Quick Navigation

Report Overview

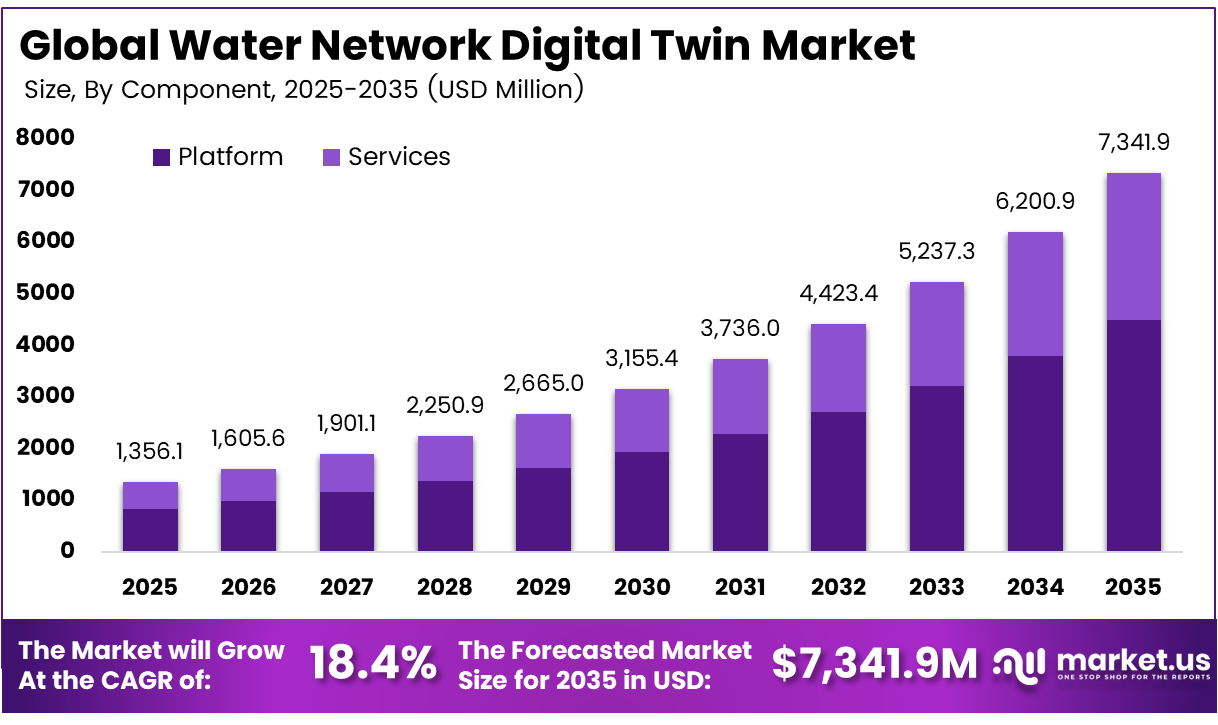

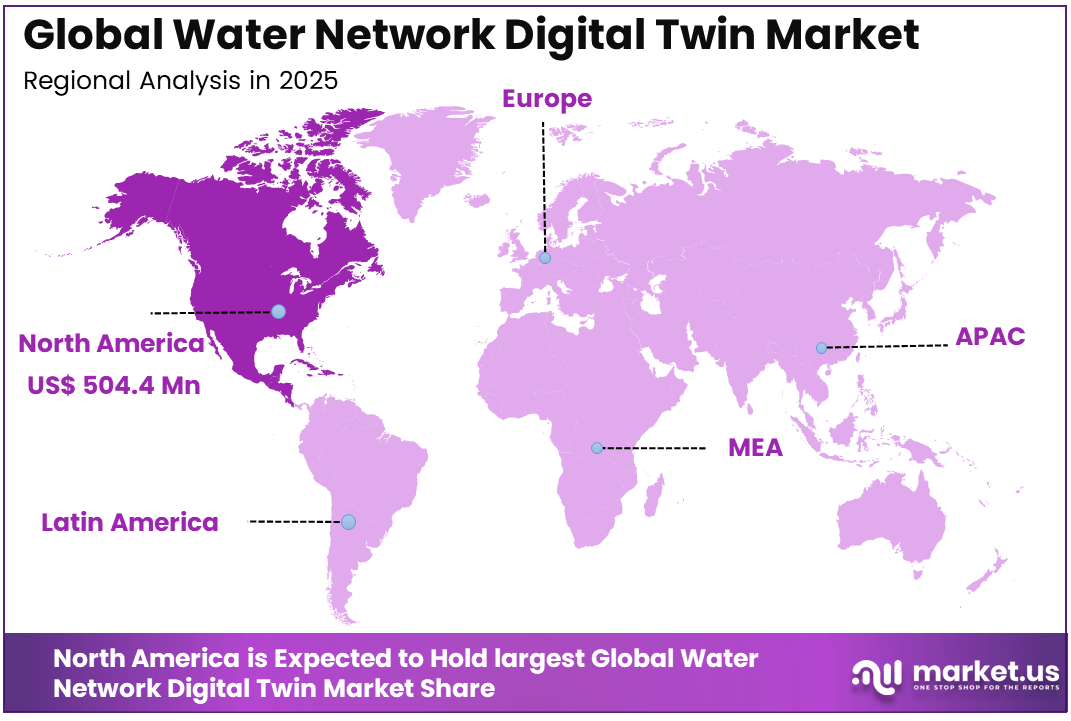

The Global Water Network Digital Twin Market size is expected to be worth around USD 7,341.9 million by 2035, from USD 1,356.1 million in 2025, growing at a CAGR of 18.4% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 37.2% share, holding USD 504.4 million in revenue.

Water Network Digital Twin refers to a virtual model of a physical water distribution system that uses real-time data from sensors, meters, and control systems. It helps utilities monitor pipelines, pumps, valves, pressure, flow, and water quality to detect issues early, improve planning, reduce losses, and support a reliable water supply.

Top driving factors include growing water stress in cities, leakage rates that can exceed 30% in aging networks, and public pressure for more dependable supply. Rising energy costs are also pushing utilities to reduce waste across pumps, treatment, and distribution. Stricter water quality rules further encourage operators to improve monitoring, transparency, and system efficiency.

Top driving factors include growing water stress in cities, leakage rates that can exceed 30% in aging networks, and public pressure for more dependable supply. Rising energy costs are also pushing utilities to reduce waste across pumps, treatment, and distribution. Stricter water quality rules further encourage operators to improve monitoring, transparency, and system efficiency.

The market for Water Network Digital Twin is driven by the growing need to manage water networks with better accuracy, efficiency, and reliability. Utilities are adopting these systems to detect leaks, reduce water losses, monitor pressure, and improve maintenance planning. Rising urban demand, aging pipelines, stricter service expectations, and climate-related water stress are further supporting adoption across municipal and industrial water systems.

Demand is growing as utilities see clear operating gains, including double-digit cuts in non-revenue water, lower pump energy use, and fewer unplanned outages through predictive maintenance. Mid-sized utilities are also testing digital water systems through pilots. Falling sensor and computing costs have made adoption more practical beyond large metropolitan networks.

For instance, in March 2025, AVEVA pushed further into digital water by aligning its PI System data infrastructure with AVEVA’s modeling tools to support full water‑network twins. Operators can now stream time‑series data from pumps, reservoirs, and meters into virtual networks, improving leak localization, alarming, and energy‑performance benchmarking across large utility fleets.

Key Takeaway

- In 2025, the Platform segment held a dominant market position, capturing a 61.3% share of the Global Water Network Digital Twin Market.

- In 2025, the Leak Detection & Water Loss Management segment held a dominant market position, capturing a 28.4% share of the Global Water Network Digital Twin Market.

- In 2025, the Cloud segment held a dominant market position, capturing a 61.5% share of the Global Water Network Digital Twin Market.

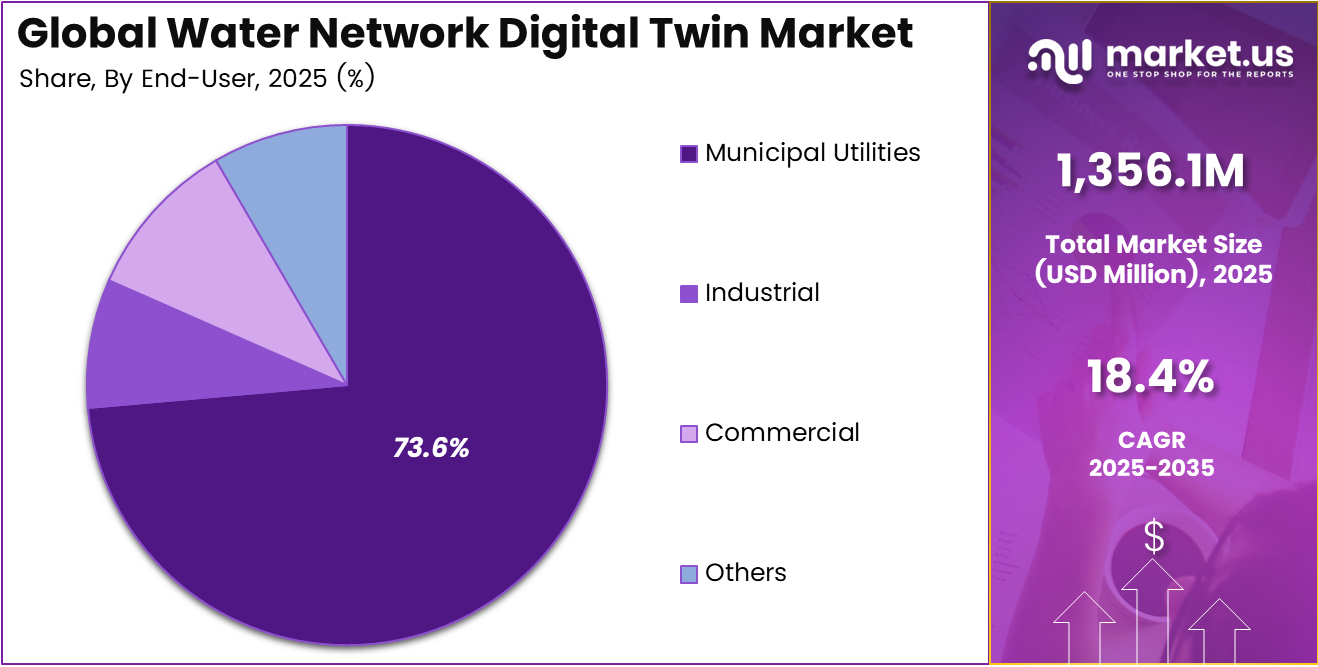

- In 2025, the Municipal Utilities segment held a dominant market position, capturing a 73.6% share of the Global Water Network Digital Twin Market.

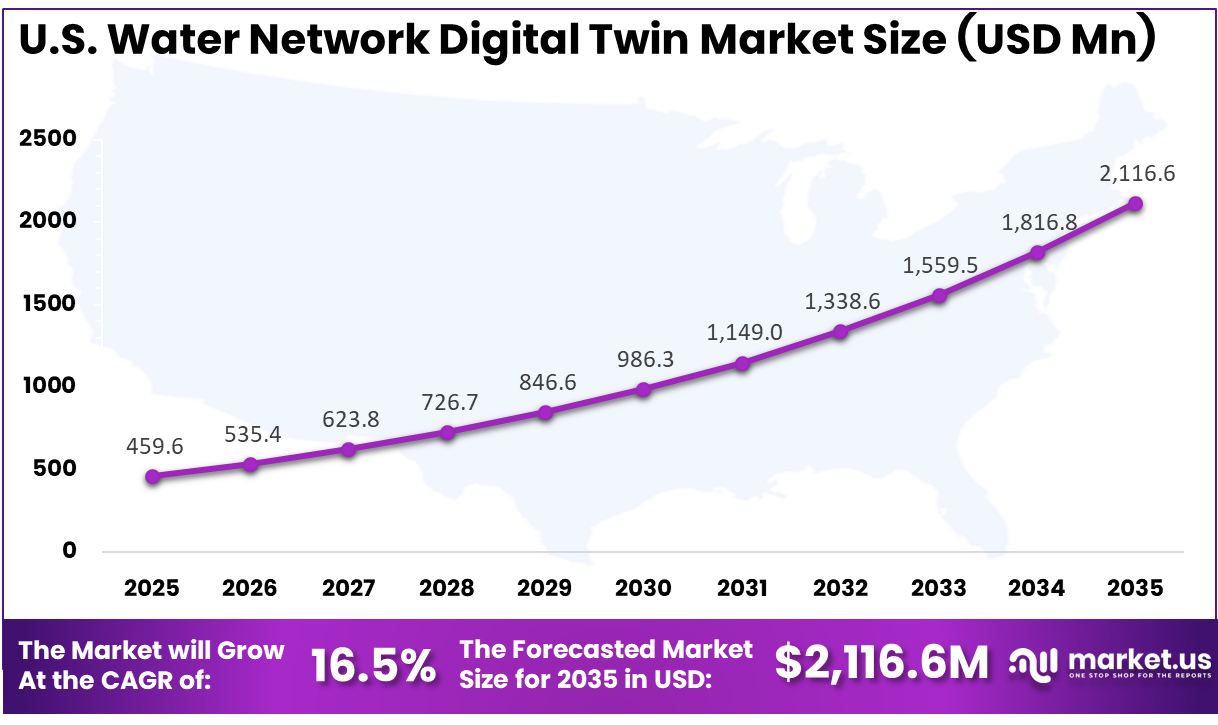

- The U.S. Water Network Digital Twin Market was valued at USD 459.6 Million in 2025, with a robust CAGR of 16.5%.

- In 2025, North America held a dominant market position in the Global Water Network Digital Twin Market, capturing more than a 37.2% share.

Role of Generative AI

Generative AI is changing how operators use water network digital twins. It is moving systems beyond static dashboards by helping teams test scenarios, create synthetic failures, and review possible responses. GenAI-driven twins can simulate realistic leak and anomaly patterns that rule-based models may miss in complex urban networks.

Early studies in smart water systems show that GenAI-enhanced twins can cut leak and abnormal event detection time by over 30%. This is mainly done by learning normal flow and pressure patterns. For utilities where non-revenue water is often above 20% of system input, faster detection can protect revenue.

Investment and Business Benefits

Investment opportunities span sensor hardware, communication networks, hydraulic and AI software, system integration, and long-term managed analytics. Niche players can also benefit from rising demand for cybersecurity, data quality tools, and workforce training. These areas are becoming important as utilities face skill gaps and growing concerns around secure data handling.

Business benefits include lower operating costs, fewer customer complaints, stronger regulatory compliance, and better resilience during storms, floods, or droughts. Some utilities report measurable gains, such as reduced response times during outages and more accurate demand forecasts at sub-daily time scales. These improvements help operators plan resources and protect service reliability.

Regional Analysis

In 2025, North America held a dominant market position in the Global Water Network Digital Twin Market, capturing more than a 37.2% share, holding USD 504.4 million in revenue. This dominance is due to advanced utility infrastructure, strong digital adoption, and rising investment in smart water management. Many utilities in the region are using digital twins to reduce leakage, improve asset planning, and strengthen service reliability. Aging pipelines, climate-related water stress, and strict water quality requirements further support faster adoption across municipal water systems.

For instance, in May 2024, IBM advanced North America’s role in utility digital twins by working with energy and utilities customers on AWS to build AI‑enabled digital twin models of critical networks, using analytics and WatsonX-driven insights to optimize infrastructure performance, reduce risk, and support low‑carbon transition strategies that also benefit water‑related assets.

U.S. Water Network Digital Twin Market Size

The market for Water Network Digital Twin within the U.S. is growing tremendously and is currently valued at USD 459.6 million; the market has a projected CAGR of 16.5%. The market is growing due to aging water infrastructure, rising leakage concerns, and the need for better control over urban water networks. Utilities are adopting digital twins to monitor pipelines, predict failures, manage pressure, and improve service reliability. Strong smart city investments, stricter water quality expectations, and rising climate risks are also encouraging wider use of real-time network modelling across public utilities.

For instance, in May 2025, Bentley Systems expanded digital twin adoption for U.S. water networks by partnering with HRG to deploy its OpenFlows WaterSight software across mid‑Atlantic utilities, integrating SCADA, GIS, hydraulic models, and operations data so operators can cut non‑revenue water, improve energy efficiency, and strengthen capital planning.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Component Analysis

In 2025, the Platform segment held a dominant market position, capturing a 61.3% share of the Global Water Network Digital Twin Market. This dominance is due to the need for a central system that brings network data, hydraulic models, alerts, and operating decisions into one place. Water utilities prefer platform-based digital twins because they help teams monitor assets, identify risks, and plan maintenance with better visibility.

Platform adoption is also supported by the shift from manual network management to connected control systems. These platforms make it easier to compare field data with model outputs, test operating scenarios, and improve coordination between engineering, operations, and planning teams.

For instance, in March 2025, ABB promoted its Ability Water Management System as a central, vendor-neutral platform for overseeing water operations from source to distribution. The system pulls together data from multiple assets into a single workspace, reflecting how utilities favor platform architectures that simplify monitoring and decision making.

Application Analysis

In 2025, the Leak Detection & Water Loss Management segment held a dominant market position, capturing a 28.4% share of the Global Water Network Digital Twin Market. This dominance is due to the growing need to reduce hidden losses across aging water networks. Utilities are using digital twins to detect unusual flow and pressure patterns, locate possible leakage zones, and respond before small issues turn into service disruptions.

Leak detection and water loss management remain a priority because wasted water directly affects cost, supply reliability, and public trust. Digital twin tools help operators make faster decisions, improve repair planning, and manage pressure more effectively across complex distribution systems.

For instance, in July 2025, Xylem described how digital twins and smart monitoring enable utilities to compare real-time data with model behavior to pinpoint problem areas in the network. This approach helps detect hidden leaks and inefficiencies, encouraging more utilities to deploy leak-focused applications as an early digital twin use case.

Deployment Mode Analysis

In 2025, the Cloud segment held a dominant market position, capturing a 61.5% share of the Global Water Network Digital Twin Market. This dominance is due to the flexibility cloud systems offer for storing, processing, and sharing water network data. Utilities can access digital twin platforms from different locations, connect field sensors more easily, and support faster updates without heavy on-site technology infrastructure.

Cloud deployment is also gaining preference because it supports scalable operations as more meters, sensors, and monitoring devices are added. It allows utilities to manage growing data volumes, run simulations, and improve collaboration between technical teams, field crews, and decision makers.

For instance, in March 2026, Schneider Electric emphasized flexible, secure digital water solutions that can scale with city growth without locking utilities into rigid on-site systems. This reflects a clear push toward cloud-based or hybrid deployments, where utilities gain access to new capabilities without building and maintaining large local data centers.

End-User Analysis

In 2025, the Municipal Utilities segment held a dominant market position, capturing a 73.6% share of the Global Water Network Digital Twin Market. This dominance is due to the large responsibility municipal utilities carry in managing public water supply networks. These organizations must maintain service reliability, reduce leakage, protect water quality, and respond quickly to faults across wide urban and suburban distribution systems.

Municipal utilities are also under pressure to modernize aging infrastructure while keeping services affordable and compliant. Digital twins support better asset planning, faster incident response, and more informed investment decisions, making them highly useful for city-level water operations.

For instance, in May 2026, at IFAT 2026, Siemens unveiled an integrated control center designed for municipal and industrial environmental infrastructure, including drinking water and wastewater utilities. The solution gives city operators a single view of assets and facilities, showing how municipal utilities are central to digital twin adoption.

Key Market Segments

By Component

- Platform

- Hydraulic & Water Quality Modeling Engines

- Data Integration & IoT Platforms

- AI/ML & Analytics Modules

- Others

- Services

- Consulting & Implementation

- Managed Services & Ongoing Support

By Application

- Asset Management

- Network Optimization

- Leak Detection & Water Loss Management

- Water Quality Monitoring

- Predictive Maintenance

- Others

By Deployment Mode

- On-Premises

- Cloud

By End-User

- Municipal Utilities

- Industrial

- Commercial

- Others

Emerging Trends

A major trend is the integration of IoT sensors, advanced analytics, and digital twins into unified monitoring platforms. These systems allow utilities to simulate flow, pressure, and water quality across the network in real time. Adoption is also expanding from treatment plants into distribution, wastewater, reuse, and watershed applications.

Large-scale digital twin programs are also being used for rivers and basins. Some national systems now track data from tens of thousands of hydrological stations and millions of water projects. One national water conservation map includes about 16 million infrastructure assets and more than 50,000 precipitation stations.

Growth Factors

Growth is supported by the need for stronger resilience under climate stress. Utilities are facing more droughts, intense rainfall, and stricter checks on reliability and safety. Digital twins help extend asset life, reduce non-revenue water, and support compliance, making them useful even when capital budgets remain tight.

Another factor is the rapid use of smart meters and sensors. These devices provide real-time hydraulic and quality data, which keeps a digital twin accurate and useful. As smart city programs expand in North America, Europe, and parts of Asia, water digital twin investment is rising with utility modernisation.

Market Dynamics

Drivers - Growing Need for Efficient Water Resource Management

Water utilities are under rising pressure to manage supply more carefully as cities grow and water demand becomes less predictable. Water network digital twins help operators understand flow, pressure, and asset performance in a clearer way, making daily planning and resource control more efficient.

These systems also support better decisions on leakage, pumping, storage, and maintenance. By using live network data, utilities can reduce waste, improve service reliability, and respond faster to faults. This makes digital twins useful for both large city networks and smaller public water systems.

For instance, in October 2025, Brabant Water partnered with Xylem to build one of Europe’s largest smart water networks using a digital twin and around 120,000 smart meters. The project focuses on real‑time monitoring, leak detection, and network optimisation to improve water efficiency and resilience for more than two million people.

Restraint - Integration Complexity

Integration complexity remains a key barrier because many utilities still work with old systems, scattered records, and limited sensor coverage. Connecting these assets with a digital twin platform can take time, planning, and strong technical support across operations, engineering, and data teams.

Utilities may also face difficulty in aligning hydraulic models, billing systems, GIS data, and field inputs into one reliable platform. When data formats are inconsistent or outdated, the twin may not reflect real network conditions accurately, which can slow trust and adoption among operators.

For instance, in May 2026, Siemens announced an integrated control centre for water and waste operations that gathers data from many subsystems into one platform. The launch highlights how fragmented legacy systems drive demand for unified solutions but also shows the complexity of integrating diverse assets, sensors, and software.

Opportunities - Smart City and Sustainability Initiatives

Smart city programs are creating strong opportunities for water network digital twins. Cities are investing in connected infrastructure to manage utilities more efficiently, and water systems are becoming an important part of this shift. Digital twins help link water planning with energy use, climate resilience, and public service goals.

Sustainability initiatives are also encouraging utilities to reduce losses, conserve water, and improve asset life. Digital twins support these goals by helping teams test operating scenarios before making changes in the field. This makes them valuable for long-term planning and responsible water management.

For instance, in May 2026, Siemens expanded its digital portfolio for water and waste management with AI‑based leak detection, process modelling, and energy management. The integrated control centre and quality monitoring tools support smarter cities by giving operators real‑time insight and helping reduce resource use and emissions.

Challenges - Skills and Security Gaps

Skills and security gaps remain a major concern for utilities adopting digital twin systems. Many operators need staff who understand water engineering, data analytics, cybersecurity, and platform management. Without the right training, even advanced systems may not be used fully in day-to-day operations.

Security risks also increase as water networks become more connected through sensors, cloud tools, and remote monitoring. Utilities must protect operational data and control systems from misuse. Strong access control, staff awareness, and secure data practices are needed to build confidence in digital twin adoption.

For instance, in January 2025, Bentley pointed out that water utilities already handle diverse data sources but often struggle to turn them into operational intelligence. The digital twin strategy requires staff capable of working across GIS, SCADA, sensors, and models, which can be a significant skills challenge.

Key Players Analysis

One of the leading players in March 2025, Schneider Electric partnered with Malaysian utility Air Selangor to deploy a water‑distribution digital twin, using advanced modeling and real‑time data to optimise pressure, cut leakage, and improve resilience across Selangor’s large urban network, signalling accelerating adoption of digital twins in operational water systems worldwide.

Top Key Players in the Market

- Xylem Inc.

- Schneider Electric

- Siemens AG

- ABB Ltd.

- Bentley Systems

- IBM Corporation

- Dassault Systèmes

- AVEVA Group plc

- Innovyze

- Aquasuite

- Ayyeka Technologies

- Trimble Inc.

- TaKaDu Ltd.

- Idrica

- Grundfos Holding A/S

- Badger Meter, Inc.

- Others

Recent Developments

- In March 2025, ABB advanced its position in digital water infrastructure by integrating ABB Ability condition monitoring with hydraulic modeling platforms, effectively creating near‑real‑time twins for critical pumping assets. This lets operators predict failures, schedule maintenance with minimal downtime, and coordinate equipment operations against energy tariffs and water‑demand peaks.

- In March 2025, Innovyze enhanced Info360 on AWS with dynamic digital twins for predictive water operations, preventing disruptions in North American utilities. The platform processes IoT sensor data in real-time, cutting service outages by 30% through advanced analytics.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1,356.1 Million |

| Forecast Revenue (2035) | USD 7,341.9 Million |

| CAGR (2026-2035) | 18.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Component (Platform, Services), By Application (Asset Management, Network Optimization, Leak Detection & Water Loss Management, Water Quality Monitoring, Predictive Maintenance, Others), By Deployment Mode (On-Premises, Cloud), By End-User (Municipal Utilities, Industrial, Commercial, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Xylem Inc., Schneider Electric, Siemens AG, ABB Ltd., Bentley Systems, IBM Corporation, Dassault Systèmes, AVEVA Group plc, Innovyze, Aquasuite, Ayyeka Technologies, Trimble Inc., TaKaDu Ltd., Idrica, Grundfos Holding A/S, Badger Meter, Inc., Others |

| Customization Scope | Customization at the segment and region/country levels will be provided. Moreover, customization can be tailored to the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |