Quick Navigation

Report Overview

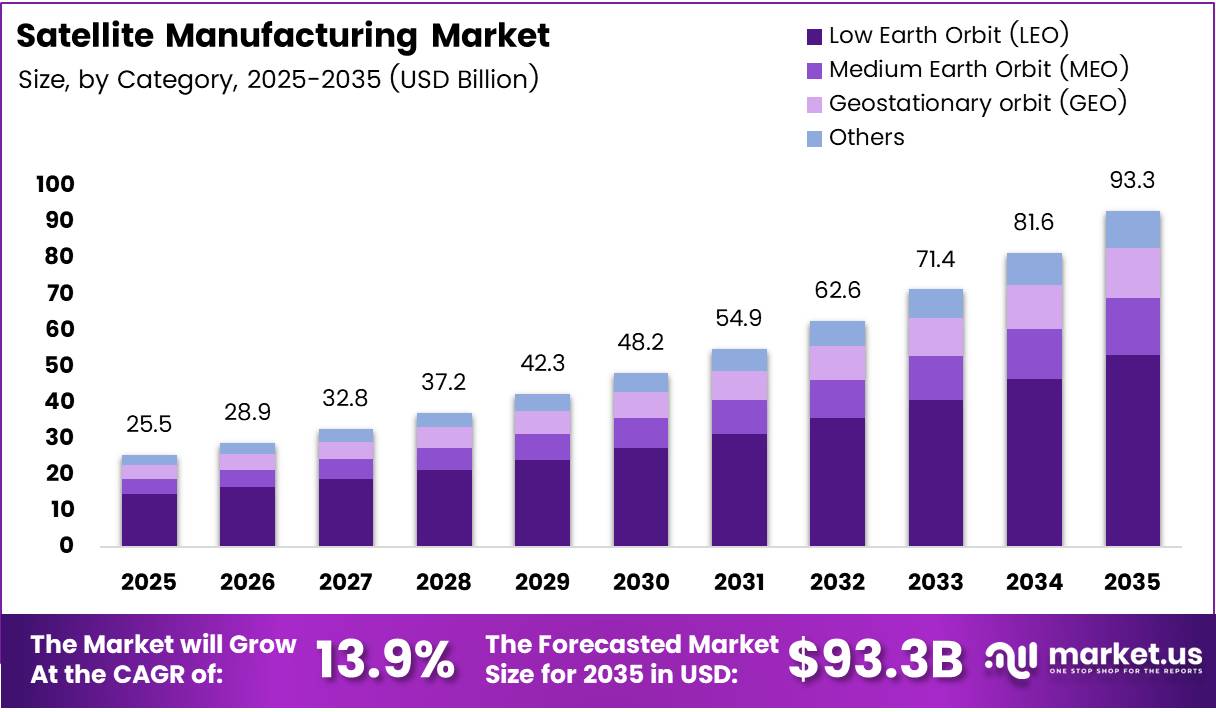

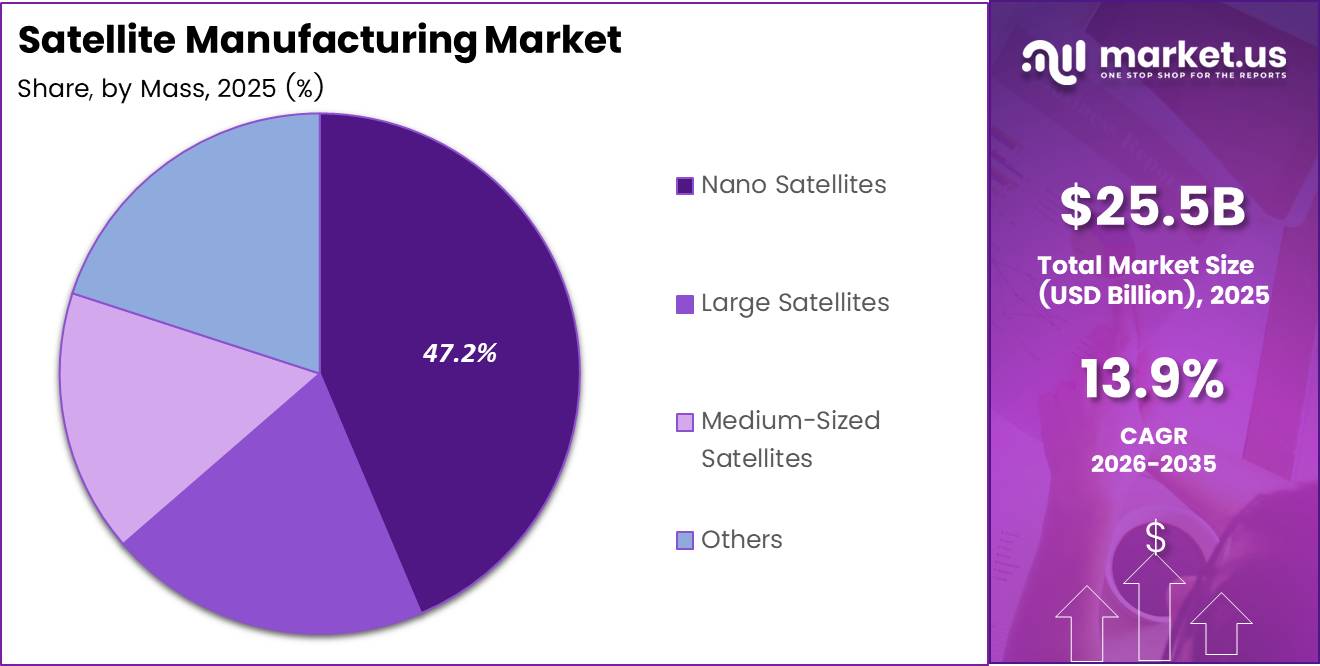

Global Satellite Manufacturing Market size is expected to be worth around USD 93.3 Billion by 2035 from USD25.5 Billion in 2025, growing at a CAGR of 13.9% during the forecast period 2026 to 2035.

Satellite manufacturing covers the design, integration, and testing of spacecraft across Low Earth Orbit, Medium Earth Orbit, and Geostationary platforms. The market spans commercial and government buyers purchasing communication, earth observation, navigation, and surveillance assets. This breadth of application makes satellite production one of the most capital-intensive and strategically critical segments in the aerospace sector.

Commercial operators now account for 69.3% of total demand, a share that reflects the fundamental restructuring of satellite procurement away from government-exclusive programs toward commercially driven constellation deployments. This shift compresses manufacturing timelines and forces suppliers to scale production infrastructure that was historically built for single-unit or small-batch government contracts.

LEO satellites represent 56.9% of the market by orbital category, driven by connectivity constellation projects requiring hundreds to thousands of units. This volume dynamic changes the economics of satellite manufacturing entirely — unit economics, not mission complexity, now define competitive advantage for manufacturers targeting this segment.

Nano satellites hold 47.2% share by mass class, signaling that miniaturization has moved from experimental to mainstream. Smaller form factors reduce per-unit cost and launch weight, enabling faster constellation build-out cycles and attracting a new class of commercial and institutional buyers who previously could not afford orbital access.

In April 2026, Amazon announced plans to spend $11 billion on satellite assets to compete directly with Starlink, a move that signals the scale of capital now entering the LEO connectivity race. Commitments of this size from hyperscale technology firms validate the commercial satellite manufacturing pipeline well beyond the current forecast window.

According to eoportal.org, the Pléiades Neo constellation’s 4 satellites deliver a combined daily acquisition capacity of 2,000,000 km² per day — nearly 3× the output of first-generation systems. This performance benchmark illustrates how next-generation satellite architectures compress the hardware required to achieve global imaging coverage, directly informing how defense and commercial earth observation buyers are specifying new procurement programs.

According to eoportal.org, each Pléiades Neo satellite captures 500,000 km² per day at 0.3 m resolution. That per-unit productivity benchmark matters to procurement planners because it sets a new baseline for what acceptable imaging performance looks like — raising the bar for manufacturers competing on sensor and platform capability rather than price alone.

Key Takeaways

- The global Satellite Manufacturing Market is valued at USD 25.5 Billion in 2025 and is forecast to reach USD 93.3 Billion by 2035.

- The market advances at a CAGR of 13.9% from 2026 to 2035.

- By orbital category, Low Earth Orbit (LEO) satellites lead with 56.9% market share.

- By mass class, Nano Satellites hold the largest share at 47.2%.

- By type of business, Commercial buyers represent 69.3% of total market demand.

- By application, Communication satellites account for 38.5% of the market.

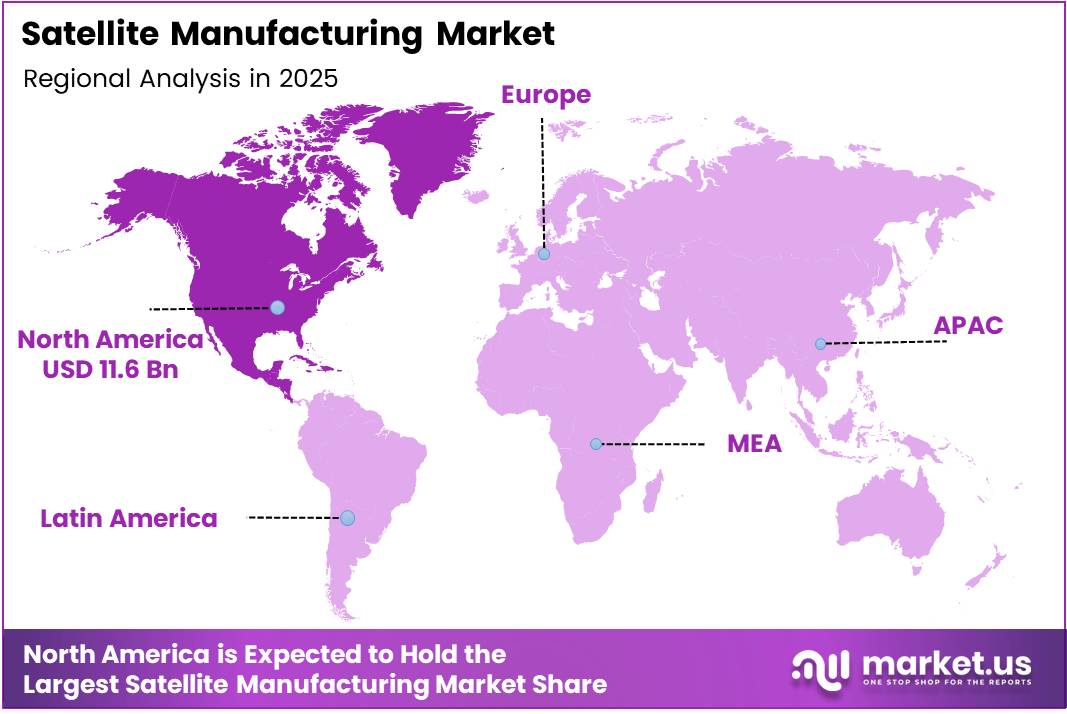

- North America dominates the regional landscape with 45.80% share, valued at USD 11.6 Billion.

Category Analysis

Low Earth Orbit (LEO) dominates with 56.9% due to high-volume constellation deployment demand.

In 2025, Low Earth Orbit (LEO) held a dominant market position in the By Category segment of the Satellite Manufacturing Market, with a 56.9% share. LEO’s leadership reflects the commercial connectivity race, where operators require hundreds to thousands of spacecraft per constellation. This volume dynamic forces manufacturers to industrialize production lines, creating structural advantages for those who invest in assembly-at-scale infrastructure early.

Medium Earth Orbit (MEO) serves as the preferred orbital band for navigation constellations and specialized broadband networks. MEO satellites carry higher per-unit cost and complexity than LEO platforms, limiting the addressable buyer pool to well-capitalized government navigation programs and a narrow set of commercial broadband operators. Consequently, MEO contributes a smaller but high-value slice of total manufacturing revenue.

Geostationary Orbit (GEO) differentiates through long mission lifespans and wide-area coverage from a fixed orbital position. GEO satellites represent the traditional anchor of broadcast and government communication infrastructure. However, the rising performance of LEO constellations is pressuring GEO refresh cycles — buyers now evaluate GEO replacements against hybrid architectures that blend orbital layers.

Others in the orbital category include highly elliptical orbits and emerging cislunar mission profiles. These segments remain niche today but attract R&D investment from space agencies and defense customers exploring persistent polar coverage and deep-space communication relay architectures. Their manufacturing volumes are low but their technical complexity commands premium pricing.

Mass Analysis

Nano Satellites dominate with 47.2% due to low-cost miniaturized platform accessibility.

In 2025, Nano Satellites held a dominant market position in the By Mass segment of the Satellite Manufacturing Market, with a 47.2% share. Their dominance reflects the commercial and institutional shift toward affordable orbital access — nano platforms reduce both manufacturing cost and launch mass, enabling startups, universities, and emerging market space agencies to deploy assets that were previously unaffordable. This democratization effect expands the total addressable buyer base.

Large Satellites carry the highest per-unit revenue within the mass segment and remain the backbone of government defense, deep-space, and high-capacity GEO communication programs. Large satellite contracts are typically long-cycle, high-margin programs that anchor manufacturer backlogs. However, competition from constellations of smaller platforms is gradually compressing the use cases where large, single-asset spacecraft are the preferred solution.

Medium-Sized Satellites occupy the performance-cost middle ground, favored by earth observation operators and government remote sensing programs that require more capability than nano platforms but cannot justify large spacecraft budgets. Medium platforms are gaining share in dual-use applications where imaging resolution and revisit frequency must both meet commercial and defense requirements simultaneously.

Others in the mass classification include microsatellites and picosatellites — form factors that sit between defined mass bands and serve highly specialized missions. These platforms are increasingly used for in-orbit technology demonstration, where low cost per unit allows operators to validate new sensors or propulsion systems without committing to a full-scale program.

Type of Business Analysis

Commercial buyers dominate with 69.3% due to large-scale private constellation investment.

In 2025, Commercial buyers held a dominant market position in the By Type of Business segment of the Satellite Manufacturing Market, with a 69.3% share. This majority position signals a structural market shift — private operators now set the production volume and technology specification agenda that manufacturers must meet. Vendors unable to align with commercial procurement timelines and pricing structures will find themselves progressively locked out of the largest order books.

Government procurement remains essential to manufacturer financial stability because government contracts carry longer durations, higher technical specifications, and more predictable revenue profiles than commercial programs. However, the government share of total manufacturing demand has compressed as commercial constellation programs scale. Manufacturers serving both segments benefit from government contracts that fund advanced capability development, which then feeds into commercial platform upgrades.

Application Analysis

Communication satellites dominate with 38.5% due to broadband connectivity infrastructure demand.

In 2025, Communication satellites held a dominant market position in the By Application segment of the Satellite Manufacturing Market, with a 38.5% share. Broadband connectivity constellations targeting underserved and maritime markets are the primary demand driver. The scale of investment by hyperscale technology firms confirms that satellite-delivered internet has moved from a niche service to a core infrastructure category with global competitive significance.

Earth Observation and Remote Sensing represents the fastest-evolving application segment in terms of sensor performance requirements. Commercial operators now specify sub-meter imaging resolution and daily revisit capability as standard procurement criteria — performance thresholds that push manufacturers to integrate advanced optics and precise attitude control systems into increasingly compact platforms.

Navigation satellites underpin critical infrastructure across aviation, maritime, and autonomous vehicle sectors. Sovereign navigation programs in Europe, China, and India continue to drive steady government procurement, while commercial augmentation services create parallel demand for navigation payload manufacturing. The security sensitivity of this application means government buyers retain strong influence over supplier qualification.

Research and Development satellites serve as testbeds for next-generation propulsion, materials, and sensor technologies. Space agencies allocate R&D satellite budgets to validate technologies before committing to operational programs, creating a structured pipeline of small-to-medium platform contracts that feed future LEO and GEO production runs.

Military Surveillance satellites represent a high-value, low-volume segment with strict supplier qualification requirements. Defense procurement programs prioritize encryption-capable data links, hardened components, and extended mission lifespans. These specifications increase manufacturing complexity and cost but also create defensible supplier positions that commercial-only manufacturers cannot easily enter.

Others within the application segment include weather monitoring, scientific research, and technology demonstration missions. These programs are typically funded by national space agencies and international research bodies, providing stable if modest volumes that help manufacturers maintain capability across a wide platform range.

Key Market Segments

By Category

- Low Earth Orbit (LEO)

- Medium Earth Orbit (MEO)

- Geostationary Orbit (GEO)

- Others

By Mass

- Nano Satellites

- Large Satellites

- Medium-Sized Satellites

- Others

By Type of Business

- Commercial

- Government

By Application

- Communication

- Earth Observation and Remote Sensing

- Navigation

- Research and Development

- Military Surveillance

- Others

Drivers

Defense Budgets and Private Capital Together Drive Satellite Production to Industrial Scale

Government defense agencies and commercial constellation operators are simultaneously expanding procurement, creating a dual-demand environment that pushes satellite manufacturing volumes far beyond historical norms. In February 2026, Intuitive Machines committed $175 million to advance satellite capabilities following its Lanteris acquisition — a direct signal that private capital is now funding production-scale infrastructure, not just mission-level contracts.

LEO constellation programs require manufacturers to produce hundreds of spacecraft per program cycle, a volume discipline that legacy aerospace supply chains were not designed to handle. According to eoportal.org, Pléiades Neo laser communication terminals are 60% lighter and smaller than previous-generation units — illustrating that miniaturization advances are enabling higher-performance satellites at lower production cost, which directly accelerates commercial buyer adoption.

Earth observation and climate monitoring mandates from both defense agencies and environmental regulatory bodies generate recurring procurement cycles. Buyers now specify daily global revisit capability as a minimum operational requirement, which forces manufacturers to design platforms with higher agility and faster production cadence. This performance specification shift locks in demand for advanced manufacturing capability over the entire forecast period.

Restraints

Capital Intensity and Supply Chain Fragility Slow Satellite Production Scale-Up

Satellite manufacturing requires sustained capital investment in cleanroom facilities, precision tooling, and space-grade component inventories before a single unit ships. These upfront costs create a high barrier for new market entrants and limit the speed at which established manufacturers can expand capacity to meet order surges from commercial constellation programs.

Space-grade components — radiation-hardened electronics, specialized propulsion materials, and precision optical assemblies — depend on a concentrated supplier base with limited geographic redundancy. Any disruption to this supply chain, whether from geopolitical trade restrictions or single-source supplier failures, cascades directly into program delays. Manufacturers cannot substitute commercial-grade components without redesign cycles that extend delivery timelines by months.

Complex manufacturing processes involving vibration testing, thermal vacuum qualification, and RF compatibility verification cannot be compressed without risking mission failure. These technical realities impose minimum production cycle times that constrain how rapidly manufacturers can respond to new contract awards. For buyers with urgent operational requirements, this lag creates a structural gap between order placement and deployment readiness.

Growth Factors

Modular Designs, SataaS Models, and Commercial Partnerships Open New Revenue Channels

Modular satellite architectures allow manufacturers to build standardized bus platforms and swap mission-specific payloads, compressing both design cycles and per-unit production cost. This approach lets manufacturers serve multiple application segments — communication, observation, navigation — from a shared production infrastructure, improving factory utilization and reducing the capital cost per delivered spacecraft.

Satellite-as-a-Service (SataaS) business models shift buyer relationships from one-time hardware procurement to recurring data and capacity subscriptions. In April 2026, Amazon moved to expand its Leo satellite network through the Globalstar acquisition, demonstrating that hyperscale technology operators now view satellite capacity as a managed service asset. According to eoportal.org, Pléiades Neo achieves 0.3 m ground sample distance versus 0.5 m for first-generation systems — a 40% resolution improvement that raises the performance floor buyers expect from SataaS providers.

IoT-enabled satellite networks connect remote industrial assets across agriculture, energy, and logistics sectors where terrestrial networks do not reach. This application category generates demand for large numbers of low-cost, purpose-built LEO platforms — a production profile that benefits manufacturers with standardized nano and small satellite assembly lines. Partnerships between commercial operators and national space agencies accelerate market entry in regulated sectors where government endorsement determines procurement eligibility.

Emerging Trends

Reusable Launch Economics, AI-Driven Design, and Mega-Constellation Scale Reshape Satellite Manufacturing

Reusable launch vehicles reduce the per-kilogram cost of reaching orbit, which directly changes how satellite manufacturers design platforms. When launch cost falls, operators tolerate heavier or more capable satellites, shifting the performance-cost tradeoff that has historically driven miniaturization. Manufacturers who understand this dynamic can now offer higher-capability platforms without pricing themselves out of commercial programs.

AI-driven satellite design tools compress the engineering cycle by automating fault analysis, thermal modeling, and component selection. These tools reduce the labor cost embedded in each design iteration, making it commercially viable to develop custom platforms for smaller buyer segments. Additionally, 3D printing of satellite structural components is cutting lead times on precision parts that previously required months of machined fabrication.

According to eoportal.org, the Pléiades Neo constellation delivers 2,000,000 km² of daily acquisition capacity — approximately 2.9× the 700,000 km² delivered by first-generation Pléiades 1A/1B satellites. Mega-constellation programs now set coverage benchmarks at this scale, compelling manufacturers to build production systems capable of delivering dozens of spacecraft annually. Early movers who establish high-throughput manufacturing infrastructure will hold a durable cost advantage as constellation refresh cycles accelerate.

Regional Analysis

North America Dominates the Satellite Manufacturing Market with a Market Share of 45.80%, Valued at USD 11.6 Billion

North America commands 45.80% of the global market, valued at USD 11.6 Billion, driven by a combination of established defense procurement programs, a mature commercial space sector, and a deep supply chain of space-grade component manufacturers. The United States government’s sustained satellite investment and the concentration of major private constellation operators in this region create a structural demand base that competitors in other geographies cannot quickly replicate.

Europe Satellite Manufacturing Market Trends

Europe maintains a strong position through its sovereign launch infrastructure and institutional procurement programs managed through the European Space Agency and national defense agencies. The region’s manufacturing base supports both GEO broadcast and MEO navigation programs, with OHB’s November 2025 acquisition of a TechniSat production facility signaling active capacity expansion to capture a larger share of next-generation constellation contracts.

Asia Pacific Satellite Manufacturing Market Trends

Asia Pacific advances through government-led national space programs in China, Japan, India, and South Korea, each pursuing sovereign satellite manufacturing capability to reduce dependency on Western suppliers. China’s state-directed investment in LEO mega-constellations and India’s expanding commercial launch and manufacturing ecosystem position this region as the fastest-scaling production geography outside North America over the forecast period.

Middle East and Africa Satellite Manufacturing Market Trends

Middle East and Africa represent an emerging procurement market rather than a manufacturing base, with Gulf state space agencies contracting European and North American manufacturers for communication and earth observation platforms. However, the UAE’s Mohamed bin Rashid Space Centre and Saudi Arabia’s space program are establishing domestic assembly and integration capabilities that will gradually shift some manufacturing activity into the region.

Latin America Satellite Manufacturing Market Trends

Latin America’s satellite manufacturing activity concentrates in Brazil and Argentina, where national aerospace agencies maintain technical capability for small satellite development. Regional demand for earth observation and communication services outpaces local manufacturing capacity, meaning most procurement flows to North American and European suppliers. Domestic program investment remains constrained by public budget priorities competing against other infrastructure needs.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Airbus SE positions itself as a vertically integrated satellite manufacturer capable of serving both GEO telecommunication programs and high-resolution earth observation constellations. Its control over satellite bus design, payload integration, and ground segment architecture gives it negotiating leverage with institutional buyers that systems integrators without in-house manufacturing cannot match. This integration depth creates switching costs that sustain long-term customer relationships.

ArianeGroup combines launch vehicle expertise with satellite propulsion and manufacturing capability, giving it a structurally advantaged position as operators seek single-source accountability across the launch-to-orbit value chain. Its alignment with European sovereign space policy means it benefits from defense and institutional procurement that prioritizes European supply chain independence — a policy driver that insulates its order book from pure commercial price competition.

The Boeing Company leverages its defense contracting relationships and large satellite manufacturing heritage to target high-value government and military programs that require radiation-hardened components, encrypted payloads, and multi-year support contracts. Boeing’s scale in defense procurement means its satellite division benefits from shared supplier relationships and political access that smaller specialized manufacturers cannot replicate.

Lockheed Martin Corporation focuses on next-generation military and national security satellite programs where performance requirements exceed what commercial platforms can deliver. Its investment in advanced manufacturing techniques and government-cleared facilities positions it as the preferred supplier for programs that carry the highest technical and security specifications. This niche creates a defensible revenue base that is structurally insulated from commercial price pressure.

Key Players

- Airbus SE

- ArianeGroup

- Azista BST Aerospace

- The Boeing Company

- Dhruva Space Private Limited

- Gilmour Space Technologies

- INVAP

- Lockheed Martin Corporation

- Maxar Technologies Inc

- Mitsubishi Electric Corporation

- Northrop Grumman

Recent Developments

- March 2026 – York Space acquired satellite propulsion manufacturer Orbion Space, adding in-house propulsion capability to its small satellite production platform. This vertical integration move reduces York’s dependency on third-party propulsion suppliers and strengthens its competitive position in high-volume LEO constellation contracts.

- April 2026 – Amazon announced plans to acquire Globalstar and expand its Amazon Leo satellite network, intensifying direct competition with Starlink in the satellite internet market. The acquisition positions Amazon to deploy additional orbital capacity beyond its existing Project Kuiper constellation commitments.

- November 2025 – OHB acquired a TechniSat production facility to expand its satellite manufacturing capacity across European programs. This investment signals OHB’s intention to capture a larger share of next-generation constellation and government satellite contracts as European procurement volumes increase.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 25.5 Billion |

| Forecast Revenue (2035) | USD 93.3 Billion |

| CAGR (2026-2035) | 13.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Category (Low Earth Orbit, Medium Earth Orbit, Geostationary Orbit, Others), By Mass (Nano Satellites, Large Satellites, Medium-Sized Satellites, Others), By Type of Business (Commercial, Government), By Application (Communication, Earth Observation and Remote Sensing, Navigation, Research and Development, Military Surveillance, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Airbus SE, ArianeGroup, Azista BST Aerospace, The Boeing Company, Dhruva Space Private Limited, Gilmour Space Technologies, INVAP, Lockheed Martin Corporation, Maxar Technologies Inc, Mitsubishi Electric Corporation, Northrop Grumman |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |