Global Torpedo Market Size, Share, Growth Analysis By Weight (Heavyweight Torpedoes, Lightweight Torpedoes), By Launch Platform (Sea-launched, Surface-launched, Underwater-launched, Air-launched), By Propulsion (Electric, Conventional), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: May 2026

- Report ID: 185887

- Number of Pages: 267

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

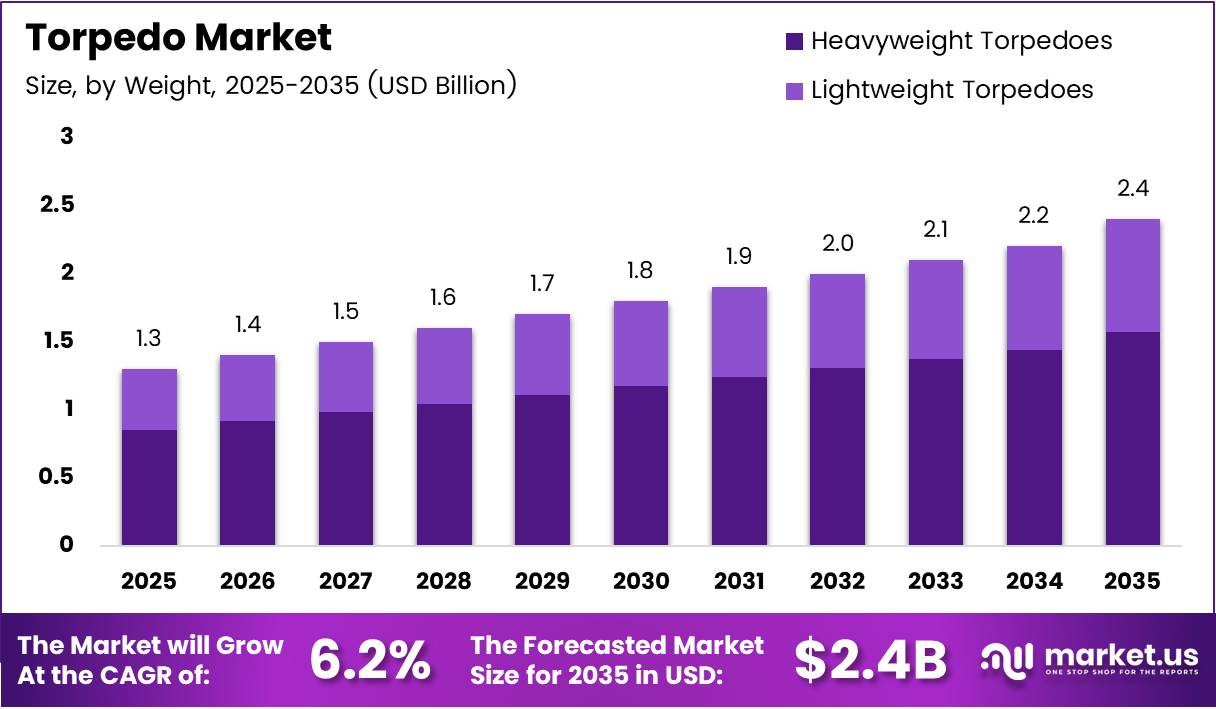

Global Torpedo Market size is expected to be worth around USD 2.4 Billion by 2035 from USD 1.3 Billion in 2025, growing at a CAGR of 6.2% during the forecast period 2026 to 2035.

The torpedo market covers the design, development, and procurement of underwater weapon systems deployed from submarines, surface vessels, and aircraft. Naval forces worldwide treat torpedoes as core anti-submarine warfare assets, making procurement cycles closely tied to broader naval modernization budgets and defense policy shifts.

Rising submarine fleet expansions across Asia-Pacific and Europe are reshaping procurement priorities. Nations that historically relied on imported systems now fund indigenous underwater weapon programs, broadening the supplier base and intensifying competition for long-range, precision-guided torpedo contracts.

Maritime security pressures are pushing defense ministries to accelerate anti-submarine warfare investments. The shift is not marginal — governments are committing multiyear budgets to torpedo systems, as demonstrated by the U.S. Navy’s MK 54 Lightweight Torpedo Program, which drew a potential $807.6 million contract award to General Dynamics Mission Systems in December 2024.

Technological advancement is moving the market toward acoustic homing, fiber-optic guidance, and electric propulsion — each designed to reduce acoustic signatures and improve strike accuracy. These upgrades directly raise the cost-per-unit but also widen the performance gap between modern systems and legacy alternatives, accelerating replacement cycles.

In 2024, Naval Group launched its F21 heavyweight torpedo under France’s Artemis program, replacing the older F17 with enhanced detection, speed, and endurance. Its integration into both French and Brazilian naval forces signals that allied procurement partnerships are becoming a primary channel for market expansion beyond domestic orders.

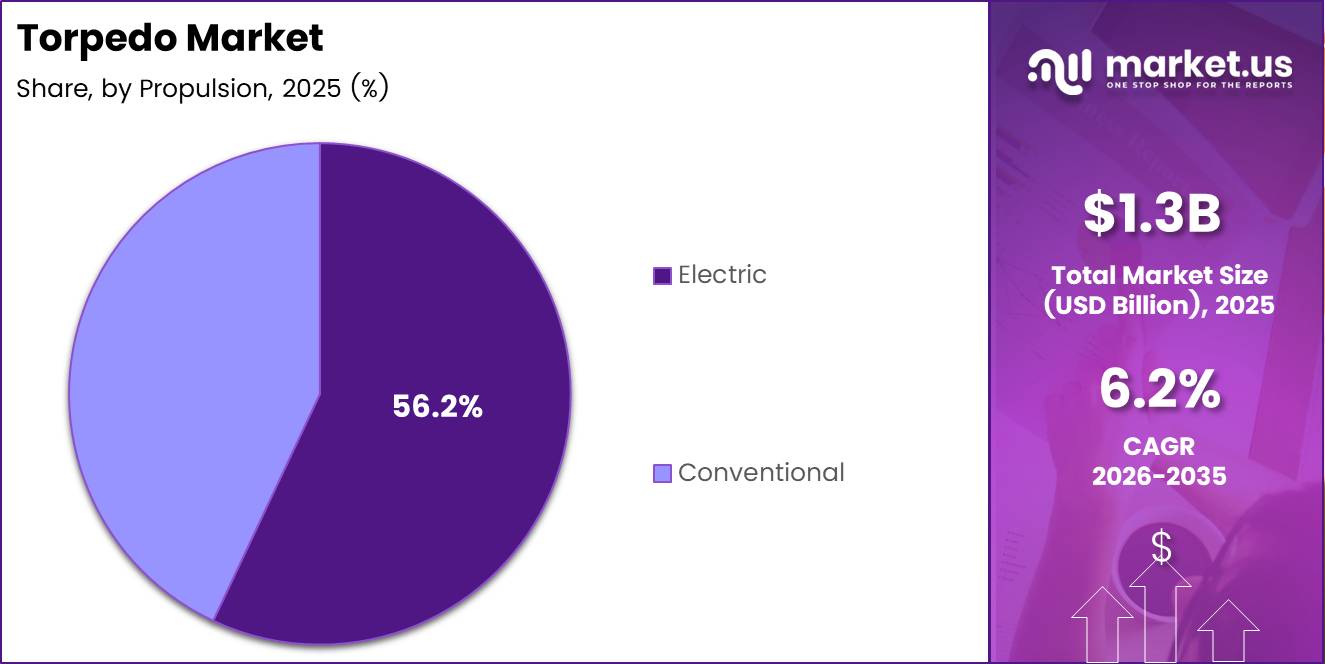

Electric propulsion now leads with a 56.2% share of the By Propulsion segment. This dominance reflects a structural shift in naval doctrine — quieter underwater weapons reduce detection risk, and navies that prioritize stealth operations are no longer willing to accept the acoustic trade-offs of conventional propulsion systems.

Heavyweight torpedoes hold a 65.3% share of the By Weight segment, confirming that submarine-launched deep-water engagement remains the primary mission requirement driving procurement. This concentration of spend in heavyweight systems signals where defense budgets are flowing — and where suppliers with certified heavyweight programs hold a durable competitive position.

Key Takeaways

- The global Torpedo Market is valued at USD 1.3 Billion in 2025 and is forecast to reach USD 2.4 Billion by 2035.

- The market advances at a CAGR of 6.2% during the forecast period 2026 to 2035.

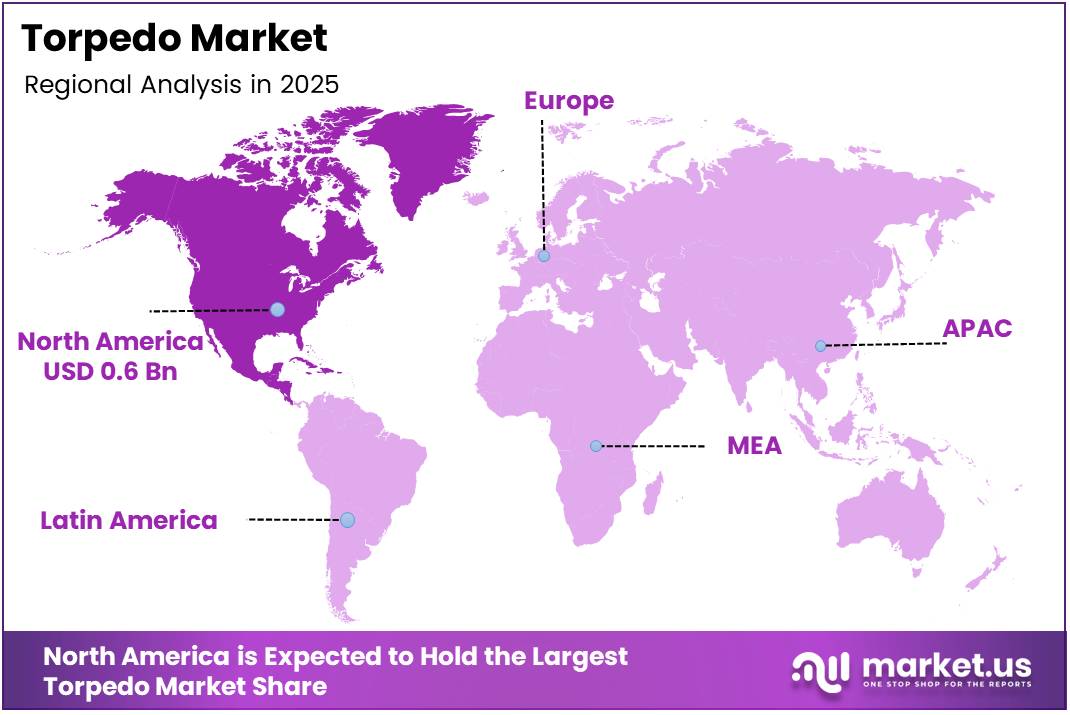

- North America leads all regions with a 43.70% market share, valued at USD 0.6 Billion.

- Heavyweight Torpedoes dominate the By Weight segment with a 65.3% share.

- Sea-launched platforms lead the By Launch Platform segment with a 73.7% share.

- Electric propulsion holds a 56.2% share of the By Propulsion segment.

- Northrop Grumman secured a $233 million contract in January 2026 to manufacture the MK54 MOD 2 advanced lightweight torpedo for the U.S. Navy.

- SAIC received a $242 million contract in November 2025 to support MK 48 Heavyweight and MK 54 Lightweight Torpedo systems.

Product Analysis

Heavyweight Torpedoes dominate with 65.3% due to submarine deep-water engagement mission priority.

In 2025, Heavyweight Torpedoes held a dominant market position in the By Weight segment of the Torpedo Market, with a 65.3% share. Submarine fleets worldwide treat heavyweight systems as their primary long-range strike weapon, and as nations expand their submarine programs, procurement of heavyweight torpedoes follows directly — making this segment the most budget-intensive in the entire market.

Lightweight Torpedoes serve as the primary anti-submarine weapon for helicopter and maritime patrol aircraft deployments. Their lower unit cost and compatibility with airborne platforms make them attractive for navies building out layered anti-submarine warfare coverage. Saab’s SEK 1.3 billion order from Sweden’s FMV in May 2025 confirms active procurement momentum in this segment.

Launch Platform Analysis

Sea-launched platforms dominate with 73.7% due to submarine fleet expansion across major naval powers.

In 2025, Sea-launched platforms held a dominant market position in the By Launch Platform segment of the Torpedo Market, with a 73.7% share. Submarines remain the primary delivery vehicle for torpedo engagements, and the steady growth of submarine fleets in Asia-Pacific and Europe directly translates into procurement demand for sea-launched torpedo systems — the segment’s lead is structural, not cyclical.

Surface-launched platforms extend torpedo deployment capability to frigates and destroyers, providing fleet commanders with anti-submarine options beyond the submarine force. Surface launch systems are generally integrated into broader naval shipbuilding programs, making their procurement tied to warship construction schedules rather than standalone torpedo budgets.

Underwater-launched platforms, including autonomous underwater vehicles and fixed seabed systems, represent an emerging deployment category. Defense agencies are funding research into integrating torpedo launch capabilities with underwater combat drones, a development that could reshape platform diversity within this segment over the forecast period.

Air-launched torpedoes serve maritime patrol aircraft and naval helicopters operating in anti-submarine warfare roles. Their deployment range from aircraft gives naval commanders flexibility to engage submarines at distances well beyond surface ship range, making air-launched systems a strategically valued component of multi-layer underwater defense architectures.

Propulsion Analysis

Electric propulsion dominates with 56.2% due to stealth requirements in modern submarine warfare doctrine.

In 2025, Electric propulsion held a dominant market position in the By Propulsion segment of the Torpedo Market, with a 56.2% share. Navies conducting stealth operations require weapons that match the acoustic discipline of their submarine platforms. Electric propulsion eliminates combustion noise, preventing the torpedo itself from revealing the launching vessel’s position during an engagement.

Conventional propulsion systems retain relevance in cost-sensitive procurement environments where absolute acoustic stealth is a secondary requirement. However, as threat detection technologies improve globally, the performance gap between electric and conventional systems widens — putting conventional propulsion systems under longer-term substitution pressure as modernization programs advance.

Key Market Segments

By Weight

- Heavyweight Torpedoes

- Lightweight Torpedoes

By Launch Platform

- Sea-launched

- Surface-launched

- Underwater-launched

- Air-launched

By Propulsion

- Electric

- Conventional

Drivers

Naval Modernization Budgets and Submarine Fleet Expansion Drive Heavyweight Torpedo Procurement

Defense ministries across Asia-Pacific, Europe, and North America are committing multiyear budgets to submarine fleet expansion and naval modernization. This directly translates into sustained torpedo procurement cycles, as each new submarine platform requires a certified weapon inventory — creating a demand pipeline that extends well beyond single-year defense appropriations.

Maritime security pressures, particularly around contested sea lanes and anti-submarine warfare preparedness, have elevated torpedo systems from legacy inventory to active procurement priority. Governments are no longer deferring underwater weapon upgrades — the strategic calculus now treats anti-submarine warfare capability as a near-term readiness requirement, not a long-cycle modernization item.

Technological advances in acoustic homing and guidance mechanisms are compressing replacement cycles. In December 2024, the U.S. Navy awarded General Dynamics Mission Systems a potential $807.6 million contract for MK 54 Lightweight Torpedo production and support — a contract scale that confirms procurement velocity is accelerating, not plateauing, as performance thresholds rise across allied navies.

Restraints

High Production Costs and Export Controls Constrain Market Access for Advanced Torpedo Systems

Modern heavyweight torpedo systems require specialized materials, precision manufacturing, and extensive underwater testing — cost drivers that push unit prices well beyond what smaller naval procurement budgets can absorb. This creates a two-tier market where only well-funded defense programs can acquire the most capable systems, limiting the addressable customer base for premium suppliers.

Export restrictions and defense trade regulations add a structural ceiling to international market penetration. Torpedo technologies fall under stringent arms export control regimes in most producing nations, meaning that even commercially viable export opportunities require lengthy government approval processes — delaying revenue realization and creating uncertainty for suppliers planning international sales strategies.

Together, these cost and regulatory constraints slow the pace at which advanced torpedo systems reach new markets. Suppliers face a difficult commercial position: the technology development costs are high, testing requirements are expensive, and the pathway to international sales is controlled by export licensing — compressing the window in which development investments can generate returns.

Growth Factors

Autonomous Torpedo Development and Defense Collaboration Programs Open New Revenue Streams

Development of autonomous smart torpedoes with enhanced target recognition capabilities represents the most significant product evolution in this market. AI-assisted targeting reduces reliance on operator guidance mid-engagement, making torpedoes effective in contested electromagnetic environments — a capability gap that multiple navies are now funding programs to close.

Naval helicopter deployment programs are driving fresh investment in lightweight torpedo systems. As navies expand rotary-wing anti-submarine warfare fleets, demand for air-deployable, compact torpedo systems grows in parallel. In January 2026, Northrop Grumman secured a $233 million U.S. Navy contract to manufacture the MK54 MOD 2 advanced lightweight torpedo — developed in cooperation with the Australian Defence Force, signaling allied co-development as a model for expanding this segment.

Indigenous underwater weapon manufacturing programs, supported by defense collaboration agreements, are creating new domestic supplier bases in markets previously dependent on imports. Bharat Dynamics Limited’s imminent delivery of India’s first Advanced Lightweight Torpedo to the Indian Navy in February 2025 — with a 20km strike range and 50-knot speed — demonstrates that emerging market producers can now develop competitive systems, widening the global supplier landscape.

Emerging Trends

Fiber-Optic Guidance, AI Targeting, and Countermeasure Resistance Redefine Torpedo Performance Standards

Fiber-optic guidance technology is replacing older wire-guided systems in advanced torpedo programs. Fiber-optic links deliver higher data bandwidth, allowing the launching platform to maintain real-time control of the weapon across longer engagement distances — a capability that fundamentally changes the tactical options available to submarine commanders during engagements.

AI-assisted underwater target tracking systems are moving from research programs into active development contracts. By automating target classification and engagement decisions, AI integration reduces the reaction time between detection and weapon deployment. Early movers — both suppliers who embed AI guidance and navies that fund its development — gain a decision-speed advantage that legacy systems cannot replicate.

Countermeasure-resistant navigation technologies address a growing tactical problem: as decoy and jamming systems improve, older torpedo guidance is increasingly vulnerable to evasion. Suppliers investing in countermeasure-resistant navigation are positioning their products as future-proof platforms — a differentiation point that commands premium contract pricing and insulates against competition from lower-cost conventional alternatives.

Regional Analysis

North America Dominates the Torpedo Market with a Market Share of 43.70%, Valued at USD 0.6 Billion

North America holds a 43.70% share of the global torpedo market, valued at USD 0.6 Billion. The U.S. Navy’s sustained investment in MK 48 Heavyweight and MK 54 Lightweight Torpedo programs, backed by billion-dollar multiyear contracts, drives this regional lead. Mature defense procurement infrastructure and continuous R&D funding keep North America ahead of all other regions.

Europe Torpedo Market Trends

Europe maintains a strong position through active naval modernization in France, the UK, Germany, and Sweden. France’s Artemis program producing the F21 heavyweight torpedo and Sweden’s SEK 1.3 billion SLWT order from Saab reflect consistent government commitment to sovereign underwater weapon capabilities — a procurement pattern that signals stable regional demand through the forecast period.

Asia Pacific Torpedo Market Trends

Asia Pacific represents the fastest-expanding demand base, driven by submarine fleet growth in India, China, South Korea, and Australia. India’s development of the Advanced Lightweight Torpedo through Bharat Dynamics Limited and NSTL demonstrates a strategic pivot toward indigenous production — reducing import dependency while creating a new regional supplier competing for domestic and allied contracts.

Middle East and Africa Torpedo Market Trends

The Middle East and Africa region shows early-stage torpedo procurement activity tied to naval force modernization programs among Gulf states. Investments remain limited compared to North America and Asia Pacific, but growing maritime security concerns in key sea lanes are prompting select nations to evaluate anti-submarine warfare capabilities for the first time.

Latin America Torpedo Market Trends

Latin America’s torpedo market centers on Brazil, which operates a meaningful submarine fleet and has integrated the French F21 heavyweight torpedo into its naval inventory. This procurement decision reflects Brazil’s strategy of aligning with advanced allied defense technology — and positions the country as the primary regional market for sophisticated underwater weapon systems.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Aselsan, Turkey’s leading defense electronics company, has built its torpedo market position on domestic naval modernization priorities. By developing torpedo countermeasure and guidance systems for the Turkish Navy, Aselsan reduces its home market’s dependence on foreign suppliers — a strategy that insulates it from export restriction risks while creating a proven domestic reference base for international sales conversations.

Atlas Elektronik GmbH specializes in naval underwater systems, with expertise spanning torpedo development, sonar, and mine countermeasures. Its integration into the TKMS (thyssenkrupp Marine Systems) group gives it direct access to submarine construction programs — an advantage that places its torpedo systems on new platforms at the design stage, locking in long-term weapon supply relationships before competitive procurement begins.

BAE Systems positions its torpedo capabilities within a broader naval combat systems portfolio, allowing it to offer integrated underwater warfare solutions rather than standalone weapons. This systems-level approach strengthens its position in large naval platform programs where buyers prefer single-supplier accountability for weapon system integration — reducing BAE’s exposure to price-only competition from specialized torpedo manufacturers.

Bharat Dynamics Limited (BDL) occupies a strategically important position as India’s primary state-owned guided weapon manufacturer. Its imminent delivery of the Advanced Lightweight Torpedo to the Indian Navy confirms BDL’s ability to execute on domestically developed underwater weapons — a milestone that strengthens its case for future Indian Navy contracts and positions it as a regional supplier for allied South Asian naval programs.

Key Players

- Aselsan

- Atlas Elektronik GmbH

- BAE Systems

- Bharat Dynamics Limited

- Leonardo SpA

- Lockheed Martin Corporation

- Naval Group

- Northrop Grumman Corporation

- Raytheon Company

- Rosoboronexport

- Saab AB

Recent Developments

- January 2025 — Fincantieri S.p.A acquired Whitehead Alenia Sistemi Subacquei S.p.A (WASS) from Leonardo S.p.A for $428 million (€415 million). The acquisition enables Fincantieri to integrate advanced underwater acoustic technologies and weapons systems, reinforcing its position in the underwater defense sector.

- February 2025 — Bharat Dynamics Limited confirmed the imminent delivery of its first Advanced Lightweight Torpedo (ALWT) to the Indian Navy. The ALWT, developed by the Naval Science and Technological Laboratory in Visakhapatnam, features a striking range of up to 20km, speeds of 50 knots, and operational depths reaching 650 metres.

- May 2025 — Saab received an order from the Swedish Defence Materiel Administration (FMV) for Saab Lightweight Torpedoes (SLWT) and torpedo tubes, valued at approximately SEK 1.3 billion (approximately $135.4 million). Deliveries are scheduled to begin in 2026, reflecting Sweden’s sustained commitment to sovereign lightweight torpedo capability.

- November 2025 — SAIC was awarded a $242 million contract by the U.S. Navy to operate, maintain, and upgrade the Propulsion Test Facility Complex. The contract supports the MK 48 Heavyweight Torpedo, MK 54 Lightweight Torpedo, and related underwater weapon systems.

Report Scope

Report Features Description Market Value (2025) USD 1.3 Billion Forecast Revenue (2035) USD 2.4 Billion CAGR (2026-2035) 6.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Weight (Heavyweight Torpedoes, Lightweight Torpedoes), By Launch Platform (Sea-launched, Surface-launched, Underwater-launched, Air-launched), By Propulsion (Electric, Conventional) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Aselsan, Atlas Elektronik GmbH, BAE Systems, Bharat Dynamics Limited, Leonardo SpA, Lockheed Martin Corporation, Naval Group, Northrop Grumman Corporation, Raytheon Company, Rosoboronexport, Saab AB Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Aselsan

- Atlas Elektronik GmbH

- BAE Systems

- Bharat Dynamics Limited

- Leonardo SpA

- Lockheed Martin Corporation

- Naval Group

- Northrop Grumman Corporation

- Raytheon Company

- Rosoboronexport

- Saab AB

Our Clients

- 185887

- May 2026