Quick Navigation

Report Overview

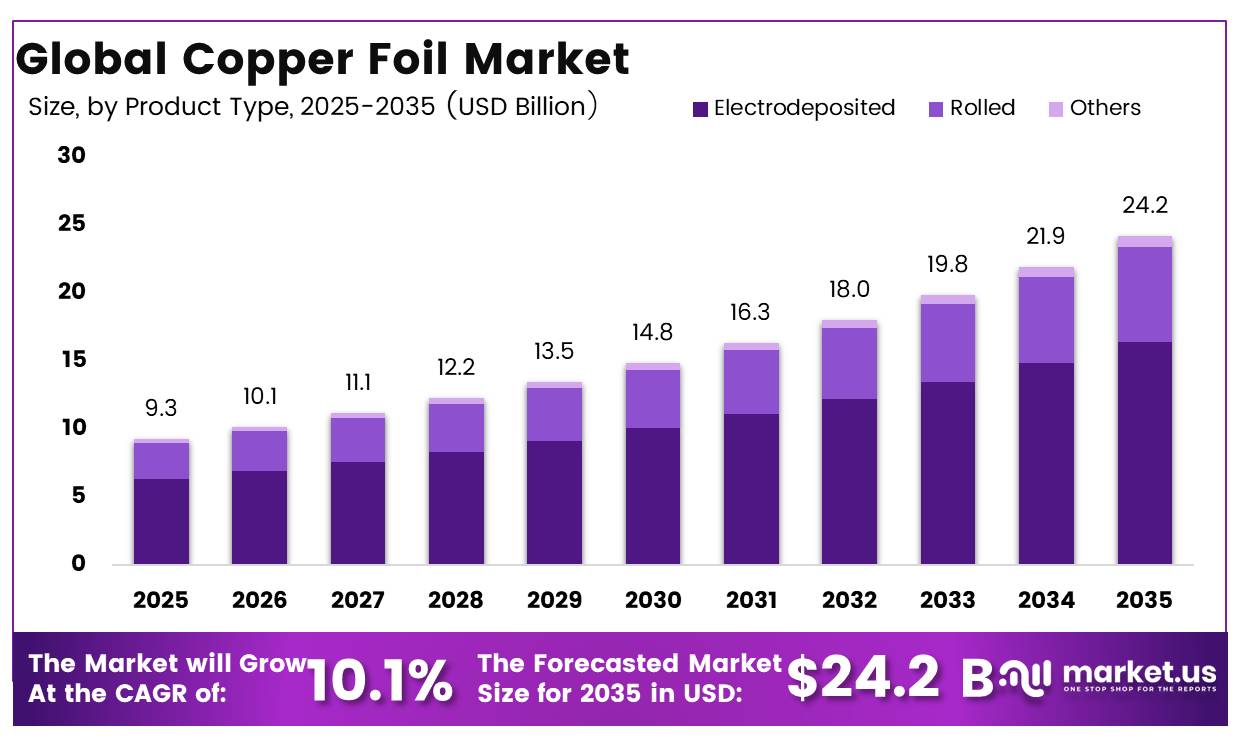

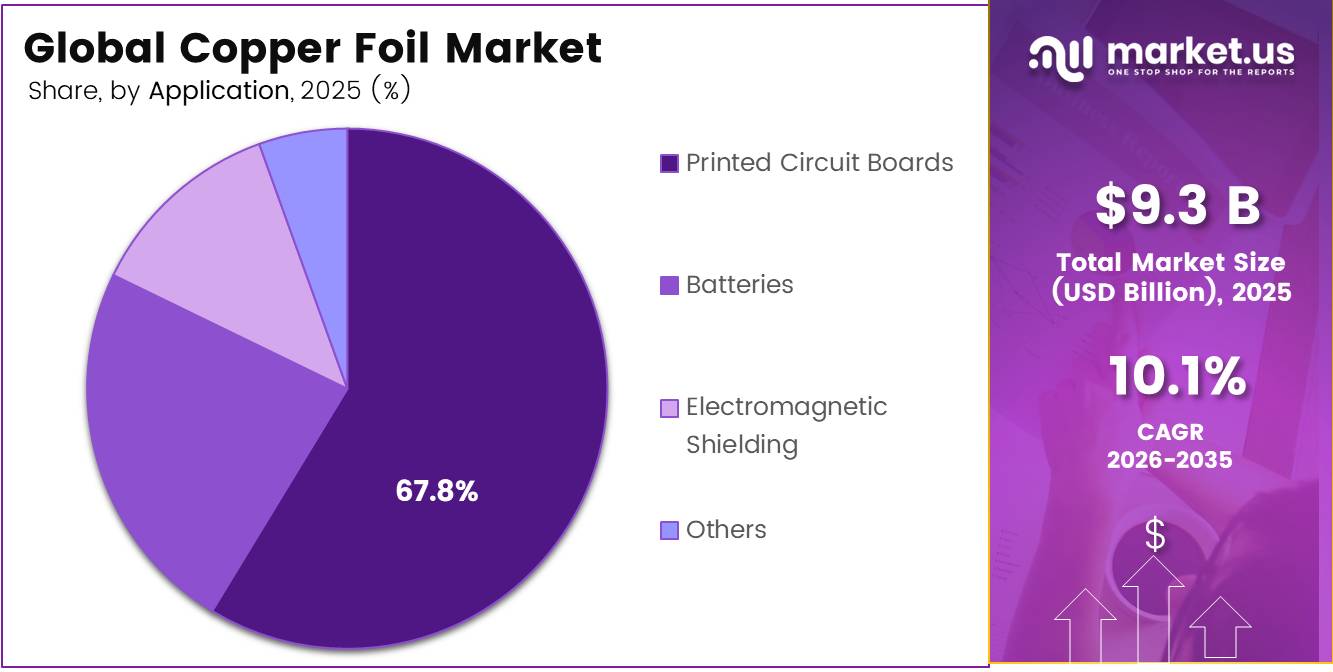

In 2025, the Global Copper Foil Market was valued at USD 9.3 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 10.1%, reaching about USD 24.2 billion by 2035. Asia pacific led the market, achieving over 32.50% share with a revenue of USD 5.43 Billion.

Copper foil is a thin, high-conductivity material used as the anode current collector in lithium-ion batteries and as a conductive layer in printed circuit boards, flexible electronics, electromagnetic shielding and industrial components. Battery-grade foil is produced through electrodeposition, followed by surface treatment, inspection and precision slitting, while rolled copper foil serves applications requiring flexibility and fatigue resistance.

- The International Energy Agency reported that global electric-car sales exceeded 20 million units in 2025, representing one-quarter of all new cars sold. EV battery deployment reached 1.2 TWh, rising almost 30% from 2024, while global lithium-ion battery nameplate capacity surpassed 4 TWh by year-end. These trends support demand for electrodeposited copper foil used across cylindrical, prismatic and pouch cells.

Key Takeaways

- The global copper foil market was valued at USD 9.3 billion in 2025.

- The global market is projected to grow at a CAGR of 10.1% and is estimated to reach USD 24.2 billion by 2035.

- On the basis of product type, the electrodeposited copper foil dominated the market, constituting 67.8% of the total market share.

- Based on the application, the printed circuit boards dominated the copper foil market, with a substantial market share of around 58.7%.

- Among the end-use industries, the electrical and electronics industry held a major share in the copper foil market, accounting for 45.6% of the market share.

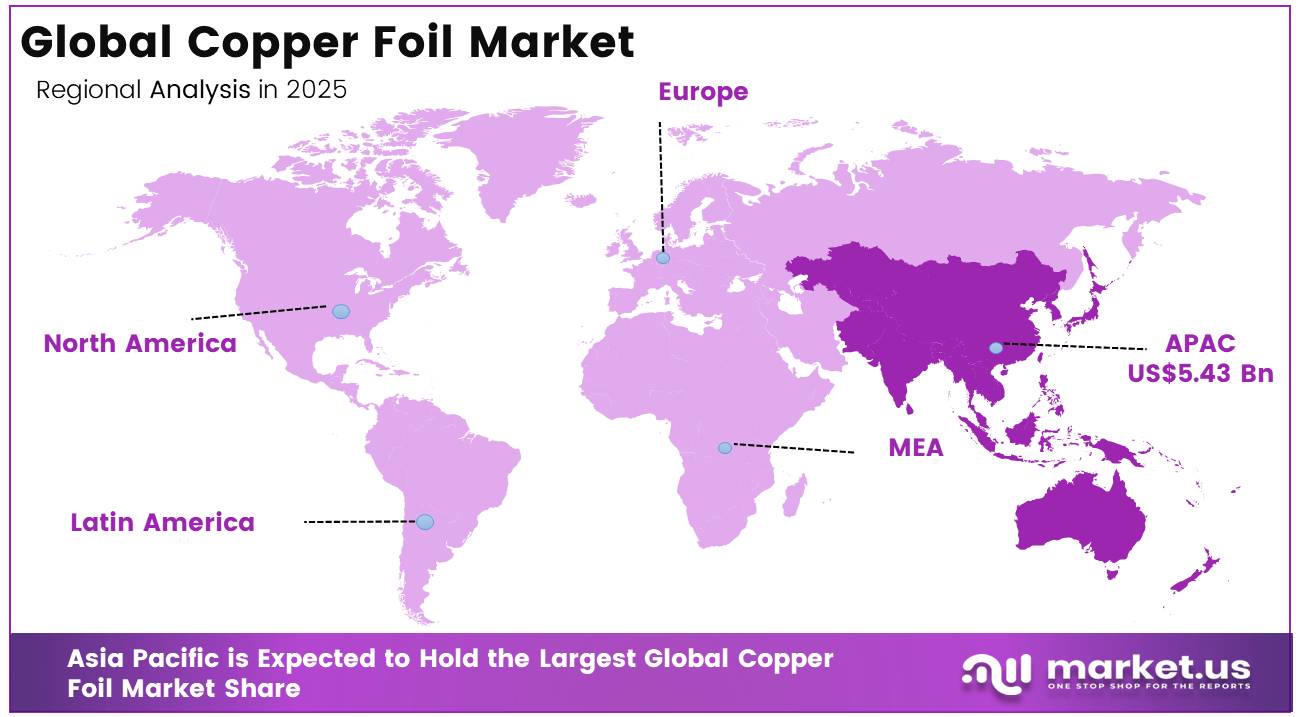

- In 2025, the Asia Pacific was the most dominant region in the copper foil market, accounting for 58.7% of the total global consumption.

Copper sits at the centre of modern industry because it is one of the few materials that cannot be easily replaced in electrification, power grids, and digital infrastructure. Global demand reached around 27 million tonnes in 2024, and is projected to rise toward 42 million tonnes by 2040, driven by EV expansion, renewable energy buildout, and the rapid scaling of AI data centres, as highlighted across recent IEA critical minerals outlooks and S&P Global analysis on long-term copper demand.

On the supply side, production is heavily concentrated in a small group of countries, with Chile at roughly 5.3 million tonnes (~23% of global output) and the DRC at about 3.4 million tonnes in 2025, while bringing new mines online typically takes around 17 years, according to USGS mineral supply data and IEA pipeline assessments. Even though recycling now contributes about 20% of refined supply, it is still expected to cover only around 1/3 of total demand by 2040, meaning the market continues to rely heavily on primary mining that is not expanding fast enough to close the gap.

Copper Foil Market Segment

Product Type Analysis

Electrodeposited copper foil represents dominant Segment in the Market.

Electrodeposited copper foil clearly leads the global market with a 67.8% share, mainly because it fits seamlessly into large-scale electronics and battery manufacturing systems. Its production process is cost-efficient and highly scalable, which makes it the preferred choice for high-volume applications like printed circuit boards and lithium-ion batteries. Over time, manufacturers have also built their production ecosystems around electrodeposited foil specifications, which has created strong switching barriers.

Rolled annealed foil is growing faster because it offers better flexibility and mechanical strength. This makes it more suitable for applications where bending, folding, or repeated mechanical stress is involved, such as flexible electronics and next-generation battery designs. In 2025, increasing activity in foldable consumer devices and early-stage solid-state battery development has supported incremental demand for this type of foil. The remaining 3.3% includes niche specialty foils used in advanced or highly specific industrial applications.

Application Analysis

Printed Circuit Boards Are the Most Widely Used Application.

Printed circuit boards remain the largest application segment, accounting for 58.7% of total demand. This dominance is not new; it is the result of decades of electronics expansion. What continues to strengthen this segment today is the increasing complexity of electronic devices. Modern technologies such as 5G infrastructure, AI computing systems, and advanced automotive electronics all require more compact and layered PCB designs, which directly increases copper foil consumption per unit.

Battery applications are growing faster than any other segment. This is closely linked to the rapid expansion of electric vehicles and energy storage systems. Copper foil is a critical component in lithium-ion batteries, and demand rises sharply as gigafactories scale production. In 2025, several large battery manufacturers expanded capacity in both Asia and Europe, reflecting strong long-term confidence in EV adoption. However, growth is still constrained by the technical difficulty of producing ultra-thin battery-grade foil at large scale.

End Use Analysis

Copper Foil Are Mostly Utilized in the Electrical and Electronics Sector.

Electrical and Electronics Sector is the largest end-use industry, contributing 45.6% of global demand. This is driven by the broad and continuous expansion of electronic systems in everyday life. From smartphones and laptops to data centers and industrial automation, nearly every modern device depends on copper foil-based PCBs. What sustains this dominance is not just volume growth, but also increasing material intensity per device as designs become more complex and performance-driven.

The automotive sector is growing the fastest, mainly due to the shift toward electric vehicles. EVs require significantly more copper than traditional vehicles, particularly in batteries, power electronics, and control systems. In 2025, policy support in both Europe and North America continued to accelerate EV manufacturing investments, encouraging automakers to secure long-term copper supply agreements. This marks a shift from short-term procurement to structured sourcing strategies.

Key Market Segments

By Product Type

- Electrodeposited

- Rolled

- Others

By Application

- Printed Circuit Boards

- Batteries

- Electromagnetic Shielding

- Others

By End Use

- Aerospace and Defense

- Automotive

- Building and Construction

- Electrical and Electronics

- Industrial Equipment

- Medical

- Others

Driver Analysis

EV battery anode collector expansion

The dominant 2026 growth driver for copper foil is the sustained rise in lithium-ion battery output for electric vehicles, because copper foil remains the standard anode current collector and scales almost linearly with battery manufacturing volume. BloombergNEF’s 2026 EV Outlook indicates global passenger EV sales are reaching 23.3 million units in 2026, up 11% year on year, while the IEA-referenced coverage similarly places 2026 EV sales near 23 million and 28% of global car sales after 20+ million units in 2025.

This scale matters upstream: every battery cell requires copper foil in the anode stack, so higher EV volumes translate into direct foil tonnage pull, particularly in China, Europe, Korea, Japan, and North America where gigafactory build-outs remain concentrated. The commercial effect is not only volume growth but mix improvement, as battery-linked foil commands tighter tolerance, cleaner surfaces, and stronger adhesion performance than many standard electronics applications, allowing suppliers with stable yield and qualification depth to capture premium pricing.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV battery anode collector expansion | +2.8% | China core, EU battery belt, North America core, Korea-Japan | Medium term (2-4 years) |

| Ultra-thin foil migration to 6–4.5 µm | +2.1% | China, Korea, Japan, EU gigafactory corridors | Medium term (2-4 years) |

| Composite foil and light-weighting adoption | +1.4% | China pilot lines, Korea-Japan R&D hubs, EU premium cells | Long term (≥ 4 years) |

| AI server PCB and CCL intensity | +1.7% | Taiwan, China, Korea, North America data-center chains | Short term (≤ 2 years) |

| Stationary storage and grid battery scale-up | +1.3% | China, US, EU, India renewable corridors | Medium term (2-4 years) |

| High-frequency electronics miniaturization demand | +1.1% | APAC electronics hubs, North America, EU industrial tech | Short term (≤ 2 years) |

Restraint Analysis

Battery foil overcapacity

The market is also being restrained by a mismatch between aggressive capacity build-outs and uneven realization of downstream demand, particularly in China’s lithium-battery copper foil segment. SMM data show China’s overall copper foil operating rate reached 84.22% in October 2025 and 84.49% was expected in November, but the split is more revealing: large enterprises operated near 89.95%, while medium-sized players were only at 55.22% and small enterprises at 71.35%, indicating structural oversupply and uneven asset utilization rather than uniform tightness.

This is a classic value-destructive pattern: leading producers keep lines full through scale and customer lock-in, while second-tier suppliers discount aggressively to defend volumes, pulling down realized industry margins even when shipments rise. The restraint is amplified by the scale of the build cycle, with industry-overview data showing combined global lithium-battery and PCB copper foil shipments rising from about 735,000 tons in 2020 to 1.523 million tons in 2024 and projected to reach 3.3 million tons by 2030, a pace that encourages new entrants and speculative expansions before demand fully matures.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copper price volatility | -2.0% | Global, APAC core, EU, North America | Short term (≤ 2 years) |

| Battery foil overcapacity | -1.8% | China core, Korea, Taiwan, spill-over global | Medium term (2-4 years) |

| Ultra-thin yield bottlenecks | -1.5% | China, Korea, Japan, EU battery corridors | Medium term (2-4 years) |

| Localization and qualification barriers | -1.3% | North America, EU, Mexico, Eastern Europe | Medium term (2-4 years) |

| Energy and capex intensity | -1.2% | Asia manufacturing hubs, EU processors | Medium term (2-4 years) |

| PCB demand concentration risk | -0.9% | Taiwan, China, Korea, electronics export hubs | Short term (≤ 2 years) |

Opportunity Analysis

Composite current collector commercialization

Composite copper foil is not yet a baseline market driver because it remains pre-mass-commercial rather than broadly deployed, but it is one of the clearest long-duration opportunities to create new TAM in advanced batteries. Peer-reviewed 2024 research describes composite copper foil as a future-proof anode current collector for high-energy-density LIBs, showing a polypropylene-based structure with approximately 7 times stronger peel performance than an untreated comparison and strong electrochemical results.

The strategic upside comes from material efficiency and system-level economics: if composite formats reduce copper use per square meter while maintaining conductivity and mechanical stability, battery makers could potentially lower current collector mass by double-digit percentages and improve pack energy density enough to justify qualification in premium EV, aviation, or next-generation storage cells.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Localized battery foil platforms | +2.3% | North America core, EU battery belt, India emerging | Medium term (2-4 years) |

| Composite current collector commercialization | +1.9% | China, Korea, Japan, EU premium cell hubs | Long term (≥ 4 years) |

| AI laminate-grade foil premiumization | +1.6% | Taiwan, China, Korea, US data-center chain | Short term (≤ 2 years) |

| Recycling-linked low-carbon foil | +1.5% | EU, North America, Japan, Korea | Medium term (2-4 years) |

| India import-substitution scale-up | +1.4% | India core, South Asia spill-over, Middle East link | Medium term (2-4 years) |

| M&A in fragmented foil supply | +1.2% | China, Korea, Taiwan, EU niche processors | Short term (≤ 2 years) |

Challenges Analysis

Ultra-thin foil yield control

A 2026 technical review states that 6 µm foil still represents the mainstream product with about 58% market share, while 4.5 µm foil penetration is rising and composite copper foil is the next development path, which means suppliers are being pushed into tighter process windows before yields are fully optimized.

At the same time, China’s new GB safety standard effective July 1, 2026 tightens purity and tensile-strength thresholds, compelling local mills to upgrade electrodeposition lines or risk specification failures, thereby increasing pressure on already sensitive ultra-thin production. In practical terms, even a 3%–5% drop in first-pass yield on high-end foil can erase much of the gross-margin premium over standard grades because scrap, rework, and throughput loss rise nonlinearly at thinner gauges, and customer qualification lots become harder to reproduce consistently across shifts and lines.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Ultra-thin foil yield control | -1.6% | China, Korea, Japan, EU battery hubs | Medium term (2-4 years) |

| Customer qualification lag | -1.4% | North America, EU, Korea, Japan | Medium term (2-4 years) |

| AI-grade foil allocation stress | -1.2% | Taiwan, China, Korea, US electronics chain | Short term (≤ 2 years) |

| Operating-rate imbalance across suppliers | -1.1% | China core, APAC export hubs, global spill-over | Medium term (2-4 years) |

| Process energy and chemistry optimization | -1.0% | Asia manufacturing hubs, EU processors | Long term (≥ 4 years) |

| Compliance and localization adaptation | -0.9% | North America core, EU battery belt, China exporters | Medium term (2-4 years) |

Geopolitical Impact Analysis

Geopolitical Fragmentation Is Creating Multi-Theatre Supply Risk and Sustained Cost Inflation Across the Copper Value Chain.

The Russia-Ukraine war, Middle East tensions, and the US-China trade confrontation are now operating simultaneously, creating a compounded risk structure across the copper foil supply chain rather than isolated, manageable disruptions. Russia’s continued role in nickel and cobalt supply, combined with war-driven defence copper consumption, has tightened the broader critical minerals system, while Ukrainian copper reserves remain inaccessible. According to the IEA Global Critical Minerals Outlook 2025, multi-point geopolitical stress amplifies supply concentration risks particularly in markets where production is already heavily clustered in Asia.

Middle East conflict has intensified logistics and energy cost pressures through risks surrounding the Strait of Hormuz, identified by Wood Mackenzie as a key global energy risk point, while sulphuric acid supply disruptions have tightened copper refining inputs. Copper prices briefly surged above USD 14,500 per tonne in early 2026 before stabilising near USD 13,000, with ISM attributing part of this volatility to logistics disruption and insurance cost escalation. China’s export licensing system for critical minerals, highlighted by the USTR, reinforces long-term supply uncertainty given China’s dominant share of global copper foil capacity.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Copper Foil Market.

Asia Pacific remains the dominant region with a 58.7% share, largely because it is the global center of electronics manufacturing and battery production. Countries like China, South Korea, Japan, and Taiwan host a dense network of PCB manufacturers, EV battery producers, and consumer electronics assembly plants. This creates a tightly integrated supply chain where copper foil is produced and consumed within the same ecosystem, reducing logistics costs and improving production efficiency.

North America, however, is emerging as the fastest-growing region. Growth here is being driven more by policy and investment decisions than by existing manufacturing scale. Incentives supporting domestic EV battery production and semiconductor manufacturing are encouraging companies to build new facilities across the United States and Canada. In 2025, several large-scale battery plants reached operational or near-operational stages, contributing to rising copper foil demand.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Copper foil manufacturers compete primarily on three axes: electrolytic process technology ownership, substrate-grade purity capability, and customer qualification infrastructure across battery and printed circuit board supply chains. Competitive positioning is determined less by price alone and more by the ability to consistently deliver ultra-thin, high-elongation foil within tight thickness tolerances that lithium-ion battery cell manufacturers require for energy density optimisation at scale.

Producers without proprietary electrolytic process technology are responding by deepening long-term supply agreements with electric vehicle platform programmes, investing in surface treatment and anti-oxidation coating capabilities that differentiate product performance in high-temperature battery cycling environments, and expanding manufacturing capacity in markets where domestic content requirements under the US Inflation Reduction Act and EU Battery Regulation create regulatory incentives for locally produced battery materials.

The Major Players In The Industry

- Chang Chun Group

- Furukawa Electric Co. Ltd.

- JX Advanced Metals Corporation

- Londian Wason (Shenzhen) Holdings Group Co., Ltd.

- Lotte Energy Materials Corporation

- Mitsui Mining & Smelting Co. Ltd.

- Nippon Denkai, Ltd

- Rogers Corporation

- Schlenk

- SK Nexilis

- Sumitomo Metal Mining Co., Ltd.

- Targray

- UACJ Foil Corporation

- Other Key Players

Key Development

- In May 2026, JX Advanced Metals Corporation, Mitsui Mining and Smelting Co. Ltd., and Marubeni Corporation executed a definitive agreement to integrate Mitsubishi Materials Corporation’s copper concentrates procurement and product sales into Pan Pacific Copper Co. Ltd., Japan’s largest refined copper supplier, consolidating upstream raw material sourcing to reduce costs and streamline sales operations across the combined entity’s copper value chain.

- In March 2026, SK Nexilis presented next-generation copper foil technologies at InterBattery 2026 in Seoul, including materials designed for solid-state and lithium-metal batteries, along with high-adhesion foil compatible with dry electrode processing. These developments are being positioned for early-stage commercial qualification rather than prototype research, targeting future EV and energy storage platforms. The move strengthens SK Nexilis’s position in next-generation battery supply chains by enabling early design-in positioning, where material selection is locked in before mass production begins, creating long-term structural supply advantages.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$9.3 Bn |

| Forecast Revenue (2035) | US$24.2 Bn |

| CAGR (2026-2035) | 10.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Electrodeposited, Rolled, and Others), By Application (Printed Circuit Boards, Batteries, Electromagnetic Shielding, and Others), By End Use Industry (Aerospace and Defense, Automotive, Building and Construction, Electrical and Electronics, Industrial Equipment, Medical, and Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Chang Chun Group, Furukawa Electric Co. Ltd., JX Advanced Metals Corporation, Londian Wason (Shenzhen) Holdings Group, Lotte Energy Materials Corporation, Mitsui Mining & Smelting Co. Ltd., Nippon Denkai, Ltd, Rogers Corporation, Schlenk, SK Nexilis, Sumitomo Metal Mining Co., Ltd., Targray, UACJ Foil Corporation, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |