Quick Navigation

- Report Overview

- Key Takeaways

- Business Benefits of Veggie Meals

- By Type Analysis

- By Meal Type Analysis

- By Ingredient Type Analysis

- By Cuisine Analysis

- By Storage Analysis

- By End-User Analysis

- By Distribution Channel Analysis

- Key Market Segments

- Driving Factors

- Restraining Factors

- Growth Opportunity

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

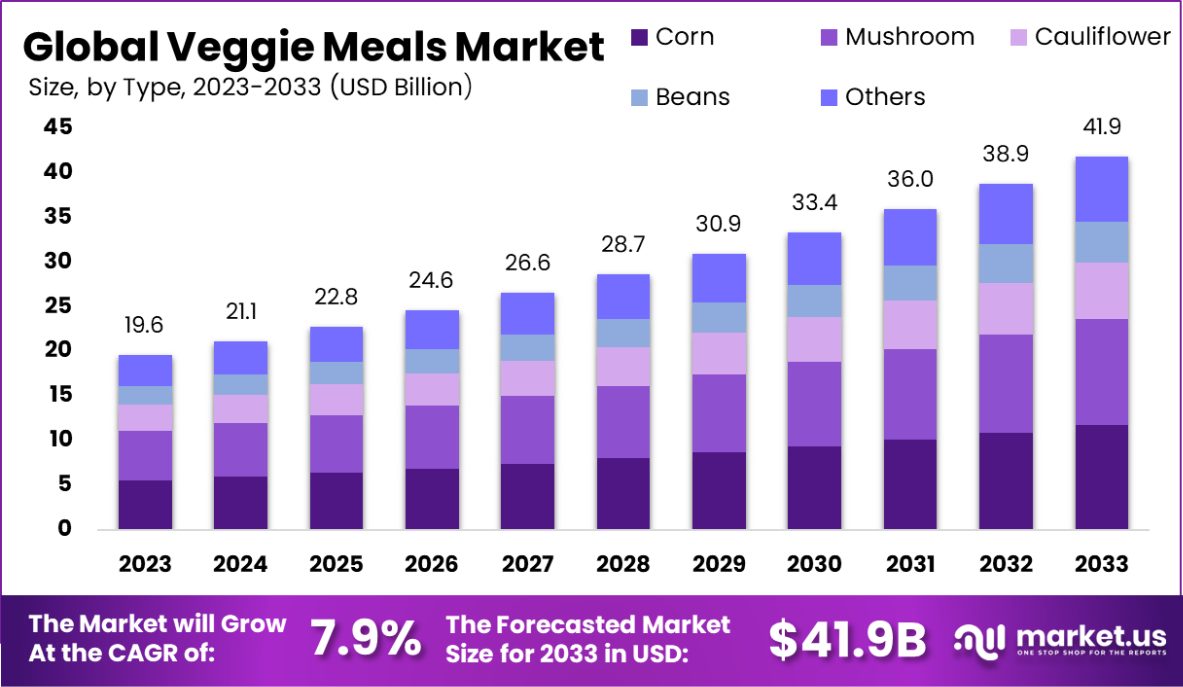

The Global Veggie Meals Market is expected to be worth around USD 41.9 Billion by 2033, up from USD 19.6 Billion in 2023, and grow at a CAGR of 7.9% from 2024 to 2033. Asia-Pacific dominates Veggie Meals Market with 42.7%, USD 8.4 Bn.

The veggie meals market is experiencing a robust surge in demand, driven by shifting consumer preferences toward healthier and sustainable food options. This market encompasses a diverse range of plant-based meal solutions, including ready-to-eat products, meal kits, and frozen food meals that cater to a growing demographic seeking alternatives to traditional meat-based diets.

Industrially, the veggie meals market is characterized by strong competition, with established food brands competing against innovative startups. The sector has witnessed an influx of investment as companies strive to develop products that mimic the taste, texture, and nutritional profile of conventional meals while leveraging plant-based ingredients.

Several factors are driving the expansion of the veggie meals market. Chief among them is the increasing awareness of health-related issues such as obesity, heart disease, and diabetes, which has prompted consumers to adopt plant-centric diets.

Furthermore, the global push toward reducing carbon footprints has motivated many individuals to reduce meat consumption. Governments and organizations are also endorsing these shifts by introducing initiatives and policies that promote plant-based eating.

Emerging trends in the market include the rising demand for clean-label products free from artificial additives and preservatives. Consumer preference for organic, non-GMO, and gluten-free veggie meals is on the rise, creating opportunities for manufacturers to innovate.

Additionally, there is a growing focus on cultural and regional flavors in veggie meal offerings, aiming to cater to diverse palates. The integration of functional ingredients such as protein, fiber, and vitamins has also gained momentum, allowing manufacturers to position their products as complete nutritional solutions.

The veggie meals market is experiencing a significant transformation, driven by growing consumer demand for sustainable, plant-based food options. Rising health consciousness, coupled with environmental and ethical concerns, has spurred the adoption of vegetarian and vegan diets.

This shift has catalyzed growth in the market, projected to achieve a CAGR of over 8% from 2023 to 2030, with its valuation expected to surpass $25 billion by the end of the decade.

Regions like North America and Europe remain dominant due to mature plant-based ecosystems, while Asia-Pacific emerges as a high-growth region fueled by urbanization and changing dietary habits.

Supporting this growth is the increasing inclusion of veggie meals in institutional food programs. For instance, during the 2023-2024 school year, Virginia public schools served 65.3 million breakfasts and 117.5 million lunches through the National School Lunch Program (NSLP) and School Breakfast Program (SBP), with 51.2 million free breakfasts and 79.9 million free lunches claimed, demonstrating rising adoption rates.

Furthermore, 90 of Virginia’s 131 school divisions fully participated in the Community Eligibility Provision (CEP), underscoring the systemic integration of veggie meal options. This trend reflects broader opportunities for manufacturers and policymakers to capitalize on the increasing alignment of nutrition, accessibility, and sustainability in institutional meal programs.

Key Takeaways

- The Global Veggie Meals Market is expected to be worth around USD 41.9 Billion by 2033, up from USD 19.6 Billion in 2023, and grow at a CAGR of 7.9% from 2024 to 2033.

- Corn dominates with a 27.4% market share, reflecting its versatility and affordability.

- Ready-to-eat meals lead with 54.5%, driven by convenience and busy consumer lifestyles.

- Non-organic options comprise 75.3% of the market, appealing to cost-conscious consumers globally.

- Asian cuisine holds a 37.2% share, benefiting from bold flavors and cultural adaptability.

- Refrigerated veggie meals account for 65.2%, highlighting the demand for fresh and premium-quality offerings.

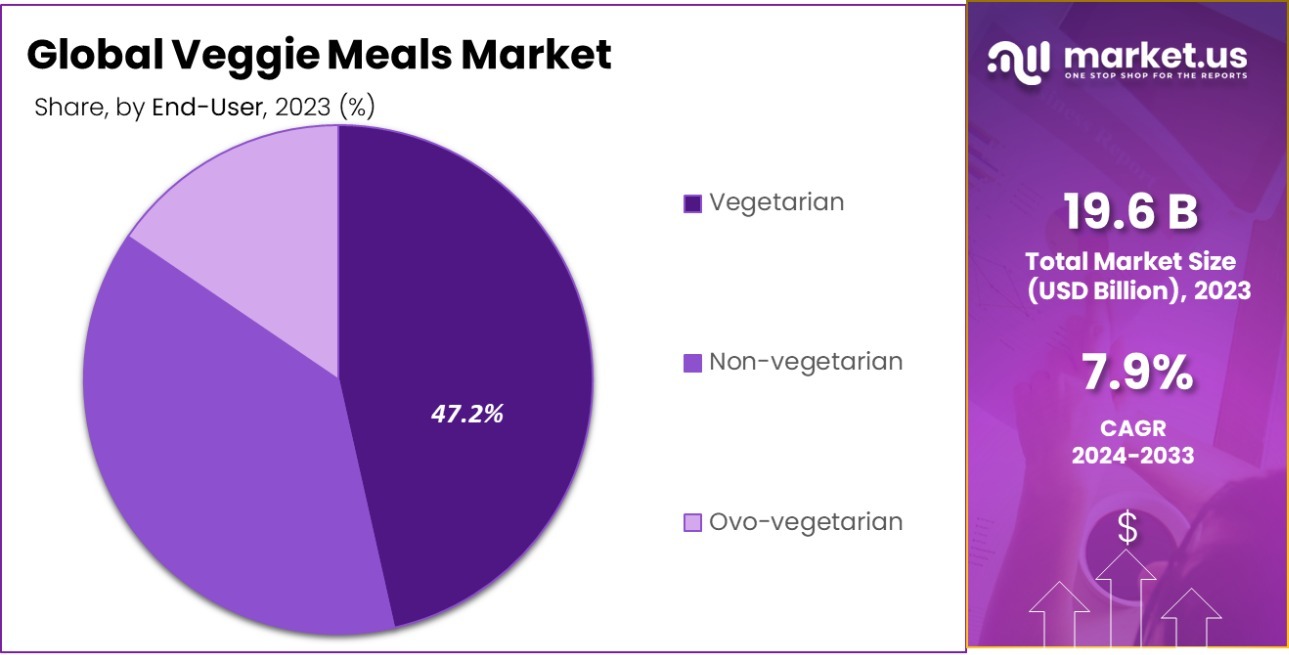

- Vegetarians represent 47.2% of the market, underscoring significant adoption beyond fully vegan demographics.

- Supermarkets and hypermarkets dominate with 53.4%, preferred for accessibility and diverse product assortments.

- The Asia-Pacific Veggie Meals Market holds 42.7%, valued at USD 8.4 billion.

Business Benefits of Veggie Meals

Veggie meals offer significant business benefits, aligning with evolving consumer preferences and global trends toward health and sustainability. One of the primary advantages is catering to the growing demand for plant-based diets.

This shift is driven by health-conscious consumers seeking nutritious, low-fat alternatives to meat, providing businesses with a lucrative opportunity to tap into this expanding market.

Veggie meals also appeal to a broader audience, including vegetarians, vegans, flexitarians, and even non-vegetarians looking to reduce meat consumption. This inclusivity enables businesses to target diverse consumer segments, enhancing customer loyalty and brand appeal.

From a production perspective, veggie meals are often more cost-effective compared to meat-based products, as plant-based ingredients require fewer resources like water and land. This not only reduces production costs but also aligns businesses with sustainable practices, improving their environmental, social, and governance (ESG) credentials.

Additionally, offering veggie meals helps businesses stay competitive in an industry where innovation and differentiation are key. Creative recipes and diverse cuisines attract health-conscious and adventurous eaters alike.

By Type Analysis

Corn dominates the market with a share of 27.4%, highlighting versatility.

In 2023, Corn held a dominant market position in the “By Type” segment of the Veggie Meals Market, with a 27.4% share. This prominence can be attributed to its versatile application in various cuisines and the increasing demand for plant-based food products.

Following closely, mushrooms accounted for 21.3% of the market, appreciated for their meat-like texture and flavor, which appeals to both vegetarians and non-vegetarians seeking healthier meal options.

Cauliflower captured a 19.2% market share, driven by its use as a low-carb substitute in numerous traditional dishes, which has become particularly popular among consumers adhering to ketogenic and paleo diets.

Beans held an 18.1% share, favored for their high protein content and role in numerous traditional and modern recipes. The preference for these vegetables is influenced by growing health consciousness, the rising vegan population, and the global shift towards sustainable eating practices.

The varied applications of these vegetables in ready-to-eat and easy-to-prepare formats further bolster their standing in the market, reflecting consumer preferences for convenience combined with nutritional benefits.

By Meal Type Analysis

Ready-to-eat meals lead with 54.5%, reflecting consumer convenience preferences.

In 2023, Ready-to-Eat Meals held a dominant market position in the “By Meal Type” segment of the Veggie Meals Market, with a 54.5% share. This segment’s robust performance is driven by consumer preferences for convenience and time-saving options in their daily routines.

Following Ready-to-Eat Meals, Frozen Meals captured a significant portion of the market, holding a 30.2% share. This segment benefits from the prolonged shelf life of frozen products and the perception of retaining nutritional value, which appeals to health-conscious consumers.

Home-Cooked Meal kits and ingredients, designed to offer the experience and satisfaction of cooking without the hassle of extensive preparation, accounted for 15.3% of the market. The dominance of Ready-to-Eat Meals underscores the shifting dynamics within the Veggie Meals Market, where efficiency and minimal preparation time are increasingly prioritized by consumers.

This trend is further bolstered by the rising number of single-person households and the busy lifestyles of urban dwellers, making convenient meal solutions more appealing. Overall, the growth within this segment reflects a broader consumer shift towards plant-based diets, coupled with a demand for quicker, healthier, and easy-to-prepare food options.

By Ingredient Type Analysis

Non-organic ingredients capture 75.3%, driven by cost-effectiveness and accessibility.

In 2023, Non-Organic held a dominant market position in the “By Ingredient Type” segment of the Veggie Meals Market, with a 75.3% share. This substantial market presence can be attributed to the generally lower price point of non-organic ingredients compared to their organic counterparts, making them more accessible to a broader consumer base.

Organic ingredients, while growing in popularity due to increasing health awareness and environmental concerns, captured 24.7% of the market.

The preference for non-organic ingredients is further supported by their widespread availability and extensive variety, which cater to the diverse culinary needs and preferences of consumers. Despite the growing trend towards organic produce, the higher cost and limited availability of these options in certain regions continue to restrain their market share.

However, the gap between organic and non-organic segments may narrow as consumer preferences shift towards more sustainable and health-conscious eating options. Increasing awareness of the benefits associated with organic farming and the rising incidence of dietary restrictions are factors that could drive a gradual increase in the market share of organic ingredients in the coming years.

By Cuisine Analysis

Asian cuisine holds 37.2%, appealing to diverse and expanding global taste preferences.

In 2023, Asian cuisine held a dominant market position in the “By Cuisine” segment of the Veggie Meals Market, with a 37.2% share. This leadership can be attributed to the widespread popularity of Asian dishes, known for their rich flavors and versatile use of plant-based ingredients like tofu, soy, and vegetables, appealing to both vegetarians and flexitarians globally.

Indian cuisine followed closely, accounting for 29.8% of the market. Its significant share is driven by a long-standing tradition of vegetarianism in Indian culture and the use of spices and pulses to create flavorful meals.

Mexican cuisine captured a 20.1% share, leveraging its appeal for bold flavors and the adaptability of dishes like burritos, tacos, and enchiladas to vegetarian formats. Italian cuisine held a 12.9% share, supported by the popularity of pasta, pizza, and risotto, which are easily customizable to plant-based options.

The dominance of Asian cuisine reflects a global preference for diverse and exotic flavors, coupled with the increasing acceptance of traditional Asian ingredients in Western markets. Additionally, the growth of Indian and Mexican cuisines highlights a consumer shift toward ethnic foods that align with the rising trend of plant-based and sustainable eating.

By Storage Analysis

Refrigerated veggie meals dominate at 65.2%, ensuring freshness and extended product shelf life.

In 2023, Refrigerated products held a dominant market position in the “By Storage” segment of the Veggie Meals Market, with a 65.2% share. This segment’s leadership can be attributed to the rising consumer demand for fresh, high-quality meals with minimal preservatives.

Refrigerated veggie meals are perceived as healthier and more natural, aligning with the growing preference for clean-label products. Additionally, advancements in cold-chain logistics have enhanced the distribution of these products, ensuring freshness and longer shelf life.

Shelf-stable products accounted for 34.8% of the market, driven by their convenience and longer storage periods without refrigeration. These products are particularly popular among consumers in regions with limited access to refrigeration facilities or for those seeking portable meal solutions. The shelf-stable segment benefits from innovations in packaging and preservation techniques that retain nutritional value and flavor.

The dominance of the refrigerated segment highlights the increasing importance of freshness and quality in consumer purchasing decisions. However, the shelf-stable segment remains a significant contributor, catering to the needs of busy urban consumers and those in areas with inadequate cold storage infrastructure.

By End-User Analysis

Vegetarians account for 47.2%, showcasing the growing plant-based diet adoption.

In 2023, Vegetarian consumers held a dominant market position in the “By End-User” segment of the Veggie Meals Market, with a 47.2% share. This leadership reflects the rising popularity of plant-based diets among health-conscious individuals and those adopting sustainable eating practices.

The vegetarian segment benefits from increasing awareness of the environmental impact of meat consumption and the health advantages associated with a vegetarian diet, such as reduced risks of chronic diseases.

Non-vegetarian consumers accounted for 36.5% of the market, highlighting the growing appeal of veggie meals among flexitarians who seek to reduce meat intake without eliminating it. This trend is driven by a broader acceptance of plant-based alternatives as complementary meal options that align with health and environmental goals.

Ovo-vegetarian consumers, those who include eggs in their vegetarian diet, represented 16.3% of the market. This niche segment is gaining traction due to its focus on high-protein meal options and the versatility of eggs in vegetarian recipes.

The dominance of vegetarian end-users underlines the global shift toward plant-based eating, with flexitarian and ovo-vegetarian groups contributing to market growth by expanding the consumer base. This diverse appeal ensures sustained demand across varying dietary preferences and lifestyles.

By Distribution Channel Analysis

Supermarkets and hypermarkets lead at 53.4%, offering convenience and product variety.

In 2023, Supermarkets and Hypermarkets held a dominant market position in the “By Distribution Channel” segment of the Veggie Meals Market, with a 53.4% share. These retail outlets remain the preferred choice for consumers due to their wide product variety, competitive pricing, and convenient one-stop shopping experience.

Their ability to showcase veggie meals in prominent sections, supported by promotional activities and discounts, has further solidified their market leadership.

Convenience Stores accounted for 19.2% of the market, catering to urban consumers seeking quick and easily accessible meal options. These stores benefit from their proximity to residential and office areas, making them a popular choice for on-the-go purchases.

Specialty Stores held a 15.6% share, driven by their focus on premium, organic, and niche veggie meal offerings. These stores attract a dedicated consumer base that prioritizes quality and specific dietary requirements, such as gluten-free or vegan options.

Online Stores captured 11.8% of the market, reflecting the growing trend of e-commerce in food retail. The convenience of home delivery, availability of diverse brands, and subscription models for regular purchases contribute to the segment’s steady growth.

Key Market Segments

By Type

- Corn

- Mushroom

- Cauliflower

- Beans

- Others

By Meal Type

- Ready-to-Eat Meals

- Frozen Meals

- Home-Cooked Meals

By Ingredient Type

- Organic

- Non-Organic

By Cuisine

- Asian

- Indian

- Mexican

- Italian

By Storage

- Refrigerated

- Shelf-stable

By End-User

- Vegetarian

- Non-vegetarian

- Ovo-vegetarian

By Distribution channel

- Supermarket and Hypermarket

- Convenience stores

- Specialty Stores

- Online Stores

- Others

Driving Factors

Growing Demand for Plant-Based Diets Globally

The increasing preference for plant-based diets is a key driver in the Veggie Meals Market. Consumers are shifting toward healthier and sustainable eating habits, fueled by concerns over the environmental impact of meat production and the health benefits of vegetarian meals.

Rising awareness about chronic diseases, such as obesity and heart conditions, has further accelerated this trend. Additionally, the growing vegan and flexitarian population worldwide, supported by innovative plant-based meal offerings, is expanding the market’s consumer base significantly.

Convenience of Ready-to-Eat and Frozen Veggie Meals

The demand for convenient food options is boosting the growth of the Veggie Meals Market. Busy urban lifestyles and rising disposable incomes have made ready-to-eat and frozen veggie meals a preferred choice for many consumers. These products offer time-saving solutions without compromising on nutrition and taste.

Advancements in packaging and preservation technologies have enhanced the shelf life and quality of these meals, making them accessible to a wider audience and contributing to the market’s steady growth.

Increasing Availability Through Diverse Retail Channels

The expansion of retail channels is driving the Veggie Meals Market’s growth. Supermarkets, hypermarkets, and specialty stores are prominently showcasing veggie meals to meet rising consumer demand. Additionally, the rapid growth of e-commerce platforms is making these products more accessible to a tech-savvy consumer base.

Promotional campaigns, discounts, and subscription models offered by retailers are further encouraging purchases, ensuring a broader reach across various demographics and contributing to sustained market expansion.

Restraining Factors

High Cost of Premium Veggie Meals is Restraining

The elevated cost of premium veggie meals is a significant restraint in the market. Organic and specialty plant-based ingredients often come with higher production and procurement costs, leading to expensive end products.

This pricing limits accessibility, particularly for cost-sensitive consumers in emerging economies. While awareness of health benefits is increasing, affordability remains a critical barrier, hindering wider adoption. Bridging this price gap will be crucial to expanding the market’s reach and overcoming this challenge.

Limited Availability in Rural and Remote Areas

The restricted distribution of veggie meals in rural and remote regions is restraining the market’s growth. Supply chain limitations, lack of refrigeration infrastructure, and lower awareness among rural populations contribute to limited accessibility.

Urban areas dominate sales, while rural consumers often rely on traditional diets. Expanding distribution networks and creating affordable options tailored for these regions are essential steps to address this challenge and unlock untapped market potential.

Consumer Perception of Taste and Satisfaction

A portion of the consumer base perceives veggie meals as lacking in taste or not as filling as traditional meat-based options. This misconception acts as a barrier to adoption, particularly among non-vegetarians.

Overcoming this restraint requires continuous innovation in flavor profiles, textures, and meal variety to match or exceed consumer expectations. Educating consumers about the taste and nutritional equivalence of veggie meals will also play a key role in addressing this challenge.

Growth Opportunity

Expansion into Emerging Economies Boosting Market Growth

Emerging economies present significant growth opportunities for the Veggie Meals Market. Rising disposable incomes and increasing urbanization in regions like Asia-Pacific and Latin America are driving demand for convenient and healthy meal options.

Additionally, growing awareness about plant-based diets and government initiatives promoting sustainable food practices are further supporting market expansion. Establishing affordable and culturally adapted veggie meal offerings in these regions can unlock vast untapped potential, making emerging markets a key focus for manufacturers and retailers.

Innovation in Product Varieties to Capture New Consumers

Product innovation offers a promising opportunity for growth in the Veggie Meals Market. Developing new flavors, textures, and meal formats can attract a broader audience, including non-vegetarians and flexitarians. Incorporating global cuisines and catering to specific dietary preferences, such as gluten-free or high-protein meals, can enhance market appeal.

Brands investing in research and development to meet diverse consumer expectations and launching creative marketing campaigns stand to gain a competitive advantage and expand their consumer base.

Growth of Online Channels Expanding Market Reach

The rapid growth of e-commerce platforms provides significant opportunities for the Veggie Meals Market. Online channels allow brands to reach a wider, tech-savvy audience while offering the convenience of home delivery and subscription services. Leveraging digital marketing and social media can enhance product visibility and drive sales.

Additionally, partnerships with online grocery platforms and food delivery services can further boost market penetration, making online channels a key area for future growth and investment.

Latest Trends

Increasing Demand for Plant-Based Protein Alternatives

The rising popularity of plant-based protein alternatives is a key trend in the Veggie Meals Market. Consumers are actively seeking protein-rich options derived from peas, lentils, and soy to meet their nutritional needs. This trend is driven by growing health consciousness and environmental concerns, particularly among flexitarians and millennials.

Manufacturers are responding with innovative products that mimic the taste and texture of traditional meat, enhancing their appeal across diverse consumer groups and positioning plant-based proteins as a market growth driver.

Organic and Clean Label Products Gaining Momentum

The preference for organic and clean-label veggie meals is growing as consumers become more health-conscious and environmentally aware. Products free from artificial additives, preservatives, and pesticides are highly sought after, with demand surging in both developed and emerging markets.

Brands emphasizing transparency and ethical sourcing practices are better positioned to capture this expanding consumer segment. This trend not only addresses health concerns but also aligns with the increasing focus on sustainability, creating opportunities for premium product lines in the market.

Fusion Cuisines Driving Innovation in Veggie Meals

Fusion cuisines are emerging as a popular trend in the Veggie Meals Market. Combining flavors and techniques from different culinary traditions, these meals cater to adventurous eaters and food enthusiasts. Examples include Asian-inspired veggie bowls, Mexican-Indian wraps, and Italian-style vegan pizzas.

This innovation not only enhances consumer interest but also expands the variety of options available, attracting a broader audience. Fusion cuisines reflect changing consumer preferences for diverse and exciting flavors, positioning them as a key driver of product development and market growth.

Regional Analysis

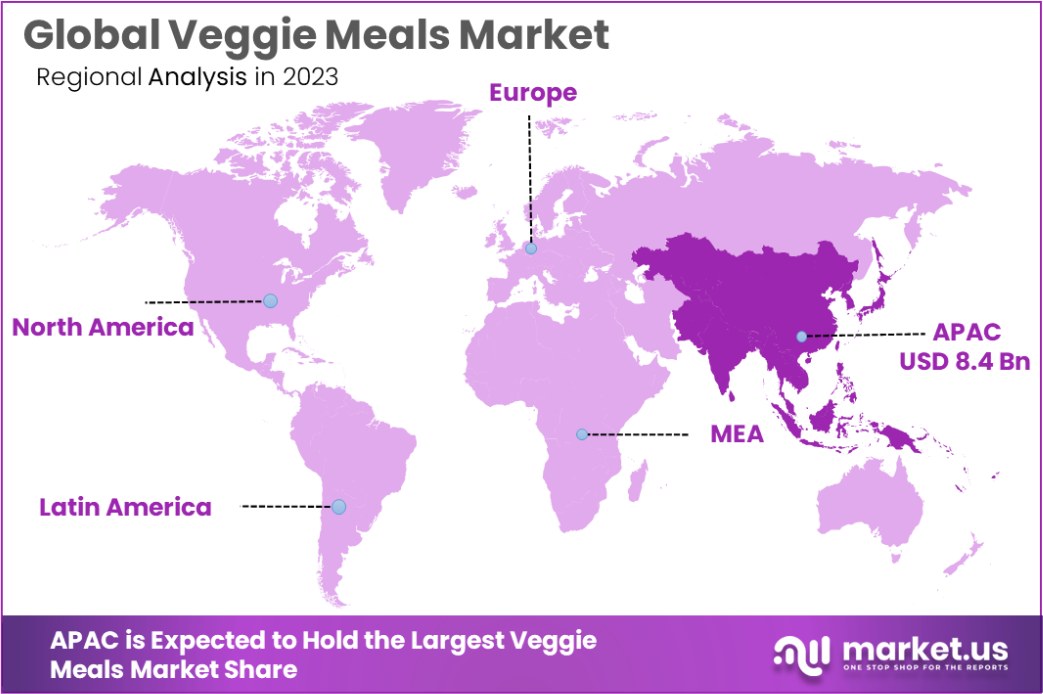

The Asia-Pacific region accounted for 42.7% of the Veggie Meals Market, valued at USD 8.4 billion.

In 2023, the Veggie Meals Market exhibited significant regional dynamics, with Asia-Pacific dominating the market with a 42.7% share, valued at USD 8.4 billion. This dominance is driven by the region’s large population base, increasing health consciousness, and rising adoption of plant-based diets, particularly in countries such as China, India, and Japan.

Rapid urbanization and growing disposable incomes further support the market growth in this region. North America holds the second-largest market share, fueled by the strong presence of vegan and flexitarian populations. The increasing popularity of plant-based protein alternatives and innovation in ready-to-eat veggie meals drive the market in the U.S. and Canada.

Europe also contributes significantly to the market, driven by stringent regulations promoting sustainable eating and the rising trend of organic and clean-label products. The region benefits from high consumer awareness and the presence of established players catering to a health-conscious demographic.

Latin America and the Middle East & Africa collectively represent emerging markets, with growth opportunities stemming from improving infrastructure and rising awareness of plant-based diets. The global expansion of retail and e-commerce channels further enables market penetration across all regions. Asia-Pacific’s leadership highlights the region’s pivotal role in shaping the future trajectory of the Veggie Meals Market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The global Veggie Meals Market in 2023 has witnessed significant contributions from leading companies, each leveraging unique strategies to cater to the growing demand for plant-based and vegetarian meal options. Amy’s Kitchen, a pioneer in organic and vegetarian meals, continues to capture consumer loyalty through its commitment to sustainability and clean-label products.

Beyond Meat and Impossible Foods are redefining the market with innovative plant-based meat alternatives, attracting flexitarians and non-vegetarians seeking healthier choices. Similarly, Gardein and Lightlife Foods have expanded their portfolios to include a diverse range of protein-rich veggie meals.

Traditional food giants like Nestlé S.A., Kellogg’s, and General Mills are strategically investing in plant-based product lines, capitalizing on their global distribution networks to enhance accessibility.

Brands like Green Giant and Healthy Choice focus on frozen veggie meals, catering to the convenience-driven consumer segment. Quorn Foods and Yves Veggie Cuisine emphasize high-protein options, meeting the nutritional demands of health-conscious customers.

Regional favorites, including Kitchens of India, InnovAsian Cuisine, and Thai Kitchen, have tapped into cultural and ethnic preferences to gain market share in Asia-Pacific and beyond. Companies such as Marie Callender’s and Stouffer’s leverage ready-to-eat meal solutions to address busy urban lifestyles.

Collaborations, product innovation, and sustainability initiatives remain key strategies among players like Unilever and McCain Food. As competition intensifies, these companies are driving market growth through technological advancements, targeted marketing, and diversified product offerings, shaping the global veggie meal landscape.

Top Key Players in the Market

- Amy’s Kitchen

- Beyond Meat

- Field Roast

- Gardein

- Veggies Made Great

- General Mills

- Great Value

- Green Giant

- Healthy Choice

- Impossible Foods

- InnovAsian Cuisine

- Kellogg’s

- Kitchens of India

- Knorr

- Lightlife Foods

- Marie Callender’s

- McCain Food

- Morning Star Farms

- Nasoya

- Praeger’s Sensible Foods

- Quorn Foods

- Stouffer’s

- Tasty Bite

- Thai Kitchen

- Tofurky

- Unilever

- Yves Veggie Cuisine Nestle S. A

Recent Developments

- In 2024, Beyond Meat introduced its fourth-generation Beyond Burger® and Beyond Beef® with improved taste and nutrition, achieving $81M in Q3 revenues (+7.6% from 2023) through strategic pricing, expanded distribution, and commitment to sustainability via its ESG initiatives.

- In 2023, Amy’s Kitchen, a leader in organic vegetarian meals, focused on sustainability 2023 with initiatives like a Regenerative Agriculture Pilot Project and consumer surveys. It reinforced its market presence by promoting inclusive, meat-free recipes, driving demand for plant-based options.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 19.6 Billion |

| Forecast Revenue (2033) | USD 41.9 Billion |

| CAGR (2024-2033) | 7.9% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Corn, Mushroom, Cauliflower, Beans, Others), By Meal Type (Ready-to-Eat Meals, Frozen Meals, Home-Cooked Meals), By Ingredient Type (Organic, Non-Organic), By Cuisine (Asian, Indian, Mexican, Italian), By Storage (Refrigerated, Shelf-stable), By End-User (Vegetarian, Non-vegetarian, Ovo-vegetarian), By Distribution channel (Supermarket and Hypermarket, Convenience stores, Specialty Stores, Online Stores, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Amy’s Kitchen, Beyond Meat, Field Roast, Gardein, Veggies Made Great, General Mills, Great Value, Green Giant, Healthy Choice, Impossible Foods, InnovAsian Cuisine, Kellogg’s, Kitchens of India, Knorr, Lightlife Foods, Marie Callender’s, McCain Food, Morning Star Farms, Nasoya, Praeger’s Sensible Foods, Quorn Foods, Stouffer’s, Tasty Bite, Thai Kitchen, Tofurky, Unilever, Yves Veggie Cuisine Nestle S. A |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |