Quick Navigation

Report Overview

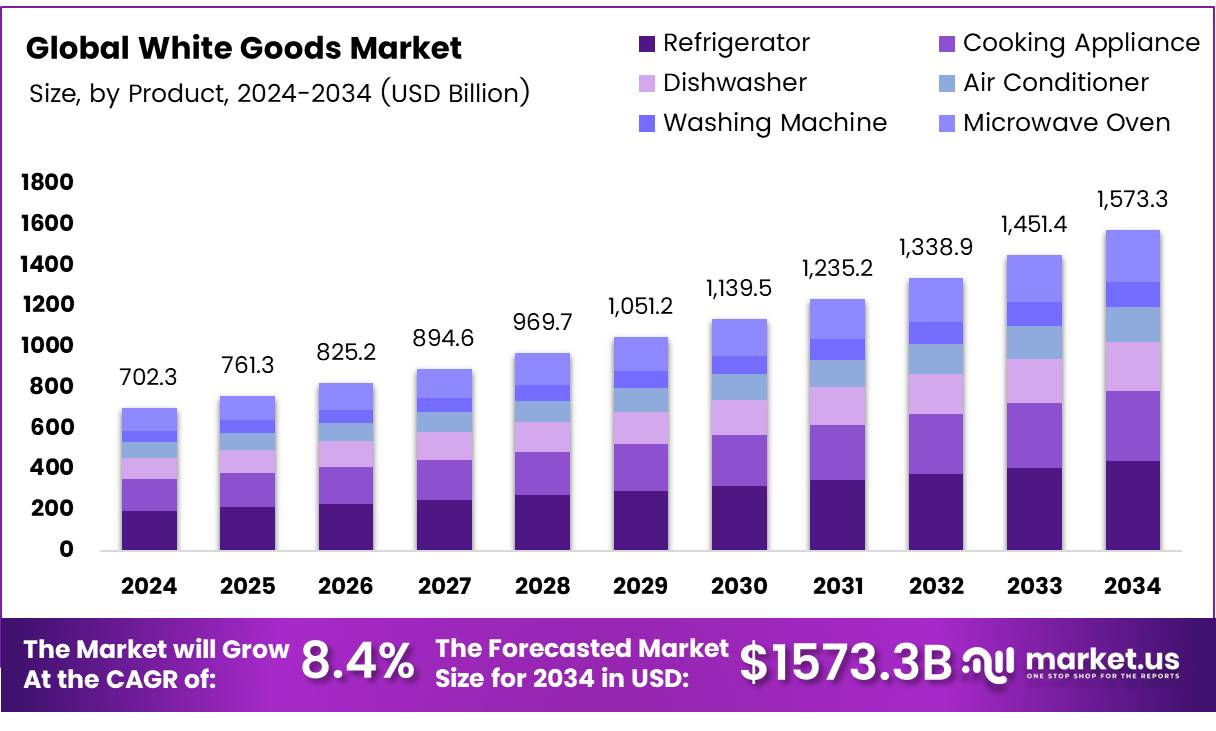

The Global White Goods Market size is expected to be worth around USD 1573.3 Billion by 2034, from USD 702.3 Billion in 2024, growing at a CAGR of 8.4% during the forecast period from 2025 to 2034.

White goods refer to large household appliances like refrigerators, washing machines, dishwashers, air conditioners, and ovens. These are durable goods used for routine tasks within the home. The white goods market includes both major appliances and small appliances used for cooking, cleaning, and preserving food.

The global market is characterized by rapid technological innovation, the integration of smart features, and growing consumer demand for energy-efficient solutions. This sector plays a key role in the consumer electronics and home appliances industries.

The white goods sector has witnessed substantial growth driven by increasing consumer spending, rising disposable incomes, and the trend toward smart home integration. Consumers’ desire for high-performance, energy-efficient, and technologically advanced appliances is pushing manufacturers to innovate constantly.

The integration of IoT (Internet of Things) in white goods, like smart refrigerators and washing machines, is opening new avenues for market expansion. With growing concerns about environmental impact, consumers are leaning towards energy-efficient and sustainable products, creating a steady demand for innovations in the white goods market.

According to Study, global retail sales of major appliances in 2024 are expected to surpass 400 billion U.S. dollars, while sales of small appliances will reach 250 billion U.S. dollars. This indicates a strong market presence and sustained growth prospects.

The white goods market is expected to continue its upward trajectory, supported by several macroeconomic factors. Growth in developing regions, especially in Asia-Pacific and Latin America, where rising urbanization is increasing the demand for household appliances, presents significant market opportunities.

Furthermore, government initiatives, including investment in energy-efficient technologies and eco-friendly regulations, are driving the transition toward greener products. Regulatory frameworks and incentives aimed at promoting sustainability are expected to accelerate the adoption of energy-efficient appliances.

According to Study, in 2023, the global refrigerator industry generated approximately 117 billion U.S. dollars in revenue, highlighting the market’s strong demand for essential appliances. According to industry report,, there were 7.1 million refrigerator shipments globally, with 120,799 buyers and 120,719 suppliers, showcasing the competitive landscape and opportunities for growth within the sector.

Key Takeaways

- The global white goods market is expected to reach USD 1573.3 billion by 2034, growing at a CAGR of 8.4%.

- Refrigerators led the product segment in 2023 with a 40.6% market share, driven by energy-efficient and smart models.

- The residential segment dominated the application segment in 2023, accounting for 60.3% of the market share.

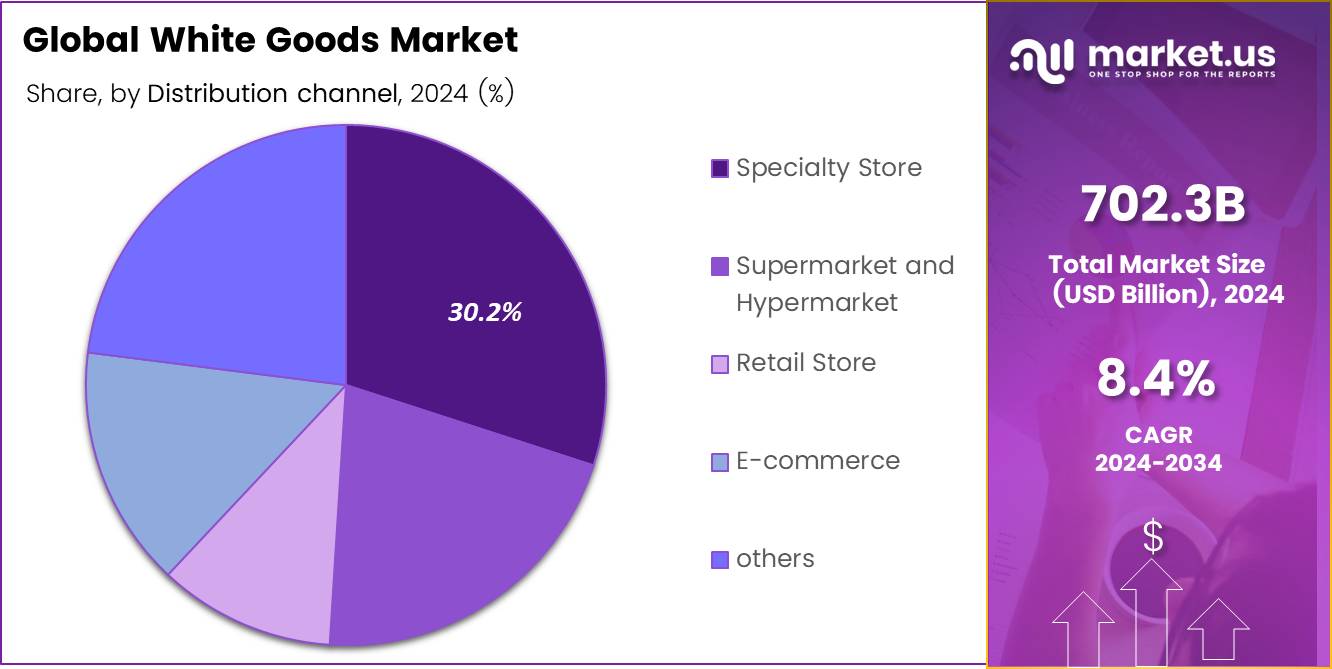

- Specialty stores captured 30.2% of the market share in 2023, offering a personalized shopping experience.

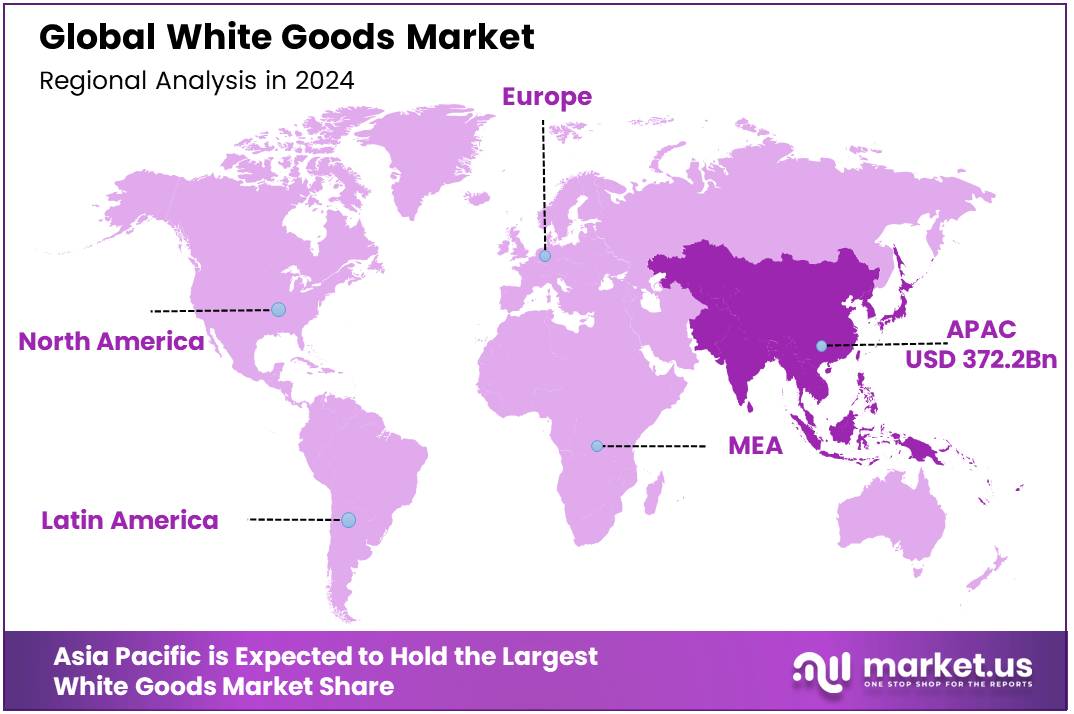

- Asia Pacific is the leading region in the white goods market with a 53.6% share, valued at USD 372.2 billion.

Product Analysis

In 2023, Refrigerators Captured 40.6% of the White Goods Market Share by Product Segment

In 2023, refrigerators held a dominant market position in the By Product Analysis segment of the White Goods Market, with a 40.6% share.

The refrigerator segment continued to be a significant contributor to the overall market due to evolving consumer preferences for energy-efficient, smart, and space-saving models. These appliances, driven by advancements in cooling technology and design, remain a staple in households and commercial spaces.

Cooking appliances, including microwave ovens, stoves, and ranges, followed in market significance, commanding a substantial share as home cooking trends gained momentum. Their versatility and continued innovation in features like smart cooking, energy efficiency, and user-friendly interfaces have contributed to their growing demand.

Dishwashers, with their convenience, especially in regions with busy lifestyles, maintained steady growth in the market. The rise of dual-function models, offering both washing and sanitizing capabilities, helped drive interest.

Air conditioners saw a robust demand due to climate change and rising temperatures in many regions, contributing to their significant share. Washing machines, further enhanced by features such as water-saving technologies and automation, continued to perform well as essential household items.

Application Analysis

Residential Segment Dominates White Goods Market with 60.3% Share in 2023

In 2023, the Residential segment held a dominant market position in the By Application Analysis segment of the White Goods Market, accounting for 60.3% of the total market share. The continued rise in disposable income, coupled with evolving consumer preferences for advanced home appliances, drove the substantial growth in this segment.

Consumers increasingly prioritize energy-efficient, smart, and multi-functional appliances to enhance convenience and comfort at home. This trend is particularly noticeable in developed markets, where technological innovations in washing machines, refrigerators, and ovens are becoming standard in most households.

Moreover, the post-pandemic boom in home renovation and improvement further fueled demand for modern white goods.

The Commercial segment is driven by demand in industries such as hospitality, healthcare, and retail, where large-scale appliances like commercial refrigerators and dishwashers are critical.

However, the growth in the Commercial segment is slower compared to Residential due to higher upfront costs and longer replacement cycles for such products. Despite these challenges, the Commercial segment is expected to see steady growth, driven by the expansion of service industries and increasing adoption of energy-efficient technologies in commercial establishments.

Distribution Channel Analysis

Specialty Stores Lead with 30.2% Market Share

In 2023, Specialty Stores held a dominant market position in the By Distribution Channel Analysis segment of the White Goods Market, capturing a 30.2% share. This growth can be attributed to the tailored shopping experience offered by these outlets, where customers are provided with expert guidance and specialized product assortments.

Specialty Stores continue to appeal to consumers seeking high-quality, premium white goods, often backed by superior after-sales service and warranties.

Supermarkets and Hypermarkets followed as significant players, accounting for a substantial portion of market sales. These channels benefit from their wide reach and convenience, offering competitive pricing and attracting a broad customer base. The presence of white goods alongside everyday household items enhances their appeal to shoppers looking for convenience and cost-effectiveness.

Retail Stores also maintained a notable presence, serving as local hubs for consumers who prefer to engage with products in person before making purchasing decisions. E-commerce, while growing rapidly, secured a smaller market share due to logistical challenges and delayed delivery times for large appliances.

Lastly, other channels, including direct sales and catalogs, accounted for the remaining share of the market. Overall, traditional retail and specialty channels remained the dominant forces in the white goods distribution landscape.

Key Market Segments

By Product

- Refrigerator

- Cooking Appliance

- Dishwasher

- Air Conditioner

- Washing Machine

- Microwave Oven

By Application

- Residential

- Commercial

By Distribution channel

- Specialty Store

- Supermarket and Hypermarket

- Retail Store

- E-commerce

- others

Drivers

Urbanization and rising incomes drive white goods demand as people seek modern appliances for better living standards

Urbanization and rising disposable incomes, especially in developing countries, are pivotal drivers of the white goods market. As more people move to urban areas and experience an increase in their earnings, there is a noticeable shift towards purchasing modern appliances like refrigerators, washing machines, and air conditioners.

Additionally, there’s a significant rise in consumer awareness around energy efficiency and environmental sustainability. More consumers now prioritize eco-friendly, energy-efficient appliances, driven by concerns over long-term energy costs and environmental impact. This has spurred innovation, with manufacturers developing products that consume less power while maintaining high performance.

The surge in real estate development, especially in emerging markets, also plays a critical role. As more residential units are being built, the demand for white goods increases, as new homeowners or renters seek to equip their homes with modern appliances.

This rise in new homeownership and the construction of residential buildings is boosting the demand for essential household items, further expanding the market for white goods globally.

Restraints

High Initial Costs and Economic Challenges

The white goods market faces several restraints, particularly the high initial cost associated with advanced appliances. Consumers are often deterred by the hefty price tag of modern, energy-efficient, or smart appliances, which can make them seem out of reach for those on a budget.

This price sensitivity is especially evident in markets where disposable income is lower, as consumers prioritize essential spending over expensive household upgrades.

Furthermore, economic uncertainty exacerbates this challenge. Factors like inflation, economic recessions, and global financial instability can significantly reduce household income and purchasing power. As people tighten their budgets during tough financial times, the demand for high-end or non-essential white goods tends to drop.

This can lead to slower market growth, particularly in developed economies where these appliances are often considered premium. With limited disposable income, many consumers may opt for more affordable alternatives, delaying the purchase of energy-efficient or smart appliances. Manufacturers, in turn, may face challenges in maintaining their sales growth and profitability amidst these economic pressures.

Growth Factors

Growth Opportunities in the White Goods Market Driven by Innovation and Sustainability

The white goods market presents numerous growth opportunities, particularly through advancements in smart, energy-efficient, and connected appliances. One of the key drivers is the rise of IoT-enabled appliances that allow consumers to control and monitor their devices remotely via smartphones or other connected platforms. This trend aligns with the growing demand for convenience and improved home automation.

Additionally, as consumers become more environmentally conscious, there is a significant opportunity to develop and market energy-efficient appliances. These products not only reduce electricity bills but also support sustainability goals, which are becoming increasingly important to buyers worldwide.

Another important growth avenue is in emerging markets, where rising disposable incomes and rapid urbanization are making white goods more accessible to a larger portion of the population.

These regions, particularly in Asia and Africa, are expected to see a strong demand for both basic and advanced appliances. Lastly, the replacement and upgrade market is growing, as older appliances are being replaced with more modern, efficient, and feature-rich alternatives.

Consumers are looking for products that offer better performance, reliability, and long-term value, thus creating continuous demand for new appliances. Together, these factors are set to drive the white goods market forward, presenting ample opportunities for companies to innovate and capture market share.

Emerging Trends

Rising Values of Energy Efficiency and Smart Features in White Goods Reflect Consumer Demand for Convenience and Sustainability

The white goods market is evolving rapidly due to various technological advancements and consumer demands. Smart home integration is a key trend, with more people opting for appliances that can be controlled remotely or via voice commands, thanks to the rise of smart home systems.

Energy efficiency and sustainability are also becoming increasingly important, as consumers prefer appliances that save energy, reduce costs, and are made with eco-friendly materials. Voice-controlled features, such as compatibility with Alexa or Google Assistant, are being integrated into appliances like refrigerators, ovens, and washing machines, adding convenience and appeal.

Furthermore, minimalistic design trends are influencing the aesthetic of white goods, with sleek, modern-looking appliances becoming more popular in homes. These shifts reflect a growing desire for convenience, sustainability, and smarter living spaces.

Manufacturers are responding by developing more intuitive, energy-efficient products, which not only align with consumer preferences but also contribute to reducing environmental impact.

Regional Analysis

Asia Pacific Leads White Goods Market with 53.6% Share and USD 372.2 Billion Value

The global white goods market is experiencing significant growth across various regions, with Asia Pacific leading as the dominant market, holding a share of 53.6% valued at USD 372.2 billion. This dominance is primarily driven by rapid urbanization, a burgeoning middle class, and increasing disposable incomes in key countries such as China and India.

The region also benefits from robust manufacturing capabilities, with many leading global appliance brands operating in or sourcing from Asia. Additionally, the expansion of e-commerce platforms and the growing demand for energy-efficient appliances further boost market potential.

Regional Mentions:

In North America, the white goods market is witnessing steady growth, supported by strong consumer demand for innovative and technologically advanced home appliances. The presence of well-established brands in the U.S. and Canada contributes significantly to the market’s expansion. Increasing consumer interest in sustainable and energy-efficient products has also spurred innovation in the region.

Europe is another key market for white goods, with demand driven by consumer preferences for high-quality and durable appliances. The European market has seen a shift towards smart appliances and sustainability-focused innovations, as consumers prioritize energy efficiency and environmental responsibility. Major markets include Germany, the UK, and France, with significant growth in Eastern Europe as well.

The Middle East & Africa market is expanding at a moderate pace, primarily driven by rising urbanization and the increasing adoption of modern household appliances. While the region’s growth is slower compared to Asia Pacific, emerging markets like the UAE, Saudi Arabia, and South Africa are showing promising potential due to their growing affluent populations.

In Latin America, market growth is supported by the increasing purchasing power of middle-class households in countries such as Brazil and Mexico. However, economic challenges in certain countries may temper growth, with consumers being more price-sensitive and gravitating towards cost-effective, durable appliances.

Key Regions and Countries covered іn thе rероrt

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The global white goods market in 2023 remains highly competitive, with a mix of established leaders and emerging innovators. Key players span diverse sectors, including home appliances, knives, robotic cleaning, and smart technology, reflecting the broadening scope of white goods beyond traditional household appliances.

Samsung Electronics Co., Ltd. and LG Electronics Inc. continue to dominate, leveraging their advanced technology in appliances such as refrigerators, washers, and air conditioners. Their ability to integrate smart home features and sustainable technologies has helped them maintain leadership positions. Both companies are also at the forefront of energy efficiency and connected home ecosystems, appealing to tech-savvy, eco-conscious consumers.

Dyson Limited has made a significant impact in the premium segment of the white goods market with its innovative products like vacuum cleaners and air purifiers. Dyson’s ability to combine cutting-edge technology with sleek design continues to position it as a leader in home care solutions.

Panasonic Corporation and Sharp Corporation bring strong capabilities in the electronics space, with a focus on high-efficiency appliances, air quality systems, and energy-saving technologies. Their efforts in improving the performance and longevity of products help maintain their competitive edge.

Shenzhen Proscenic Technology Co. Ltd. and Neato Robotics, Inc. exemplify the growing importance of smart home and robotics in white goods. With the rise of robot vacuums and other automated solutions, these companies cater to the growing demand for convenience and time-saving innovations in household maintenance.

Friedr. Dick GmbH & Co., Victorinox AG, and M.A.C. Knife represent the niche segment of premium kitchenware and tools, maintaining strong market positions through high-quality, precision-engineered products.

Top Key Players in the Market

- Victorinox AG

- Anker Innovation Technology Co., Ltd.

- GLOBAL APPLIANCES USA

- KAI USA LTD

- Kiya corp.

- M.A.C. Knife

- Samsung Electronics Co., Ltd

- Shenzhen Proscenic Technology Co. Ltd.

- L.G. Electronics Inc

- Dyson Limited

- Messermeister

- Neato Robotics, Inc.

- Cecotec Innovaciones S.L.

- Panasonic Corporation

- Sharp Corporation

Recent Developments

- In November 2024, Beyond Appliances successfully secured $2 million in seed funding to accelerate the growth of its smart kitchen appliance business, aiming to revolutionize home cooking with advanced technology.

- In March 2024, Upliance.ai, a smart home appliance startup, achieved a significant milestone by reaching Rs 5 million in sales within a single month, showcasing strong demand for its innovative products.

- In September 2024, the U.S. Department of Energy (DOE) announced a $38.8 million funding initiative under the BENEFIT 2024 program to support technology R&D projects focused on decarbonizing the building sector.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 702.3 Billion |

| Forecast Revenue (2033) | USD 1573.3 Billion |

| CAGR (2024-2033) | 8.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Refrigerator, Cooking Appliance, Dishwasher, Air Conditioner, Washing Machine, Microwave Oven), By Application (Residential, Commercial), By Distribution channel (Specialty Store, Supermarket and Hypermarket, Retail Store, E-commerce, others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Friedr. Dick GmbH & Co, Victorinox AG, Anker Innovation Technology Co., Ltd., GLOBAL APPLIANCES USA, KAI USA LTD, Kiya corp., M.A.C. Knife, Samsung Electronics Co., Ltd, Shenzhen Proscenic Technology Co. Ltd., L.G. Electronics Inc, Dyson Limited, Messermeister, Neato Robotics, Inc., Cecotec Innovaciones S.L., Panasonic Corporation, Sharp Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |