Quick Navigation

Report Overview

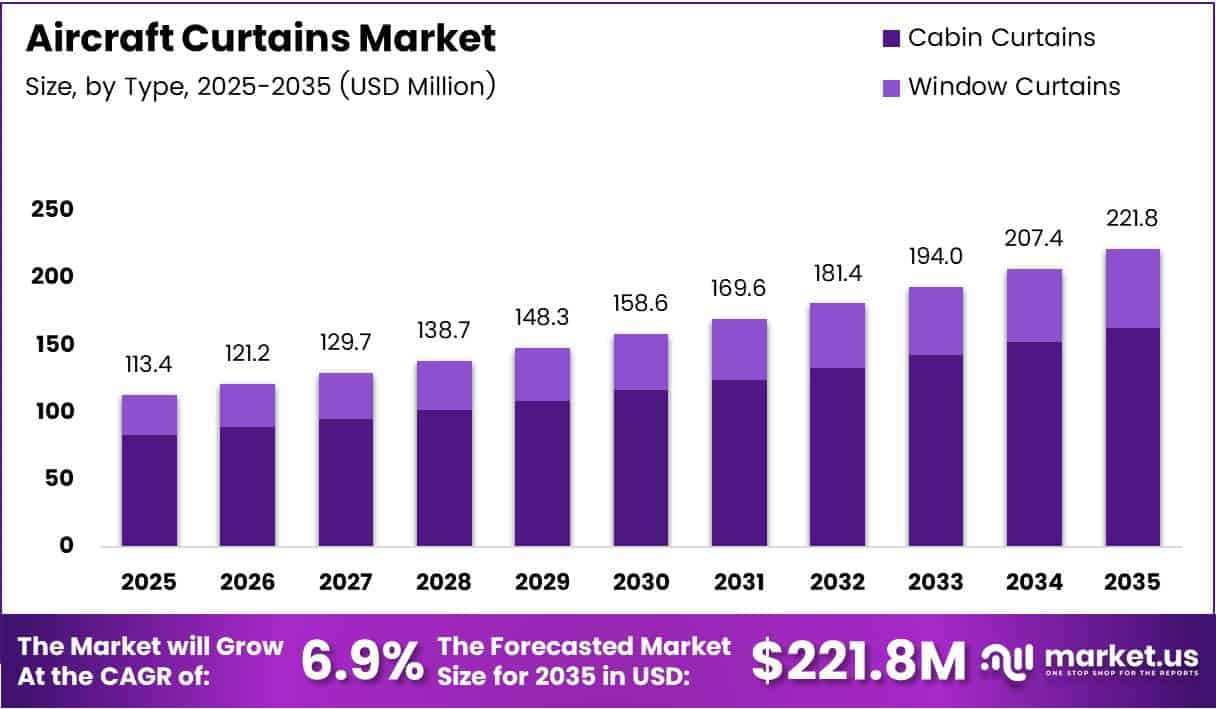

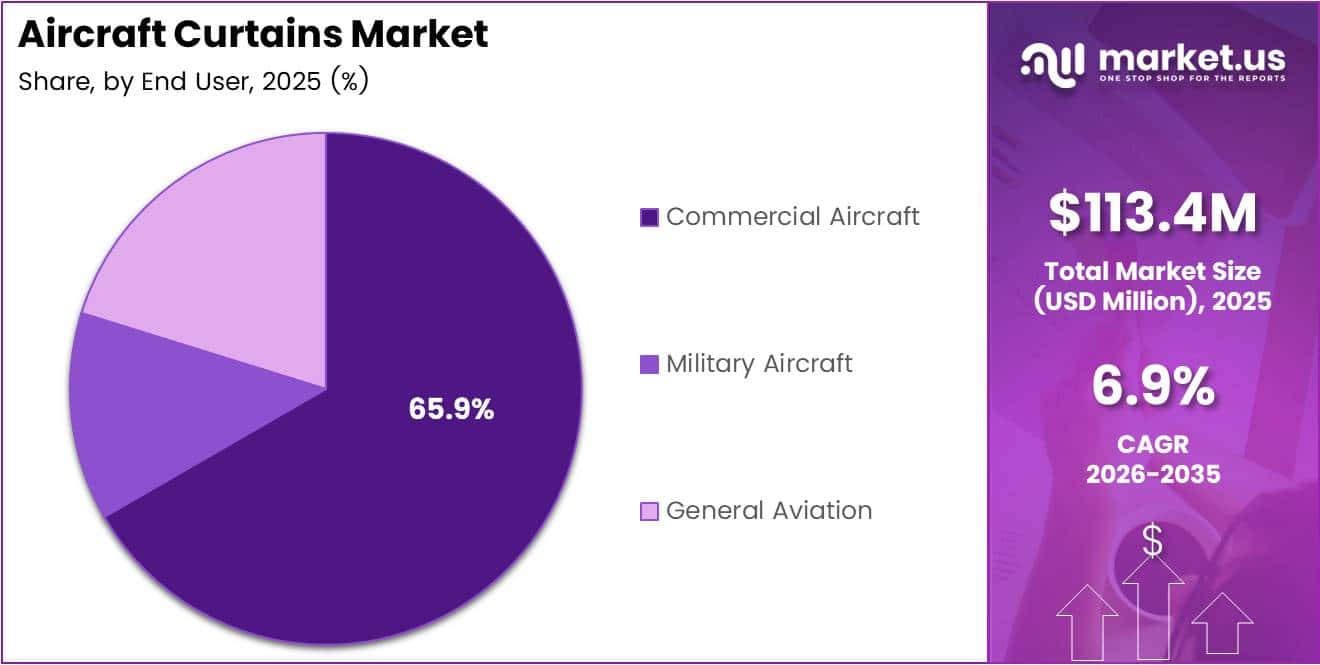

Global Aircraft Curtains Market size is expected to be worth around USD 221.8 Million by 2035 from USD 113.4 Million in 2025, growing at a CAGR of 6.9% during the forecast period 2026 to 2035.

Aircraft curtains are specialized textile products used inside commercial, military, and general aviation aircraft to separate cabin zones, provide passenger privacy, and comply with aviation fire safety mandates. These products are engineered components subject to strict regulatory testing, not simple furnishing items.

Cabin curtains serve a structural function in cabin management. Airlines use them to define business class, premium economy, and economy boundaries — directly influencing how passengers perceive service quality. As airlines compete on cabin experience, curtain specifications have become a deliberate product decision rather than a compliance afterthought.

Commercial aviation accounts for the dominant share of this market, with 65.9% of demand. This concentration reflects the scale of widebody and narrowbody fleets requiring certified cabin textiles. Every aircraft in commercial service carries multiple curtain positions, creating recurring replacement and retrofit demand across airline maintenance cycles.

The market’s 6.9% CAGR signals that fleet expansion in Asia Pacific and the Middle East, combined with accelerating cabin upgrade programs in mature markets, is generating procurement volumes that outpace pre-pandemic replacement cycles. Suppliers with certified, multi-performance materials are best positioned to capture this shift.

Aviation safety regulation drives material specification at a foundational level. According to BusinessWire, under FAR/CS 25.853 vertical flammability requirements, fire in cabin interior materials including curtains must not spread more than 43.2 cm (17 in) from the ignition source during testing. This mandatory threshold eliminates standard textiles from aircraft use entirely, creating a protected category for certified curtain manufacturers.

Material engineering is now a core competitive axis. According to airtraveldesign.guide, moving from heavy woven wool to lightweight polyester-blend textiles reduces fabric areal density from 300–400 g/m² down to 150–250 g/m² — roughly a 30–50% reduction in fabric mass per square metre while still meeting FAR 25.853 requirements. This means airlines can reduce cabin weight without sacrificing compliance.

Government safety mandates and airline fleet investment strategies together create a market where demand is structurally embedded in aircraft operations. Procurement decisions involve engineering validation, not just purchasing preference — which means barriers to entry remain high and established certified suppliers hold durable revenue positions.

Key Takeaways

- The global Aircraft Curtains Market was valued at USD 113.4 Million in 2025 and is forecast to reach USD 221.8 Million by 2035.

- The market advances at a CAGR of 6.9% over the forecast period 2026 to 2035.

- By Type, Cabin Curtains dominate with a 73.5% market share in 2025.

- By End User, Commercial Aircraft leads with a 65.9% share, reflecting large fleet volumes.

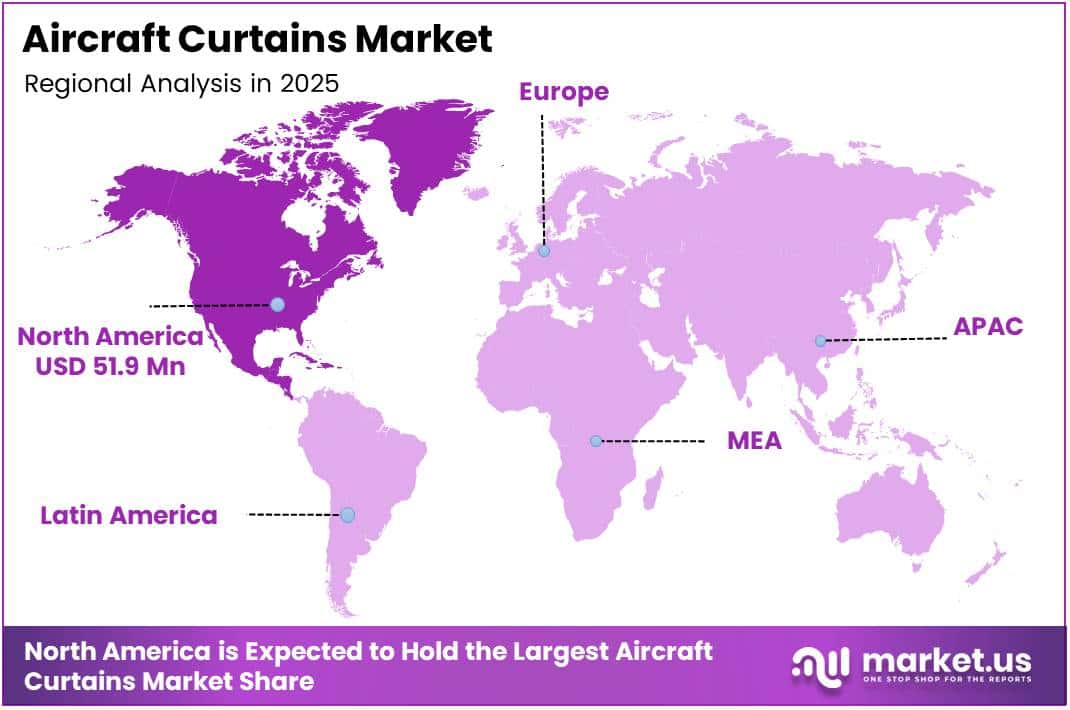

- North America holds the largest regional share at 45.80%, valued at USD 51.9 Million.

- Military Aircraft and General Aviation represent the remaining end-user segments with measurable growth potential.

- Window Curtains constitute the secondary product type, serving as cabin light-control and aesthetic components.

Product Analysis

Cabin Curtains dominate with 73.5% due to mandatory zone separation in certified cabins.

In 2025, Cabin Curtains held a dominant market position in the By Type segment of the Aircraft Curtains Market, with a 73.5% share. Every transport-category aircraft requires certified curtains to physically separate cabin classes and crew areas, making cabin curtains a non-discretionary procurement item embedded in aircraft delivery and maintenance cycles.

Window Curtains serve a distinct functional role focused on light management and thermal comfort at individual seating positions. Airlines in long-haul premium markets specify window curtains as part of differentiated cabin aesthetics. However, lower unit counts per aircraft and longer replacement intervals keep this segment’s revenue contribution well below that of cabin dividers.

End-User Analysis

Commercial Aircraft dominates with 65.9% due to large fleet scale and continuous retrofit cycles.

In 2025, Commercial Aircraft held a dominant market position in the By End User segment of the Aircraft Curtains Market, with a 65.9% share. The sheer volume of widebody and narrowbody aircraft in global commercial service creates recurring replacement demand. Airlines replace cabin textiles during scheduled maintenance and cabin refresh programs, sustaining a predictable procurement pipeline for certified curtain suppliers.

Military Aircraft represents a procurement channel governed by defense budgets and government specifications rather than competitive tender. Curtain requirements in military aircraft differ from commercial applications — focusing on operational durability and tactical compartmentalization. This segment offers stable, albeit lower-volume, revenue for suppliers who hold defense-specific material certifications.

General Aviation captures the smallest share but carries disproportionate margin potential. Business jet completions and private aircraft interiors command premium material specifications, with owners prioritizing bespoke design and high-quality fabric. Consequently, general aviation buyers tend to spend significantly more per unit than commercial airlines operating at scale-driven procurement terms.

Key Market Segments

By Type

- Cabin Curtains

- Window Curtains

By End User

- Commercial Aircraft

- Military Aircraft

- General Aviation

Drivers

Aviation Safety Mandates and Fleet Expansion Force Systematic Cabin Curtain Procurement

FAR/CS 25.853 flammability requirements apply simultaneously to seat covers, carpets, curtains, and wall coverings across all transport-category aircraft. When airlines upgrade safety specifications or refresh cabin branding, regulations push them to replace entire textile sets rather than individual items. This regulatory structure converts periodic cabin overhauls into multi-SKU procurement events for certified curtain suppliers.

Fleet expansion across emerging economies in Asia Pacific and the Middle East directly multiplies aircraft interior procurement volumes. Each new widebody delivery includes multiple curtain positions covering business class, premium economy, and galley zones. Moreover, Air New Zealand’s October 2024 comprehensive upgrade of its Boeing 787-9 fleet — installing high-density privacy curtains as part of its Skynest cabin overhaul — illustrates how premium cabin investment programs generate discrete, high-value curtain contracts.

According to airtraveldesign.guide, multi-layer sound-absorbing divider solutions reduce cabin zone sound levels by 5–8 dB under realistic aircraft conditions. This acoustic performance data gives airlines a functional justification for upgrading curtain systems beyond basic compliance. Therefore, performance-differentiated curtain products now compete on measurable cabin comfort metrics, not just material certification, widening addressable demand beyond simple replacement cycles.

Restraints

High Material Certification Costs and Long Product Lifespans Compress Replacement Frequency

Advanced flame-retardant textile materials certified to aviation standards carry significantly higher production costs than standard industrial fabrics. Curtain suppliers must invest in inherently flame-retardant fibers, intumescent back-coatings, and repeated regulatory testing to maintain certifications. These costs transfer to airlines as premium unit pricing, which budget-conscious carriers frequently resist — particularly on narrowbody fleets where cabin specifications face tighter cost scrutiny.

According to globalplasticsheeting.com, FAA requirements under FAR 25.853 and Appendix F limit peak heat release to 65 kW/m² and smoke density to a specific optical density of 200 in flaming mode. Meeting both thresholds simultaneously requires manufacturers to adopt halogen-free formulations that reduce smoke generation by roughly 30–50% compared to legacy systems. The R&D investment required to achieve this dual compliance adds further cost pressure throughout the supply chain.

Aircraft curtains carry long operational lifespans relative to other cabin consumables. Airlines frequently extend curtain service life beyond initial design specifications, deferring replacements to reduce maintenance expenditure. Consequently, even when airlines operate aging cabin interiors, replacement triggers remain infrequent unless safety authority inspections or brand refresh programs force action — limiting the annual addressable replacement volume available to suppliers.

Growth Factors

Lightweight Materials, Cabin Retrofit Programs, and Smart Textiles Expand the Revenue Base

Cabin modernization programs represent a structural growth channel beyond new aircraft deliveries. Airlines retiring older cabin configurations invest in retrofit programs that include curtain systems as part of broader interior refreshes. According to ensingerplastics.com, replacing heavier interior structures with certified polymer and composite solutions can contribute fuel-burn improvements of 1–2% for widebody aircraft — a direct financial incentive for airlines to adopt lightweight certified curtain materials in retrofit programs.

In December 2024, Safran SA entered a strategic partnership with a material science firm to develop next-generation multifunctional textiles integrating antimicrobial properties directly into aircraft curtain fibers. This development signals that curtain suppliers are expanding product value beyond compliance into hygiene performance — a category that gained strategic importance following the COVID-19 pandemic and which airlines now actively communicate to passengers as a service differentiator.

Business aviation and private jet completions provide a high-margin growth avenue for curtain suppliers. General aviation buyers prioritize bespoke aesthetics and premium fabric quality over cost optimization, creating demand for custom-engineered curtain solutions. Additionally, the integration of digitally printed branding and smart fabric technologies into curtain designs gives airlines a new customization layer — extending curtain product cycles and increasing per-unit value across both commercial and private segments.

Emerging Trends

Sustainability Requirements and Cabin Personalization Redefine Aircraft Curtain Specifications

Airlines now treat cabin sustainability as a measurable commitment rather than a marketing statement. Recycled and halogen-free materials for aircraft curtains address two parallel pressures simultaneously: carbon reduction targets and passenger safety expectations. According to ensingerplastics.com, newer halogen-free flame-retardant systems generate significantly lower toxicity and corrosivity of smoke — meaning airlines can communicate both environmental and safety credentials through material selection decisions.

Digitally printed and branded cabin curtains are shifting from a niche customization to a standard procurement option. Airlines use cabin textiles to reinforce brand identity, especially in premium class where visual differentiation supports yield management. In September 2024, Lantal Textiles AG launched its AeroPure Recycled collection — aircraft curtains made from 100% post-consumer recycled polyester meeting all aviation flammability standards — demonstrating that sustainability and brand performance can co-exist in a single certified product.

Antimicrobial fabric integration and smart textile development represent the next performance tier for aircraft cabin materials. Suppliers who establish certifiable antimicrobial performance standards ahead of regulatory mandates will hold a first-mover advantage in airline procurement cycles. Consequently, material science investment today directly positions suppliers for the next cabin specification refresh wave — particularly among carriers that prioritize passenger health communication as a commercial differentiator.

Regional Analysis

North America Dominates the Aircraft Curtains Market with a Market Share of 45.80%, Valued at USD 51.9 Million

North America leads the global aircraft curtains market with a 45.80% share, valued at USD 51.9 Million in 2025. The region’s dominance reflects the presence of major commercial airline fleets, stringent FAA certification infrastructure, and a mature MRO ecosystem that generates consistent cabin retrofit demand. US carriers’ ongoing cabin modernization investments sustain procurement volumes beyond new aircraft deliveries alone.

Europe Aircraft Curtains Market Trends

Europe holds a substantial secondary position driven by large fleet operators across the UK, Germany, and France, combined with EASA-aligned flammability certification requirements that mirror FAA standards. European airline alliances’ long-haul cabin refresh programs, particularly in business and premium economy classes, generate structured demand for high-specification curtain materials meeting both CS 25.853 compliance and sustainability targets.

Asia Pacific Aircraft Curtains Market Trends

Asia Pacific represents the fastest-expanding regional market, fueled by fleet delivery pipelines across China, India, and Southeast Asia. Low-cost carrier expansion and the growth of widebody fleets among Gulf-connected Asian carriers translate directly into first-fit curtain procurement volumes. Additionally, rising passenger expectations in premium cabins across Chinese and Japanese carriers create demand for higher-specification curtain products beyond basic compliance.

Middle East and Africa Aircraft Curtains Market Trends

The Middle East benefits from aggressive fleet expansion among Gulf carriers pursuing long-haul premium market share. These carriers specify premium cabin materials and invest in frequent interior refreshes to maintain product positioning on competitive intercontinental routes. Africa’s contribution remains nascent but is supported by regional airline development programs that prioritize cabin standards in new fleet acquisitions.

Latin America Aircraft Curtains Market Trends

Latin America’s market contribution is shaped by fleet modernization programs among Brazilian and Mexican carriers replacing aging narrowbody and widebody fleets. Aviation infrastructure investment and gradual low-cost carrier growth in the region generate baseline curtain procurement demand. However, currency volatility and constrained airline capital expenditure budgets in several markets slow the pace of premium cabin upgrade activity.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

ABC International operates as a specialist in aviation cabin textile solutions with positioning centered on compliance-first product development. Its strategic advantage lies in maintaining multi-standard certifications that serve both commercial and military end users simultaneously. This dual-market capability gives ABC International procurement access across segments that most single-focus suppliers cannot address within a single product line.

ACM Aircraft Cabin Modification GmbH has built a competitive position through cabin customization expertise rather than mass-volume production. In February 2025, the company secured an exclusive contract from a newly launched Middle Eastern airline to supply all cabin curtains for its inaugural fleet of 30 widebody aircraft — a contract that validates its ability to serve greenfield airline launches requiring end-to-end cabin textile specification and delivery.

Arville differentiates through advanced technical textile manufacturing capabilities that extend beyond standard curtain production into engineered fabric solutions. Its positioning in the aircraft curtains market leverages industrial weaving expertise applicable to high-performance aviation specifications. This manufacturing depth allows Arville to compete on material performance metrics — including weight, acoustic properties, and flammability compliance — rather than purely on price.

Belgraver Aircraft Interiors focuses on interior completions with curtains as part of a broader cabin furnishing portfolio. This integrated approach gives Belgraver a commercial advantage in contracts where airlines seek single-supplier cabin textile procurement. Consequently, Belgraver captures wallet share across multiple cabin textile categories per airline relationship, reducing the per-contract cost of qualification and certification overhead.

Key Players

- ABC International

- ACM Aircraft Cabin Modification GmbH

- Arville

- Belgraver Aircraft Interiors

- Botany Weaving

- FELLFAB

- Fu-Chi Innovation Technology Co Ltd

- Lantal

- Industrial Neotex SA

- NIEMLA

- Spectra Interior Products

- Vandana Carpets

- EPSILON AEROSPACE

Recent Developments

- September 2024 — Lantal Textiles AG launched its AeroPure Recycled collection, a new aircraft curtain line made from 100% post-consumer recycled polyester. The collection meets all aviation flammability certification standards, positioning Lantal as an early mover in certified sustainable cabin textiles.

- February 2025 — ACM Aircraft Cabin Modification GmbH secured an exclusive contract from a newly launched Middle Eastern airline to supply all cabin curtains for its inaugural fleet of 30 widebody aircraft. This contract establishes ACM as the sole curtain supplier across that carrier’s entire launch fleet.

- May 2025 — Botany Weaving successfully commercialized a new lightweight wool-blend fabric for aircraft curtains that reduces material weight by 15% compared to previous-generation textiles. This weight reduction supports airline fuel efficiency targets without compromising aviation flammability compliance.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 113.4 Million |

| Forecast Revenue (2035) | USD 221.8 Million |

| CAGR (2026-2035) | 6.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Cabin Curtains, Window Curtains), By End User (Commercial Aircraft, Military Aircraft, General Aviation) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | ABC International, ACM Aircraft Cabin Modification GmbH, Arville, Belgraver Aircraft Interiors, Botany Weaving, FELLFAB, Fu-Chi Innovation Technology Co Ltd, Lantal, Industrial Neotex SA, NIEMLA, Spectra Interior Products, Vandana Carpets, EPSILON AEROSPACE |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |