Quick Navigation

Report Overview

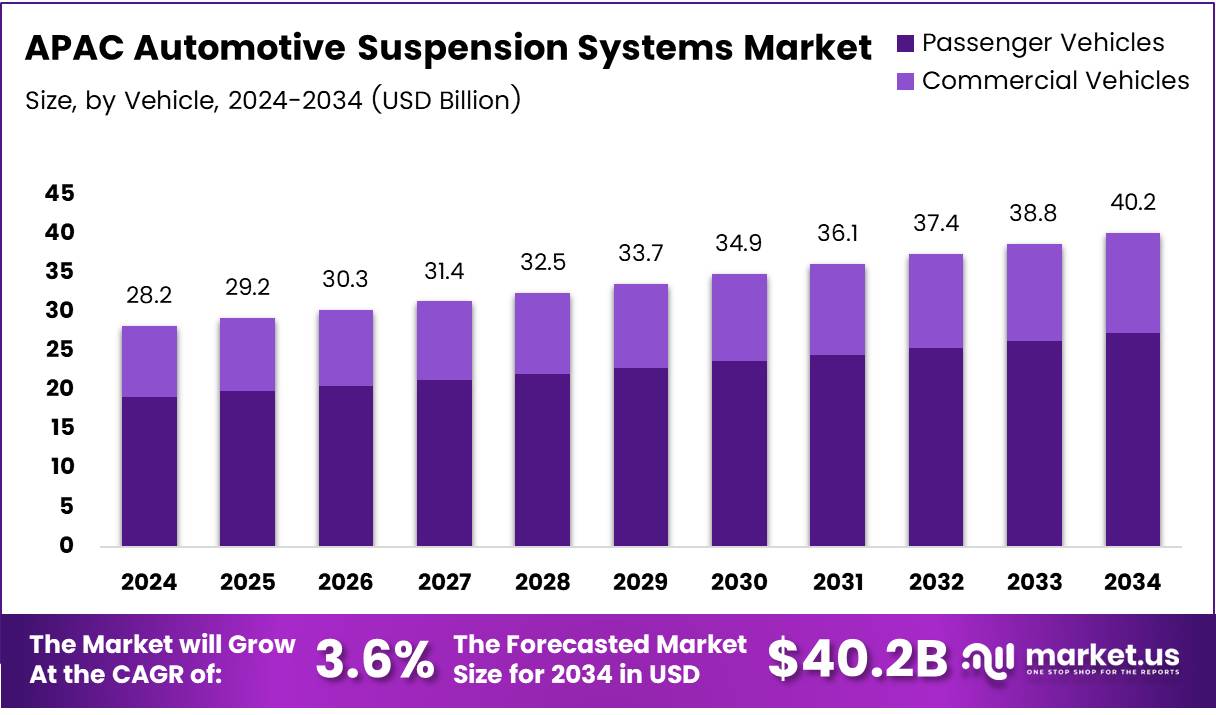

The APAC Automotive Suspension Systems Market size is expected to be worth around USD 40.2 Billion by 2034, from USD 28.2 Billion in 2024, growing at a CAGR of 3.6% during the forecast period from 2025 to 2034.

The APAC Automotive Suspension Systems market is a crucial segment within the region’s automotive industry, focusing on technologies that support vehicle performance and safety. Suspension systems are responsible for improving vehicle handling, comfort, and safety by absorbing road shocks. The market has witnessed significant growth due to increasing vehicle production, rising consumer demand for better driving experiences, and expanding automotive infrastructure across key economies.

In recent years, the automotive industry in APAC has experienced substantial growth, with a notable increase in car production. According to ACEA, global car production reached 76 million units, reflecting a 10.2% increase. This growth directly contributes to the rising demand for advanced suspension systems as automotive manufacturers seek to enhance vehicle stability and passenger comfort.

The Asia-Pacific region, being a key player in global automotive manufacturing, has seen a surge in the adoption of advanced suspension technologies like the CDC (Continuously Controlled Damping) hydraulic suspension.

As of 2023, the assembly volume of CDC hydraulic suspension in APAC approached 1.3 million vehicles, marking a year-on-year growth of 52.7%, as reported by ResearchInChina. This indicates strong market potential, driven by the growing demand for premium and high-performance vehicles equipped with advanced suspension systems.

Moreover, the ongoing shift towards electric vehicles (EVs) and autonomous vehicles (AVs) in the region further drives the development of next-generation suspension technologies to meet the evolving needs of these vehicles.

Government investments and regulations play a significant role in shaping the future of the APAC Automotive Suspension Systems market. Several countries within the region have implemented policies to support the automotive sector’s growth, particularly through subsidies for electric vehicles and innovations in vehicle safety standards. This regulatory push encourages automotive manufacturers to adopt advanced suspension systems that comply with stringent safety and environmental regulations.

Key Takeaways

- APAC Automotive Suspension Systems Market is projected to reach USD 40.2 Billion by 2034, growing from USD 28.2 Billion in 2024, at a CAGR of 3.6%.

- Passenger Vehicles held 85.8% market share in 2024, driven by rising consumer demand for personal mobility solutions.

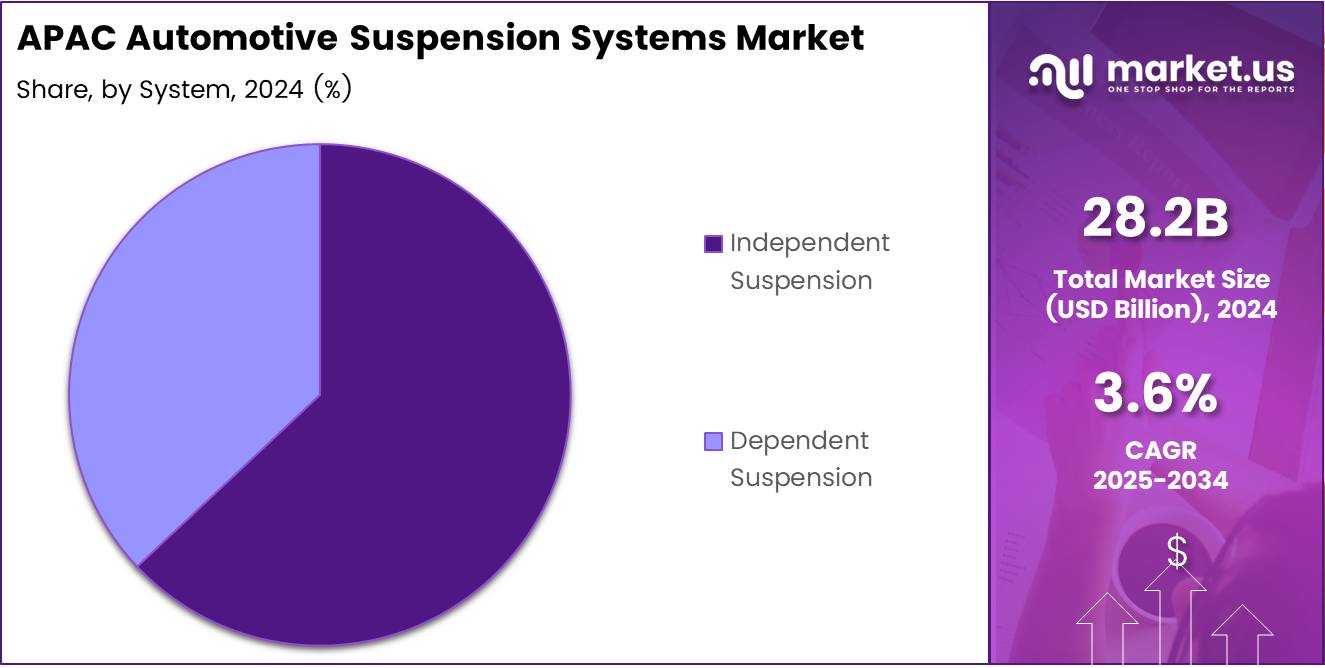

- Independent Suspension Systems dominated the By System Analysis segment in 2024 due to superior stability, ride quality, and handling.

- Hydraulic Damping maintained a leading market share in 2024 for its effective shock absorption and improved vehicle performance.

- Shock Absorbers/Dampeners were the dominant component in 2024, crucial for vehicle stability, comfort, and safety.

Vehicle Analysis

In 2024, Passenger Vehicles held a dominant market position in By Vehicle Analysis segment of APAC Automotive Suspension Systems Market, with a 85.8% share

In 2024, Passenger Vehicles continued to dominate the APAC Automotive Suspension Systems Market with a 85.8% share. The growing consumer demand for personal mobility solutions, particularly in emerging economies, played a significant role in this market position. The robust expansion of urbanization and the increasing preference for private cars are driving the demand for advanced suspension systems in passenger vehicles.

Passenger vehicles utilize suspension systems that are finely tuned for comfort, durability, and safety. The adoption of technologies aimed at improving ride comfort and handling performance is a key factor contributing to this segment’s dominance. The 85.8% market share highlights the substantial preference for passenger vehicles equipped with advanced suspension systems, underscoring the ongoing growth in the sector.

On the other hand, the demand for commercial vehicles is steadily growing but does not yet match the overwhelming share held by passenger vehicles in the market. Despite this, commercial vehicles are expected to experience steady growth, driven by e-commerce expansion and urban logistics needs.

System Analysis

In 2024, Independent Suspension held a dominant market position in By System Analysis segment of APAC Automotive Suspension Systems Market

In 2024, Independent Suspension systems continued to dominate the By System Analysis segment of the APAC Automotive Suspension Systems Market. This technology is favored for its ability to enhance vehicle stability, ride quality, and handling. Independent suspension systems provide better comfort by isolating each wheel’s movement, which improves the vehicle’s ability to absorb road irregularities.

As consumer preference shifts toward improved driving experience and vehicle performance, independent suspension is increasingly being adopted in both passenger and commercial vehicles. The growing emphasis on safety features such as stability control and anti-roll systems has further fueled the adoption of independent suspension. This system is also more adaptable to varying driving conditions, making it highly sought after in markets with diverse road conditions.

Though dependent suspension systems hold a smaller share, they are still preferred in certain vehicle types due to their simplicity and cost-effectiveness, particularly in commercial applications. Nevertheless, independent suspension is expected to continue growing in popularity due to its superior performance attributes.

Damping Analysis

In 2024, Hydraulic Damping held a dominant market position in By Damping Analysis segment of APAC Automotive Suspension Systems Market

In 2024, Hydraulic Damping maintained a dominant market share in the By Damping Analysis segment of the APAC Automotive Suspension Systems Market. Hydraulic damping is widely adopted due to its effective ability to control shock absorption and improve the overall performance of a vehicle’s suspension system. The technology helps in reducing vibrations, enhancing ride comfort, and improving the overall handling of vehicles.

The reliability and efficiency of hydraulic damping systems are key factors behind their widespread adoption, particularly in high-performance passenger vehicles. These systems allow for precise control of the vehicle’s suspension, ensuring a smoother ride even on uneven road surfaces. Additionally, their cost-effectiveness and long lifespan contribute to their preference in both mass-market and premium vehicles.

Although electromagnetic damping and air suspension technologies are gaining traction due to their advanced features, hydraulic damping remains the most commonly used damping solution in the region, particularly in mid-range vehicles. The competition within the damping technologies is expected to intensify in the coming years as automotive manufacturers explore new innovations to meet the evolving needs of consumers.

Component Analysis

In 2024, Shock Absorber/Dampener held a dominant market position in By Component Analysis segment of APAC Automotive Suspension Systems Market

In 2024, Shock Absorbers/Dampeners held a dominant position in the By Component Analysis segment of the APAC Automotive Suspension Systems Market. These components are essential for maintaining vehicle stability and comfort by absorbing and dampening the forces generated from road impacts. Shock absorbers are crucial for ensuring that the vehicle’s suspension system functions smoothly, thus improving ride quality and vehicle safety.

The dominance of shock absorbers in this segment can be attributed to their widespread application across all types of vehicles, from passenger cars to heavy-duty trucks. With constant advancements in materials and technology, shock absorbers have become more durable and efficient, further enhancing their performance in various road conditions. The widespread need for improved driving dynamics and safety features has increased the demand for shock absorbers in the region.

Although other components like ball joints and springs are also important, shock absorbers play a central role in ensuring ride comfort and vehicle stability, which contributes to their dominant market share. As automotive technologies continue to evolve, the demand for high-quality shock absorbers is expected to grow, especially in regions with diverse and challenging driving environments.

Key Market Segments

By Vehicle

- Passenger Vehicles

- Commercial Vehicles

- Heavy Commercial Vehicles

- Light Commercial Vehicles

By System

- Independent Suspension

- Dependent Suspension

By Damping

- Hydraulic Damping

- Electromagnetic Damping

- Air Suspension

- Others

By Component

- Shock Absorber/Dampener

- Ball Joints

- Springs

- Control Arms

- Others

Drivers

Rising Vehicle Production Drives Growth in APAC Automotive Suspension Systems Market

The automotive suspension systems market in the Asia Pacific (APAC) region is seeing significant growth. This growth is mainly driven by the increasing demand for vehicles, particularly in emerging economies like China and India. As vehicle production and sales continue to rise in these countries, the demand for high-quality suspension systems is also increasing.

Suspension systems are critical to vehicle performance, ensuring a smooth ride and good handling. As a result, automakers are under pressure to adopt more advanced suspension technologies that can meet consumer expectations for comfort, performance, and reliability. This demand is especially strong in both economy and luxury vehicle segments.

Consumers are increasingly prioritizing comfort and safety features in vehicles. This shift in consumer preferences is encouraging manufacturers to invest in advanced suspension systems. Technologies like air suspension, which improve ride quality, are becoming more common as automakers aim to deliver enhanced comfort and safety to their customers.

Overall, the combination of rising vehicle production and shifting consumer expectations is a key driver of growth in the APAC automotive suspension systems market.

Restraints

High Manufacturing Costs and Awareness Gaps Restrain APAC Automotive Suspension Systems Market

Despite the market’s growth, several challenges are limiting the widespread adoption of advanced suspension systems in the APAC region. One of the main obstacles is the high cost of manufacturing these systems. Technologies like air suspension and electronic suspension systems require complex processes and expensive materials, which increases production costs.

These high costs can make it difficult for automakers to implement advanced suspension systems in lower-cost vehicles. As a result, the widespread adoption of such systems is slowed, especially in price-sensitive markets.

Another challenge is the lack of awareness about advanced suspension technologies in some parts of the APAC region. In countries where the automotive industry is still developing, consumers and manufacturers may not fully understand the benefits of technologies like air suspension or semi-active systems. This lack of awareness can prevent the adoption of these innovations in budget-friendly vehicles.

Addressing both the cost issues and awareness gaps is crucial for overcoming the constraints on the APAC automotive suspension systems market.

Growth Factors

Growth Opportunities in the APAC Automotive Suspension Systems Market

The APAC automotive suspension systems market is witnessing several growth opportunities. One of the most significant is the rise of electric vehicles (EVs). EVs require specialized suspension systems due to their different weight distribution and unique driving dynamics. As the demand for EVs continues to increase in the region, the need for customized suspension solutions will grow.

In addition, the development of autonomous driving technology presents another opportunity. Autonomous vehicles require advanced suspension systems that can adapt to different road conditions in real time. Smart, adaptive suspension systems are essential to improving the comfort, stability, and safety of self-driving cars, which opens a new avenue for innovation.

Another opportunity lies in the growing demand for aftermarket suspension system replacements. As vehicles age, suspension systems tend to wear out and need to be replaced. The increasing number of older vehicles in the APAC region presents a consistent demand for aftermarket parts, which provides a steady business opportunity for manufacturers and suppliers.

Together, the rise of electric vehicles, the growth of autonomous driving, and the demand for aftermarket replacements offer promising growth prospects for the APAC automotive suspension systems market.

Emerging Trends

Emerging Trends in APAC Automotive Suspension Systems Market

Several key trends are emerging in the APAC automotive suspension systems market. One of the most notable trends is the integration of electric and magnetic suspension technologies. These systems provide better control, stability, and comfort by adjusting to road conditions in real time. As automakers seek to offer superior driving experiences, magnetic suspension is gaining popularity in the region.

Another trend is the increased focus on lightweight materials for suspension components. Automakers are using materials like aluminum and composites to reduce vehicle weight, which helps improve fuel efficiency and overall vehicle performance. This trend is particularly important as global emissions regulations become stricter.

Lastly, the growth of autonomous vehicles is driving demand for advanced suspension systems. Self-driving cars require suspension systems that can adapt to different driving environments, ensuring a smooth and safe ride. These advanced systems are key to improving the overall passenger experience in autonomous vehicles.

Together, these trends reflect the growing innovation and competition in the APAC automotive suspension systems market, as automakers aim to meet the evolving demands of consumers and regulatory standards.

Key Players Analysis

In 2024, the APAC Automotive Suspension Systems market remains highly competitive with several established players dominating the industry.

F-TECH INC. stands out for its innovative approaches in suspension technology, offering lightweight and performance-enhancing solutions to automakers, which positions it well in the region’s growing demand for advanced suspension systems.

NHK SPRING Co., Ltd. is another key player with a strong presence in the APAC region. The company leverages its expertise in manufacturing high-quality coil springs, stabilizer bars, and other suspension components, which are integral to the performance and safety of vehicles, making it a trusted supplier for both traditional and electric vehicle manufacturers.

KYB Corporation has long been a leader in the automotive suspension market, known for its shock absorbers and suspension components that provide superior ride quality. With its focus on expanding production capabilities and enhancing product features, KYB continues to cater to the increasing consumer demand for improved vehicle comfort and handling in APAC markets.

Tenneco Inc., recognized for its global footprint and diversified product offerings, provides a wide range of suspension systems, including air suspension solutions. Their robust presence in the APAC market is driven by ongoing investment in R&D and a commitment to sustainability, ensuring they meet the evolving demands of the automotive industry.

Top Key Players in the Market

- F-TECH INC.

- NHK SPRING Co., Ltd.

- KYB Corporation

- Tenneco Inc.

- thyssenkrupp AG

- Rassini

- ZF Friedrichshafen AG

- Multimatic Inc.

- Marelli Holdings Co., Ltd.

- Sogefi SpA

- HL Mando Corp.

- ContiTech Deutschland GmbH

Recent Developments

- In January 2025, Gabriel India acquired the Motherson assets of Marelli for Rs 60 crore, strengthening its portfolio in the auto components sector and enhancing its manufacturing capabilities.

- In November 2024, MidOcean Partners acquired Arnott Industries, a leading platform for suspension products in the automotive aftermarket, marking a strategic move to expand its global footprint in the auto industry.

- In July 2024, TVS Mobility’s SI Air Springs successfully acquired Italy’s Roberto Nuti Group, a key player in air suspension systems, further bolstering its presence in the European automotive market.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 28.2 Billion |

| Forecast Revenue (2034) | USD 40.2 Billion |

| CAGR (2025-2034) | 3.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Vehicle (Passenger Vehicles, Commercial Vehicles, Heavy Commercial Vehicles, Light Commercial Vehicles), By System (Independent Suspension, Dependent Suspension), By Damping (Hydraulic Damping, Electromagnetic Damping, Air Suspension, Others), By Component (Shock Absorber/Dampener, Ball Joints, Springs, Control Arms, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | F-TECH INC., NHK SPRING Co., Ltd., KYB Corporation, Tenneco Inc., thyssenkrupp AG, Rassini, ZF Friedrichshafen AG, Multimatic Inc., Marelli Holdings Co., Ltd., Sogefi SpA, HL Mando Corp., ContiTech Deutschland GmbH |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |