Quick Navigation

Report Overview

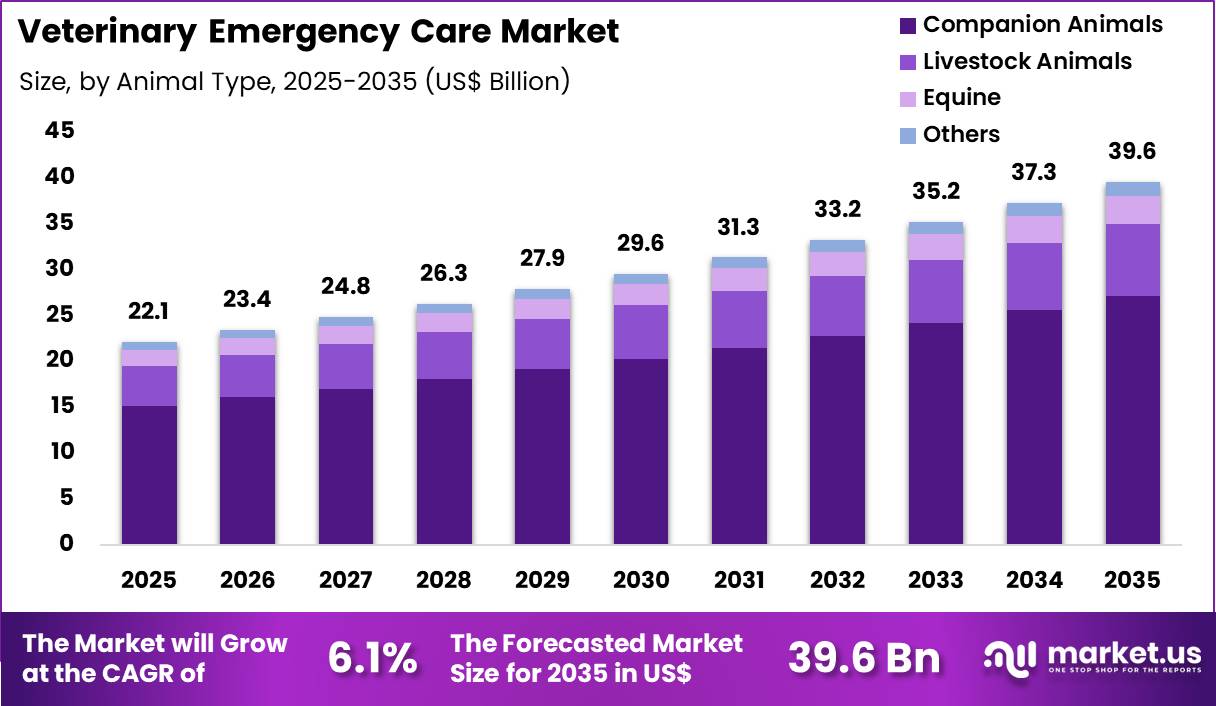

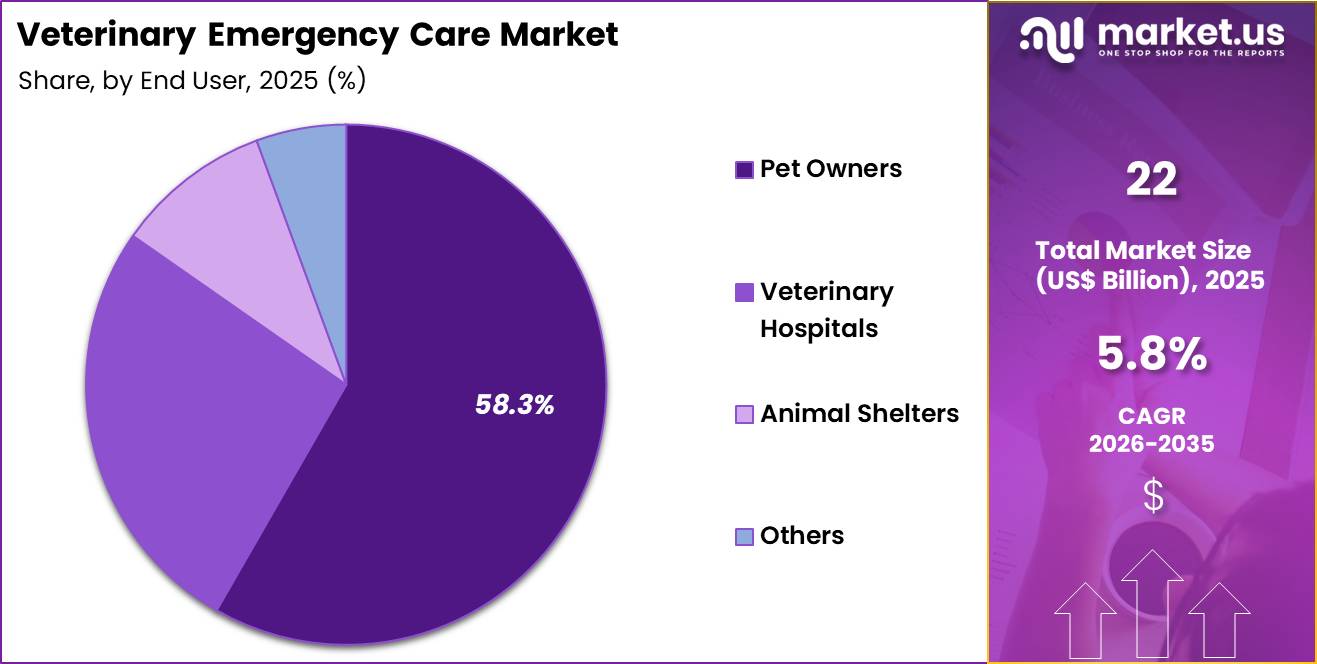

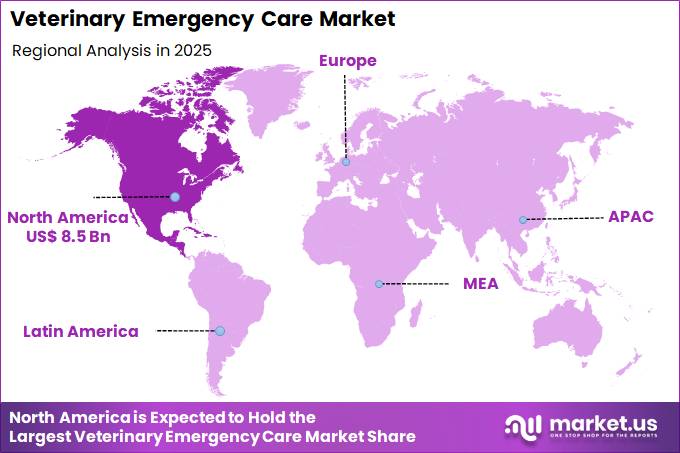

Global Veterinary Emergency Care Market size is expected to be worth around US$ 39.6 Billion by 2035 from US$ 22.1 Billion in 2025, growing at a CAGR of 6.0% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 38.4% share with a revenue of US$ 8.5 Billion.

Increasing frequency of pet-related emergencies and the growing complexity of companion animal care propel the Veterinary Emergency Care market as pet owners and veterinary professionals seek specialized, rapid-response services that address acute and life-threatening conditions.

Emergency veterinary hospitals increasingly manage trauma cases from vehicular accidents, falls, and bite wounds, providing immediate stabilization, diagnostic imaging, and surgical intervention to improve survival rates and long-term outcomes.

These facilities support critical care for acute abdominal emergencies, including gastric dilatation-volvulus in large-breed dogs and intestinal obstructions, where rapid surgical decompression and intensive monitoring are essential.

Veterinarians in emergency settings also treat toxin ingestions, such as chocolate, xylitol, or rodenticides, delivering targeted decontamination, antidote administration, and supportive therapies to mitigate organ damage. The market further encompasses respiratory emergencies, including laryngeal paralysis and congestive heart failure exacerbations, where oxygen therapy, thoracocentesis, and pharmacologic intervention restore stability.

By November 2025, MedVet expanded its footprint by launching new multi-specialty and emergency hospitals in Atlanta, Austin, and Phoenix. These facilities emphasize a veterinarian-led ownership structure, offering an alternative approach to the increasing corporate consolidation across the North American veterinary care market while maintaining clinical autonomy.

Veterinary emergency care providers pursue opportunities to integrate advanced diagnostic and monitoring technologies, expanding applications in 24/7 critical care where continuous telemetry and point-of-care ultrasound improve real-time decision-making for unstable patients.

These advancements support development of tiered care models that range from urgent care to full intensive care units, accommodating varying acuity levels and optimizing resource allocation. In December 2025, Serenity Vet Inc. introduced a subscription-based relief management platform designed to address ongoing staffing shortages.

The system enables emergency veterinary hospitals to efficiently manage networks of relief veterinarians, ensuring consistent 24/7 service availability and reducing operational disruptions.

Recent trends emphasize veterinarian-led ownership models, technology-enabled staffing solutions, and integrated multi-specialty emergency centers, positioning the market for growth in resilient, high-quality emergency veterinary services focused on rapid intervention, clinical excellence, and sustainable operational models.

Key Takeaways

- In 2025, the market generated a revenue of US$ 22.1 Billion, with a CAGR of 6.0%, and is expected to reach US$ 39.6 Billion by the year 2035.

- The service type segment is divided into emergency consultation, trauma and injury care, poisoning and toxicity management, critical care and monitoring, surgical emergency services, diagnostic imaging and others, with emergency consultation taking the lead with a market share of 28.5%.

- Considering animal type, the market is divided into companion animals, livestock animals, equine and others. Among these, companion animals held a significant share of 68.6%.

- Furthermore, concerning the end user segment, the market is segregated into pet owners, veterinary hospitals, animal shelters and others. The pet owners sector stands out as the dominant player, holding the largest revenue share of 58.3% in the market.

- North America led the market by securing a market share of 38.4%.

Service Type Analysis

Companion animals accounted for 68.6% of growth within animal type and dominate the veterinary emergency care market due to the rising global pet population and increasing emotional attachment between owners and pets. Dogs and cats frequently experience acute conditions such as injuries, poisoning, infections, and sudden illnesses that require immediate medical attention.

Veterinary reports indicate that companion animals represent the majority of emergency visits, which strengthens demand for urgent care services. This segment is expected to expand as pet ownership continues to rise across urban and suburban regions.

Pet owners are likely to seek immediate treatment for emergencies to ensure survival and reduce complications. The segment benefits from growing awareness of animal health and increased spending on pet care.

Emergency services are projected to become more accessible as veterinary infrastructure improves. As pets are increasingly treated as family members, companion animals are estimated to maintain their dominant position in this market.

Animal Type Analysis

Emergency consultation accounted for 28.5% of growth within service type and dominates the veterinary emergency care market due to its role as the first point of contact during urgent situations. Pet owners often seek immediate professional advice when animals show sudden symptoms such as distress, injury, or abnormal behavior.

Emergency consultations help veterinarians assess severity and determine appropriate treatment pathways quickly. This service is expected to grow as awareness of emergency veterinary care increases. Clinics are likely to offer 24/7 consultation services to meet rising demand.

The segment benefits from the need for rapid diagnosis and decision-making in critical situations. Increasing use of tele-veterinary consultations is projected to support accessibility. As early intervention remains crucial in emergency care, this segment is anticipated to retain its leading position.

End-User Analysis

Pet owners accounted for 58.3% of growth within end user and dominate the veterinary emergency care market due to their direct responsibility for seeking and financing emergency treatment for animals. Pet owners actively pursue immediate care when pets face life-threatening conditions, which drives demand for emergency services.

Rising disposable income and willingness to spend on pet healthcare strengthen this segment. Pet owners are expected to continue leading as awareness of emergency care options improves. They are likely to prioritize quick access to veterinary services to ensure better outcomes.

The segment benefits from increasing pet insurance adoption and improved veterinary accessibility. As the humanization of pets continues to grow, pet owners are estimated to maintain their dominant share in the veterinary emergency care market.

Key Market Segments

By Service Type

- Emergency Consultation

- Trauma and Injury Care

- Poisoning and Toxicity Management

- Critical Care and Monitoring

- Surgical Emergency Services

- Diagnostic Imaging

- Others

By Animal Type

- Companion Animals

- Livestock Animals

- Equine

- Others

By End User

- Pet Owners

- Veterinary Hospitals

- Animal Shelters

- Others

Drivers

Growth in companion animal populations and pet humanization trends is driving the Veterinary Emergency Care market.

The continued rise in pet ownership has intensified the requirement for immediate, specialized intervention when acute medical situations arise outside regular clinic hours. Households increasingly regard companion animals as integral family members, prompting swift action during traumatic injuries, toxin exposures, or sudden illnesses rather than deferring treatment.

Data from the American Veterinary Medical Association indicate sustained high levels of dog and cat populations in the United States throughout the 2022–2025 period, supporting elevated baseline demand for urgent services. Pet owners demonstrate greater willingness to pursue advanced diagnostics and critical interventions, even at elevated costs, reflecting emotional attachment and perceived value of timely care.

This behavioral shift contributes to higher utilization of 24-hour facilities and emergency departments within veterinary hospitals. Expansion of urban and suburban pet demographics further concentrates cases in regions with established after-hours infrastructure.

Public awareness campaigns on pet safety and health risks reinforce the expectation of rapid response capabilities. Veterinary practices respond by extending operating hours or partnering with dedicated emergency providers to accommodate unpredictable caseloads.

These societal and demographic dynamics generate consistent procedural volumes across trauma, gastrointestinal, and respiratory emergencies. In summary, evolving owner attitudes combined with population growth establish a foundational impetus for sector advancement during the 2022–2025 timeframe.

Restraints

Escalating service costs and price sensitivity among pet owners are restraining the Veterinary Emergency Care market.

Substantial fees associated with after-hours diagnostics, stabilization, and intensive monitoring create financial barriers that influence decision-making for many households facing unexpected pet health crises. Veterinary service prices have outpaced general inflation in recent years, with notable increases observed in 2025 that moderated only slightly from prior peaks.

Annual veterinary care expenditures per household have risen, yet a declining proportion of owners report feeling financially prepared for major medical events. This sensitivity manifests in delayed presentations or selective pursuit of care, particularly among lower-income segments or those without insurance coverage.

Practices encounter challenges in balancing quality standards with affordability, occasionally resulting in deferred capital investments for specialized equipment. Smaller or independent facilities face disproportionate pressure when competing with larger networks that achieve economies of scale.

Reimbursement inconsistencies for emergency procedures further complicate revenue predictability. These economic realities contribute to moderated utilization rates despite underlying clinical need. Persistent household budget constraints therefore temper the pace of demand realization and infrastructure expansion across the sector.

Opportunities

Corporate consolidation and network expansion of specialized emergency facilities are creating growth opportunities in the Veterinary Emergency Care market.

Large-scale operators have accelerated the establishment of dedicated emergency and critical care centers, enabling standardized protocols, shared resources, and improved surge capacity across geographic regions. This model facilitates recruitment and retention of board-certified specialists in emergency and critical care medicine, enhancing service sophistication and outcome consistency.

Opportunities emerge for integrated referral networks that streamline transitions from primary care to intensive management, reducing fragmentation and supporting continuity. Expansion into underserved suburban and secondary urban markets broadens accessibility while addressing gaps in traditional provision.

Technology-enabled triage and remote consultation features complement physical facilities, optimizing staff deployment during peak or off-hours periods. Alignment with pet insurance growth provides a buffer against direct cost burdens, encouraging utilization of higher-acuity services.

Collaborative arrangements with general practices allow for efficient case handoffs and reciprocal support during high-volume intervals. These structural developments foster scalable operations and diversified revenue streams through bundled critical care packages.

Overall, consolidation-driven models unlock substantial potential for enhanced capacity, professional development, and geographic penetration within the emergency care ecosystem.

Impact of Macroeconomic / Geopolitical Factors

Economic and geopolitical forces are redefining how veterinary emergency care services expand, price their offerings, and manage operational capacity. Rising pet ownership and increasing willingness to spend on urgent animal care are strengthening demand for emergency interventions across both urban and semi-urban regions.

However, inflation is elevating treatment costs, staffing expenses, and facility overheads, which is making emergency care less accessible for cost-sensitive pet owners and creating revenue concentration among higher-income clients. Workforce shortages remain a structural constraint, limiting service availability and increasing wait times in critical situations.

Geopolitical instability is adding further complexity by disrupting supply chains for medical equipment and pharmaceuticals, which affects timely care delivery in emergency settings. Current US tariffs on imported medical devices, diagnostic tools, and electronic components are increasing capital expenditure for veterinary hospitals, which forces providers to adjust pricing or delay infrastructure expansion.

These pressures can restrict access in underserved areas and slow the rollout of advanced emergency facilities. At the same time, providers are responding by investing in localized supply chains, mobile emergency units, and tele-triage systems to improve reach and efficiency.

In a broader perspective, despite short-term financial and operational strain, the essential nature of emergency care and growing pet humanization trends are expected to sustain long-term market resilience.

Latest Trends

Emergence of hybrid urgent care models and extended-hour operations represents a recent trend in the Veterinary Emergency Care market.

Throughout 2024 and 2025, veterinary providers have introduced dedicated urgent care clinics positioned as an intermediate tier between routine appointments and full emergency departments, addressing non-life-threatening conditions during evenings and weekends. This approach alleviates overcrowding in traditional emergency settings while offering more predictable scheduling and cost structures for pet owners.

Corporate entities have expanded 24/7 networks through acquisitions and new site openings, incorporating advanced imaging and laboratory capabilities to support rapid diagnostics. Integration of telemedicine triage tools enables preliminary assessment and guidance, directing cases appropriately and optimizing in-facility resources.

Industry observations during this period note sustained demand for after-hours services amid broader trends of price sensitivity in wellness visits, with emergency and critical care volumes demonstrating relative resilience. Extended clinic hours in primary practices have also proliferated to mitigate gaps in local availability.

The trend aligns with workforce strategies that incorporate flexible scheduling and relief staffing to manage burnout while maintaining coverage. Prominent developments observed in 2024–2025 underscore a maturation toward tiered, technology-supported delivery frameworks that prioritize timely intervention without defaulting exclusively to high-intensity emergency environments.

Regional Analysis

North America is leading the Veterinary Emergency Care Market

North America accounted for 38.4% of the veterinary emergency care market in 2025, reflecting the region’s well-established network of 24/7 animal hospitals and growing reliance on specialized urgent care services for companion animals.

Pet owners across the United States are increasingly seeking immediate clinical intervention for trauma, poisoning, and acute medical conditions, supported by rising awareness and willingness to spend on advanced veterinary care.

Data from the American Pet Products Association indicates that overall pet industry expenditure surpassed USD 136 billion in 2022, underscoring strong financial commitment toward animal health services, including emergency treatment. Veterinary groups are expanding dedicated emergency and critical care units equipped with advanced diagnostics, surgical capabilities, and intensive monitoring systems.

Consolidation within veterinary service providers has also enabled the development of large multi-location emergency networks. Clinicians are adopting rapid diagnostic tools and triage protocols that improve response time and clinical outcomes. Workforce specialization in emergency and critical care medicine is further strengthening service quality.

Tele-triage services and digital consultation platforms are also emerging to support initial case assessment. These factors have collectively contributed to sustained expansion of urgent veterinary care services across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to register steady growth over the forecast period as veterinary infrastructure strengthens and demand for immediate animal care services rises across urban centers. Countries such as China, India, Japan, and Australia are witnessing increasing pet ownership alongside a shift toward professional veterinary care.

The World Organisation for Animal Health emphasizes the importance of accessible veterinary services in safeguarding animal welfare and public health, encouraging governments to expand clinical care capacity. Veterinary clinics across the region are gradually introducing emergency response capabilities, including after-hours services and critical care units.

Private hospital chains are investing in advanced equipment and skilled personnel to support complex case management. Urbanization and changing lifestyles are also contributing to higher incidence of accidental injuries and acute health conditions in pets.

Training programs are enhancing clinical expertise in emergency medicine and surgical intervention. Digital platforms are enabling faster communication between pet owners and veterinary professionals during urgent situations. These developments are expected to support continued expansion of veterinary emergency care services across Asia Pacific.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the Veterinary Emergency Care Market expand growth by establishing 24/7 emergency clinics, strengthening referral networks with general veterinary practices, and investing in advanced critical care infrastructure that supports rapid diagnosis and treatment.

Companies focus on expanding specialty services such as trauma care, intensive care units, and emergency surgery to address rising demand for urgent animal healthcare. They also integrate tele-triage platforms and digital communication tools that help pet owners access immediate guidance during emergencies.

Mars Veterinary Health represents a prominent participant in the Veterinary Emergency Care Market and operates as a global veterinary services provider that manages a wide network of animal hospitals, specialty clinics, and emergency care centers across multiple regions.

The company emphasizes high-quality clinical care, workforce development, and expanded service accessibility to improve patient outcomes. Industry competitors continue to open new emergency facilities, strengthen clinical capabilities, and invest in advanced diagnostic technologies to support timely intervention and sustained market growth.

Top Key Players

- VCA Animal Hospitals

- Banfield Pet Hospital

- BluePearl Pet Hospital

- MedVet Medical & Cancer Centers for Pets

- Pet+ER

- Veterinary Emergency Group

- Animal Emergency & Referral Center

- DoveLewis Emergency Animal Hospital

- Pittsburgh Veterinary Specialty & Emergency Center

- Schwarzman Animal Medical Center

- Thrive Pet Healthcare

Recent Developments

- In March 2025, Portland Veterinary Emergency and Specialty Care announced the development of a 42,000-square-foot facility in Falmouth, expected to open in Spring 2026. This expansion reflects a broader industry shift toward large-scale veterinary “super-hospitals” that combine emergency care with specialized services such as sports medicine and oncology under one roof, improving patient outcomes and operational efficiency.

- Throughout late 2024 and 2025, BluePearl, part of Mars Veterinary Health, focused on upgrading and expanding its existing infrastructure. Its Grand Rapids medical center, opened in October 2025, doubled its size to approximately 29,000 square feet to meet growing demand for round-the-clock emergency services and advanced diagnostic capabilities, including imaging and critical care.

- In August 2025, Terravet Real Estate Solutions acquired the property of Dogwood Veterinary Specialty & Emergency for $3.33 million. This transaction highlights a growing trend of real estate investment in high-acuity veterinary emergency facilities, which are increasingly viewed as stable, recession-resistant assets due to their essential services and steady revenue streams.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 22.1 Billion |

| Forecast Revenue (2035) | US$ 39.6 Billion |

| CAGR (2026-2035) | 6.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Service Type (Emergency Consultation, Trauma and Injury Care, Poisoning and Toxicity Management, Critical Care and Monitoring, Surgical Emergency Services, Diagnostic Imaging and Others), By Animal Type (Companion Animals, Livestock Animals, Equine and Others), By End User (Pet Owners, Veterinary Hospitals, Animal Shelters and Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, The U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | VCA Animal Hospitals, Banfield Pet Hospital, BluePearl Pet Hospital, MedVet Medical & Cancer Centers for Pets, Pet+ER, Veterinary Emergency Group, Animal Emergency & Referral Center, DoveLewis Emergency Animal Hospital, Pittsburgh Veterinary Specialty & Emergency Center, Schwarzman Animal Medical Center, Thrive Pet Healthcare. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |