Global Zygomatic and Pterygoid Implants Market By Material Type (Titanium Implants and Zirconia Implants), By Application (Maxillary Bone Loss, Severe Alveolar Atrophy, Maxillary Sinuses and Other Applications), By End User (Hospitals, Dental Clinics, Ambulatory Surgical Centers, Academic Institutions and Others), By Distribution Channel (Direct Sales, Dental Distributors and Online Channel), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 182260

- Number of Pages: 318

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

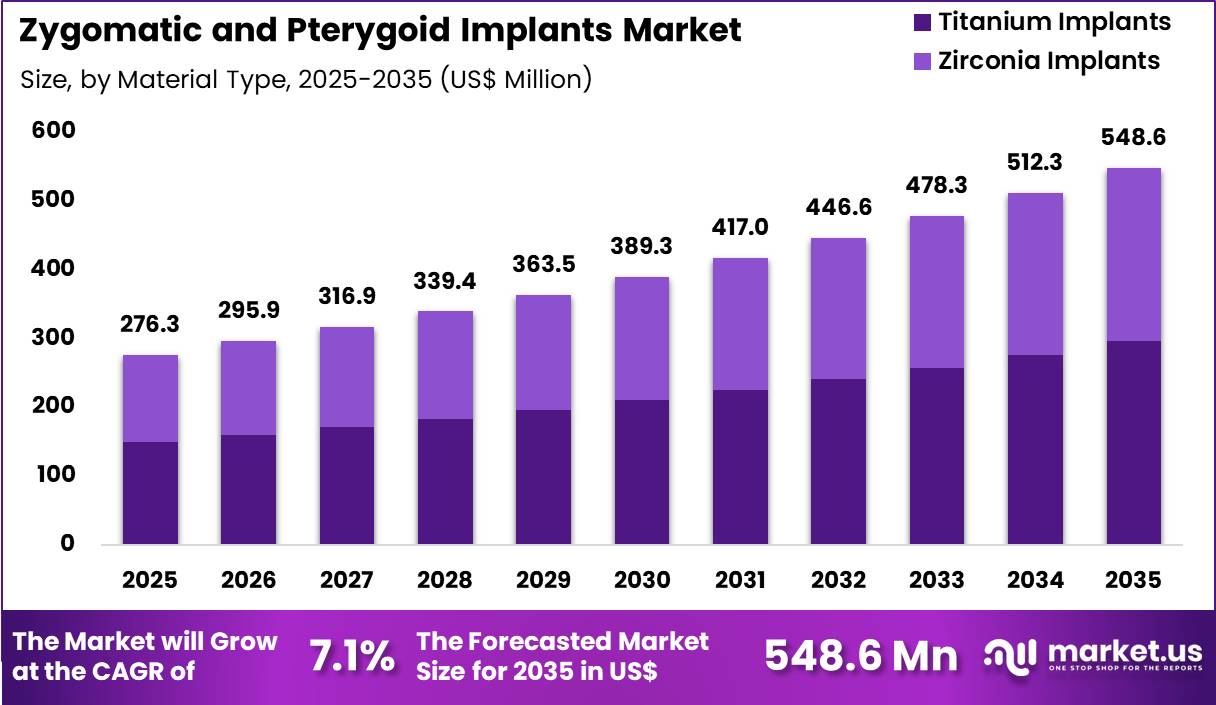

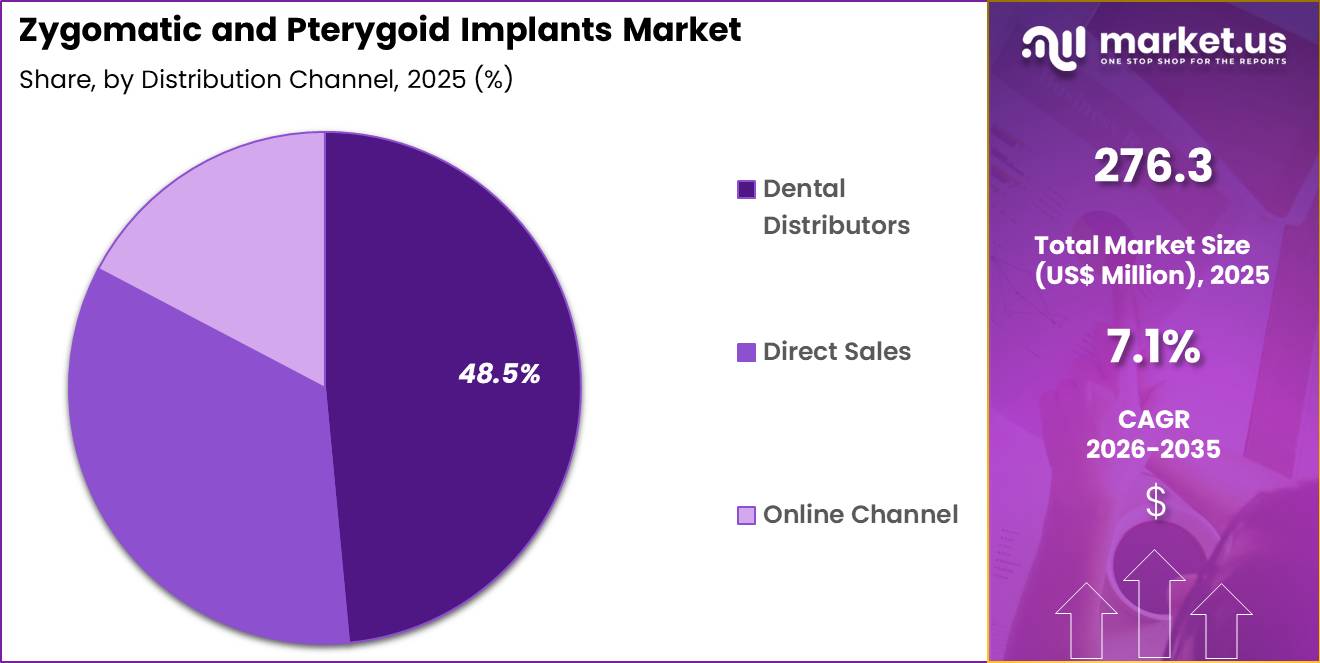

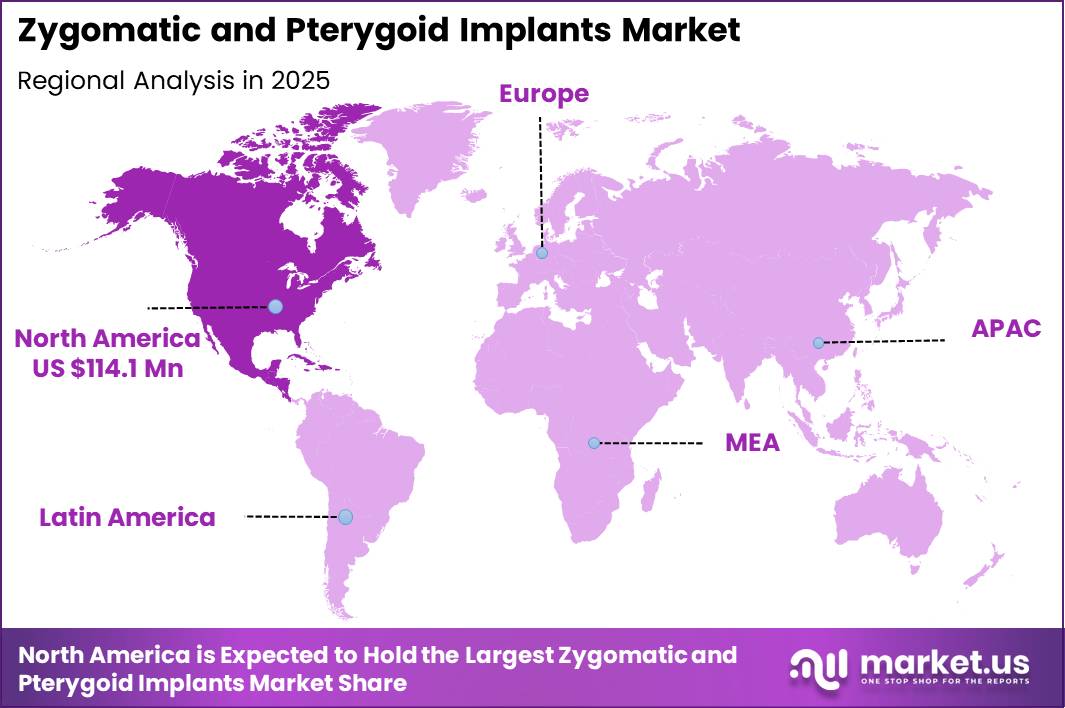

The Global Zygomatic and Pterygoid Implants Market size is expected to be worth around US$ 548.6 Million by 2035 from US$ 276.3 Million in 2025, growing at a CAGR of 7.1% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 41.3% share with a revenue of US$ 114.1 Million.

Rising prevalence of severe maxillary atrophy and edentulism in aging populations accelerates the Zygomatic and Pterygoid Implants market as oral surgeons and prosthodontists seek reliable alternatives to traditional grafting for full-arch rehabilitation in compromised bone scenarios.

Surgeons increasingly place zygomatic implants in the posterior maxilla to anchor fixed prostheses in patients with extensive bone resorption following long-term denture use or failed conventional implants, bypassing the need for sinus lifts or bone augmentation procedures.

These implants support immediate loading protocols in edentulous cases, where clinicians anchor tilted zygomatic fixtures to achieve primary stability and deliver provisional restorations on the same day, reducing treatment time and improving patient satisfaction. Pterygoid implants find application in posterior maxillary reconstruction, engaging the pterygomaxillary junction to provide distal support for hybrid prostheses when anterior bone availability remains limited.

In combination cases, surgeons utilize both zygomatic and pterygoid implants to restore complete maxillary arches without grafting, enabling fixed rehabilitation in patients previously deemed unsuitable for implant therapy due to severe pneumatization or bone deficiency. These approaches also facilitate rehabilitation in oncology patients following maxillectomy, restoring occlusal function and facial aesthetics through anchored prosthetic solutions.

Manufacturers pursue opportunities to refine implant designs with improved thread patterns and surface treatments that enhance primary stability and long-term osseointegration in low-density posterior bone, expanding applications in immediate-function protocols for high-risk patients. These advancements support guided surgery workflows that incorporate patient-specific anatomy for precise angulation and depth control, reducing sinus membrane perforation risks.

Opportunities emerge in digital planning software that simulates zygomatic and pterygoid trajectories, optimizing prosthesis design and load distribution. Companies invest in minimally invasive instrumentation and angled abutments that accommodate anatomical variations and improve prosthetic emergence profiles.

In September 2025, Southern Implants published three-year clinical follow-up data on its ZAGA approach, which adapts implant placement to individual patient anatomy. The results demonstrated high success rates and supported the effectiveness of anatomy-guided techniques in reducing complications associated with sinus involvement.

Dentsply Sirona announced plans to host its Implant Solutions World Summit in June 2026 in Gothenburg, Sweden. The event will highlight new clinical protocols designed for immediate loading in patients with severe maxillary bone loss, emphasizing evidence-based approaches to complex implant rehabilitation.

Recent trends focus on anatomy-guided placement, immediate loading, and digital integration, positioning the market for growth in graftless, patient-specific full-arch solutions that enhance predictability and patient acceptance in advanced maxillary rehabilitation.

Key Takeaways

- In 2025, the market generated a revenue of US$ 276.3 Million, with a CAGR of 7.1%, and is expected to reach US$ 548.6 Million by the year 2035.

- The material type segment is divided into titanium implants and zirconia implants, with titanium implants taking the lead with a market share of 53.9%.

- Considering application, the market is divided into maxillary bone loss, severe alveolar atrophy, maxillary sinuses and other applications. Among these, maxillary bone loss held a significant share of 55.1%.

- Furthermore, concerning the end user segment, the market is segregated into hospitals, dental clinics, ambulatory surgical centers, academic institutions and others. The dental clinics sector stands out as the dominant player, holding the largest revenue share of 58.6% in the market.

- The distribution channel segment is segregated into direct sales, dental distributors and online channel, with the dental distributors segment leading the market, holding a revenue share of 48.5%.

- North America led the market by securing a market share of 41.3%.

Material Type Analysis

Titanium implants accounted for 53.9% of growth within material type and dominate the zygomatic and pterygoid implants market because clinicians continue to prioritize long clinical history, mechanical strength, and predictable osseointegration in complex maxillary restorations. FDI states that the majority of dental implants in use today are made of titanium or titanium alloy, which reflects the material’s entrenched position in implant dentistry.

Titanium surfaces support bone anchorage and biomechanical stability, and published literature continues to identify surface engineering as a major reason for rapid and reliable integration in oral implantology. This advantage becomes especially important in zygomatic and pterygoid procedures, where implant placement often involves long fixtures, high insertion stability, and demanding anatomical pathways.

Surgeons prefer titanium systems because they are widely available across premium and mid-tier product portfolios and because training pathways, surgical kits, and prosthetic components are already optimized around titanium-based workflows.

The burden of oral disease also continues to support demand. WHO reports that oral diseases affected 3.5 billion people globally in 2019, while complete tooth loss affected about 350 million people and severe periodontal disease affected 1 billion people. These conditions increase the pool of patients who later require advanced implant-supported rehabilitation.

Titanium implants are expected to maintain leadership as clinicians seek durable fixation, favorable load distribution, and strong long-term restorative confidence. Ongoing advances in surface modification, corrosion resistance, and antimicrobial enhancement are projected to further support segment growth in demanding full-arch and atrophic maxilla cases.

Application Analysis

Maxillary bone loss accounted for 55.1% of growth within application and dominates the zygomatic and pterygoid implants market because these implants directly address severe posterior maxillary resorption where conventional implants often face inadequate anchorage.

WHO notes that tooth loss represents the end point of major oral diseases, and the global prevalence of complete tooth loss reaches almost 7% among adults aged 20 years or older and about 23% among people aged 60 years or older. Severe periodontal disease also causes destruction of supporting tissues and bone, which contributes to functional maxillary deficiency and raises the need for advanced rehabilitation.

Zygomatic and pterygoid implants are particularly relevant in these cases because they allow surgeons to bypass insufficient alveolar bone and use denser anatomical structures for support. Clinical literature continues to describe zygomatic implants as an effective solution for severely atrophic maxillae and as an option that helps avoid extensive grafting in selected patients.

This treatment pathway appeals to providers because it shortens rehabilitation time, reduces dependence on multistage grafting, and supports full-arch restoration in patients with advanced bone loss. Demand is anticipated to increase further as aging populations, chronic periodontal disease, edentulism, and long-term denture wear continue to drive resorption of the upper jaw.

The segment is also likely to benefit from wider use of CBCT-based planning, guided surgery, and full-arch digital prosthetic workflows, which improve case selection and surgical precision in anatomically compromised maxillary cases.

End User Analysis

Dental clinics accounted for 58.6% of growth within end user and dominate the zygomatic and pterygoid implants market because they serve as the primary point of care for implant consultations, treatment planning, prosthetic rehabilitation, and long-term follow-up. Most implant cases begin in specialized dental settings rather than general hospitals, especially when treatment depends on imaging review, occlusal assessment, prosthetic design, and staged restorative management.

FDI represents more than one million dentists worldwide, which highlights the scale and central role of dental professionals in global oral care delivery. Dental clinics increasingly invest in cone beam imaging, digital impressions, surgical planning software, and chairside restorative coordination, which strengthens their ability to handle advanced implant workflows.

These facilities also offer greater scheduling flexibility, stronger continuity of care, and closer patient engagement throughout surgical and prosthetic phases. For edentulous and severely atrophic patients, treatment often requires repeated assessments, provisionalization, hygiene maintenance, and prosthetic adjustments, all of which align well with clinic-based care models.

Rising patient preference for specialized oral rehabilitation centers is expected to reinforce this trend. Dental clinics are projected to retain their lead as implantologists and oral surgeons expand full-arch service lines and as referral networks between general dentists, prosthodontists, and surgical specialists become more structured.

Growing awareness of fixed alternatives to removable dentures is also likely to support higher procedural volumes at dental clinics, particularly in urban and private practice markets where advanced implant services are more accessible.

Distribution Channel Analysis

Dental distributors accounted for 48.5% of growth within distribution channel and dominate the zygomatic and pterygoid implants market because they provide the broadest reach across clinics, hospitals, and specialist implant centers while simplifying procurement of high-value surgical systems. These procedures rely on more than the implant fixture alone.

Providers require drills, prosthetic parts, angled abutments, surgical guides, kits, biomaterials, and compatible restorative components. Distributors create value by bundling these products, maintaining inventory, and offering technical coordination across multiple brands and treatment stages. This model is especially important in implant dentistry, where clinicians prioritize timely delivery, product traceability, local training support, and access to replacement parts.

Dental distributors also help manufacturers penetrate fragmented provider networks without building a direct sales force in every geography. Their local relationships with oral surgeons, prosthodontists, and dental clinics are expected to remain a major competitive advantage.

The segment is likely to expand as product portfolios become more specialized and as providers seek dependable channel partners for premium implant systems used in anatomically complex maxillary cases. Distributors often support workshops, clinical education, and live case training, which further improves product adoption in advanced procedures such as zygomatic and pterygoid implantation.

As procedural complexity rises and inventory management becomes more critical, distributor-led supply chains are projected to remain the most efficient and scalable route to market for this category.

Key Market Segments

By Material Type

- Titanium Implants

- Zirconia Implants

By Application

- Maxillary Bone Loss

- Severe Alveolar Atrophy

- Maxillary Sinuses

- Other Applications

By End User

- Hospitals

- Dental Clinics

- Ambulatory Surgical Centers

- Academic Institutions

- Others

By Distribution Channel

- Direct Sales

- Dental Distributors

- Online Channel

Drivers

Rising demand for graftless solutions in severe maxillary atrophy cases is driving the market.

Zygomatic and pterygoid implants enable full-arch rehabilitation without bone grafting in patients with extreme maxillary resorption. Surgeons select these options to avoid donor site morbidity and extended healing periods associated with traditional grafting.

The driver supports immediate loading protocols that restore function and esthetics within days of surgery. Practices report higher patient acceptance rates for graftless approaches in edentulous cases. The trend aligns with increased referrals from general dentists to specialists for advanced implant solutions.

Enhanced primary stability in zygomatic bone facilitates predictable outcomes in compromised anatomy. Providers integrate these implants into hybrid protocols combining conventional and advanced anchorage. The expansion reflects growing expertise in extra-maxillary placement techniques. Facilities achieve reduced treatment timelines through streamlined surgical workflows. This factor sustains consistent clinical adoption of specialized anchorage systems.

Restraints

Limited long-term comparative data for pterygoid configurations is restraining the market.

Pterygoid implants lack extensive multi-center studies documenting survival beyond five years compared to zygomatic alternatives. Surgeons exercise caution when recommending pterygoid anchorage in complex cases due to variable bone quality in the pterygoid plate. The restraint slows broader protocol standardization across implant centers.

Manufacturers face challenges demonstrating superiority in prospective trials for regulatory expansions. The factor contributes to selective use restricted to highly experienced operators. Practices prioritize zygomatic options with more established evidence bases.

The dynamic moderates demand for dedicated pterygoid instrumentation and training programs. Providers encounter insurance reimbursement hurdles for less-documented techniques. This constraint limits market velocity in emerging application segments. The limitation persists in influencing adoption patterns among conservative surgical teams.

Opportunities

Development of hybrid zygomatic-pterygoid protocols is creating growth opportunities.

Clinicians combine zygomatic and pterygoid anchorage in quad-implant configurations to achieve balanced load distribution in severely atrophic maxillae. These hybrid approaches enable immediate provisionalization with enhanced biomechanical stability. Opportunities arise for customized treatment planning software tailored to mixed anchorage designs.

The framework supports reduced cantilever lengths and improved prosthesis longevity. Developers gain capacity to refine surgical guides for precise extra-maxillary placement. The development facilitates training modules for combined techniques in advanced education programs. Such protocols attract referrals from prosthodontists seeking graftless full-arch solutions.

The opportunity fosters collaboration between implant manufacturers and digital planning providers. Stakeholders anticipate expanded indications through accumulated clinical outcomes. This advancement positions participants for innovation in complex rehabilitation cases.

Impact of Macroeconomic / Geopolitical Factors

Zygomatic and pterygoid implants serve complex maxillary cases, and economic signals directly shape how dental surgeons and clinics plan these high-value procedures. Cost inflation lifts prices for titanium, precision machining, and sterile packaging, which raises implant and surgical kit expenses. Expensive credit reduces clinic appetite for inventory builds and advanced surgical equipment tied to these procedures.

Cross-border tensions complicate sourcing of specialty alloys, cutting tools, and guided surgery components, which introduces delivery risk. Current US tariffs on imported dental implants, instruments, and metal inputs increase landed costs and pressure distributor pricing strategies. These factors can postpone elective treatments in price-sensitive patient segments and slow case volumes in smaller practices.

At the same time, manufacturers expand regional production and optimize supply networks to stabilize availability and pricing. Strong clinical demand for graft-free solutions in severe bone loss continues to support a durable and positive market trajectory.

Latest Trends

FDA clearance for NobelZygoma TiUltra implant system is driving the market.

The U.S. Food and Drug Administration granted 510(k) clearance for the NobelZygoma TiUltra implant system on August 25, 2025. This approval covers both 0° and 45° angulated variants with TiUltra surface technology for extra-maxillary placement. The clearance validates indications for severe maxillary resorption cases requiring zygomatic anchorage.

Surgeons gain access to advanced anodized implants supporting immediate loading when primary stability is achieved. The 2025 regulatory milestone aligns with demands for optimized surface characteristics in atrophic bone. Facilities benefit from expanded prosthetic compatibility with multi-unit abutments.

The development stimulates integration with existing navigation and guided surgery workflows. Early adopters report consistent performance in hybrid full-arch reconstructions. The clearance facilitates broader availability through established distribution networks. Overall, this advancement elevates treatment predictability and accessibility for graftless maxillary rehabilitation.

Regional Analysis

North America is leading the Zygomatic and Pterygoid Implants Market

North America accounted for 41.3% of the zygomatic and pterygoid implants market in 2025 as oral surgeons and implant specialists increasingly adopted advanced solutions for patients with severe maxillary bone loss. Dental clinics across the United States and Canada expanded use of these implants to avoid complex bone grafting procedures and enable immediate loading protocols in edentulous patients.

According to the Centers for Disease Control and Prevention, about 26% of adults aged 65 years and older in the United States had lost all their natural teeth in recent years, highlighting a significant patient base requiring full-arch rehabilitation solutions. Growing geriatric population and rising prevalence of periodontal disease have therefore increased demand for alternative implant techniques that provide stability in cases of limited bone structure.

Oral and maxillofacial surgeons are increasingly performing advanced implant procedures supported by digital planning and guided surgery technologies. Dental service organizations are also expanding full-arch rehabilitation programs that rely on complex implant placement techniques.

Technological advancements in implant design, surface treatment, and surgical navigation have improved clinical success rates and reduced recovery time. Training programs and continuing education in implantology are enhancing clinician expertise in advanced procedures.

These developments collectively supported strong growth of complex dental implant solutions across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to witness strong expansion during the forecast period as dental healthcare infrastructure improves and awareness of advanced implantology increases across emerging economies. Countries such as China, India, Japan, and South Korea are expanding dental clinics and specialized implant centers to address rising demand for restorative dental treatments.

The World Health Organization reported in 2022 that severe periodontal disease affects around 19% of the global adult population, creating a large pool of patients who may require advanced tooth replacement solutions. Growing middle-class income and increasing focus on dental aesthetics are encouraging patients to seek long-term restorative treatments rather than removable prosthetics.

Dental professionals across the region are adopting advanced surgical techniques that enable treatment of patients with significant bone loss without extensive grafting procedures. Governments and private healthcare providers are investing in dental education and training programs that strengthen expertise in complex implant procedures.

International dental technology companies are expanding their presence in Asia through partnerships with local clinics and training institutes. Digital dentistry tools such as 3D imaging and guided surgery systems are improving treatment precision and patient outcomes. These developments are expected to accelerate adoption of advanced implant solutions across Asia Pacific in the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the Zygomatic and Pterygoid Implants market expand their footprint by advancing long-length implant designs, strengthening surgical training programs, and collaborating with maxillofacial specialists to improve outcomes in complex bone loss cases. Companies invest in surface modification technologies and high-strength biomaterials that enhance osseointegration and long-term stability in challenging anatomical conditions.

They also broaden global distribution and conduct clinician education initiatives to increase adoption of advanced implant techniques in full-arch restorations. Nobel Biocare represents a prominent participant in the Zygomatic and Pterygoid Implants market and operates as a Switzerland-based dental implant company that develops innovative implant systems, prosthetics, and digital dentistry solutions for dental professionals worldwide.

The company focuses on research-driven implant design and digital workflow integration to support complex rehabilitation procedures. Industry competitors continue to introduce specialized implant systems, expand clinical collaborations, and invest in digital planning tools to strengthen adoption and improve surgical precision.

Top Key Players

- Straumann Holding AG

- Dentsply Sirona Inc.

- Southern Implants

- Noris Medical

- S.I.N. Implant System

- Bioline Dental Implants

- B&B Dental Implant Company

- IDC Implant and Dental Company

- Megagen Implant Co., Ltd.

Recent Developments

- In March 2026, Straumann entered into a strategic collaboration with Malo Clinic to advance full-arch rehabilitation solutions. The partnership centers on combining the Straumann Pro Arch Zygomatic system with a digital workflow approach, enabling faster treatment timelines and supporting same-day or next-day restoration in complex edentulous cases.

- In March 2026, Noris Medical presented its PATZI protocol at the Academy of Osseointegration, focusing on advanced remote anchorage techniques such as pterygoid, transnasal, and zygomatic implants. The company is expanding hands-on training programs, including cadaver-based workshops, to improve surgical proficiency in these highly specialized implant procedures.

Report Scope

Report Features Description Market Value (2025) US$ 276.3 Million Forecast Revenue (2035) US$ 548.6 Million CAGR (2026-2035) 7.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Material Type (Titanium Implants and Zirconia Implants), By Application (Maxillary Bone Loss, Severe Alveolar Atrophy, Maxillary Sinuses and Other Applications), By End User (Hospitals, Dental Clinics, Ambulatory Surgical Centers, Academic Institutions and Others), By Distribution Channel (Direct Sales, Dental Distributors and Online Channel) Regional Analysis North America – The US, Canada; Europe – Germany, France, The U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America Competitive Landscape Straumann Holding AG, Dentsply Sirona Inc., Southern Implants, Noris Medical, S.I.N. Implant System, Bioline Dental Implants, B&B Dental Implant Company, IDC Implant and Dental Company, Megagen Implant Co., Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Zygomatic and Pterygoid Implants MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Zygomatic and Pterygoid Implants MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Straumann Holding AG

- Dentsply Sirona Inc.

- Southern Implants

- Noris Medical

- S.I.N. Implant System

- Bioline Dental Implants

- B&B Dental Implant Company

- IDC Implant and Dental Company

- Megagen Implant Co., Ltd.

Our Clients

- 182260

- March 2026