Global Utility Tractor Market Size, Share, And Industry Analysis Report By Engine Power (40–60 HP, 61–80 HP, 81–100 HP), By Drive Type (2-Wheel Drive, 4-Wheel Drive), By Fuel Type (Diesel, Electric, Hybrid), By Application (Agriculture, Construction, Landscaping, Municipal), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 181497

- Number of Pages: 354

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

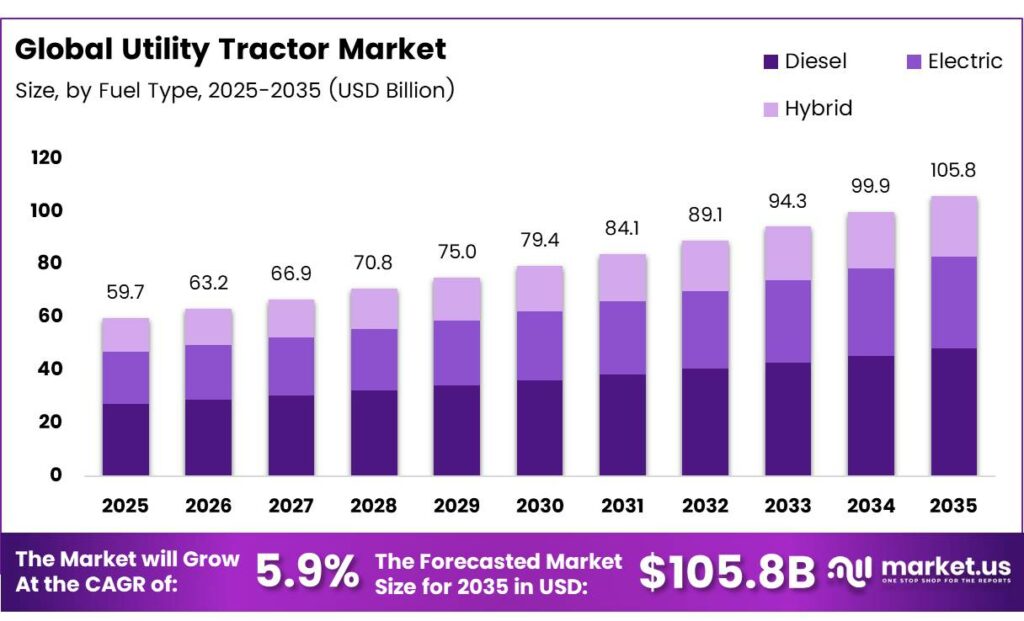

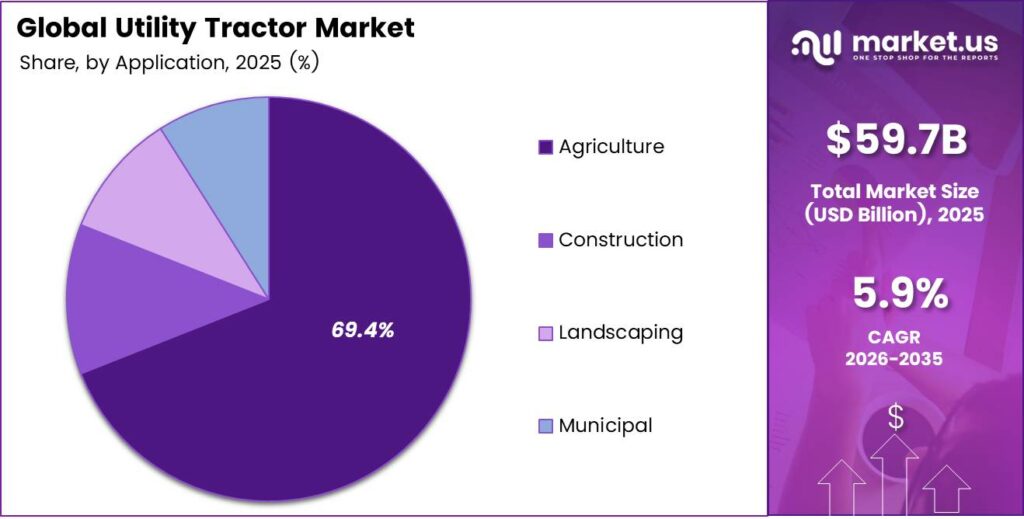

The Global Utility Tractor Market size is expected to be worth around USD 105.8 billion by 2035 from USD 59.7 billion in 2025, growing at a CAGR of 5.9% during the forecast period 2026 to 2035.

The utility tractor market covers a broad range of multi-purpose agricultural machines designed for farm operations, landscaping, construction, and municipal tasks. These machines deliver flexible power outputs, typically ranging from 40 HP to over 100 HP, making them suitable for diverse terrain and workload requirements worldwide.

Utility tractors serve as the backbone of modern agriculture, enabling smallholder and commercial farmers alike to manage planting, tilling, harvesting, and material handling efficiently. Moreover, expanding use in non-farm sectors such as groundskeeping, road maintenance, and light construction has widened the market’s addressable base considerably.

Domestic tractor sales reached 42,273 units in November 2025, up 33% from 31,746 units in November 2024. This sharp year-on-year gain reflects strong rural income recovery and favorable monsoon conditions stimulating replacement and first-time purchases across India’s farming communities.

India’s total tractor sales, including domestic and exports, reached 154,417 units in September 2025. Deere and Company equipment operations net sales totaled $38,917 million in fiscal year 2025, underscoring the scale at which leading manufacturers continue to operate globally despite near-term volume pressures in key markets.

Precision agriculture adoption further strengthens the market’s growth trajectory. Farmers increasingly integrate GPS-guided systems, telematics, and smart steering solutions into utility tractor operations. Therefore, original equipment manufacturers invest heavily in technology-enabled product lines to meet rising demand for connected farm equipment.

Key Takeaways

- The Global Utility Tractor Market is valued at USD 59.7 billion in 2025 and is projected to reach USD 105.8 billion by 2035. at a CAGR of 5.9% during the forecast period 2026 to 2035.

- The 40–60 HP segment holds the dominant share at 42.6% in 2025.

- The 2-Wheel Drive segment leads with a 67.2% share in 2025.

- The Diesel segment dominates with a 87.9% share in 2025.

- The Agriculture segment holds the largest share at 69.4% in 2025.

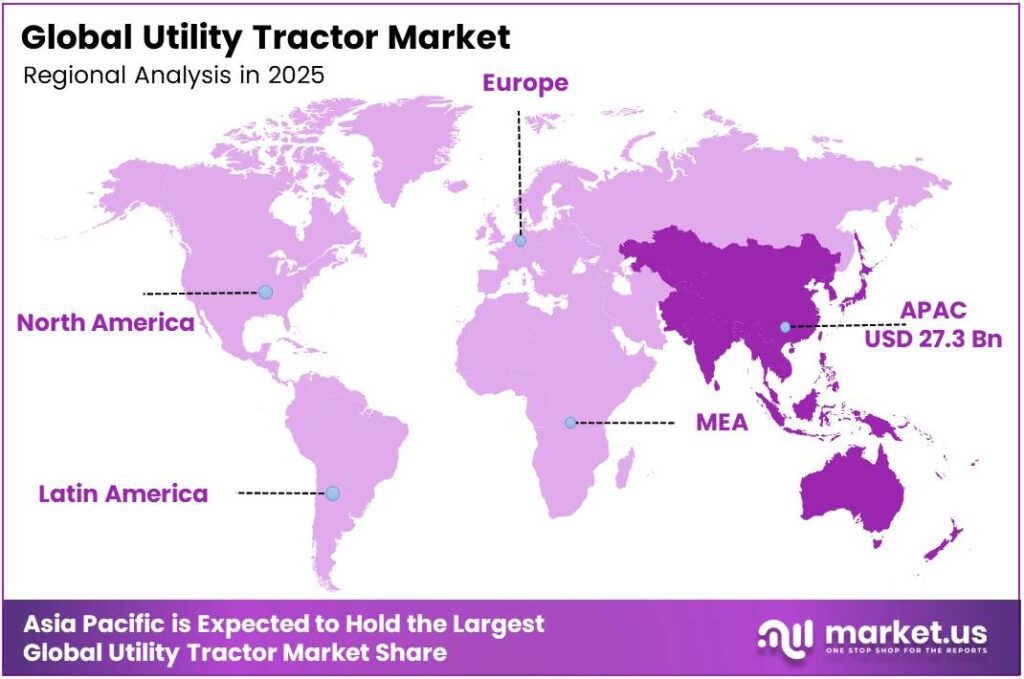

- Asia Pacific dominates the regional landscape with a 45.8% market share, valued at USD 27.3 billion in 2025.

By Engine Power Analysis

40–60 HP dominates with 42.6% due to its suitability for small and mid-size farm operations.

In 2025, the 40–60 HP segment held a dominant market position in the By Engine Power segment of the Utility Tractor Market, with a 42.6% share. This power range suits a wide variety of field tasks, including plowing, seeding, and hauling. Moreover, its affordability and fuel efficiency make it highly accessible to smallholder and mid-scale farmers across developing agricultural economies.

The 61–80 HP segment serves medium to large farm operations requiring higher pull force and attachment capacity. Consequently, demand for this range grows steadily in commercial farming regions across North America, Europe, and parts of the Asia Pacific, where farm consolidation trends favor larger, more capable utility machines for multi-season field work.

By Drive Type Analysis

2-Wheel Drive dominates with 67.2% due to its lower cost and wide availability across flat agricultural terrain.

In 2025, the 2-Wheel Drive segment held a dominant market position in the By Drive Type segment of the Utility Tractor Market, with a 67.2% share. These tractors remain the preferred choice for farmers operating on flat, stable terrain where full four-wheel traction is not required. Furthermore, their lower purchase price and simpler maintenance needs make them attractive to budget-conscious buyers in price-sensitive markets.

The 4-Wheel Drive segment is growing in relevance as farmers expand operations into hilly, wet, and uneven terrain. Moreover, four-wheel drive tractors deliver superior grip and load management for orchard farming, highland cultivation, and construction-adjacent tasks. Therefore, manufacturers continue expanding four-wheel drive portfolios with modern power-split transmission systems for improved efficiency across challenging working environments.

By Fuel Type Analysis

Diesel dominates with 87.9% due to its proven reliability, energy density, and widespread availability in rural markets.

In 2025, the Diesel segment held a dominant market position in the By Fuel Type segment of the Utility Tractor Market, with a 87.9% share. Diesel engines deliver the high torque and endurance required for prolonged fieldwork. Additionally, diesel infrastructure remains deeply established in rural and agricultural zones globally, making it the default fuel choice for farmers regardless of geography or farm size.

The Electric segment is gaining traction as battery technology improves and emission regulations tighten. Governments in Europe and North America actively incentivize electric tractor development. However, limited battery range, high upfront costs, and inadequate rural charging infrastructure continue to slow broader adoption among cost-sensitive farming communities outside of well-supported pilot markets.

By Application Analysis

Agriculture dominates with 69.4% due to the essential role utility tractors play in crop production and farm management.

In 2025, the Agriculture segment held a dominant market position in the By Application segment of the Utility Tractor Market, with a 69.4% share. Farm mechanization programs and rising labor costs push farmers toward tractor-based solutions for plowing, planting, and harvesting. Moreover, precision agriculture adoption strengthens demand for technologically equipped utility tractors across both smallholder and commercial farming operations globally.

The Construction segment uses utility tractors for material hauling, grading, and site preparation on small to medium project sites. These machines offer cost-effective performance compared to dedicated construction equipment. Additionally, compact utility tractors equipped with front loaders and backhoe attachments serve contractors managing urban landscaping projects and rural infrastructure development tasks efficiently.

Key Market Segments

By Engine Power

- 40–60 HP

- 61–80 HP

- 81–100 HP

By Drive Type

- 2-Wheel Drive

- 4-Wheel Drive

By Fuel Type

- Diesel

- Electric

- Hybrid

By Application

- Agriculture

- Construction

- Landscaping

- Municipal

Emerging Trends

Sustainable Powertrains and Low-Emission Technologies Reshape Product Portfolios

The utility tractor industry is shifting toward low-emission powertrains as environmental regulations tighten across major markets. Manufacturers actively develop electric and hybrid models to meet sustainability targets. India’s tractor production reached 102,915 units in November 2025, reflecting strong volume momentum that pushes producers to accelerate clean-technology integration across product lines.

Digital AgTech and Telematics Drive Smarter Farm Equipment Adoption

Digital agriculture technology is transforming how utility tractors operate on modern farms. Telematics platforms provide real-time data on fuel use, engine health, and field performance. CNH Industrial consolidated revenues totaled $19,836 million in 2024, and the company continues to invest in digital connectivity features that help farmers monitor and manage equipment remotely for improved operational efficiency.

Drivers

Labor Shortages and Government Subsidies Accelerate Mechanization Adoption

Aging rural populations and acute labor shortages push farm operators toward mechanized solutions across all major agricultural regions. Governments in India, China, and Southeast Asia offer direct subsidies and financing support to accelerate tractor adoption. According to Mahindra and Mahindra, YTD November 2025 domestic tractor sales totaled 361,680 units, up 20% from 302,308 units in the same prior period, demonstrating strong policy-driven demand expansion.

Precision Agriculture and Multi-Purpose Applications Expand Market Reach

GPS-guided systems, automated steering, and precision field management tools expand the operational value of utility tractors significantly. Deere and Company’s Small Agriculture and Turf segment, which includes utility tractors, recorded net sales of $10,224 million in fiscal year 2025. Additionally, growing demand for multi-purpose equipment in landscaping, construction, and municipal sectors broadens addressable market opportunities beyond traditional agriculture.

Restraints

High Ownership Costs Create Barriers for Small-Scale Farm Operators

Utility tractors carry significant upfront purchase costs, and ongoing maintenance and fuel expenses add to the total ownership burden. Small-scale farmers in developing markets often lack access to affordable financing, making tractor ownership prohibitive. Consequently, many subsistence-level operators continue relying on manual labor or animal-drawn tools despite the clear productivity benefits that mechanized equipment would deliver.

Specialized Machinery Competition Limits Utility Tractor Market Penetration

Purpose-built machinery such as combine harvesters, dedicated tillers, and compact construction equipment increasingly competes with utility tractors in specific application segments. Moreover, contractors and large commercial farms often prefer specialized equipment for efficiency reasons. Therefore, utility tractor manufacturers must continuously innovate attachment ecosystems and multi-function capabilities to defend market share against growing competition from segment-specific alternatives.

Growth Factors

Electric Models and Urbanization Open New Market Opportunities

Electric and hybrid utility tractor development accelerates as sustainability regulations expand globally. Governments in Europe and North America mandate emission reductions, creating structural demand for cleaner equipment. According to the Tractor Manufacturers Association, India’s tractor production reached 104,329 units in June 2025, and Kubota Corporation’s Farm Equipment and Engines segment generated revenue of 2,003.3 billion yen in fiscal year 2025, confirming production scale and investment capacity across leading manufacturers.

AI Integration and Rising Adoption Among Small Farmers Drive Long-Term Growth

Artificial intelligence, autonomous steering, and remote monitoring technologies rapidly integrate into mid-range utility tractor product lines. These features lower labor dependency and improve field productivity for operators of all scales. Moreover, rising adoption among small-scale and hobby farmers in the Asia-Pacific regions generates consistent incremental volume, supporting sustained market expansion well into the next decade.

Regional Analysis

Asia Pacific Dominates the Utility Tractor Market with a Market Share of 45.8%, Valued at USD 27.3 Billion

Asia Pacific leads the global utility tractor market with a commanding 45.8% share, valued at USD 27.3 billion in 2025. India and China account for the largest share of regional demand, driven by government farm mechanization programs, rural labor shortages, and growing smallholder purchasing power. Furthermore, high tractor production volumes across Indian manufacturers reinforce the region’s dominant position in global supply and consumption.

North America maintains a strong market position driven by large commercial farming operations and high technology adoption rates. The United States leads regional demand for precision-equipped utility tractors used in row cropping, livestock operations, and landscaping. Moreover, municipal procurement programs sustain steady institutional demand for versatile, multi-attachment tractor configurations across urban and suburban public works applications.

Europe’s utility tractor market benefits from stringent emission standards that accelerate the transition toward cleaner, Stage V-compliant diesel engines and emerging electric models. Germany, France, and the United Kingdom represent the largest national markets. Additionally, the Common Agricultural Policy and national subsidy frameworks continue to support equipment investment cycles among both large-scale and smallholder farming communities across the continent.

The Middle East and Africa region presents a growing demand for utility tractors as governments invest in agricultural self-sufficiency and rural infrastructure programs. Countries such as South Africa, Egypt, and Saudi Arabia drive regional adoption. However, limited financing access and underdeveloped dealer networks in sub-Saharan Africa continue to constrain market penetration rates among smallholder farming communities.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Deere and Company stands as the world’s largest agricultural equipment manufacturer with a comprehensive utility tractor portfolio spanning compact to high-horsepower models. The company integrates advanced precision agriculture features, including GPS guidance, telematics, and autonomous operation capabilities, into its product lines. Deere’s global dealer network and strong brand loyalty position it as the market leader across North America and key international agricultural markets.

CNH Global NV operates two of the most recognized tractor brands globally, offering a wide spectrum of utility tractors designed for farm, construction, and specialty applications. The company focuses heavily on digital agriculture integration, clean engine technology, and multi-region distribution strength. CNH’s extensive service network and financing solutions support farmers and contractors across North America, Europe, Latin America, and the Asia Pacific markets effectively.

AGCO Corporation delivers utility tractor solutions under multiple strong brand identities targeting both developed and emerging agricultural markets worldwide. The company invests consistently in precision farming technology, sustainable powertrain development, and connected equipment platforms. AGCO’s regional manufacturing strategy allows it to maintain cost competitiveness while meeting local emissions standards and serving diverse customer segments across global agricultural regions.

CLAAS KGaA mbH brings European engineering expertise to the utility tractor segment, emphasizing fuel efficiency, operator comfort, and precision field management integration. The company’s product development priorities align closely with European farm consolidation trends and emission compliance requirements. Moreover, CLAAS expands its international distribution reach to capture growing demand in the Asia Pacific and Latin American agricultural markets through strategic partnerships and dealer network expansion.

Top Key Players in the Market

- Deere and Company

- CNH Global NV

- AGCO Corporation

- CLAAS KGaA mbH

- Mahindra and Mahindra Corporation

- Kubota Corporation

- Escorts Group

- Tractors and Farm Equipment Limited (TAFE)

- Kuhn Group

- Yanmar Company Limited

Recent Developments

- In January 2026, CNH announced the completion of its New Holland T5 range with the new 2026 T5 Electro Command models. These tractors are positioned as “smart utility tractors” in the 100–120 hp segment. They feature a 16×16 semi-powershift transmission with IntelliShift for smoother, automated shifting.

- In February 2026, John Deere unveiled its redesigned 2027 model year 1 Series Compact Utility Tractors (CUTs). This new lineup, which includes the 1E 23, 1M 25, and 1R 25 models, focuses on improved ergonomics, year-round capability, and easier operation. Key updates include a factory-installed HVAC cab option for the 1M and 1R models, a redesigned fender console for more intuitive controls, and standard LED lighting.

Report Scope

Report Features Description Market Value (2025) USD 59.7 Billion Forecast Revenue (2035) USD 105.8 Billion CAGR (2026-2035) 5.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Engine Power (40–60 HP, 61–80 HP, 81–100 HP), By Drive Type (2-Wheel Drive, 4-Wheel Drive), By Fuel Type (Diesel, Electric, Hybrid), By Application (Agriculture, Construction, Landscaping, Municipal) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Deere and Company, CNH Global NV, AGCO Corporation, CLAAS KGaA mbH, Mahindra and Mahindra Corporation, Kubota Corporation, Escorts Group, Tractors and Farm Equipment Limited (TAFE), Kuhn Group, Yanmar Company Limited Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Deere and Company

- CNH Global NV

- AGCO Corporation

- CLAAS KGaA mbH

- Mahindra and Mahindra Corporation

- Kubota Corporation

- Escorts Group

- Tractors and Farm Equipment Limited (TAFE)

- Kuhn Group

- Yanmar Company Limited

Our Clients

- 181497

- March 2026