Global Wood Pulp Market Size, Share, And Industry Analysis Report By Type (Hardwood, Softwood), By Grade (Chemical, Mechanical, Semi-Chemical, Others), By End Use (Packaging (Food and Beverages, Pharmaceutical, Personal Care and Cosmetics, Automotive, Others), Paper (Newspaper, Books and Magazines, Tissues, Others), Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 180550

- Number of Pages: 214

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

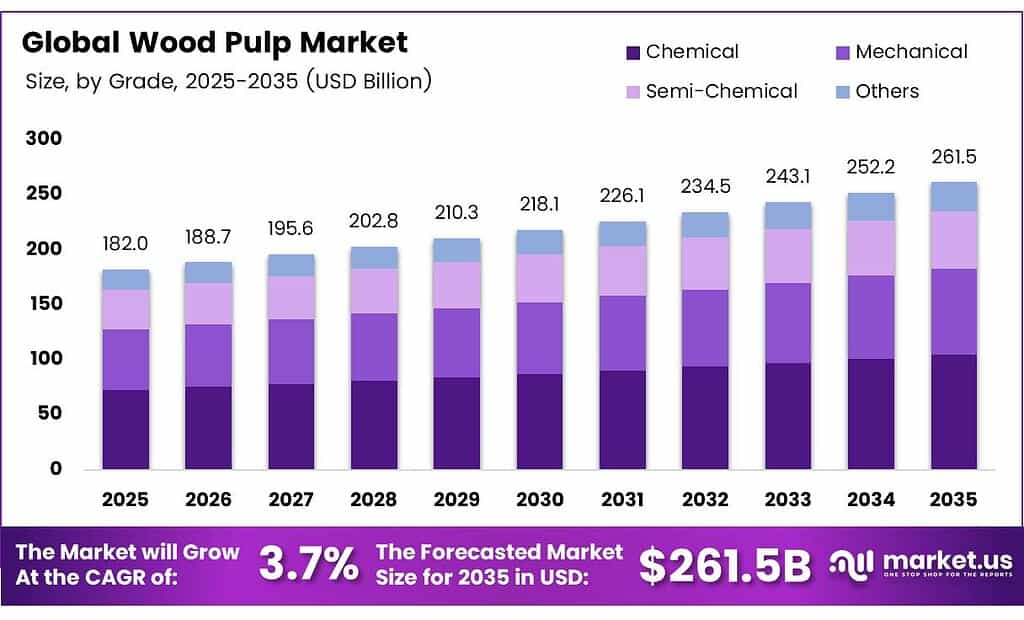

The Global Wood Pulp Market size is expected to be worth around USD 261.5 billion by 2035 from USD 182.0 billion in 2025, growing at a CAGR of 3.7% during the forecast period 2026 to 2035.

Wood pulp is a cellulose-based fibrous material derived from processed wood. Manufacturers use it as a primary raw material for producing paper, packaging materials, hygiene products, and specialty textiles. Its wide industrial applications make it a cornerstone commodity in global supply chains.

The market covers multiple product types, including chemical pulp, mechanical pulp, and semi-chemical pulp. Chemical pulp dominates production due to its superior fiber strength and brightness. Moreover, the growing shift toward sustainable fiber sourcing continues to reshape how producers extract and process raw wood materials globally.

- According to the World Bank WITS, China imported USD 612.161 million of semi-chemical wood pulp in 2024, equal to 1,223,320,000 kg. This volume signals China’s enormous domestic demand for pulp-based materials, reinforcing Asia Pacific’s role as the world’s largest consumption hub for wood fiber products.

Global demand for wood pulp accelerates as packaging, tissue, and specialty applications expand. E-commerce growth drives paper-based packaging consumption sharply upward. Additionally, governments across major producing nations actively support certified forestry programs, which creates a more stable and regulated supply chain for long-term market growth.

- Brazil’s pulp production totaled 25,524 thousand tons in January–December 2024, while pulp exports reached 18,570 thousand tons during the same period. These figures demonstrate Brazil’s critical position as the world’s leading pulp exporter, supplying major markets across Europe, North America, and Asia.

Government policies in North America, Europe, and the Asia Pacific increasingly mandate sustainable sourcing and emissions compliance. These regulations encourage investments in certified pulp production facilities. Consequently, producers upgrade their mill infrastructure and adopt cleaner bleaching technologies to meet evolving environmental standards and maintain access to regulated export markets.

Key Takeaways

- The Global Wood Pulp Market is valued at USD 182.0 billion in 2025 and is projected to reach USD 261.5 billion by 2035, at a CAGR of 3.7% during the forecast period 2026 to 2035.

- Hardwood pulp holds the dominant position with a 61.4% market share in 2025.

- Chemical pulp leads with a 51.7% share, driven by demand for high-strength fiber applications.

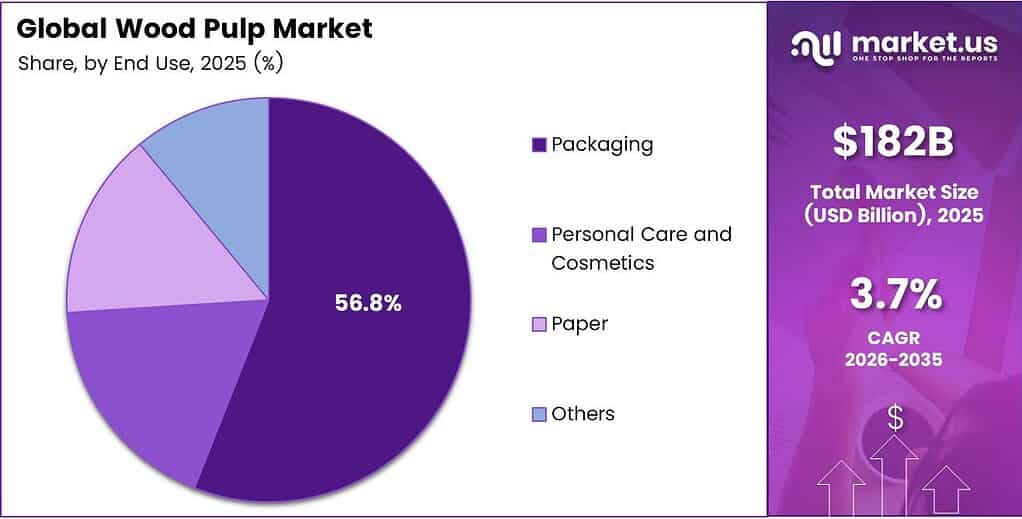

- Packaging captures the largest share at 56.8%, fueled by e-commerce and sustainable packaging trends.

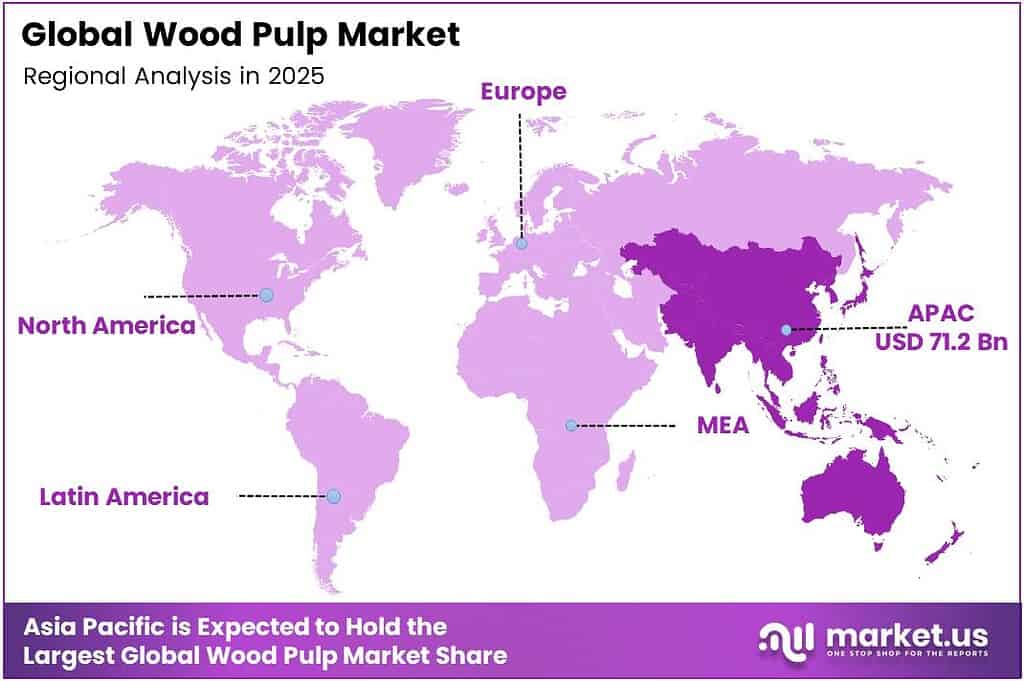

- Asia Pacific dominates the global market with a 39.1% share, valued at USD 71.2 billion.

By Type Analysis

Hardwood pulp dominates with 61.4% due to its widespread use in printing, writing, and tissue paper manufacturing.

In 2025, Hardwood held a dominant market position in the By Type segment of the Wood Pulp Market, with a 61.4% share. Hardwood pulp delivers shorter fibers that produce smooth, high-quality paper surfaces. Moreover, its compatibility with chemical pulping processes makes it a preferred input for tissue, printing, and packaging paper producers worldwide.

Softwood pulp contributes significantly to the global wood pulp market due to its long fiber structure. These long fibers provide superior tensile strength, making softwood pulp essential for producing kraft paper, corrugated boards, and specialty industrial papers. Consequently, softwood pulp remains a critical complement to hardwood in blended paper grades.

By Grade Analysis

Chemical pulp dominates with 51.7% due to superior brightness, strength, and versatility across end-use applications.

In 2025, Chemical pulp held a dominant market position in the by-grade segment of the Wood Pulp Market, with a 51.7% share. Chemical pulping processes remove lignin effectively, producing high-purity, strong fiber suitable for premium paper and packaging. Additionally, its compatibility with bleaching technologies supports demand from hygiene and specialty paper manufacturers globally.

Mechanical pulp serves cost-sensitive applications such as newsprint and catalog paper. It retains most of the wood’s original material, offering a higher yield per unit of raw timber. However, its lower brightness and strength limit its use to applications where cost efficiency outweighs quality requirements, keeping it relevant in print media production.

Semi-Chemical pulp combines chemical and mechanical processing methods to achieve a balance of yield and fiber quality. It finds strong application in fluting and corrugated packaging materials. Furthermore, rising global trade in semi-chemical pulp, particularly between Canada and Asia, underscores growing industrial demand for mid-grade fiber solutions.

Others in the grade segment include dissolving pulp and specialty grades used in textiles, films, and pharmaceutical applications. These niche grades attract premium pricing and growing investment as producers diversify beyond traditional paper markets. Consequently, specialty pulp demand adds a high-value growth layer to the overall wood pulp industry.

By End Use Analysis

Packaging dominates with 56.8% due to surging e-commerce demand for sustainable paper-based packaging solutions.

In 2025, Packaging held a dominant market position in the By End Use segment of the Wood Pulp Market, with a 56.8% share. The global expansion of e-commerce and retail logistics drives demand for corrugated boxes, cartons, and paper wrapping. Moreover, brands actively replace plastic packaging with pulp-based alternatives to meet sustainability and regulatory targets.

Within packaging, Food and beverage applications consume a significant share of pulp-based materials. Food-safe paperboard, liquid packaging, and food wraps require high-purity pulp grades. Additionally, Pharmaceutical packaging demands specialized, contamination-free pulp for blister packs and medicine cartons, creating a growing premium segment within pulp end-use markets.

Personal Care and Cosmetics packaging rely on pulp for boxes, inserts, and sustainable wrapping. The shift away from plastic in personal care drives volume. Meanwhile, Automotive applications use specialty pulp composites in interior components, reflecting broader material substitution trends as manufacturers seek lighter, greener alternatives to synthetic materials.

The Paper segment remains a core end-use category, covering newspapers, books, magazines, and tissues. Tissue paper demand grows consistently due to rising hygiene awareness globally. Others in end-use include construction paper, specialty industrial applications, and dissolving pulp for textile manufacturing, which collectively contribute to overall market volume diversification.

Key Market Segments

By Type

- Hardwood

- Softwood

By Grade

- Chemical

- Mechanical

- Semi-Chemical

- Others

By End Use

- Packaging

- Food and Beverages

- Pharmaceutical

- Personal Care and Cosmetics

- Automotive

- Others

- Paper

- Newspaper

- Books and Magazines

- Tissues

- Others

- Others

Emerging Trends

Sustainability and Innovation Drive New Directions in Wood Pulp Processing

Chemical wood pulp gains market momentum as manufacturers prioritize fiber strength and product quality. Producers favor chemical pulping over mechanical methods for premium packaging and hygiene applications. Additionally, the adoption of Elemental Chlorine-Free and Totally Chlorine-Free bleaching processes reduces environmental impact and aligns with tightening global regulatory standards for pulp exports.

- Recycled pulp integration accelerates as manufacturers seek alternatives to virgin fiber sources. Mills increasingly blend recovered fiber with fresh pulp to reduce raw material costs and carbon footprints. According to the World Bank WITS, the EU imported US$30.055 million of semi-chemical wood pulp from Canada in 2024, reflecting strong cross-regional trade flows that support fiber diversification strategies.

Bio-refinery integration emerges as a transformative trend in modern pulp mills. Producers extract value-added byproducts such as bioenergy, bio-chemicals, and lignin-based materials alongside traditional pulp output. Consequently, bio-refinery models improve overall mill profitability, reduce waste, and support circular economy goals that increasingly influence procurement decisions among global paper and packaging buyers.

Drivers

Rising Hygiene Awareness and Sustainable Packaging Demand Drive Wood Pulp Market Growth

Global demand for tissue and hygiene products surges as health awareness rises across developed and emerging markets. Consumers increasingly prioritize sanitary paper products for daily use. Moreover, post-pandemic behavior shifts have permanently elevated tissue consumption volumes, driving continuous capacity expansion among pulp producers to meet long-term hygiene product manufacturing requirements.

- According to OEC World, Canada exported US$3.79 billion of sulfate chemical woodpulp in 2024, demonstrating the scale of global trade flows in high-quality chemical pulp. This export volume reflects strong international demand for kraft-grade fiber, particularly from Asia Pacific markets where packaging and tissue manufacturing capacity continues to grow rapidly year over year.

Government policies increasingly support certified forestry and afforestation programs worldwide. Regulatory frameworks in the EU, North America, and Asia promote sustainable wood sourcing and reduce illegal logging. Consequently, certified pulp supply chains attract greater institutional investment and command premium pricing, reinforcing growth in responsibly managed wood fiber production across key producing regions.

Restraints

Regulatory Pressures and Raw Material Volatility Constrain Wood Pulp Market Expansion

Stringent deforestation regulations in the EU and North America raise compliance costs for pulp producers significantly. Companies must invest in certified forestry management systems and emissions monitoring infrastructure. Moreover, evolving environmental laws require continuous operational upgrades, increasing capital expenditure burdens that smaller producers struggle to absorb while maintaining competitive pricing in global markets.

- Mercer International’s full-year Operating EBITDA reached negative US$22.0 million in 2025, illustrating how operational cost pressures can erode profitability across the pulp sector. Rising energy costs and raw material price volatility compound financial strain, particularly for producers operating aging mill infrastructure without the scale needed to offset input cost fluctuations effectively.

Supply chain disruptions caused by volatile timber and energy prices challenge operational planning for wood pulp producers. Price swings in key input materials reduce margin predictability and complicate long-term contract negotiations. Therefore, producers face growing pressure to adopt hedging strategies, diversify fiber sources, and invest in energy efficiency programs to stabilize cost structures.

Growth Factors

Sustainable Capacity Expansion and Technology Integration Accelerate Wood Pulp Market Growth

Expansion of low-carbon certified sustainable pulp production facilities creates new capacity across Latin America, Southeast Asia, and Scandinavia. Producers invest in cleaner mill technologies that reduce water use and carbon emissions. Moreover, certified sustainable pulp commands higher prices in European and North American markets where buyer sustainability commitments drive procurement policy decisions.

- Arauco approved the construction of the Sucuriú project in Brazil with an investment of US$4.6 billion, designed for an annual production capacity of 3.5 million metric tons of dry cellulose. This investment reflects the broader trend of major producers scaling up capacity in fiber-rich emerging markets to meet growing global demand for sustainable wood pulp.

Artificial intelligence adoption for predictive maintenance and forest resource monitoring enhances mill efficiency and reduces unplanned downtime. AI-powered systems optimize fiber yield, chemical usage, and energy consumption across production cycles. Additionally, specialty pulp applications in textiles, bioplastics, and pharmaceuticals create high-value demand segments that expand the market beyond traditional paper and packaging end uses.

Regional Analysis

Asia Pacific Dominates the Wood Pulp Market with a Market Share of 39.1%, Valued at USD 71.2 Billion

Asia Pacific leads the global wood pulp market, holding a dominant 39.1% share valued at USD 71.2 billion. China drives regional demand as the world’s largest importer of wood pulp for paper and packaging production. Moreover, rapid industrialization, growing e-commerce activity, and rising consumer hygiene standards across India, Japan, and Southeast Asia further accelerate regional pulp consumption volumes.

North America maintains a strong position in the global wood pulp market as both a major producer and consumer. The United States and Canada together supply significant volumes of chemical and semi-chemical pulp to domestic and international markets. Additionally, growing tissue manufacturing capacity and sustainable packaging adoption among North American brands continue to support steady regional demand growth.

Europe represents a mature but innovation-driven wood pulp market. Scandinavian countries, particularly Sweden and Finland, lead in certified sustainable pulp production and export. Finland’s pulp and paper industry exports reflect the region’s strong global trade position in high-quality forest industry products.

The Middle East and Africa represent an emerging but growing segment of the global wood pulp market. South Africa hosts notable pulp production capacity through established forestry programs, while regional demand grows alongside packaging and tissue manufacturing investments. However, limited domestic fiber resources and infrastructure constraints temper the near-term expansion pace across many sub-Saharan African markets.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

APRIL Group operates large-scale pulp and paper production facilities across Indonesia and the Asia Pacific. The company focuses on sustainable fiber sourcing and invests continuously in mill efficiency upgrades. Moreover, APRIL Group supplies hardwood pulp to a broad range of international customers across packaging, tissue, and specialty paper markets, strengthening its position as a key regional supplier.

ARAUCO is a leading integrated forestry and pulp company based in Chile with significant global reach. The company manages extensive plantation forestry assets across South America. Reflecting its scale as one of the world’s largest pulp and wood products producers.

Canfor Corporation is a major North American wood products and pulp producer headquartered in Canada. The company operates softwood pulp mills and integrates pulp production with its broader lumber operations. Additionally, Canfor exports significant volumes of kraft pulp to Asian markets, positioning itself as a reliable supplier of long-fiber softwood pulp to global tissue and packaging manufacturers.

Metsä Group is a Finnish forest industry group with strong operations in chemical pulp production. The company prioritizes bio-economy solutions and sustainable forestry practices. Furthermore, Metsä Group’s bioproduct mill concept integrates pulp production with bio-energy and biomaterial outputs, representing a forward-looking model that delivers both environmental and commercial value across its European operations.

Top Key Players in the Market

- APRIL Group

- ARAUCO

- Canfor Corporation

- Metsä Group

- Nippon Paper Industries Co. Ltd

- Oji Holdings Corporation

- Sappi Limited

- Södra

- Stora Enso Oyj

- Suzano Papel e Celulose

Recent Developments

- In 2024, APRIL Group, the integrated mill, produced 3.9 million tonnes of pulp (including 1.9 million tonnes of bleached hardwood kraft pulp and 1.8 million tonnes of dissolving wood pulp), sourced from over 15 million tonnes of wood and fibre (100% traceable and from PEFC-certified/controlled sources).

- In 2025, Metsä Fibre announced a temporary production shutdown at its Joutseno pulp mill. The move adjusts output to uncertain demand, particularly in Asian markets. Restart will depend on ongoing market monitoring. This is the second market-related shutdown at Joutseno in the past nine months.

Report Scope

Report Features Description Market Value (2025) USD 182.0 Billion Forecast Revenue (2035) USD 261.5 Billion CAGR (2026-2035) 3.7% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Hardwood, Softwood), By Grade (Chemical, Mechanical, Semi-Chemical, Others), By End Use (Packaging (Food and Beverages, Pharmaceutical, Personal Care and Cosmetics, Automotive, Others), Paper (Newspaper, Books and Magazines, Tissues, Others), Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape APRIL Group, ARAUCO, Canfor Corporation, Metsä Group, Nippon Paper Industries Co. Ltd, Oji Holdings Corporation, Sappi Limited, Södra, Stora Enso Oyj, Suzano Papel e Celulose Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- APRIL Group

- ARAUCO

- Canfor Corporation

- Metsä Group

- Nippon Paper Industries Co. Ltd

- Oji Holdings Corporation

- Sappi Limited

- Södra

- Stora Enso Oyj

- Suzano Papel e Celulose

Our Clients

- 180550

- March 2026