Quick Navigation

Report Overview

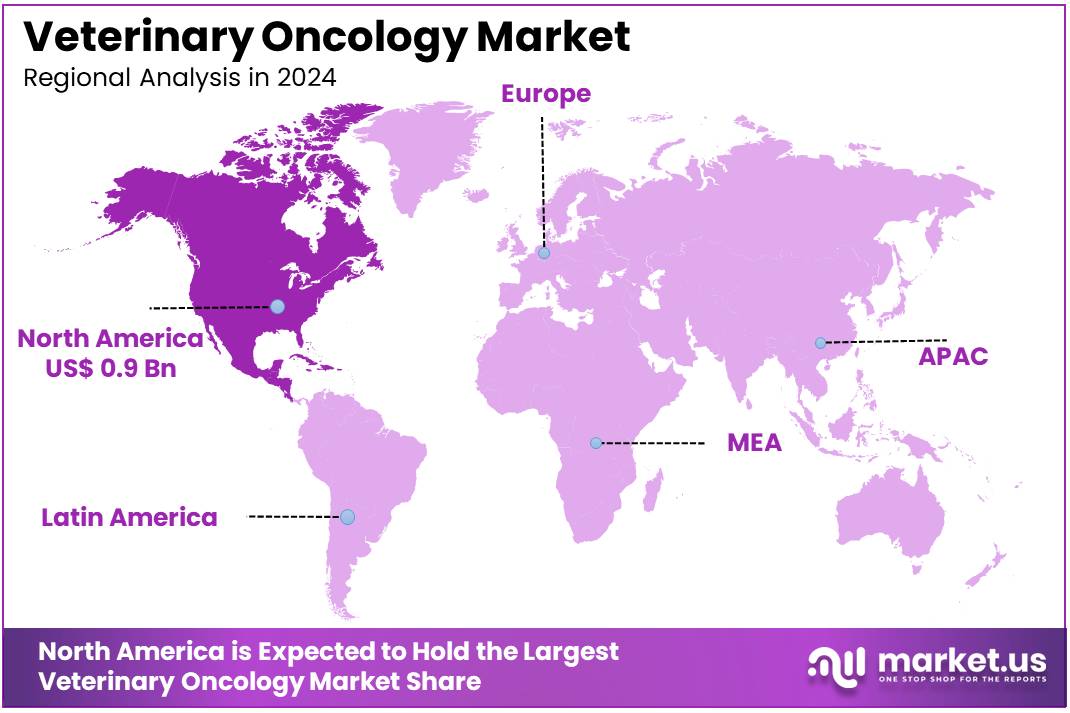

The Global Veterinary Oncology Market size is expected to be worth around US$ 5.1 Billion by 2034, from US$ 1.7 Billion in 2024, growing at a CAGR of 11.7% during the forecast period from 2024 to 2034. North America held a dominant market position, capturing more than a 53% share and holds US$ 0.9 Billion market value for the year.

The veterinary oncology market is driven by the increasing prevalence of cancer in companion animals, particularly dogs and cats. Advances in diagnostic technologies, such as molecular diagnostics and imaging, have enhanced early detection, contributing to market growth. Additionally, rising awareness among pet owners about cancer treatments and the growing willingness to spend on advanced veterinary care are significant drivers.

The development of targeted therapies and immunotherapies, similar to those used in human oncology, has further expanded treatment options. However, the market faces challenges, including the high cost of veterinary oncology treatments, which can limit access for some pet owners. Limited availability of veterinary oncologists and specialized treatment centers also restricts growth in certain regions.

Opportunities lie in increasing adoption of pet insurance and expanding research collaborations between veterinary and human oncology sectors. Cancer is a leading cause of death in dogs and cats, particularly as they age. In dogs, approximately 1 in 4 will develop neoplasia during their lifetime, and almost 50% of dogs over the age of 10 will develop cancer. Common cancers in dogs include lymphoma, mast cell tumors, and osteosarcoma. In cats, cancer accounts for approximately 32% of deaths, with lymphoma being the most common type, followed by squamous cell carcinoma and mammary gland tumors.

Key Takeaways

- The global veterinary oncology market was valued at US$ 1.7 billion in 2024 and is anticipated to register substantial growth of US$ 5.1 billion by 2034, with 11.7% CAGR.

- In 2024, the canine segment took the lead in the global market, securing 82% of the total revenue share.

- The immunotherapy segment took the lead in the global market, securing 24% of the total revenue share.

- North America maintained its leading position in the global market with a share of over 53% of the total revenue.

Animal Type Analysis

Based on animal type the market is fragmented into canine, feline, and others. Amongst these, canine dominated the global veterinary oncology market capturing a significant market share of 82% in 2024. The canine segment holds the largest share in the global veterinary oncology market, driven by the high prevalence of cancer in dogs compared to other companion animals.

Common cancers in dogs, such as lymphoma, mast cell tumors, and osteosarcoma, require advanced diagnostic and therapeutic solutions, fueling market growth. Increasing pet adoption rates and the rising human-animal bond have encouraged pet owners to invest in sophisticated veterinary care, including oncology treatments.

Treatment Type Analysis

The market is fragmented by treatment type into immunotherapy, radiotherapy, surgery, chemotherapy, and other treatment types. Immunotherapy dominated the global veterinary oncology market capturing a significant market share of 24% in 2024. Immunotherapy has established itself as a dominant segment in the global veterinary oncology market, capturing a significant share due to its advanced and targeted approach in treating cancer.

This therapy utilizes the animal’s immune system to identify and destroy cancer cells, reducing the need for invasive treatments and minimizing side effects. It has shown promising results in managing complex cancers, such as lymphoma and melanoma, particularly in dogs. The increasing availability of monoclonal antibodies, cancer vaccines, and immune checkpoint inhibitors has driven the adoption of immunotherapy.

Growing investment in veterinary research and development has further accelerated innovations in this field. Pet owners are increasingly seeking effective and less stressful cancer treatments, fuelling the demand for immunotherapy.

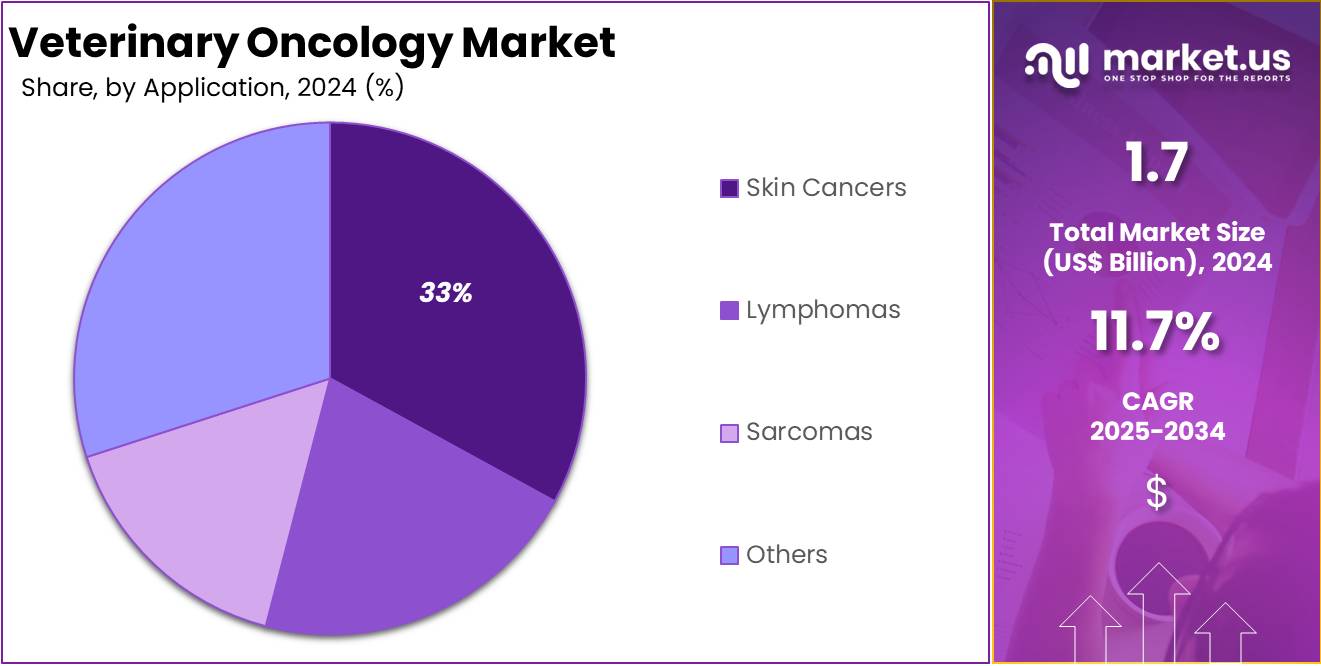

Application Analysis

The market is fragmented by application into skin cancers, lymphomas, sarcomas, and others. Skin cancers dominated the global veterinary oncology market capturing a significant market share of 32% in 2024. Skin cancers represent the largest segment in the global veterinary oncology market, driven by their high prevalence among companion animals, particularly dogs and cats.

Common types such as mast cell tumors, melanomas, and squamous cell carcinomas are frequently diagnosed, often attributed to prolonged exposure to UV radiation, genetic predisposition, or ageing. This growth is largely driven by the high prevalence of squamous cell carcinoma in cats and dogs, with skin tumors being the most common type of cancer in older dogs.

Key Segments Analysis

By Animal Type

- Canine

- Feline

- Others

By Treatment Type

- Immunotherapy

- Radiotherapy

- Surgery

- Chemotherapy

- Other Treatment Types

By Application

- Skin Cancers

- Lymphomas

- Sarcomas

- Others

Drivers

Increasing Prevalence of Cancer

The increasing prevalence of cancer among pets, particularly aging cats and dogs, is driving growth in the veterinary oncology market. Cancer has become a leading concern for pet owners, with many seeking advanced treatment options. According to The Veterinary Cancer Society, cancer is the leading cause of death in 47% of dogs over 10 years old and 32% of cats. Additionally, 1 in 4 dogs develops abnormal tissue growth during their lifetime, highlighting the urgent need for effective veterinary oncology solutions.

Advancements in veterinary oncology therapies are fueling market growth. Cutting-edge treatments, including targeted therapies and immunotherapy, are revolutionizing pet cancer care. These innovations provide improved outcomes and more precise treatments for various types of pet cancers. Research and development in this field are accelerating, with increased investment from veterinary pharmaceutical companies. As a result, pet owners now have access to advanced therapeutic options that were previously unavailable, boosting the demand for specialized oncology services.

Awareness of pet cancer is rising among pet owners, contributing to the growth of the veterinary oncology market. Many owners now prioritize their pets’ health and safety, seeking early diagnostic and treatment options. Educational efforts by veterinarians and animal health organizations play a critical role in spreading knowledge. This growing awareness has led to an increase in routine veterinary checkups and proactive cancer screenings, enhancing the adoption of oncology care for pets.

The veterinary oncology market is expanding due to the convergence of these factors. Pet owners are increasingly investing in advanced diagnostic tools and treatment plans. The focus on animal health and safety continues to grow, with a strong emphasis on improving the quality of life for pets with cancer. As demand for oncology care rises, the market is poised for further development, driven by innovation, awareness, and the unwavering commitment of pet owners to their companions’ well-being.

Restraints

High Cost of Treatment

Advanced therapies such as immunotherapy, radiation therapy, and targeted drugs are often expensive due to the complexity of development and specialized equipment required. Additionally, diagnostic tools like CT scans, MRIs, and molecular profiling contribute to the overall cost, making oncology care unaffordable for many households. The lack of widespread pet insurance exacerbates this issue, as most expenses are paid out-of-pocket by pet owners.

Even in regions with higher adoption of pet insurance, coverage for cancer treatments may be limited, further discouraging uptake. Small animal clinics in rural or underserved areas may also face challenges in providing advanced oncology care due to resource constraints. These financial barriers hinder market growth, emphasizing the need for cost-effective solutions and broader insurance coverage to expand accessibility.

Opportunities

Increasing R&D in Veterinary Oncology

The surge in research and development (R&D) activities in veterinary oncology is unlocking significant growth opportunities for the market. Advancements in diagnostic technologies, such as molecular diagnostics and imaging tools, have improved early cancer detection, enhancing treatment outcomes. Additionally, R&D is driving the development of innovative therapies, including targeted treatments, immunotherapies, and cancer vaccines, which are revolutionizing oncology care for pets.

- For instance, in May 2024, the AKC Canine Health Foundation (CHF) committed $3.6 million to canine cancer research, funding studies on oral melanoma and osteosarcoma, with potential applications for human cancer therapies.

- In September 2024, CureLab Veterinary Inc. secured $15 million to advance its gene therapy, ElenaVet, designed to enhance the immune response against cancer and mitigate chronic inflammation in pets. The company aims to improve pet health and extend their lifespan through cutting-edge cancer treatments.

Impact of macroeconomic factors / Geopolitical factors

Macroeconomic factors, such as rising disposable incomes and increased pet ownership in developed and emerging markets, significantly influence the veterinary oncology market. Economic stability fosters higher spending on advanced veterinary treatments, including oncology care. Conversely, economic downturns or inflationary pressures may limit pet owners’ ability to afford costly cancer treatments, impacting market growth.

Geopolitical factors, such as trade regulations, international conflicts, and supply chain disruptions, can affect the availability and pricing of veterinary oncology drugs and equipment. For instance, reliance on imported medical supplies may face challenges during geopolitical tensions, delaying treatment accessibility. Additionally, varying regulatory frameworks across countries impact the approval and commercialization of veterinary oncology therapies.

Trends

The veterinary oncology market is witnessing notable advancements driven by innovation and growing awareness. A key trend is the increasing adoption of targeted therapies, such as tyrosine kinase inhibitors, which offer precise treatment with fewer side effects. Immunotherapy, including cancer vaccines and monoclonal antibodies, is also gaining traction as a promising approach in veterinary oncology.

The use of artificial intelligence (AI) in diagnostics and treatment planning is another emerging trend, enabling faster and more accurate cancer detection. Telemedicine is facilitating access to veterinary oncologists, particularly in remote areas, improving treatment availability. Personalized medicine, based on genetic profiling of tumours, is becoming more common, enhancing treatment outcomes.

Regional Analysis

North America held a significant 53% share of the veterinary oncology market and holds US$ 0.9 Billion value for the year 2024. This growth is fuelled by increasing demand for advanced oncology care, driven by strategic initiatives from key players to expand access to precision medicine for pet cancer.

Companies in the region are actively collaborating to introduce innovative treatments and improve care quality. By leveraging the unique strengths of both companies, this collaboration enhances expertise, broadens access to cutting-edge precision treatments for animals, and promotes innovation within the veterinary oncology market.

- For example, in July 2023, Ardent and FidoCure announced an innovative partnership to deliver oncology advancements in the animal health sector.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The veterinary oncology market is characterized by intense competition, with several key players focusing on innovation, strategic partnerships, and geographic expansion. Prominent companies, such as Zoetis Inc., Elanco Animal Health, and Boehringer Ingelheim, dominate the market with a strong portfolio of cancer diagnostics, therapies, and vaccines.

Mergers, acquisitions, and joint ventures are common strategies for enhancing market presence and technology access. For instance, partnerships between veterinary healthcare providers and biotechnology firms are expediting the development of targeted therapies and immunotherapy solutions.

Zoetis Inc. is a global leader in animal health, offering innovative solutions for disease prevention and treatment in livestock and companion animals. The company’s portfolio includes vaccines, diagnostics, and therapeutic products, emphasizing research-driven advancements. In addition, Elanco Animal Health specializes in developing and marketing products to improve animal health and food safety. Its offerings include pharmaceuticals, vaccines, and diagnostics for pets and farm animals, focusing on sustainable and innovative solutions.

Top Key Players in the Veterinary Oncology Market

- Elanco

- Boehringer Ingelheim International GmbH

- Zoetis

- Elekta AB

- PetCure Oncology

- Accuray Incorporated

- Varian Medical Systems, Inc.

- Virbac

- Merck & Co., Inc.

- Dechra Pharmaceuticals PLC

- NovaVive Inc.

- Ardent Animal Health, LLC

Recent Developments

- In September 2024: Boehringer Ingelheim International GmbH completed the acquisition of Saiba Animal Health AG. This strategic move aims to broaden their animal therapeutics offerings, particularly enhancing the veterinary oncology sector. The integration of Saiba’s innovative vaccine development platform is expected to significantly advance cancer treatment options for animals.

- In July 2024: Dechra Pharmaceuticals PLC strengthened its pipeline by acquiring Invetx, further solidifying its position in the veterinary market.

- In March 2024: Merck & Co., Inc. completed the acquisition of Harpoon Therapeutics, Inc., aiming to diversify its oncology pipeline and broaden its therapeutic offerings.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 1.7 billion |

| Forecast Revenue (2034) | US$ 5.1 billion |

| CAGR (2025-2034) | 11.7% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Animal Type (Canine, Feline, and Others), By Treatment Type (Immunotherapy, Radiotherapy, Surgery, Chemotherapy, and Other Treatment Types), By Application (Skin Cancers, Lymphomas, Sarcomas, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Elanco, Boehringer Ingelheim International GmbH, Zoetis, Elekta AB, PetCure Oncology, Accuray Incorporated, Varian Medical Systems, Inc., Virbac, Merck & Co., Inc., Dechra Pharmaceuticals PLC, NovaVive Inc., Ardent Animal Health, LLC |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |