Quick Navigation

Overview

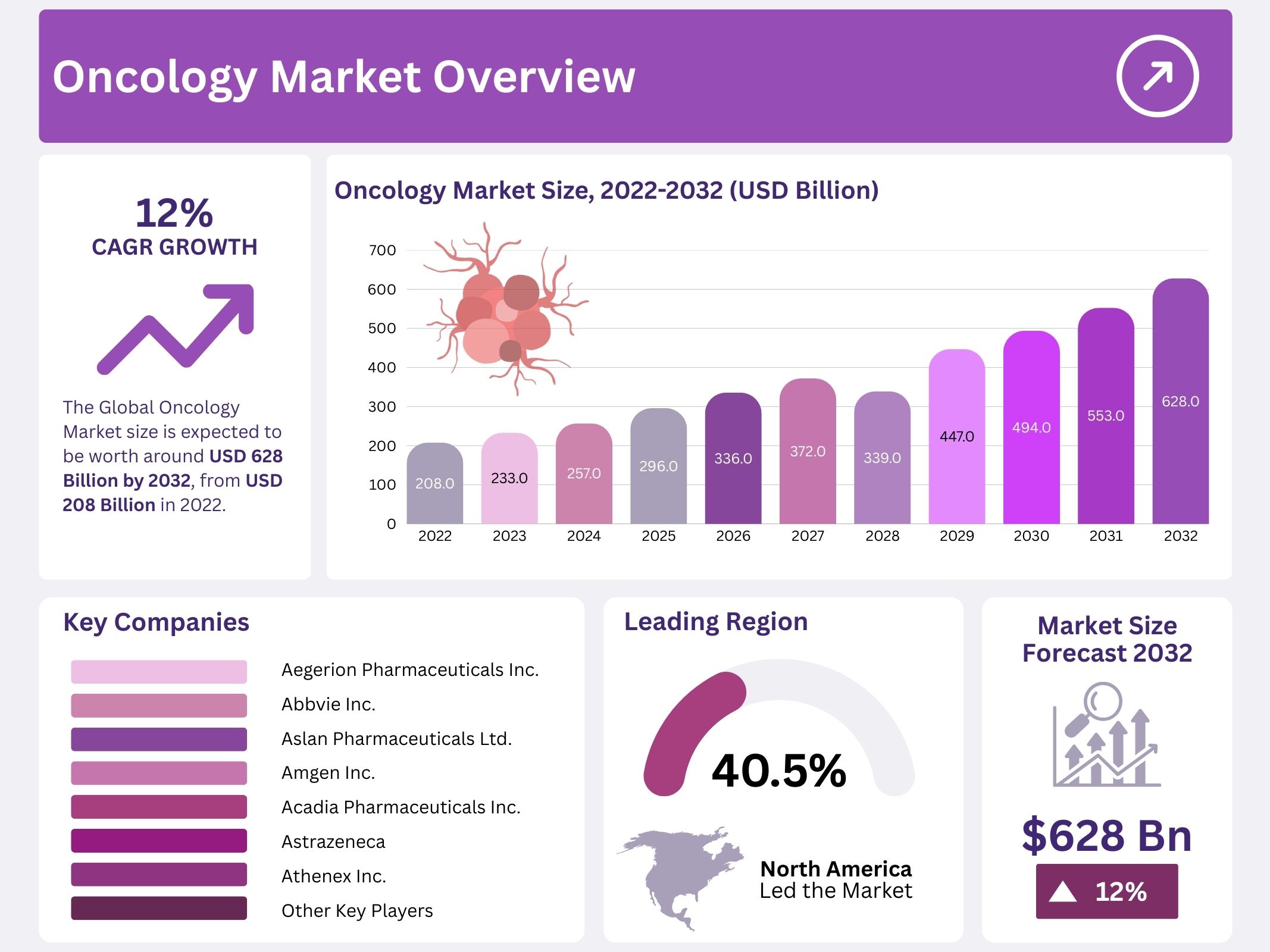

The oncology market is projected to grow significantly, reaching around USD 628 billion by 2032 from USD 208 billion in 2022. This expansion represents a compound annual growth rate (CAGR) of 12% during the forecast period. Growth is driven by multiple factors, including rising cancer incidence, increasing healthcare expenditure, and rapid technological progress in cancer diagnosis and treatment. The demand for innovative therapies, early detection tools, and effective management solutions is shaping the sector’s future outlook.

The primary driver of this market is the increasing global burden of cancer. According to the World Health Organization, cancer is the second leading cause of death worldwide, accounting for nearly 10 million deaths annually. Rising cases across regions have created consistent demand for new treatment options. The growing prevalence highlights the need for advanced diagnostics, therapies, and comprehensive oncology care, reinforcing the importance of continuous innovation and investment in the sector.

Technological advancements are playing a pivotal role in shaping oncology. Precision medicine, genomics, and immunotherapies are transforming treatment approaches. Breakthroughs in AI-driven diagnostics and liquid biopsy techniques are facilitating early detection and enhancing patient survival rates. These innovations are supporting the shift toward personalized treatment plans, which improve patient outcomes and enable more effective cancer management strategies across diverse populations.

Rising healthcare expenditure is also fueling market expansion. Governments, insurers, and patients are investing heavily in cancer care. Developed economies are increasing reimbursement support for innovative therapies, while emerging markets are expanding healthcare budgets to improve access. Significant infrastructure investments are being made to strengthen oncology care systems, ensuring that advanced treatment options become more widely available across regions.

Immuno-oncology is one of the fastest-growing segments within the industry. Therapies such as checkpoint inhibitors, CAR-T cell treatments, and monoclonal antibodies have shown strong clinical success in treating cancers previously considered untreatable. Expanding approvals across multiple cancer types are further driving adoption. Strategic collaborations, mergers, and research partnerships among pharmaceutical and biotechnology companies are also accelerating the development and commercialization of new therapies.

The oncology market is further supported by demographic and regulatory factors. The global geriatric population, expected to double by 2050, represents a major driver, as cancer risk increases with age. Additionally, regulatory agencies such as the FDA and EMA are providing accelerated approval pathways for breakthrough therapies. Awareness campaigns and national screening programs are improving early detection rates, contributing to higher demand for diagnostics and treatments. These combined dynamics underline the oncology sector’s strong growth potential through 2032.

Key Takeaways

- The global oncology market was valued at USD 208 billion in 2022, with strong growth expected in the next decade.

- The market is projected to reach USD 628 billion by 2032, indicating significant expansion driven by technological progress and rising cancer prevalence.

- An annual growth rate of 12% is forecasted for the oncology market from 2023 to 2032, highlighting steady sector advancement worldwide.

- Europe contributed 24.1% revenue share in 2022, reflecting its significant role in shaping the global oncology market’s overall development.

- North America dominated the global oncology market in 2022, capturing more than a 40.5% share and holds US$ 84.2 Billion market value for the year.

- The increasing global prevalence of cancer is attributed to population growth, aging demographics, and lifestyle changes that elevate risk factors.

- Technological advancements such as artificial intelligence detectors and liquid biopsy techniques are fueling oncology market growth by improving diagnostic precision and efficiency.

- Pharmaceutical and biotechnology companies are heavily investing in oncology-focused research and development to innovate new cancer treatment solutions.

- Governments are extending financial support for cancer immunotherapy research, accelerating the development and availability of novel and effective treatment options.

- High treatment costs continue to be a major barrier to effective cancer care, especially in low- and middle-income developing countries.

- AI-based cancer detection systems represent a recent and transformative trend in oncology, driving improvements in early diagnosis and patient outcomes.

- Hospitals currently account for the majority end-user share in the oncology market, due to high patient inflow and advanced treatment facilities.

- In North America, the oncology market is driven by advanced healthcare infrastructure, higher awareness levels, and widespread adoption of novel therapies.

- Latin America and the Middle East & Africa show moderate oncology market growth, hindered by economic constraints and limited healthcare access.

Regional Analysis

In 2022, North America held a dominant market position, capturing more than a 40.5% share and holds US$ 84.2 Billion market value for the year. The dominance of the region can be linked to the high cancer incidence in major countries, particularly the United States. According to the American Cancer Society, over 1.8 million new cancer cases and more than 606,000 related deaths were recorded in the U.S. in 2020. The most prevalent cancers include lung, colorectal, breast, and prostate cancers. These conditions continue to drive market growth across the region.

The significance of the North American oncology market is further strengthened by strong healthcare infrastructure and high healthcare spending. Since 1991, cancer mortality in the U.S. has decreased by nearly 29% due to wider adoption of oncology treatments. This steady decline highlights advancements in therapeutic options and improved accessibility. The presence of leading pharmaceutical companies and advanced clinical research institutions also reinforces the region’s dominance, positioning North America as a key hub in oncology innovations and treatment adoption.

Europe is projected to be the most opportunistic oncology market during the forecast period. Technological advancements in cancer diagnostics and treatment are driving growth across the region. In addition, rising incidence rates and growing cancer-related deaths contribute to the increasing demand for oncology services. The European Commission estimated nearly 2.7 million new cancer cases and around 1.3 million cancer deaths in 2022. Such alarming statistics are creating a pressing need for enhanced therapies, thereby encouraging continuous investments in research and development initiatives.

Asia Pacific is expected to record the fastest compound annual growth rate of 7.4% over the forecast period. The expansion is supported by a large patient pool, which facilitates the recruitment of participants for oncology clinical trials. Biotech CROs such as Novotech confirm the region’s growing importance in oncology research. With lower trial density and a strong base of active investigators, Asia Pacific is emerging as a preferred destination for clinical studies. Global biotechnology firms are increasingly outsourcing oncology CRO services to the region.

Segmentation Analysis

The cancer diagnostics market is segmented into imaging testing, biomarkers testing, in vitro diagnostic testing, and biopsy. Among these, the in vitro diagnostic testing segment is expected to witness the fastest growth during 2022–2030. This can be attributed to its increasing adoption and the introduction of new diagnostic products by leading players. The market is further categorized into instrument-based tests, laboratory tests, and liquid biopsies. The demand for accurate, early-stage cancer detection is driving rapid expansion of this segment across global healthcare systems.

The cancer treatment segment is also undergoing transformation. Targeted therapy and immunotherapy are increasingly being adopted over conventional chemotherapy. This shift is due to their lower toxicity, improved effectiveness, and ability to selectively target cancer cells while sparing healthy ones. Growing awareness of hormonal therapies and targeted approaches is strengthening market demand. As a result, targeted therapy has become a key driver of oncology market growth. Increasing public preference for advanced, less invasive treatment options continues to expand the global cancer treatment landscape.

From an end-user perspective, hospitals dominate the cancer diagnostics market, holding the largest revenue share. Hospitals are regarded as the preferred setting for diagnostics due to advanced technology, skilled staff, and comprehensive care facilities. Rising cancer prevalence, coupled with higher treatment costs in developed regions, is also contributing to this dominance. Additionally, strategic acquisitions, such as City of Hope’s USD 390 million purchase of Cancer Treatment Centers of America in 2021, are enhancing service integration. Hospitals are expected to maintain leadership as the primary centers for cancer diagnosis and treatment worldwide.

Key Players Analysis

The cancer drugs market is experiencing significant growth due to innovative product offerings and the entry of new players. Leading companies such as IBM, Azra AI, Siemens Healthineers, GE Healthcare, Intel, NVIDIA, Digital Diagnostics Inc., and Concert are at the forefront of artificial intelligence in oncology. Strategic collaborations are strengthening the development of advanced solutions. For example, Intel and the University of Pennsylvania’s Perelman School of Medicine partnered to create an AI model that assists in the identification of brain tumors, highlighting industry-wide innovation.

The AI model will be developed by Penn Medicine in collaboration with 29 global organizations through a federated learning approach. This method enables organizations to train AI models without the need to share sensitive patient data, ensuring data privacy and compliance. By adopting this innovative approach, the consortium is addressing one of the most critical challenges in healthcare AI—data confidentiality. Such initiatives are expected to accelerate adoption, improve diagnostic efficiency, and contribute to long-term market expansion in oncology.

To expand market presence, companies are increasingly pursuing mergers, acquisitions, and partnerships. A notable example includes the merger of Imagia Cybernetics and Canexia Health, which combines expertise in AI healthcare and oncology genomics. These alliances focus on developing advanced oncology diagnostics and treatments while strengthening research and development capabilities. The commitment to cutting-edge solutions reflects the strategic intent of players to capture emerging opportunities in the oncology market. Investments in research, coupled with innovative product launches, will continue to drive competitive advantage and future market growth.

Market Key Players

- Aegerion Pharmaceuticals Inc.

- Abbvie Inc.

- Aslan Pharmaceuticals Ltd.

- Amgen Inc.

- Acadia Pharmaceuticals Inc.

- Astrazeneca

- Athenex Inc.

- Takeda Oncology

- Aspen Pharmacare Holdings Limited.

- Ability Pharma

- Other key players

Conclusion

The oncology market shows strong potential for continuous growth, supported by rising cancer cases, rapid advancements in technology, and increasing healthcare investments. Demand for innovative treatments such as immunotherapy and targeted therapy is reshaping cancer care, while early detection tools are improving patient outcomes. The role of artificial intelligence and precision medicine is becoming more significant, enabling personalized treatment plans and boosting efficiency. Despite challenges such as high treatment costs and limited access in developing regions, opportunities remain substantial. With strong regional contributions, increasing collaborations, and supportive regulatory frameworks, the oncology market is positioned for steady expansion and long-term sustainability in the global healthcare landscape.

Get in Touch with Us:

Market.us (Powered By Prudour Pvt. Ltd.)

Address: 420 Lexington Avenue, Suite 300, New York City, NY 10170, United States.

Contact No: +1 718 874 1545 (International), +91 78878 22626 (Asia).

Email: [email protected]

View More

Precision Oncology Market || Radiation Oncology Market || Interventional Oncology Ablation Market || Oncology Drugs Market || Veterinary Oncology Market || Clinical Oncology Next Generation Sequencing Market || Immuno-Oncology Market || Non Oncology Precision Medicine Market || Artificial Intelligence in Oncology Market || Oncology Information Systems Market