Quick Navigation

Report Overview

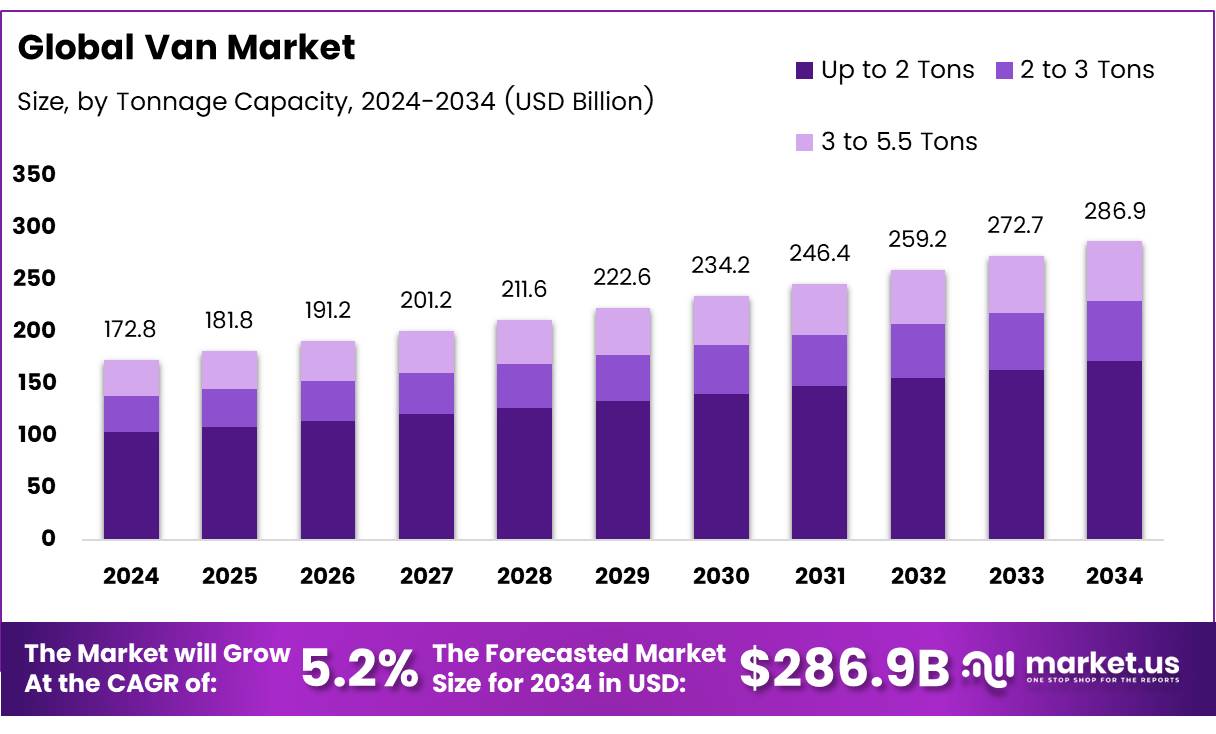

The Global Van Market size is expected to be worth around USD 286.9 Billion by 2034, from USD 172.8 Billion in 2024, growing at a CAGR of 5.2% during the forecast period from 2025 to 2034.

The van market encompasses a range of personal and commercial vehicles designed for the transport of goods and people. This sector is integral to the logistics and transportation industries, playing a crucial role in both urban and rural settings.

Vans vary in size, capacity, and powertrain, including conventional internal combustion engines as well as increasingly popular electric models. The versatility of vans makes them essential for businesses such as courier services, construction firms, and home service providers, as well as for personal use by individuals requiring spacious transportation solutions.

The van market presents several growth opportunities driven by both technological advancements and changing regulatory landscapes. The integration of electric vehicles (EVs) into commercial fleets is accelerating, supported by governmental investments and stringent emissions regulations.

For instance, since the onset of 2024, a significant uptick in electric van sales in the UK highlights a shift towards more sustainable commercial transport solutions. According to logistics data, electric vans constituted 4.8% of all new van sales in the UK during this period. Additionally, the presence of over 4.1 million vans on UK roads underscores the substantial market size and potential for further penetration of electric models as per Cambriancards.

The van market is poised for substantial growth, particularly in the electric vehicle segment. Norway, a leader in electric vehicle adoption, saw its registered electric vans increase to over 29,600 vehicles in 2023, up significantly from about 21,700 the previous year as per Study. This growth trajectory is supported by both consumer demand for greener alternatives and government incentives aimed at reducing carbon footprints.

The expanding infrastructure for EVs, such as increased charging stations and improved battery technologies, further enhances the attractiveness of electric vans for business use.

Government policies play a pivotal role in shaping the van market. Investments in EV infrastructure, such as charging stations and grid enhancements, are crucial for supporting the transition from diesel and gasoline-powered vans to electric variants.

Additionally, governments are implementing stricter emissions standards to combat climate change, which compels manufacturers to innovate and produce more environmentally friendly vehicles. These regulations not only encourage the adoption of electric vehicles but also open up new markets for van manufacturers and fleet operators looking to comply with new standards and capitalize on governmental incentives.

Key Takeaways

- Global van market projected to reach USD 286.9 billion by 2034, with a CAGR of 5.2% from 2025-2034.

- Up to 2 tons van category led the By Tonnage Capacity Analysis segment with 47.2% market share in 2024.

- Internal Combustion Engine (ICE) models dominated the propulsion segment with 62.7% market share in 2024.

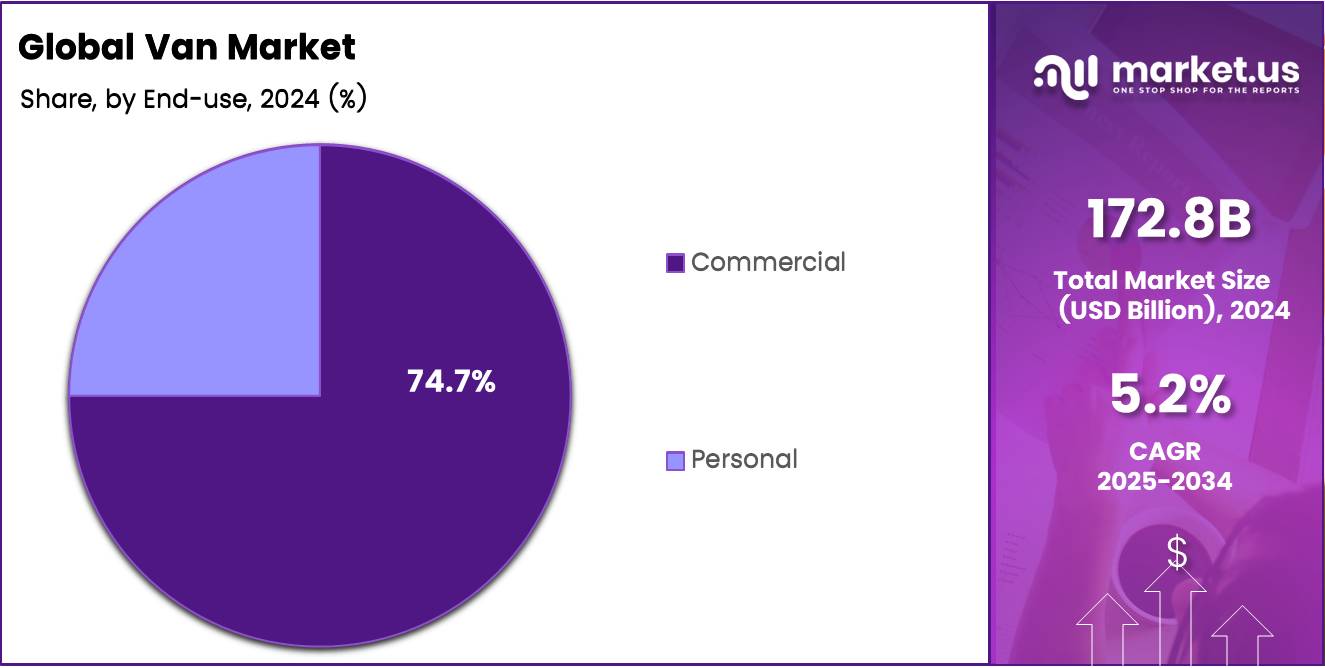

- Commercial vans dominated the end-use segment with a 74.7% share in 2024.

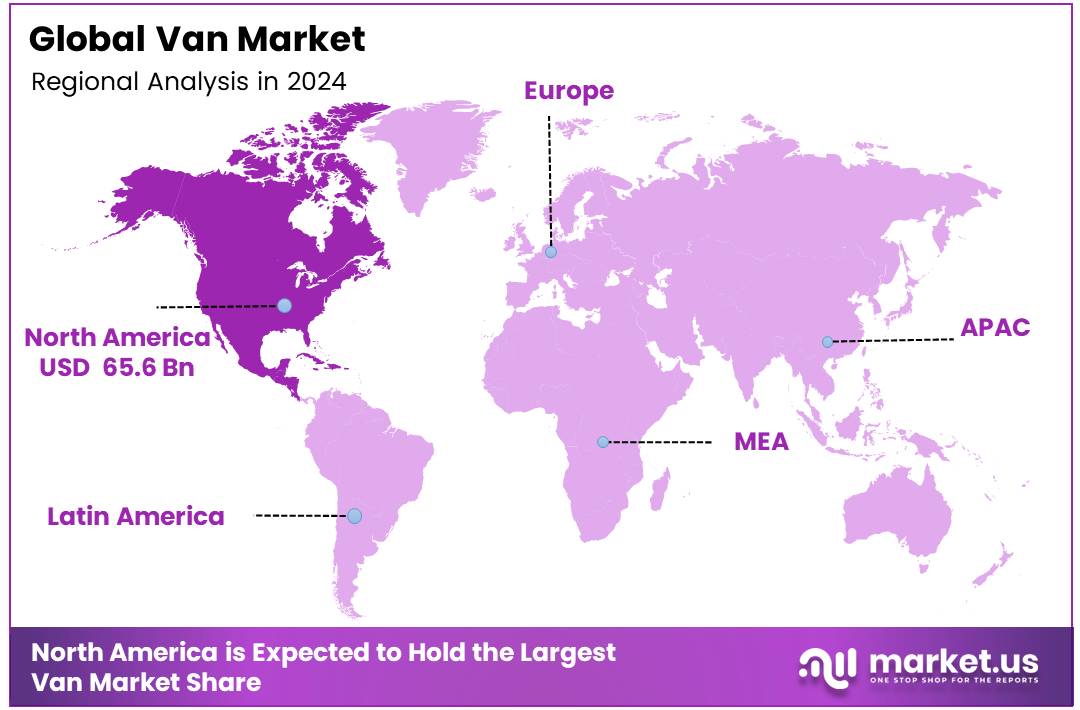

- North America led regional markets with 38.1% share, valued at USD 65.6 billion in 2024.

Tonnage Capacity Analysis

Small Vans Lead with 47.2% of the Market Share in Tonnage Capacity

In 2024, the By Tonnage Capacity Analysis segment of the van market was significantly led by the Up to 2 Tons category, capturing a 47.2% market share. This category’s dominance is largely attributed to the increasing demand for compact and fuel-efficient vehicles, especially in urban areas where navigation through congested streets is a daily challenge. Small businesses favor these vans due to their cost-effectiveness and lower operational costs, including maintenance and fuel.

The 2 to 3 Tons segment followed, with these medium-sized vans favored for their versatility in handling slightly heavier loads while still maintaining reasonable maneuverability and fuel efficiency. This segment is particularly popular among businesses that require a balance between load capacity and ease of driving, which is essential for regional deliveries.

Larger vans, categorized under 3 to 5.5 Tons, are utilized by businesses needing substantial cargo space and the ability to transport heavier goods. Although they are less fuel-efficient, their necessity in industries like construction and large-scale retail ensures a steady demand. This segment’s growth is driven by the need for robust transportation solutions in sectors that are less sensitive to fuel price fluctuations and more focused on payload capacity.

Propulsion Analysis

ICE Vans Lead the Market with 62.7% Share Owing to Established Infrastructure and Cost Efficiency

In 2024, the Van Market’s By Propulsion Analysis segment witnessed the Internal Combustion Engine (ICE) models maintaining a dominant stance, capturing 62.7% of the market. This substantial share is largely attributed to the well-established refueling infrastructure and the comparative cost efficiency of ICE vehicles over their counterparts. Despite environmental concerns and tightening emissions standards, ICE vans continue to be favored by businesses for their reliability and widespread serviceability.

The electric segment, though growing, remains in nascent stages, grappling with higher initial costs and limited charging infrastructure, which restricts its market penetration. Conversely, hybrid models are gradually gaining traction, offering a compromise with better fuel efficiency and reduced emissions, appealing to environmentally conscious consumers looking to mitigate the high upfront costs associated with fully electric vans.

The Others category, which includes alternative fuels like hydrogen and natural gas, remains a minor player in the market. These technologies, though promising for their low emissions, face significant hurdles in infrastructure and technology maturity, keeping their adoption rates low in the current market landscape.

End-use Analysis

Commercial Segment Leads in Van Market with 74.7% Share in 2024

In 2024, the commercial segment maintained a dominant stance in the van market, capturing an impressive 74.7% share in the By End-use Analysis category. This substantial market control can be attributed to the increased demand for commercial vans, driven by the growing need for efficient logistics and delivery solutions across various sectors.

As businesses continue to expand their operations, the reliance on commercial vans for transporting goods and services efficiently has seen a significant uptick. The robust build, enhanced cargo space, and reliability of these vehicles make them ideal for commercial applications, outpacing the personal use segment significantly.

On the other hand, the personal segment holds a smaller slice of the market. This segment caters primarily to individual consumers seeking versatile vehicles for personal transportation and recreational activities. Despite its smaller market share, there is a steady demand within this niche, driven by consumers valuing comfort, style, and the adaptability of vans for family or personal use.

As the market evolves, both segments show distinct growth trajectories influenced by consumer preferences and economic factors, shaping the future landscape of the van market.

Key Market Segments

By Tonnage Capacity

- Up to 2 Tons

- 2 to 3 Tons

- 3 to 5.5 Tons

By Propulsion

- Internal Combustion Engine (ICE)

- Electric

- Hybrid

- Others

By End-use

- Commercial

- Personal

Drivers

Increasing Consumer Demand Drives the Van Market

The expansion of the van market can be primarily attributed to rising consumer demand, stimulated by an increase in disposable income among consumers. This uptick in spending power enables a larger customer base to invest in vans, whether for personal use or commercial applications, thereby driving market growth.

Additionally, supportive regulatory frameworks and government policies further fuel this growth by offering subsidies and tax benefits, making van purchases more financially appealing. The van market is also benefiting from globalization trends, as manufacturers expand their reach into new international markets, capitalizing on cross-border trade opportunities.

Moreover, a surge in environmental and health awareness is prompting consumers to opt for vans that adhere to sustainability standards, aligning with global demands for eco-friendly vehicles. This collective influence of economic, political, and social factors underscores a robust upward trajectory for the van market.

Restraints

High Initial Investment Challenges Van Market Expansion

The van market faces notable restraints that hinder its rapid expansion, primarily due to the high initial investment and capital costs associated with purchasing and operating vans. This significant financial requirement can be a major barrier for new entrants and smaller operators who may struggle to secure the necessary capital.

Furthermore, the market is also challenged by stringent regulatory and compliance barriers. These regulations, which can vary significantly by region, require adherence to safety standards, emissions controls, and other operational guidelines.

Compliance with these regulations not only adds to the upfront costs but also to the ongoing operational expenses, potentially slowing market entry and limiting the agility of businesses to respond to market demands. This combination of high initial costs and complex regulatory frameworks makes it difficult for new players and limits the overall growth pace of the van market.

Growth Factors

Expansion into Emerging Markets Fuels Growth in the Van Market

The growth opportunities in the van market are promising, particularly through expansion into emerging markets and untapped regions, which offer new avenues for revenue streams. By entering developing countries, manufacturers can capitalize on lower competition and increased demand for transportation solutions.

Product diversification and customization also play a critical role, as introducing new variants and personalized features can cater to a broader consumer base with varying needs and preferences. Furthermore, forming strategic partnerships and collaborations with technology firms, suppliers, or innovative startups can significantly enhance a company’s market potential by integrating advanced technologies and expanding distribution networks.

Lastly, adapting to evolving consumer preferences, such as the increasing need for mobile offices or recreational vehicles, presents further growth prospects. These strategies not only promise to extend market reach but also allow companies to stay relevant in a dynamically changing industry landscape.

Emerging Trends

AI-Driven Analytics Boost Van Market Efficiency

The van market is experiencing significant transformation due to several trending factors that are shaping its future. First and foremost, the adoption of artificial intelligence (AI) and automation is enhancing operational efficiency across the sector. This integration allows for smarter route planning, predictive maintenance, and overall improved fleet management, which are crucial for companies relying heavily on logistics and transportation.

Furthermore, there is a noticeable shift toward subscription-based models as consumers increasingly favor Software as a Service (SaaS), rental, and subscription options over traditional purchasing methods. This trend not only meets the growing demand for flexibility and scalability but also aligns with the economic shifts in consumer behavior.

Additionally, sustainability and eco-friendly initiatives are gaining momentum. More businesses and consumers are opting for vans that incorporate green technologies and adhere to circular economy models, reducing environmental impact and promoting sustainability. Lastly, the integration of blockchain technology and enhanced cybersecurity measures are becoming more prevalent, providing unparalleled transparency, security, and efficiency in operations. These technological advancements are pivotal in driving the van market forward, making it more adaptable, secure, and environmentally responsible.

Regional Analysis

North America Leads Van Market with 38.1% Share, Valued at USD 65.6 Billion

The van market is segmented into several key regions: North America, Europe, Asia Pacific, Middle East & Africa, and Latin America. Each region showcases distinct market dynamics influenced by economic, technological, and social factors.

North America is the dominant region in the van market, holding a 38.1% market share with a valuation of USD 65.6 billion. This prominence can be attributed to the robust automotive infrastructure and high demand for commercial vehicles driven by a strong retail sector and e-commerce growth. Furthermore, advancements in vehicle technology and integration of electric vans are propelling market growth.

Regional Mentions:

Europe follows closely, characterized by stringent environmental regulations which drive the adoption of electric and hybrid vans. The region benefits from a well-established automotive industry, with a focus on innovation and sustainability. The push for reducing carbon emissions is significantly influencing van sales, with several countries offering incentives for electric vehicle purchases.

The Asia Pacific region is witnessing rapid growth due to increasing urbanization and the expansion of logistic networks. Rising disposable incomes and the growing e-commerce sector are further boosting demand for vans. China and India are pivotal markets, with local manufacturers and international players expanding their footprint.

Middle East & Africa show potential for growth with an increasing demand for commercial vehicles linked to infrastructure developments and industrial activities. However, the market is still nascent, with economic fluctuations and political instability affecting growth.

Latin America, despite economic volatility, shows resilience in the van market. Growth is spurred by the need for transportation solutions in urban and rural areas, coupled with increasing small business activities which demand reliable commercial transport.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In the global van market, projected to expand significantly in 2024, several key players are poised to shape industry dynamics. Among them, Ford Motor Company continues to lead with robust sales figures, primarily driven by the enduring popularity of its Transit and Transit Connect models in North America and Europe. The company’s commitment to electrification and smart mobility solutions is expected to further enhance its market position.

Mercedes-Benz Group AG remains a dominant force, especially in the luxury van segment, with the Mercedes-Benz Sprinter setting high standards in terms of quality, durability, and technological advancements. The introduction of electric models like the eSprinter reflects the company’s response to increasing environmental regulations and shifting consumer preferences towards sustainable transportation solutions.

Volkswagen Group and Renault Group are also significant contributors to the van market, with each bringing a strong portfolio of both combustion and electric engines. Volkswagen’s Caddy and Transporter series offer versatility and reliability, while Renault’s Trafic and Master vans are acclaimed for their practicality and efficiency in urban logistics.

Toyota Motor Corporation and Nissan Motor Co., Ltd. are enhancing their competitiveness through innovations in fuel efficiency and hybrid technology, addressing the diverse needs of global consumers. Hyundai Motor Company and Mitsubishi Motors Corporation are focusing on increasing their presence in emerging markets, offering economically viable models suited for varied commercial activities.

Stellantis NV, formed from the merger of Fiat Chrysler Automobiles and PSA Group, has a broad range of light commercial vehicles that are well-received globally, leveraging economies of scale and extensive R&D capabilities to innovate and adapt to market needs.

Top Key Players in the Market

- Ford Motor Company

- Mercedes-Benz Group AG

- Volkswagen Group

- Renault Group

- TOYOTA MOTOR CORPORATION

- Nissan Motor Co., Ltd.

- Hyundai Motor Company

- MITSUBISHI MOTORS CORPORATION

- ISUZU MOTORS LIMITED

- Stellantis NV

- Others

Recent Developments

- In December 2024, Mullen Automotive made its initial entry into the electric vehicle market by selling its first EV van to a prominent home service brand. This sale marks a significant milestone in the company’s expansion into green transportation solutions.

- In May 2024, Cummins significantly bolstered its position in the commercial vehicle market through the strategic acquisition of Meritor. This move is poised to transform Cummins’ capabilities and competitive edge in the industry.

- In December 2024, a partner of Mercedes-Benz completed the acquisition of Motus Truck & Van, aiming to establish new standards for innovation in the commercial vehicle sector.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 172.8 Billion |

| Forecast Revenue (2034) | USD 286.9 Billion |

| CAGR (2025-2034) | 5.2% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Tonnage Capacity (Up to 2 Tons, 2 to 3 Tons, 3 to 5.5 Tons), By Propulsion (Internal Combustion Engine (ICE), Electric, Hybrid, Others), By End-use (Commercial, Personal) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Ford Motor Company, Mercedes-Benz Group AG, Volkswagen Group, Renault Group, TOYOTA MOTOR CORPORATION, Nissan Motor Co., Ltd., Hyundai Motor Company, MITSUBISHI MOTORS CORPORATION, ISUZU MOTORS LIMITED, Stellantis NV, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |