Quick Navigation

Report Overview

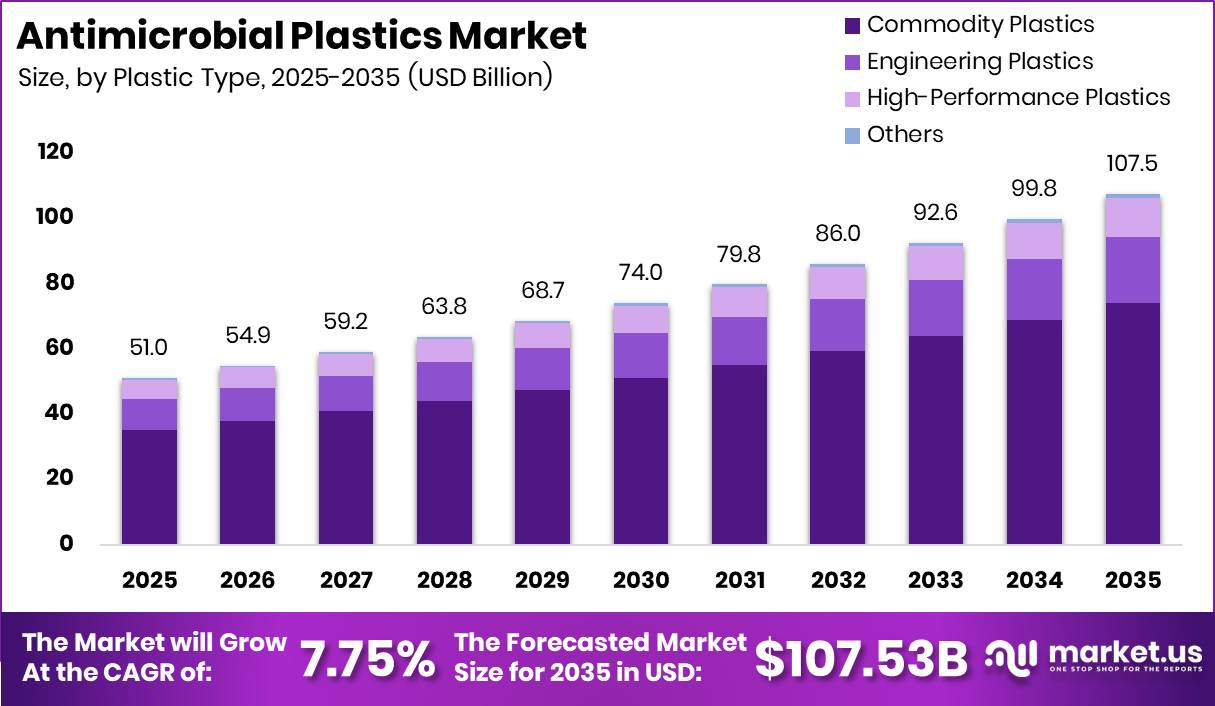

Global Antimicrobial Plastics Market size is expected to be worth around USD 107.53 Billion by 2035 from USD 51.00 Billion in 2025, growing at a CAGR of 7.75% during the forecast period 2026 to 2035.

Antimicrobial plastics are polymer products engineered with additives such as silver, copper, or zinc that resist bacterial growth on contact. Manufacturers integrate these additives into resins like ABS, PP, TPU, and PE during compounding. This structure allows the same base resin to serve healthcare, packaging, and consumer applications with built-in hygiene performance. Therefore, the market spans raw material suppliers, compounders, and converters.

Government health bodies continue to push infection control standards that shape procurement across hospitals and public facilities. As reported by ECDC, more than 3.5 Million healthcare-associated infections occur annually across EU and EEA countries. This burden keeps infection prevention budgets tied to measurable hospital costs. Hospitals therefore favor suppliers who can document antimicrobial performance at the resin level.

Data from ECDC shows healthcare-associated infections account for an estimated 2.5 Million disability-adjusted life years annually in Europe. This means regulators view antimicrobial materials as a public health tool, not a marketing feature. Consequently, suppliers who pair validated claims with regulatory documentation gain preferred status in multiyear hospital purchasing frameworks.

In September 2025, Reolite secured EPA registration for a dual-ion silver and zinc antimicrobial powder technology. This approval enables commercialization across thousands of product categories, including antimicrobial plastics. As a result, additive suppliers with regulatory clearance can move faster into medical and consumer markets than unregistered competitors.

Key Takeaways

- The global antimicrobial plastics market is valued at USD 51.00 Billion in 2025 and is projected to reach USD 107.53 Billion by 2035.

- The market is set to expand at a CAGR of 7.75% between 2026 and 2035.

- Commodity Plastics dominate the By Plastic Type segment with a 69.0% share.

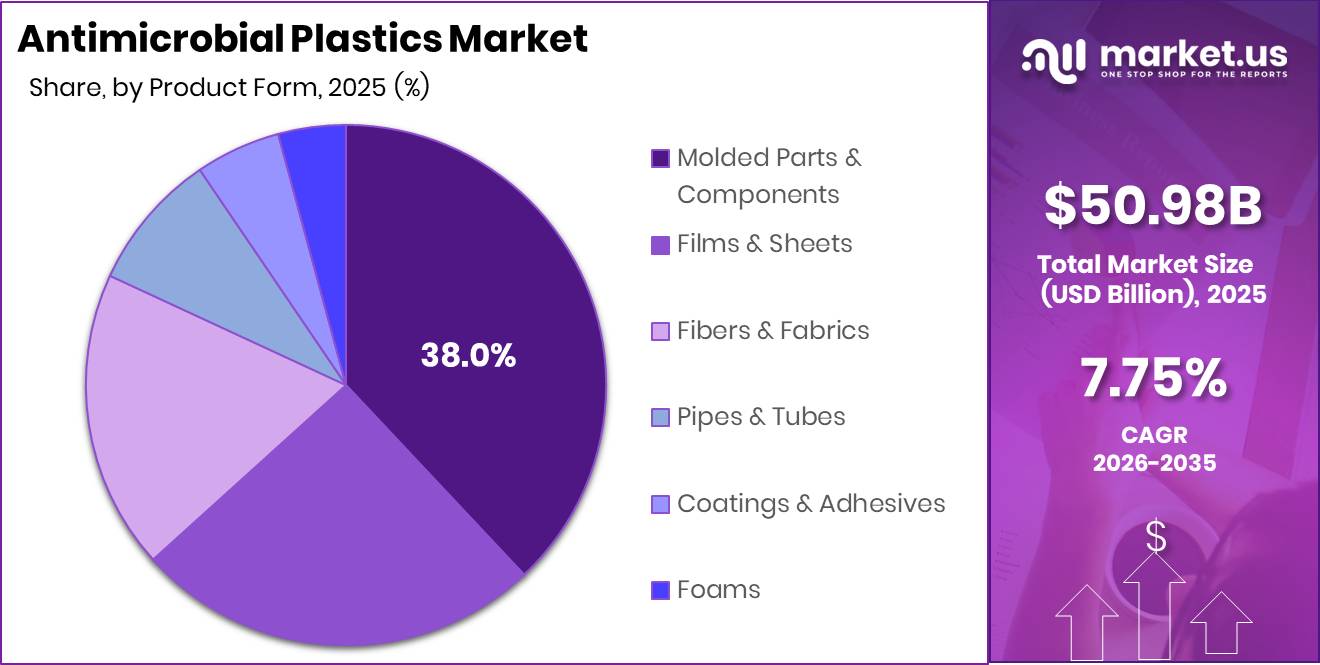

- Molded Parts and Components lead the By Product Form segment with a 38.0% share.

- Healthcare and Medical applications hold the largest By Application share at 32.0%.

- Direct Sales and B2B channels account for 55.0% of the By Distribution Channel segment.

- OEMs and Product Manufacturers represent 52.0% of the By End User Type segment.

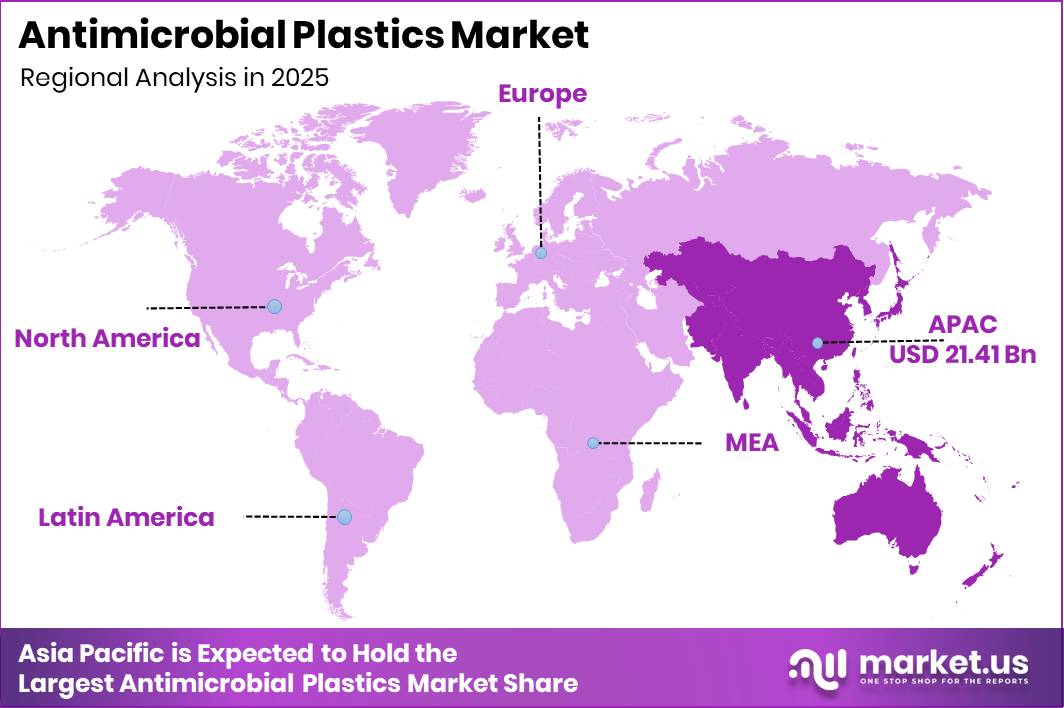

- Asia Pacific dominates the regional market with a 42.0% share, valued at USD 21.41 Billion.

Plastic Type Analysis

Commodity Plastics dominates with 69.0% due to low cost and wide processing availability.

In 2025, Commodity Plastics held a dominant market position in the By Plastic Type segment of Antimicrobial Plastics Market, with a 69.0% share. These resins, including PP, PE, and ABS, allow compounders to add antimicrobial masterbatch without major retooling. This means buyers can scale hygiene features across packaging and consumer goods at low incremental cost. Lower entry barriers also attract new compounders into this segment.

Engineering Plastics, High-Performance Plastics, and Others hold the remaining share of the segment collectively. These categories serve specialized applications where higher heat resistance or chemical stability outweighs cost sensitivity. However, their narrower processing base limits volume growth compared with commodity grades. This signals a long-term opportunity for premium additive suppliers willing to serve smaller, higher-margin orders.

Product Form Analysis

Molded Parts & Components dominates with 38.0% due to direct use in device housings.

In 2025, Molded Parts & Components held a dominant market position in the By Product Form segment of Antimicrobial Plastics Market, with a 38.0% share. Hospitals and OEMs specify antimicrobial resin directly into bed rails, housings, and cart handles. This structural integration lets suppliers sell validated compounds rather than commodity parts. As a result, margins on molded components outperform unfinished material formats.

Films & Sheets, Fibers & Fabrics, Pipes & Tubes, Coatings & Adhesives, and Foams hold the remaining share collectively across the segment. These formats serve packaging, textile, and construction channels where hygiene claims support secondary product benefits. Therefore, growth in these formats tends to follow end-use industry expansion rather than direct antimicrobial demand. This creates steady, if slower, adoption across distributed applications.

Application Analysis

Healthcare & Medical dominates with 32.0% due to infection control procurement priorities.

In 2025, Healthcare & Medical held a dominant market position in the By Application segment of Antimicrobial Plastics Market, with a 32.0% share. As reported by EPA testing on antimicrobial copper surfaces, treated materials continuously kill more than 99.9% of bacteria within 2 hours of contact. This performance level supports hospital procurement standards. Consequently, medical device makers prioritize validated antimicrobial resin over standard alternatives for high-touch components.

Data from the 2025 MAP-1 study shows 43.7% of culturable bacteria recovered from bedsheets were multidrug-resistant organisms. This finding highlights the operational importance of antimicrobial polymer technologies in infection-control environments. Healthcare facilities therefore treat antimicrobial textiles and surfaces as a measurable infection prevention tool rather than a comfort feature.

Packaging, Building & Construction, Automotive, Textile & Apparel, and Others hold the remaining share collectively within this segment. These industries adopt antimicrobial plastics to extend shelf life, reduce odor, or support hygiene marketing claims. This means demand growth in these categories tracks consumer hygiene awareness more closely than regulatory mandates.

Distribution Channel Analysis

Direct Sales / B2B dominates with 55.0% due to technical specification requirements.

In 2025, Direct Sales / B2B held a dominant market position in the By Distribution Channel segment of Antimicrobial Plastics Market, with a 55.0% share. Compounders and OEMs require technical consultation on additive loading, migration testing, and claim documentation before purchase. This complexity favors direct supplier relationships over intermediated sales. Therefore, suppliers that invest in technical sales teams retain larger accounts longer.

Distributors & Specialty Chemical Dealers, Online / E-commerce, and Licensing Model channels hold the remaining share collectively. These channels serve smaller compounders and regional buyers who need smaller order volumes. This signals an opening for distributors who can bundle technical support with smaller batch sizes.

End User Type Analysis

OEMs / Product Manufacturers dominates with 52.0% due to direct resin specification into finished products.

In 2025, OEMs / Product Manufacturers held a dominant market position in the By End User Type segment of Antimicrobial Plastics Market, with a 52.0% share. Medical device OEMs, consumer goods manufacturers, and automotive OEMs specify antimicrobial resin grades during product design rather than after launch. This early integration locks suppliers into multiyear component contracts. As a result, OEM relationships generate the most predictable recurring resin demand.

Plastic Compounders & Converters, Packaging Companies, Construction & Infrastructure Companies, and Government & Institutional Buyers hold the remainingshare collectively across this segment. These buyers purchase antimicrobial resin to fulfill specifications set by upstream OEMs or public procurement standards. This reflects a layered supply chain where compounding capacity ultimately depends on OEM design decisions.

Key Market Segments

By Plastic Type

- Commodity Plastics

- Engineering Plastics

- High-Performance Plastics

- Others

By Product Form

- Films & Sheets

- Fibers & Fabrics

- Molded Parts & Components

- Pipes & Tubes

- Coatings & Adhesives

- Foams

By Application / End-Use Industry

- Healthcare & Medical

- Packaging

- Building & Construction

- Automotive

- Textile & Apparel

- Others

By Distribution Channel

- Direct Sales / B2B

- Distributors & Specialty Chemical Dealers

- Online / E-commerce

- Licensing Model

By End User Type

- OEMs / Product Manufacturers

- Medical device OEMs

- Consumer goods manufacturers

- Automotive OEMs

- Plastic Compounders & Converters

- Packaging Companies

- Construction & Infrastructure Companies

- Government & Institutional Buyers

Regional Analysis

Asia Pacific Dominates the Antimicrobial Plastics Market with a Market Share of 42.0%, Valued at USD 21.41 Billion

Asia Pacific leads the antimicrobial plastics market through dense compounding infrastructure and proximity to export manufacturing corridors. China, Japan, South Korea, and India host large-scale extrusion and molding capacity that supplies global OEMs. This concentration allows regional converters to absorb additive cost volatility more efficiently than smaller importers. Government procurement in healthcare facilities further supports steady regional demand growth.

North America maintains strong demand through hospital infection control standards and medical device manufacturing. The CDC continues to track national healthcare-associated infection performance, which keeps board-level attention on infection prevention spending. This regulatory visibility supports premium pricing for validated antimicrobial components. Medical device OEMs in the region favor documented compounds over standard untreated resins.

Europe operates under treated-article provisions within the Biocidal Products Regulation that govern hygiene and biocidal performance claims. Suppliers must substantiate claims and meet labeling obligations before market entry. This regulatory structure slows commercialization timelines but reinforces buyer trust in verified antimicrobial performance. Converters that invest early in compliance documentation gain a durable advantage.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Drivers

Healthcare remains the clearest value pool for antimicrobial plastics because infection prevention budgets connect to measurable hospital costs rather than discretionary spending. A 2022 to 2023 European survey estimated healthcare-associated infection prevalence at 8.0%, while the CDC tracks ongoing US performance data. The WHO states strong hygiene programs can cut healthcare-associated infections by up to 70%.

This shifts supplier business models from selling standard ABS, PP, TPU, or PE parts on lowest cost toward selling validated compounds with claim support and migration documentation. Bed rails, monitor housings, cart handles, and catheter-tray components now carry resin-level protection specified into multiyear purchasing frameworks. Selling prices rise by a mid-single-digit to low-double-digit percentage versus untreated resin parts.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hospital infection-control plastics in devices, carts, bed components, and high-touch housings | +1.6% | North America core, EU, Japan, South Korea, GCC tertiary care hubs | Short term |

| Food-contact compliance and shelf-life protection in packaging formats | +1.3% | US, EU, China, India, ASEAN export packaging corridors | Short term |

| EU PPWR-led redesign of recyclable and compliant antimicrobial packaging | +0.9% | EU core, UK alignment spill-over, Turkey/North Africa export suppliers | Medium term |

| Shift toward inorganic silver, zinc, and copper additive systems with longer service life | +1.1% | North America, EU, China, India manufacturing clusters | Medium term |

| Premium appliance, HVAC, and consumer durable differentiation through built-in hygiene claims | +0.8% | China, India, Southeast Asia, North America replacement markets | Short term |

| Antimicrobial public-touch surfaces in transit, education, and commercial buildings | +0.7% | EU urban systems, US institutional retrofits, Middle East smart-city projects | Long term |

Restraints

In Europe, antimicrobial plastics sold with hygiene or biocidal performance claims face constraints under treated-article provisions within the Biocidal Products Regulation. Suppliers must substantiate claims, meet labeling obligations, and respond to consumer treatment-information requests within 45 days at no charge. Formulation dossiers and multilingual labeling changes add measurable launch friction.

This regulatory burden adds an estimated 4% to 7% to EU launch costs and extends commercialization timelines by 6 to 12 months for smaller brand owners. Asian exporters face repeated active-substance re-documentation market by market. The resulting channel hesitation weakens pricing power and lowers effective CAGR capture in EU-heavy portfolios.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Silver/copper additive inflation | -1.4% | Global; EU, North America, APAC manufacturing hubs | Short term (≤ 2 years) |

| EU treated-article compliance burden | -1.1% | EU core; exporters into EU | Medium term (2-4 years) |

| Food-contact migration testing costs | -1.0% | EU, North America, Japan, Korea | Short term (≤ 2 years) |

| Recycled-content incompatibility | -0.9% | EU, North America, advanced APAC | Medium term (2-4 years) |

| Medical claim validation delays | -0.8% | North America core, EU, Japan | Medium term (2-4 years) |

| Converter margin compression | -0.7% | Global; SME-heavy APAC, LatAm, CEE | Short term (≤ 2 years) |

Challenges

Permitted antimicrobial claims vary by jurisdiction rather than being broadly prohibited. In the US, treated-article pathways protect only the article itself and cannot extend into public-health language without triggering separate regulatory review. In the EU, treated articles must rely on permitted biocidal products under separate authorization logic.

This mismatch creates a commercialization drag of 3 to 9 months per SKU for globally marketed products. Legal review and relabeling costs rise by an estimated 0.5% to 1.5% of launch budgets. Suppliers increasingly need regulatory translation teams and region-specific claim libraries to preserve rollout velocity.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Silver-Copper Cost Volatility | -1.2% | North America imports, EU converters, APAC compounding hubs | Medium term (2-4 years) |

| Claim-Compliance Translation Burden | -0.9% | EU regulatory hubs, U.S. treated-article markets, global exporters | Medium term (2-4 years) |

| Validation Cycle Elongation | -0.8% | Medical plastics clusters, food-contact packaging markets, OEM qualification chains | Medium term (2-4 years) |

| Additive Dispersion Yield Loss | -0.7% | APAC extrusion corridors, EU specialty molding, North America compounders | Short term (≤ 2 years) |

| Specialist Talent Bottleneck | -0.6% | North America core, Western Europe, advanced Asian manufacturing bases | Long term (≥ 4 years) |

| Feedstock-Freight Shock Exposure | -1.0% | APAC export corridors, EU import-dependent buyers, transpacific supply lanes | Medium term (2-4 years) |

Opportunities

Premium food-chain hygiene packaging offers a clear future opportunity by targeting high-risk cold-chain, ready-to-eat, protein, dairy, and foodservice applications with measurable spoilage-reduction benefits. Regulatory frameworks increasingly emphasize use-condition suitability, creating scope for antimicrobial solutions in reusable bins, liners, meat trays, and dairy closures.

This opportunity strengthens as 68% of the world’s population is projected to live in urban areas by 2050, with nearly 90% of urban growth concentrated in Asia and Africa. Converters capturing 1.5% to 2.0% of premium food packaging segments while supporting 5% to 10% spoilage reductions can command 12% to 20% pricing premiums and expand margins by 200 to 400 basis points.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Reprocessed med-device polymers | +1.6% | EU, North America core | Medium term (2-4 years) |

| Premium food-chain hygiene packaging | +1.3% | North America, EU, GCC, APAC urban | Short term (≤ 2 years) |

| PCR + antimicrobial compliant packaging | +1.9% | EU, US, Japan, South Korea | Medium term (2-4 years) |

| WASH-linked institutional plastics | +1.4% | APAC emerging, Africa, LATAM | Medium term (2-4 years) |

| Treated-article private label model | +1.1% | US, EU, ASEAN | Short term (≤ 2 years) |

| M&A roll-up in additive compounding | +2.2% | North America, EU, China, India | Long term (≥ 4 years) |

Key Company Insights

In September 2025, Reolite became the first company to obtain US EPA registration for a dual-ion silver and zinc antimicrobial powder technology. This clearance enabled commercialization across thousands of product categories. The same month, Reolite entered a collaboration with a global electronics manufacturer to co-develop next-generation antimicrobial applications, positioning the company ahead of unregistered additive rivals in regulated channels.

Cupron Performance Additives signed an exclusive distribution agreement with Palmer Holland in September 2025 to expand North American commercialization of its copper-based antimicrobial technologies. As reported by EPA testing, antimicrobial copper alloys demonstrated greater than 99.9% effectiveness against MRSA within 2 hours, giving Cupron a validated performance claim across plastics, films, foams, and polymer systems.

Key Players

- Reolite

- Cupron Performance Additives

- Zonova

- MetalloBio

- BASF SE

- Parx Materials N.V

- Ray Products Company Inc.

- Covestro AG

- King Plastic Corporation

- Palram Industries Ltd.

- Clariant AG

- Sanitized AG

- Dow Inc.

- Lonza

- Other Key Players

Recent Developments

- May 2026 – Zonova completed a £2.1 Million seed funding round led by THENA Capital to accelerate commercialization of its proprietary Z-ROS antimicrobial technology engineered for medical-device polymers.

- May 2026 – MetalloBio closed a £401,000 pre-Series A funding round to advance commercialization of a new class of antimicrobial compounds targeting antimicrobial resistance.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 51.00 Billion |

| Forecast Revenue (2035) | USD 107.53 Billion |

| CAGR (2026-2035) | 7.75% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Plastic Type (Commodity Plastics, Engineering Plastics, High-Performance Plastics, Others), By Product Form (Films & Sheets, Fibers & Fabrics, Molded Parts & Components, Pipes & Tubes, Coatings & Adhesives, Foams), By Application (Healthcare & Medical, Packaging, Building & Construction, Automotive, Textile & Apparel, Others), By Distribution Channel (Direct Sales/B2B, Distributors & Specialty Chemical Dealers, Online/E-commerce, Licensing Model), By End User Type (OEMs/Product Manufacturers, Plastic Compounders & Converters, Packaging Companies, Construction & Infrastructure Companies, Government & Institutional Buyers) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Reolite, Cupron Performance Additives, Zonova, MetalloBio |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

The Global Antimicrobial Plastics Market is expected to be worth around USD 94.1 Billion by 2033. The projected CAGR of the Antimicrobial Plastics Market from 2024 to 2033 is 7.80%.

Antimicrobial plastics are widely utilized across healthcare, packaging, consumer goods, and construction sectors.

Commodity plastics, including polyethylene (PE), polypropylene (PP), polyvinyl chloride (PVC), among others, dominate the Antimicrobial Plastics Market.

The Asia Pacific (APAC) region dominates the Antimicrobial Plastics Market, holding 37.5% of the market share.