Quick Navigation

Report Overview

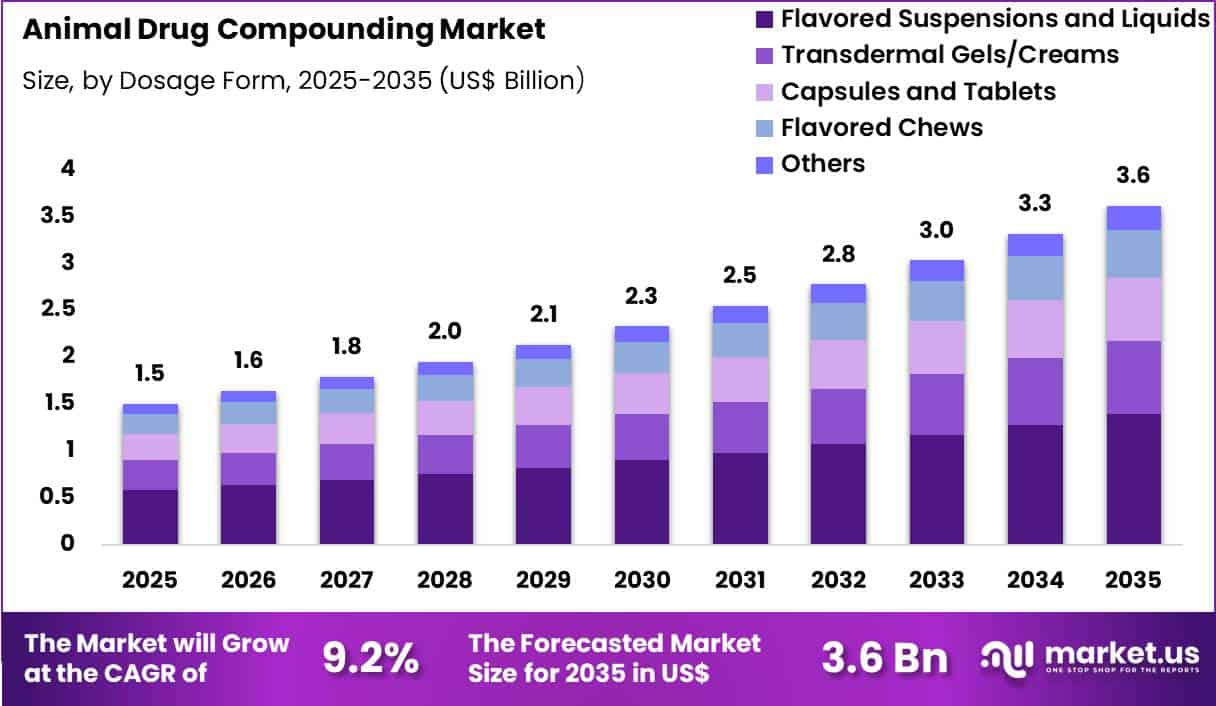

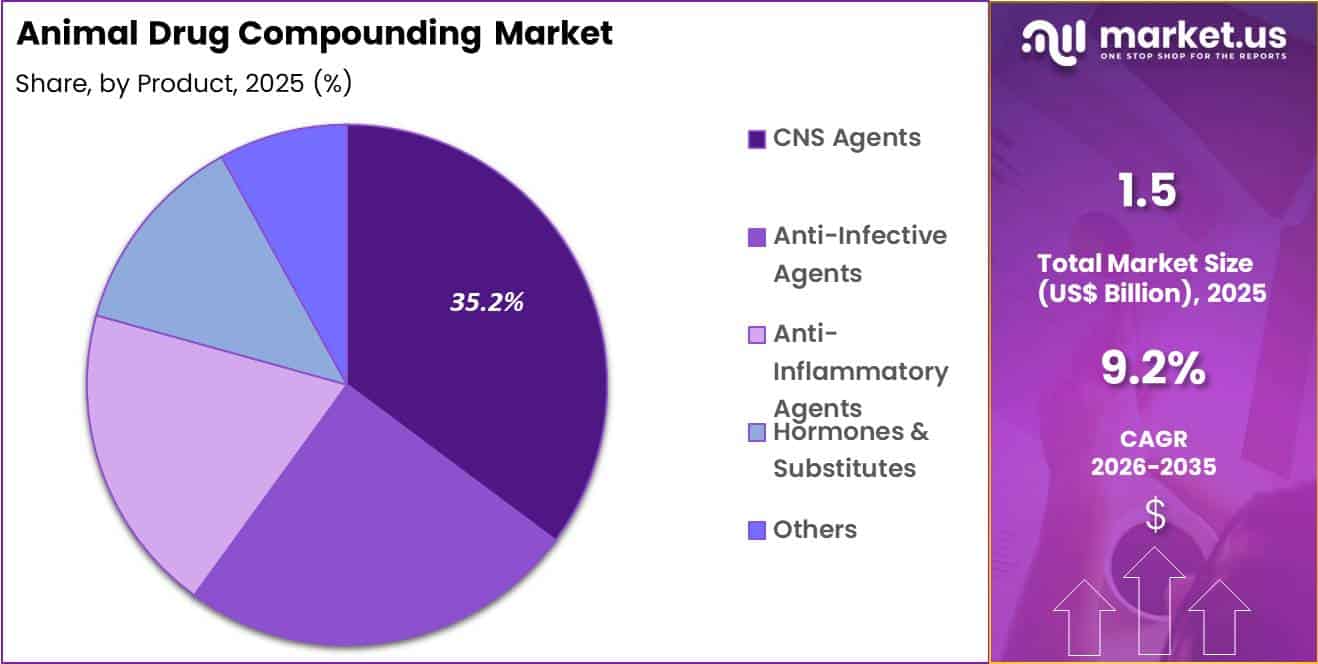

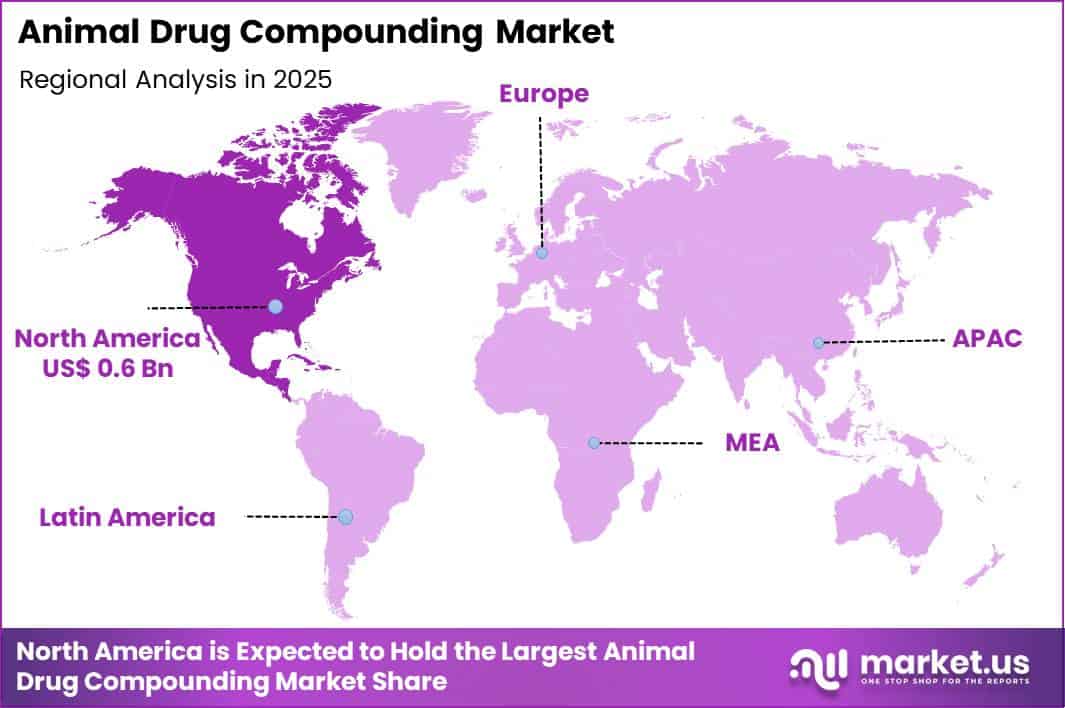

The Global Animal Drug Compounding Market size is expected to be worth around US$ 3.6 Billion by 2035 from US$ 1.5 Billion in 2025, growing at a CAGR of 9.2% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 38.1% share with a revenue of US$ 0.6 Billion.

Increasing pet ownership and the growing recognition of individualized veterinary care drive the Animal Drug Compounding market as veterinarians and pet owners demand customized medications that address unique species, breed, and patient needs.

Veterinarians increasingly compound transdermal gels to deliver pain relief and anti-inflammatory agents for cats and dogs with arthritis, allowing absorption through the skin while avoiding oral administration challenges in finicky or nauseated animals.

These compounded formulations support flavored chewables tailored to exotic species such as birds and reptiles, ensuring accurate dosing of antibiotics or antiparasitics in animals that resist standard tablets. Equine practitioners compound large-volume injectables and oral pastes for musculoskeletal disorders, adjusting concentrations to suit adult horses or ponies with specific weight and metabolism profiles.

In avian and small mammal practice, compounded suspensions and topical solutions treat chronic conditions like respiratory infections or dermatologic issues, providing palatable or easy-to-administer alternatives to commercial products. Compounding pharmacies also prepare hormone replacement therapies for reproductive disorders in breeding animals, enabling precise control of estrus cycles or thyroid function.

Compounding pharmacies and veterinary pharmaceutical partners pursue opportunities to develop advanced delivery forms such as flavored oral liquids and transdermal creams, expanding applications in geriatric pet care where swallowing difficulties and polypharmacy require simplified regimens. These innovations facilitate combination therapies that merge multiple active ingredients into single preparations, improving compliance in animals with multiple chronic conditions.

Opportunities emerge in personalized dosing based on pharmacokinetic data, particularly for exotic species where standard formulations prove inadequate. Recent industry analysis highlighted that the rising penetration of pet insurance has made specialized compounded medications more accessible to a broader range of pet owners.

According to the findings, over 70% of US households now own at least one pet, creating a consistent demand for transdermal gels and flavored chewables that simplify the administration of chronic medications. Companies invest in sterile compounding facilities and quality assurance processes to meet growing regulatory expectations.

Recent trends emphasize collaboration between veterinarians and compounding specialists to create evidence-based formulations, positioning the market for sustained expansion in companion animal and exotic species healthcare.

Key Takeaways

- In 2025, the market generated a revenue of US$ 1.5 Billion, with a CAGR of 9.2%, and is expected to reach US$ 3.6 Billion by the year 2035.

- The dosage form segment is divided into flavored suspensions and liquids, transdermal gels/creams, capsules and tablets, flavored chews and others, with flavored suspensions and liquids taking the lead with a market share of 38.6%.

- Considering product, the market is divided into CNS agents, anti-infective agents, anti-inflammatory agents, hormones & substitutes and others. Among these, cns agents held a significant share of 35.2%.

- Furthermore, concerning the route of administration segment, the market is segregated into oral, injectable, topical and other routes. The oral sector stands out as the dominant player, holding the largest revenue share of 66.9% in the market.

- The animal segment is segregated into companion animals and livestock animals, with the companion animals segment leading the market, holding a revenue share of 73.5%.

- North America led the market by securing a market share of 38.1%.

Dosage Form Analysis

Flavored suspensions and liquids accounted for 38.6% of growth within dosage form and dominate the animal drug compounding market because veterinarians frequently require customized liquid formulations to improve medication acceptance among animals. Many companion animals resist conventional tablets or capsules, which encourages veterinarians and pharmacists to prepare flavored liquids that simplify administration for pet owners.

Veterinary practice guidelines also emphasize the importance of palatable formulations to ensure proper dosing and treatment adherence in animals. The American Veterinary Medical Association reports that more than 60% of U.S. households own at least one pet, which highlights the expanding population requiring veterinary care.

This large companion animal base is expected to strengthen demand for compounded liquid medications tailored to specific species and dosing requirements. The segment is likely to grow further as pharmacists develop improved flavoring systems that support easier oral administration and better compliance during treatment.

Product Analysis

CNS agents accounted for 35.2% of growth within product and dominate the animal drug compounding market due to the increasing diagnosis and management of neurological and behavioral conditions in companion animals. Veterinarians increasingly prescribe medications for anxiety, seizures, cognitive dysfunction, and behavioral disorders in pets.

The American Veterinary Medical Association highlights that veterinary neurologic and behavioral treatments continue to expand as pets live longer and owners invest more in long-term healthcare. Compounding pharmacies prepare customized CNS medications that match species-specific dosages and alternative dosage forms when commercial options remain unavailable.

This segment is expected to strengthen as awareness of pet mental health and neurological conditions increases among veterinarians and pet owners. Growing adoption of personalized veterinary treatment plans further supports the demand for compounded CNS formulations.

Route of Administration Analysis

Oral administration accounted for 66.9% of growth within route of administration and dominate the animal drug compounding market because oral delivery remains the most convenient and widely accepted treatment approach for most veterinary medications. Veterinarians and pet owners prefer oral drugs due to their ease of administration and lower risk compared with injectable therapies.

Compounded oral formulations allow pharmacists to adjust dosage strengths and flavors based on the animal’s weight, species, and treatment condition. Veterinary treatment protocols frequently rely on oral dosing for chronic conditions such as infections, inflammation, and neurological disorders.

This segment is expected to expand as pharmaceutical compounding supports personalized dosing for animals that require long-term therapy. Increasing availability of flavored liquids and chewable formulations further strengthens oral medication acceptance among pets.

Animal Type Analysis

Companion animals accounted for 73.5% of growth within animal type and dominate the animal drug compounding market due to the growing global pet population and rising spending on veterinary healthcare. Pet owners increasingly treat animals as family members and invest in advanced medical care, preventive treatments, and specialized medications.

According to the American Pet Products Association, U.S. pet industry spending exceeded $136 billion in recent years, which reflects strong demand for veterinary services and medications. Companion animals often require individualized drug formulations because species differences make many human or standard veterinary medications unsuitable without adjustment.

Veterinary compounding allows pharmacists to tailor drug strengths, dosage forms, and flavors for dogs, cats, and other pets. This segment is projected to maintain strong growth as pet ownership and veterinary healthcare awareness continue to increase worldwide.

Key Market Segments

By Dosage Form

- Flavored Suspensions and Liquids

- Transdermal Gels/Creams

- Capsules and Tablets

- Flavored Chews

- Others

By Product

- CNS Agents

- Anti-infective Agents

- Anti-inflammatory Agents

- Hormones & Substitutes

- Others

By Route of Administration

- Oral

- Injectable

- Topical

- Other Routes

By Animal

- Companion Animals

- Livestock Animals

Drivers

Increasing demand for customized equine and companion animal medications is driving the market.

Zoetis Inc. reported U.S. equine revenue of $172 million in 2024, reflecting an 8.9% increase from $158 million in 2023. This growth demonstrates sustained need for tailored pharmaceutical solutions in performance and companion equine care. Veterinary compounding pharmacies address specific dosing requirements unavailable in commercially manufactured products.

The demand encompasses flavored suspensions, transdermal gels, and concentration adjustments for individual animal physiology. Practitioners utilize compounded formulations to manage chronic conditions in aging companion animals. The expansion aligns with rising pet ownership and equine sports participation requiring precise therapeutic options.

Owners prioritize treatments that improve compliance through palatable or convenient delivery forms. The driver supports dedicated compounding facilities focused on veterinary-exclusive preparations. Regulatory flexibility for animal-specific compounding sustains this momentum. Overall, the trend reinforces the essential role of customized medications in modern veterinary practice.

Restraints

Regulatory scrutiny on bulk drug substances is restraining the market.

The U.S. Food and Drug Administration maintains a bulks list under section 503A for human compounding, with limited veterinary-specific guidance leading to inconsistent state interpretations. Veterinary compounders face challenges when sourcing active pharmaceutical ingredients not approved for animal use. Enforcement actions against facilities utilizing unapproved bulk drugs create operational uncertainty.

The restraint arises from heightened inspections targeting non-compliant compounding practices. Pharmacies must navigate varying state pharmacy board requirements for veterinary prescriptions. The factor limits scalability for national compounding networks serving multiple jurisdictions.

Manufacturers of FDA-approved animal drugs report competitive pressure from compounded alternatives. The scrutiny influences inventory decisions for high-risk bulk substances. Providers encounter delays in fulfilling prescriptions due to sourcing restrictions. This element moderates market growth amid evolving federal oversight.

Opportunities

Expansion of sterile compounding capabilities for injectable veterinary preparations is creating growth opportunities.

Specialized compounding pharmacies are investing in ISO Class 5 cleanrooms to produce sterile injectables for equine joint therapy and companion animal critical care. These facilities enable production of customized concentrations and combinations unavailable in commercial vials. Opportunities emerge for partnerships with veterinary specialty hospitals requiring immediate-use preparations.

The development supports longer beyond-use dating through validated stability studies. Pharmacists gain capacity to compound multi-drug admixtures for complex cases. The infrastructure allows expansion into ophthalmic and intrathecal formulations for veterinary neurology.

Such advancements facilitate compliance with USP <797> standards adapted for animal applications. The opportunity fosters differentiation through documented sterility assurance levels. Stakeholders anticipate increased demand from ambulatory equine practices. This framework promotes sustainable growth in high-value sterile compounding segments.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions influence the animal drug compounding market through veterinary clinic spending, livestock health investment, and pet owner affordability for customized treatments. Inflation raises costs for active pharmaceutical ingredients, compounding equipment, sterile packaging, and regulatory compliance, which increases operating expenses for compounding pharmacies.

Higher interest rates limit expansion capital for specialized veterinary pharmacies and slow facility upgrades. Geopolitical tensions disrupt global supply chains for pharmaceutical ingredients and excipients, creating sourcing variability and delivery uncertainty.

Current US tariffs on imported APIs, chemical intermediates, and compounding equipment increase procurement costs and tighten profit margins for providers. These pressures can affect pricing flexibility and limit service expansion among smaller compounding pharmacies.

At the same time, pharmacies strengthen domestic ingredient sourcing and invest in localized production capabilities to maintain supply stability. Rising demand for personalized veterinary treatments and species-specific formulations continues to support steady and confident market growth.

Latest Trends

Introduction of FDA guidance on veterinary compounding from human-approved drugs is driving the market.

The U.S. Food and Drug Administration issued updated draft guidance in late 2024 addressing the use of human-approved drugs in veterinary compounding under enforcement discretion policies. This document clarifies conditions under which compounders may prepare medications from FDA-approved human products for animal patients.

The guidance emphasizes patient-specific prescriptions and limits on office stock distribution. Practitioners benefit from expanded access to stable, high-quality active ingredients. The 2024-2025 development reduces ambiguity surrounding extralabel use in compounding. Pharmacies align operations with recommended beyond-use dating and labeling practices.

The framework supports continued availability of essential therapies for rare species or unique indications. Regulatory clarity encourages investment in quality systems within compounding facilities. The initiative aligns with efforts to balance access and safety in veterinary medicine. Overall, this policy evolution strengthens the foundation for legitimate compounding activities.

Regional Analysis

North America is leading the Animal Drug Compounding Market

North America accounted for 38.1% of the animal drug compounding market in 2025 as veterinarians increasingly relied on customized medications to treat species-specific conditions and dosing requirements. Veterinary practitioners frequently prescribe compounded formulations when commercially available drugs do not meet the exact dosage, flavor, or delivery needs for animals such as horses, companion pets, and exotic species.

The American Veterinary Medical Association reported that the United States had more than 127000 licensed veterinarians in 2023, supporting a large clinical network that regularly uses compounded medications for individualized animal treatment.

Growing pet ownership across the United States and Canada has strengthened demand for tailored therapies used in dermatology, pain management, endocrinology, and oncology treatments for companion animals. Equine medicine and livestock management programs also depend on compounded formulations to address unique physiological differences among animal species.

Veterinary hospitals and specialty clinics are collaborating with compounding pharmacies to develop flavored oral suspensions, topical gels, and customized dosage forms that improve treatment compliance. Regulatory oversight from the U.S. Food and Drug Administration has also encouraged standardized quality practices in veterinary compounding pharmacies.

Veterinary education programs continue to emphasize individualized pharmacotherapy approaches for complex animal health conditions. These factors collectively supported steady expansion of customized veterinary pharmaceutical services across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to witness notable growth during the forecast period as expanding veterinary healthcare services and rising animal ownership increase demand for specialized pharmaceutical formulations. The Food and Agriculture Organization estimates that the global livestock population includes billions of animals raised for agriculture, with a large share located across Asian countries where veterinary treatment needs are substantial.

Governments across China, India, Australia, and Southeast Asia are strengthening veterinary healthcare systems and expanding disease management programs for both livestock and companion animals. Increasing urbanization and higher disposable income levels have encouraged growth in pet ownership, particularly among younger populations in metropolitan areas.

Veterinary clinics and hospitals are therefore seeking customized medications that address dosage flexibility and species-specific treatment requirements. Universities and veterinary training institutions across the region are strengthening pharmacology and animal medicine programs to support modern treatment approaches.

Regional pharmaceutical manufacturers and veterinary pharmacies are expanding capabilities to produce tailored dosage forms suitable for different animal species. Governments are also strengthening regulatory frameworks that support safe veterinary pharmaceutical practices and product quality standards. These developments are expected to drive continued expansion of customized veterinary medication services throughout Asia Pacific in the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key companies in the Animal Drug Compounding market pursue expansion by developing customized veterinary formulations, strengthening partnerships with veterinary clinics, and expanding specialized pharmacy networks that address unique dosing requirements for companion and livestock animals.

Firms invest in advanced compounding technologies and quality assurance systems to deliver flavored medications, alternative dosage forms, and patient-specific treatments that standard veterinary drugs cannot provide. They also broaden distribution channels through online veterinary pharmacies and direct collaboration with animal hospitals to improve medication accessibility.

Wedgewood Pharmacy represents a prominent participant in the Animal Drug Compounding market and operates as a U.S.-based veterinary compounding pharmacy that prepares customized medications for veterinarians and animal owners across a wide range of species.

The company focuses on pharmaceutical quality standards, tailored formulations, and convenient delivery services that support individualized animal care. Competitors continue to expand veterinary service networks, introduce new compounded therapies, and strengthen regulatory compliance practices to reinforce trust and accelerate growth across the Animal Drug Compounding market.

Top Key Players

- WEDGEWOOD PHARMACY

- Akina Animal Health

- Central Compounding Center South

- AVRIO Pharmacy

- NexGen Pharmaceuticals

- Pace Pharmacy

- SaveWay Compounding Pharmacy

- ScriptWorks

- Summit Veterinary Pharmacy Ltd.

- Apothecary & Co.

- Veterinary Pharmaceutical Solutions

Recent Developments

- In June 2025, Wedgewood Pharmacy announced the release of a new compounded oral antiviral formulation, GS-441524, for the treatment of feline infectious peritonitis (FIP). According to recent reports, this formulation provides a customized, flavored option that significantly improves owner compliance and treatment outcomes for a previously difficult-to-manage condition.

- In July 2025, the FDA updated its list of bulk drug substances for office stock compounding, adding gabapentin for use in non-food animals. As per the regulatory announcement, this inclusion allows veterinarians to maintain immediate access to critical medications for treating seizures and neuropathic pain in companion animals without waiting for individual patient prescriptions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 1.5 Billion |

| Forecast Revenue (2035) | US$ 3.6 Billion |

| CAGR (2026-2035) | 9.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Dosage Form (Flavored Suspensions and Liquids, Transdermal Gels/Creams, Capsules and Tablets, Flavored Chews and Others), By Product (CNS Agents, Anti-infective Agents, Anti-inflammatory Agents, Hormones & Substitutes and Others), By Route of Administration (Oral, Injectable, Topical and Other Routes), By Animal (Companion Animals and Livestock Animals) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | Wedgewood Pharmacy, Akina Animal Health, Central Compounding Center South, AVRIO Pharmacy, NexGen Pharmaceuticals, Pace Pharmacy, SaveWay, ScriptWorks, Summit Veterinary Pharmacy, Apothecary & Co., Veterinary Pharmaceutical Solutions. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |