Quick Navigation

Report Overview

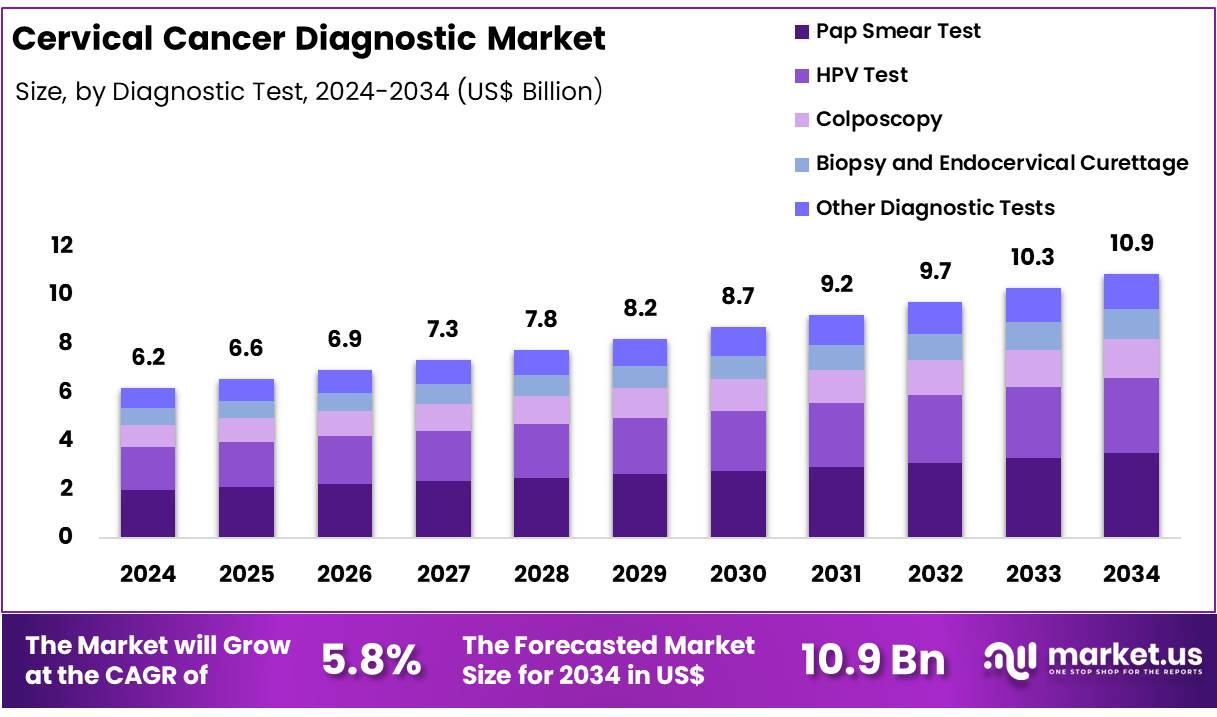

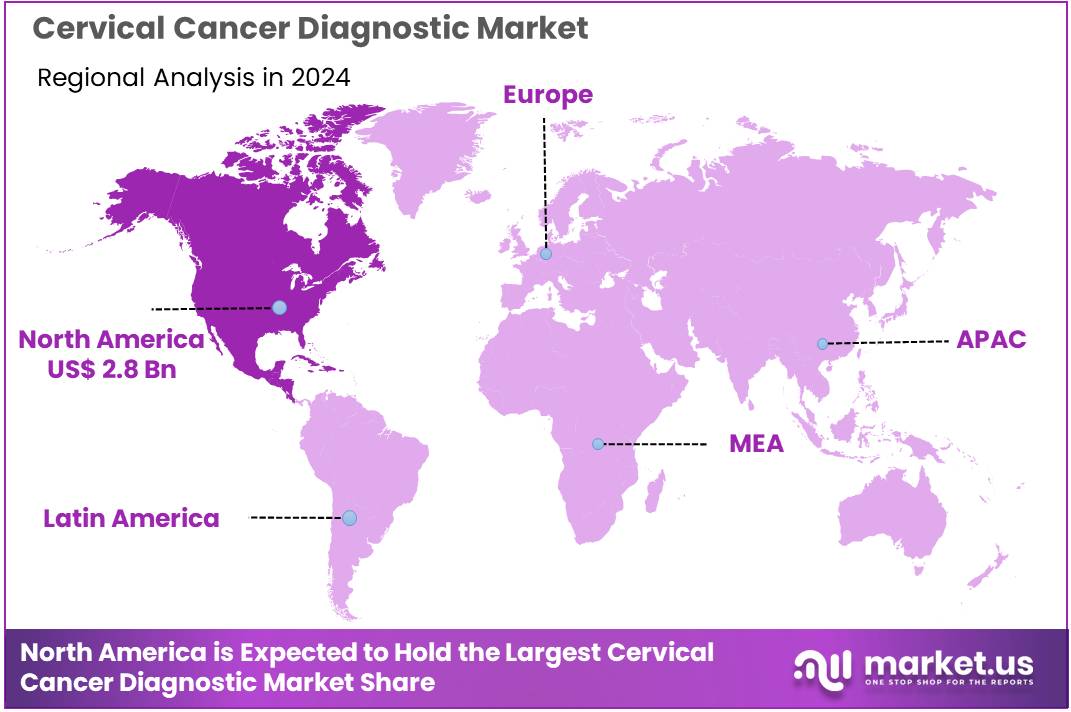

Global Cervical Cancer Diagnostic Market size is expected to be worth around US$ 10.9 Billion by 2034 from US$ 6.2 Billion in 2024, growing at a CAGR of 5.8% during the forecast period from 2025 to 2034. In 2024, North America led the market, achieving over 45.6% share with a revenue of US$ 2.8 Billion.

The cervical cancer burden remains substantial. Globally, it is the fourth most common cancer in women, with approximately 660 000 new cases and 350 000 deaths reported in 2022. The highest incidence and mortality rates are observed in low- and middle-income countries, reflecting gaps in access to preventive services and screening. Early detection through regular screening is critical, as cervical cancer can be cured when identified at a precancerous stage.

A novel diagnostic assay has been developed to streamline screening workflows. The test integrates automated image analysis with high-throughput sequencing, requiring only a simple cervical swab. Results are delivered within 48 hours, enabling rapid follow-up in both urban and low-resource settings. The ease of use and quick turnaround can support national screening initiatives and improve participation rates.

Regulatory clearance has been secured in major markets. U.S. Food and Drug Administration approval and CE marking by the European Commission have been granted, and commercial distribution is slated to begin in Q3 2025. Training programs for laboratory technicians and clinical staff are being organized in partnership with public health agencies to ensure proper implementation and quality control across testing sites.

Market growth is expected to accelerate with the introduction of new vaccines and molecular tests. In September 2022, India’s Drugs Controller General granted market authorization for CERVAVAC—the first indigenously developed quadrivalent HPV vaccine—at an affordable price point of INR 200–400 per dose. Similarly, in June 2022, Karkinos Healthcare launched CerviRaksha, a WHO-prequalified, FDA-approved HPV DNA test priced at INR 2 499 and capable of high-risk HPV type identification. These developments are expected to expand access to both prevention and early detection, driving the cervical cancer diagnostics and therapeutics market forward.

Key Takeaways

- Market Size: Global Cervical Cancer Diagnostic Market size is expected to be worth around US$ 10.9 Billion by 2034 from US$ 6.2 Billion in 2024.

- Market Growth: The market growing at a CAGR of 5.8% during the forecast period from 2025 to 2034.

- Diagnostic Test Analysis: The Pap smear test segment dominated with 32.1% market share in 2024.

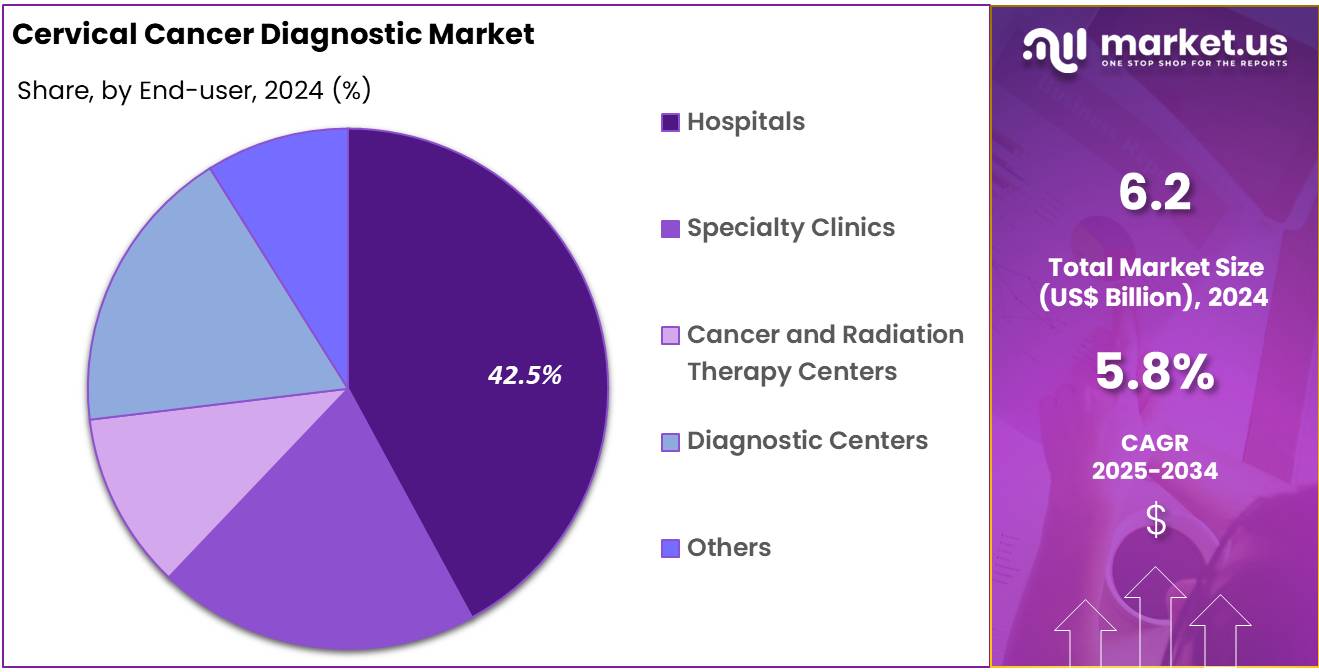

- End User Analysis: The hospitals segment dominated with a 42.5% share.

- Regional Analysis: In 2024, North America held a dominant market position, capturing more than a 45.6% share and holds US$ 2.8 billion market value for the year.

Diagnostic Test Analysis

The cervical cancer diagnostic market is segmented by test type: Pap smear, HPV test, colposcopy, biopsy and endocervical curettage (ECC), and other diagnostic procedures. The Pap smear test segment dominated with 32.1% market share, attributed to widespread adoption in routine screening and established reimbursement policies. The HPV test segment held around 28.0%, driven by guideline endorsements for primary HPV screening and its higher sensitivity for high-risk viral strains.

The colposcopy segment accounted for approximately 15.0% share, serving as a confirmatory procedure for abnormal screening outcomes. Biopsy and ECC together represented about 12.0%, reflecting their use in histopathological evaluation and lesion characterization. Other diagnostic tests, including liquid-based cytology and emerging molecular assays, comprised the remaining 12.9%, propelled by technological innovation and regulatory approvals. Market expansion has been supported by increasing national screening initiatives, favorable policy frameworks, and continued improvements in diagnostic accuracy.

End User Analysis

The end-user segmentation of the global cervical cancer diagnostics market is divided into hospitals, specialty clinics, cancer and radiation therapy centers, diagnostic centers, and others. The hospitals segment dominated with a 42.5% share, driven by established infrastructure, routine screening programs, and integrated patient-care pathways.

The specialty clinics segment accounted for approximately 24.3%, supported by focused gynecological services and expanding outpatient screening initiatives. Cancer and radiation therapy centers held around 17.2%, reflecting their role in advanced diagnostic evaluation and treatment planning for confirmed cases. Diagnostic centers captured roughly 11.0%, owing to increased patient preference for standalone facilities offering rapid test results and streamlined appointment systems.

The remaining 5.0% was contributed by other end users, including community health centers. Growth across all segments has been supported by initiatives to extend screening coverage, enhancements in reimbursement frameworks, and the adoption of point-of-care testing. Regional screening guidelines and public-health policies have further influenced end-user preferences, with hospitals and specialty clinics remaining the primary hubs for diagnostic test administration. Continued investment in outpatient and decentralized diagnostic models is expected to reshape segment dynamics over the forecast period.

Key Market Segments

By Diagnostic Test

- Pap Smear Test

- HPV Test

- Colposcopy

- Biopsy and Endocervical Curettage

- Other Diagnostic Tests

By End-user

- Hospitals

- Specialty Clinics

- Cancer and Radiation Therapy Centers

- Diagnostic Centers

- Others

Driving Factors

The growth of the cervical cancer diagnostic market can be attributed to the expansion of national screening initiatives and rising disease burden. Each year in the United States, approximately 11,500 new cases of cervical cancer are diagnosed, with nearly 4,000 deaths reported, underscoring the need for early detection and intervention.

Government programs such as the National Breast and Cervical Cancer Early Detection Program (NBCCEDP) have increased access by serving 6.8% of eligible women aged 21–64 between 2015 and 2017, though gaps remain. These coordinated efforts drive demand for a range of diagnostic modalities—including Pap smears, HPV testing, and colposcopy—fueling market expansion and public health impact.

Trending Factors

A clear shift toward HPV-based testing and at-home sample collection is reshaping the diagnostic landscape. Molecular HPV assays are increasingly replacing cytology as the primary screening tool, owing to higher sensitivity for high-risk viral strains. In May 2025, the U.S. Food and Drug Administration approved the first at-home cervical cancer screening kit, enabling self-collection of vaginal samples with clinical-grade accuracy.

This trend supports greater patient convenience and privacy, while reducing the clinical workload. Concurrently, integration of high-throughput sequencing and automated image analysis is accelerating result turnaround and standardizing interpretation.

Restraining Factors

Market growth is constrained by uneven screening coverage and infrastructure challenges in underserved regions. Despite the NBCCEDP’s efforts, only 6.8% of income-eligible women accessed cervical cancer screening services between 2015 and 2017, indicating persistent access gaps. Rural, uninsured, and minority populations often face barriers such as limited healthcare facilities, shortage of trained cytotechnologists, and low awareness of screening guidelines.

Additionally, inconsistent reimbursement policies for advanced molecular tests may hinder uptake, particularly in low-resource settings. These factors can slow adoption of novel diagnostics and undermine efforts to achieve population-wide screening targets.

Opportunity

Emerging diagnostic technologies and expanded programmatic support present significant market opportunities. The FDA’s recent approval of self-sampling kits has demonstrated that home-based HPV testing yields performance comparable to clinician-collected samples in clinical studies. Moreover, advances in point-of-care molecular assays and next-generation sequencing facilitate rapid detection of high-risk HPV genotypes and precancerous lesions, supporting decentralized screening models.

Integration of AI-driven cytology platforms promises to enhance accuracy and reduce interpretive variability. With renewed emphasis on cervical cancer elimination strategies by global health authorities, investment in these innovations could accelerate market uptake and improve screening equity.

Regional Analysis

In 2024, North America held a dominant market position, capturing more than a 45.6% share and holds US$ 2.8 billion market value for the year. This strong position is due to high awareness, early screening programs, and strong healthcare infrastructure. The region benefits from widespread adoption of diagnostic technologies like HPV testing and Pap smear screening.

The United States leads the market within North America. This is supported by government-backed cervical cancer prevention initiatives, such as the CDC’s National Breast and Cervical Cancer Early Detection Program (NBCCEDP). These efforts help increase access to screening among underserved populations.

Canada also contributes to regional growth. The country’s healthcare system covers preventive screenings under public insurance. This ensures high participation rates among women aged 25 to 69, the most affected age group for cervical cancer.

North America’s market dominance is further reinforced by the region’s high healthcare spending per capita. According to World Bank data, the U.S. spends over 16% of its GDP on healthcare. This enables rapid adoption of advanced diagnostics.

In summary, North America’s lead in the cervical cancer diagnostic market can be attributed to early detection programs, public health initiatives, and advanced infrastructure. These elements continue to support steady growth and early-stage diagnosis, improving survival rates across the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key participants in the cervical cancer diagnostic market are engaged in competitive strategies to strengthen their positions. Their primary focus is on advancing technological innovations, such as next-generation sequencing and automated cytology. Strategic collaborations with healthcare institutions and regulatory bodies have been established to expedite product approvals and broaden clinical adoption.

Geographic expansion into emerging economies has been pursued to capitalize on unmet screening needs. Product portfolios have been diversified to include multiplex assays and point-of-care solutions. Investments in manufacturing capacity have been intensified to ensure cost-effective production.

Marketing strategies emphasize clinician education and patient awareness campaigns. Pricing models are being refined to balance affordability with margin protection. Service and support networks have been enhanced to improve customer satisfaction.

Market Key Players

- Abbott Laboratories

- Aptamer Group, plc

- Becton, Dickinson and Company

- Danaher Corporation

- F. Hoffman-La Roche Ltd.

- Guided Therapeutics, Inc.

- Healthians

- Hologic, Inc.

- MobileODT Ltd

- Novartis AG

- Quest Diagnostics

- Roche Diagnostics

- Timser Group

Recent Developments

- Aptamer Group: In May 2024, Aptamer Group PLC entered into a £465,000 development agreement with Timser Group for its Optimer® binders to be applied in a novel blood-based cervical cancer biomarker panel. Under the terms, Aptamer will supply molecular binding reagents customized to Timser’s three-protein signature test, which promises higher sensitivity than conventional Pap smears.

- Danaher Corporation: In December 2023, Danaher Corporation completed its acquisition of Abcam plc for $5.7 billion in cash, broadening its life sciences and diagnostics portfolio. Abcam, a leading supplier of antibodies, immunoassays, and research reagents, supports numerous molecular platforms—including those used in HPV and cervical cancer testing workflows.

- Guided Therapeutics, Inc.: In December 2024, Guided Therapeutics secured an order and received full payment from Indonesia’s Ministry of Health for four LuViva® Advanced Cervical Scan devices and 1,200 disposable cervical guides.

- Healthians: In February 2024, Healthians entered into discussions to acquire multiple regional diagnostics firms to bolster its service portfolio ahead of a planned initial public offering. These potential acquisitions target specialized laboratories and point-of-care testing networks that complement Healthians’ direct-to-consumer model.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 6.2 Billion |

| Forecast Revenue (2034) | US$ 10.9 Billion |

| CAGR (2025-2034) | 5.8% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Diagnostic Test (Pap Smear Test, HPV Test, Colposcopy, Biopsy and Endocervical Curettage, Other Diagnostic Tests) By End-user (Hospitals, Specialty Clinics, Cancer and Radiation Therapy Centers, Diagnostic Centers, Others) |

| Regional Analysis | North America-US, Canada, Mexico;Europe-Germany, UK, France, Italy, Russia, Spain, Rest of Europe;APAC-China, Japan, South Korea, India, Rest of Asia-Pacific;South America-Brazil, Argentina, Rest of South America;MEA-GCC, South Africa, Israel, Rest of MEA |

| Competitive Landscape | Abbott Laboratories, Aptamer Group, plc, Becton, Dickinson and Company, Danaher Corporation, F. Hoffman-La Roche Ltd., Guided Therapeutics, Inc., Healthians, Hologic, Inc., MobileODT Ltd, Novartis AG, Quest Diagnostics, Roche Diagnostics, Timser Group, |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |