automotive Axles Market with a substantial 51.2% share, contributing USD 30.52 billion. This dominance is attributed to the rapid industrialization, extensive automotive production facilities, and increasing adoption of advanced automotive technologies within the region.

The region’s high market share is driven by a combination of factors including high population density, increasing urbanization, and substantial investments in road and infrastructure development. Additionally, the presence of major automotive manufacturers and suppliers in countries such as China, Japan, and South Korea further strengthens its market position.

The future influence of Asia Pacific on the global Automotive Axles Market is expected to remain strong. With ongoing technological advancements and rising vehicle sales, particularly in electric and hybrid models, the region is poised to maintain its leadership position.

Regional Mentions:

- North America: North America holds a significant market share in the Automotive Axles Market, bolstered by advanced manufacturing techniques and a high rate of vehicle ownership. The region is known for its technological innovations, which drive demand for high-performance and durable automotive axles.

- Europe: Europe is a key player in the Automotive Axles Market, supported by its stringent environmental and vehicle safety regulations. These factors promote the development of lightweight and efficient axle designs, contributing to the region’s competitive edge in the market.

- Middle East & Africa: The Middle East & Africa region is experiencing growth in the Automotive Axles Market, driven by the expansion of automotive manufacturing and assembly plants. Investments in transportation infrastructure and an increase in luxury vehicle sales are key contributors to this trend.

- Latin America: Latin America is seeing an uptick in its Automotive Axles Market share, driven by recovery in automotive production and exports. The region benefits from favorable trade agreements and a growing demand for commercial vehicles, supporting its market growth.

Key Regions and Countries Covered in the Report

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Landscape

The global Automotive Axles Market is shaped by a few dominant players who set benchmarks in innovation, production capacity, and global reach. The top four companies—ZF Friedrichshafen AG, Dana Incorporated, American Axle & Manufacturing Holdings, Inc., and GKN Automotive Limited—hold a major share of the market and drive its competitive landscape.

These companies benefit from strong manufacturing capabilities, advanced technology, and long-standing relationships with major vehicle manufacturers. Their ability to offer both front and rear axle systems, along with integrated electric axle solutions, gives them a competitive edge as the market shifts towards electric mobility.

A key strength lies in their global supply chain networks and R&D investments. For example, ZF Friedrichshafen has made strong moves in developing lightweight and high-efficiency axle systems. Dana Incorporated and American Axle continue to focus on axle designs that improve fuel efficiency and support electric vehicle (EV) platforms. GKN Automotive, with a strong presence in driveline technologies, leverages advanced materials and modular axle designs for flexibility and performance.

Strategic partnerships and acquisitions are common among these players. This allows them to enter new markets, enhance product offerings, and strengthen their positions. The shift towards electrification, especially in passenger and light commercial vehicles, is also pushing these firms to innovate in e-axles and integrated systems.

In conclusion, the Automotive Axles Market is heavily influenced by these top-tier companies. Their technical leadership, market presence, and adaptive strategies will remain critical as the industry moves toward electrification, lightweighting, and improved vehicle dynamics.

Major Companies in the Market

- ZF Friedrichshafen AG

- Dana Incorporated

- American Axle & Manufacturing Holdings, Inc.

- GKN Automotive Limited

- Meritor, Inc.

- Showa Corporation

- Hyundai WIA Corporation

- Gestamp Automoción

- JTEKT Corporation

- Kalyani Group

- Benteler International

- NAF Neunkirchener Achsenfabrik AG

- Weichai Group

Recent Developments

- American Axle & Manufacturing (AAM) Acquires Dowlais Group: On January 2025, AAM announced a £1.2 billion ($1.44 billion) cash-and-stock acquisition of UK-based Dowlais Group. This deal strengthens AAM’s presence in electric vehicle components and is expected to generate $300 million in annual cost savings. The transaction is set to close by the end of 2025, subject to regulatory approvals.

- AAM Divests Indian Commercial Vehicle Axle Business: In October 2024, AAM agreed to sell its Indian commercial vehicle axle business to Bharat Forge Limited for $65 million. The business recorded $156 million in sales over the twelve months ending June 30, 2024. The divestiture aligns with AAM’s strategy to focus on core operations.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 59.6 Billion |

| Forecast Revenue (2034) | USD 83.3 Billion |

| CAGR (2025-2034) | 3.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Axle Type (Front Axle, Rear Axle, Lift Axle), By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs), Off-Highway Vehicles) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | ZF Friedrichshafen AG, Dana Incorporated, American Axle & Manufacturing Holdings, Inc., GKN Automotive Limited, Meritor, Inc., Showa Corporation, Hyundai WIA Corporation, Gestamp Automoción, JTEKT Corporation, Kalyani Group, Benteler International, NAF Neunkirchener Achsenfabrik AG, Weichai Group |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |