Quick Navigation

Report Overview

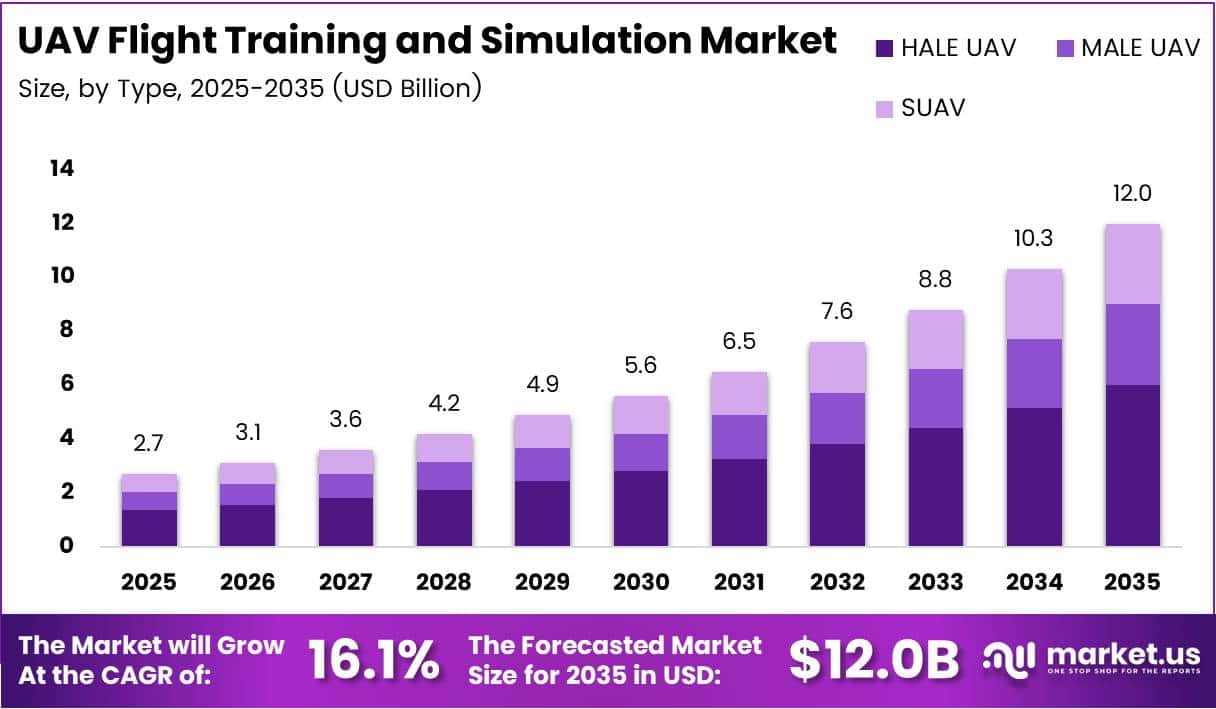

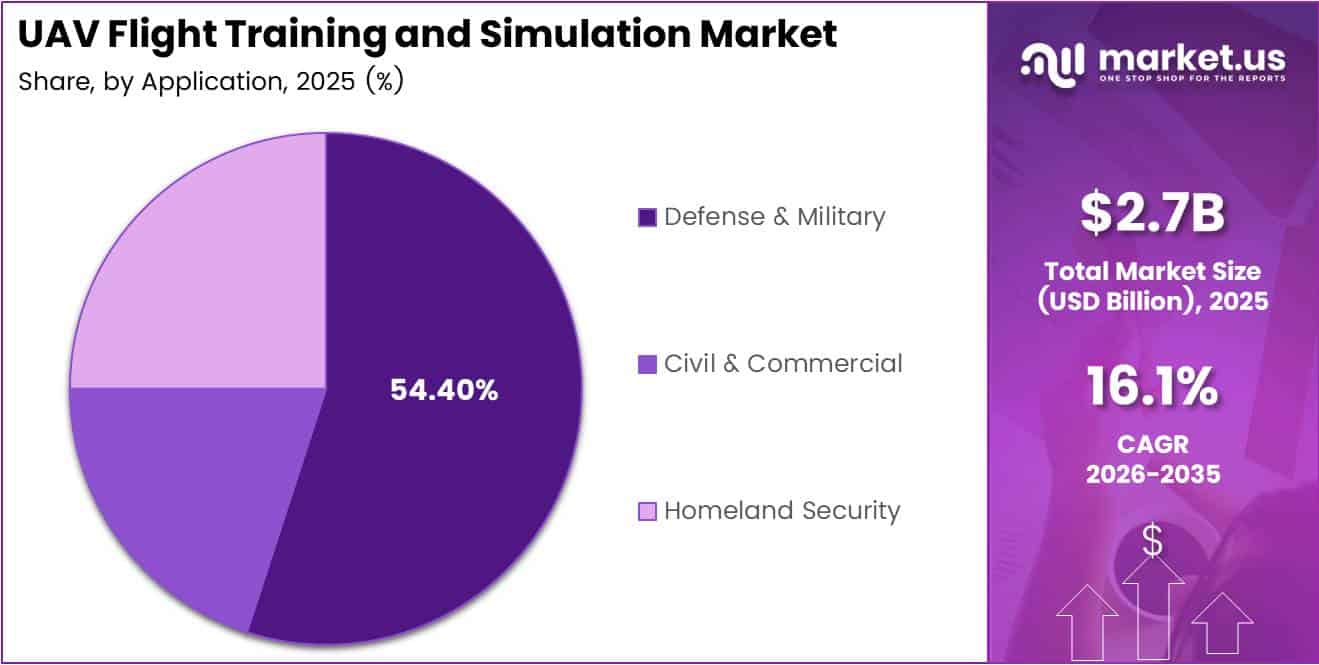

Global UAV Flight Training and Simulation Market size is expected to be worth around USD 12.0 Billion by 2035 from USD 2.7 Billion in 2025, growing at a CAGR of 16.1% during the forecast period 2026 to 2035.

The UAV flight training and simulation market covers purpose-built systems that train drone operators through digital environments, mission rehearsal platforms, and certified instruction programs. Demand extends across defense agencies, commercial aviation bodies, and civil infrastructure operators who require consistent, repeatable, and measurable pilot competency before deployment.

What makes this market structurally resilient is that simulation is not optional for most operators — it is mandated. Aviation authorities globally are tightening certification requirements for commercial and military UAV pilots, converting simulation from a procurement preference into a compliance necessity. This regulatory pressure creates a durable, recurring revenue base for training system vendors.

Defense budgets continue to prioritize UAV training infrastructure as drone platforms multiply across intelligence, surveillance, and combat roles. Military organizations cannot afford operational errors at scale, and simulation directly addresses that risk. The convergence of platform diversity and mission complexity is pushing procurement toward more sophisticated, scenario-based training systems rather than basic flight instruction.

On the commercial side, applications in agriculture, infrastructure inspection, logistics, and emergency response are creating a new class of professional drone operators who require structured training pathways. As drone fleets scale, enterprises face a skills gap that classroom instruction alone cannot close — driving investment in simulation-based training programs at the organizational level.

In March 2025, CAE Inc. announced a strategic investment to integrate AI-driven swarm training into its UAV simulation platforms, enabling operators to manage multiple autonomous drones simultaneously. This signals a market shift from single-operator training toward multi-asset mission management — a capability gap that will define the next procurement cycle.

According to a 2025 paper on the Drone Pilot Training Management System, simulation-based training can reduce operational violations by 30%, translating into savings of up to USD 6 million per year for large enterprises by avoiding property damage, injuries, and regulatory penalties. This data point reframes simulation as a cost-avoidance tool, not just a training cost — a distinction that accelerates enterprise procurement decisions.

According to a 2026 article by Extreme Aerial Productions, simulator-trained FPV pilots recorded 60% fewer crashes in their first month compared with pilots who skipped simulation entirely. This outcome demonstrates that measurable safety gains are achievable within weeks of simulator deployment, giving procurement teams a concrete ROI argument at the board level.

Key Takeaways

- The UAV Flight Training and Simulation Market was valued at USD 2.7 Billion in 2025 and is forecast to reach USD 12.0 Billion by 2035.

- The market will expand at a CAGR of 16.1% between 2026 and 2035.

- By Type, HALE UAV leads the market with a dominant share of 43.9%.

- By Application, Defense and Military holds the largest share at 54.40%.

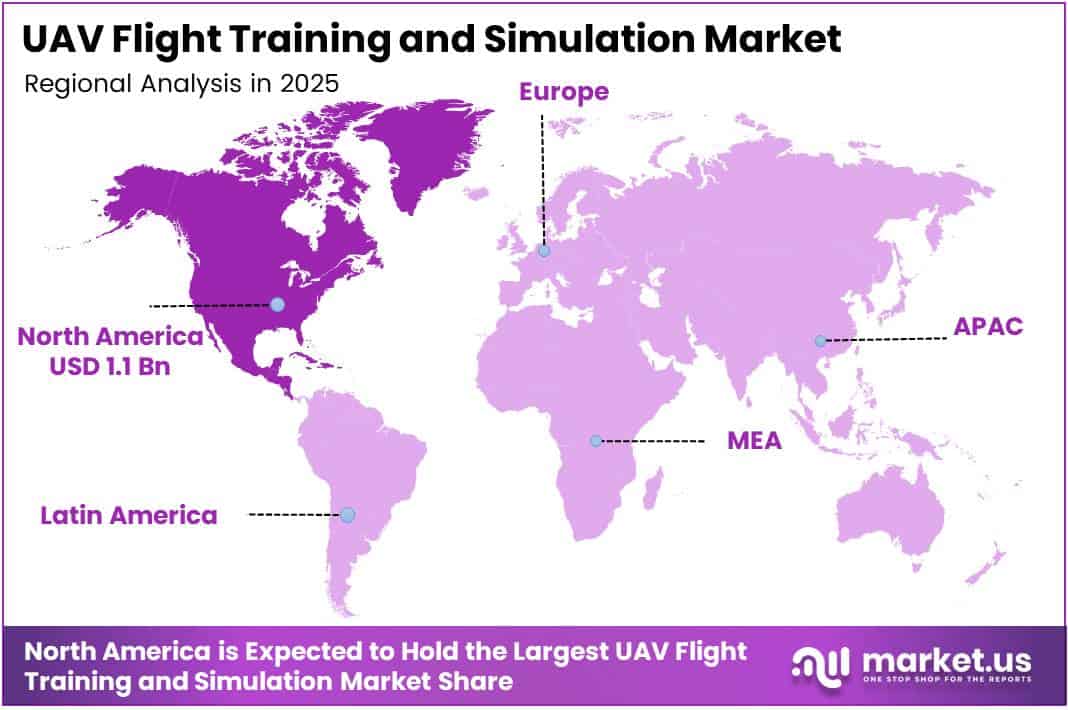

- North America leads all regions with a 43.7% market share, valued at USD 1.1 Billion.

- Key players include CAE Inc., Textron Inc., ELBIT SYSTEMS LTD., Boeing, General Atomics Aeronautical Systems, Inc., and others.

Type Analysis

HALE UAV dominates with 43.9% due to high-altitude defense and persistent surveillance demand.

In 2025, HALE UAV held a dominant market position in the By Type segment of the UAV Flight Training and Simulation Market, with a 43.9% share. High-altitude long-endurance platforms operate in the most complex flight environments, requiring extensive simulation before deployment. Their dominance in training demand reflects the operational complexity and high replacement cost of HALE assets in defense fleets.

MALE UAV serves as the operationally versatile tier between tactical and strategic drone categories. Medium-altitude long-endurance platforms are widely used across both military reconnaissance and border patrol roles, creating consistent training requirements for a broader operator base. MALE systems require regular recertification cycles, generating recurring demand for simulation platform subscriptions and structured training programs.

SUAV (Small UAV) carries the highest volume of new operator entry points across both commercial and military applications. Small UAVs are the fastest-growing deployment category in civil applications, including infrastructure inspection and public safety. However, their lower per-unit cost also means training budgets are tighter, pushing buyers toward scalable software-based simulation over dedicated hardware rigs.

Application Analysis

Defense and Military dominates with 54.40% due to mandatory certification and high-stakes operational requirements.

In 2025, Defense and Military held a dominant market position in the By Application segment of the UAV Flight Training and Simulation Market, with a 54.40% share. Military organizations treat simulation as mission-critical infrastructure, not discretionary training spend. The scale of drone deployments across ISR, strike, and logistics roles creates institutional demand for high-fidelity, scenario-based training at every procurement cycle.

Civil and Commercial applications represent the fastest-expanding buyer category outside defense, covering sectors including agriculture, construction inspection, package delivery, and media production. Commercial operators face an evolving regulatory landscape that increasingly ties licensed operations to documented simulation hours. As regulatory frameworks formalize, civil and commercial training demand moves from voluntary to compliance-driven.

Homeland Security differentiates through requirements for rapid response simulation and multi-agency coordination scenarios. Border surveillance, disaster response, and critical infrastructure protection all require drone operators trained in high-pressure, time-sensitive missions. This creates demand for specialized simulation environments beyond standard flight training, including threat identification, communication protocols, and automated handoff procedures.

Key Market Segments

By Type

- HALE UAV

- MALE UAV

- SUAV

By Application

- Defense & Military

- Civil & Commercial

- Homeland Security

Drivers

Mandatory Certification Requirements and Defense Investment Accelerate UAV Simulation Adoption

Aviation authorities globally are tightening operator certification requirements, converting simulation from a training preference into a compliance obligation. Defense agencies face the same pressure at scale — drone fleet expansion across ISR and combat roles requires trained operators faster than traditional flight programs can deliver. Simulation compresses training timelines without sacrificing safety standards.

Military procurement budgets increasingly allocate dedicated funding for UAV training infrastructure, reflecting the lesson that platform investment without operator readiness creates operational risk. Agriculture, logistics, and inspection sectors are adding professional drone operators at scale, and no organization can afford to train entirely on live aircraft. According to Extreme Aerial Productions (2026), simulator graduates self-reported 40% higher operational confidence than pilots who trained only in real-world environments — a measurable readiness advantage that procurement teams cite directly.

In March 2025, CAE Inc. announced integration of AI-driven swarm training into its simulation platforms, enabling multi-drone mission management at scale. This development illustrates that defense and commercial buyers are not just purchasing basic flight simulators — they are investing in mission rehearsal systems. The shift from single-operator to multi-asset training scenarios expands both the addressable market and the average contract value for simulation vendors.

Restraints

Fragmented Regulatory Standards and High System Costs Limit Uniform Market Penetration

No global standard governs UAV operator certification. Different countries and aviation bodies apply different hour requirements, syllabus structures, and hardware specifications for approved training systems. This fragmentation forces vendors to develop market-specific variants of their platforms, increasing development costs and extending sales cycles — particularly in emerging markets where regulatory frameworks are still forming.

Advanced simulation systems carry high upfront capital costs that smaller training providers and emerging-market operators cannot readily absorb. A full-fidelity HALE or MALE simulator requires significant hardware investment, specialized software licensing, and facility integration. For independent training schools and defense forces in lower-income regions, these costs create a barrier that delays adoption even where demand exists.

The combined effect of regulatory inconsistency and capital barriers creates a two-speed market. Large defense contractors and established training institutions can absorb both the compliance complexity and the hardware investment. Smaller operators and new market entrants cannot — meaning the addressable market remains structurally narrower than raw drone adoption figures suggest, until regulations harmonize and hardware costs decrease through scale.

Growth Factors

VR, AR Integration and Commercial Drone Expansion Create New Revenue Channels for Training Vendors

Virtual and augmented reality platforms are reducing the hardware cost of high-fidelity simulation by replacing physical cockpit rigs with software-driven immersive environments. This cost reduction opens the market to mid-tier buyers — commercial training schools, regional defense units, and enterprise fleet operators — who previously could not justify full simulation investments. VR-based platforms also enable remote delivery, removing geographic barriers to training access.

Growth in commercial drone applications across agriculture, bridge inspection, and logistics is creating new professional operator segments that require structured training at scale. According to a 2025 transportation engineering report published by ABC-UTC at FIU, increasing battery capacity from 4,000 mAh to 6,000 mAh extended simulated UAV flight duration, allowing more inspection waypoints per mission. This finding supports the case for simulation in operational planning — not just operator certification — expanding the product’s value proposition.

Partnerships between training institutes and UAV manufacturers represent a structural growth mechanism that creates captive training pipelines. When a manufacturer certifies only specific training programs for their platform, they generate recurring simulation revenue tied directly to fleet sales. Online and remote drone training programs further extend market reach, enabling vendors to serve operators in geographically dispersed markets without investing in physical training infrastructure.

Emerging Trends

AI-Driven Scenario Simulation and Cloud Platforms Redefine UAV Training Architecture

Artificial intelligence is moving UAV training from static mission scripts to adaptive, real-time scenario generation. AI-based systems adjust difficulty, introduce unexpected variables, and assess pilot decision-making in ways that fixed simulation programs cannot. For defense buyers, this capability creates training environments that more closely replicate actual operational uncertainty — a capability gap that traditional simulators leave open.

Cloud-based training platforms are separating simulation delivery from physical hardware dependency. Operators can access standardized training modules remotely, and program administrators can update scenarios without hardware replacements. This shift has meaningful cost implications: it lowers the total cost of ownership for training operators while enabling vendors to generate recurring subscription revenue rather than one-time hardware sales.

According to a 2026 study published in Nature, simulation-trained UAV control systems using an MPC–PID hybrid approach reduced system settling time from 3.15 seconds to 2.47 seconds — a 21.6% improvement — while keeping steady-state tracking error within 5%. This demonstrates that autonomous UAV training systems developed in simulation environments produce measurable performance gains. For the market, it means simulation is moving from operator training into autonomous systems development — a new and higher-value application layer.

Regional Analysis

North America Dominates the UAV Flight Training and Simulation Market with a Market Share of 43.7%, Valued at USD 1.1 Billion

North America holds 43.7% of the global market, valued at USD 1.1 Billion in 2025. The United States drives this position through the largest defense UAV budget globally, mature FAA regulatory frameworks requiring operator certification, and a dense concentration of prime defense contractors investing in proprietary simulation infrastructure. These structural conditions create institutional procurement cycles that are difficult for other regions to replicate quickly.

Europe UAV Flight Training and Simulation Market Trends

Europe maintains a strong secondary position driven by NATO member defense modernization programs and EASA’s progressive UAV regulatory framework, which mandates certified training for commercial operators. Countries including the UK, France, and Germany are allocating defense budgets specifically to drone operator readiness, creating government-backed demand. European commercial drone adoption in agriculture and logistics further sustains civil training demand.

Asia Pacific UAV Flight Training and Simulation Market Trends

Asia Pacific is the fastest-expanding region for UAV flight training investment. China operates the world’s largest commercial drone fleet, requiring a scaled training infrastructure that simulation platforms are positioned to fill. India’s defense modernization program and expanding agricultural drone use are both creating public and private training procurement. Regional aviation authorities are actively developing UAV certification standards that will formalize simulation requirements at scale.

Middle East and Africa UAV Flight Training and Simulation Market Trends

The Middle East drives regional demand through high-value defense procurement, with Gulf states investing in sovereign UAV capability that includes domestic operator training infrastructure. The UAE and Saudi Arabia have both launched national drone programs that depend on structured simulation training. Africa remains at an early stage, with demand concentrated in humanitarian and infrastructure inspection applications where simulation budgets are limited.

Latin America UAV Flight Training and Simulation Market Trends

Latin America presents early-stage but structurally sound demand, anchored by agricultural drone adoption in Brazil and Mexico — two of the world’s largest farming economies. As precision agriculture expands, enterprise-scale drone fleets require trained operators across geographically dispersed farm operations, creating demand for remote and online simulation-based training programs. Regulatory frameworks are developing but remain inconsistent across the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

CAE Inc. positions itself as the market’s technology integration leader through its investment in AI-driven swarm simulation, announced in March 2025. By enabling operators to manage multiple autonomous drones simultaneously within a single training environment, CAE addresses a capability requirement that no other major training provider has productized at scale. This positions the company ahead of the next procurement cycle in both defense and commercial fleet management.

Textron Inc. leverages its dual role as both a UAV manufacturer and a training system provider, creating a vertically integrated advantage that competitors without platform assets cannot replicate. In April 2026, Textron Systems secured a USD 9.5 million contract with the US Air Force for Advanced EW Simulation, demonstrating the company’s ability to win high-value, mission-specific training contracts that go beyond standard pilot certification programs.

ELBIT SYSTEMS LTD. competes on the strength of its deep integration with defense operators across Israel, Europe, and the United States, where its simulation systems are embedded directly into platform procurement contracts. This creates a dependency relationship that drives long-term, multi-year training system relationships rather than one-time equipment sales. Elbit’s focus on defense-specific scenario fidelity differentiates it from vendors targeting the commercial segment.

Boeing brings enterprise-scale systems integration experience that allows it to embed UAV simulation within broader defense training ecosystems rather than selling standalone products. Boeing’s competitive advantage lies not in simulation hardware alone but in its ability to bundle training solutions with platform maintenance contracts and operator lifecycle support — a total capability offering that smaller, specialist vendors cannot match at comparable scale.

Key Players

- CAE Inc.

- Textron Inc.

- ELBIT SYSTEMS LTD.

- Boeing

- General Atomics Aeronautical Systems, Inc.

- Lockheed Martin Corporation

- L3Harris Technologies, Inc.

- Northrop Grumman Corporation

- Thales Group

- Kratos Defense & Security Solutions, Inc.

Recent Developments

- November 2025 — Adani Group moved to acquire FSTC, an established pilot training company in India, signaling the conglomerate’s intent to build a vertically integrated aviation training capability. The acquisition reflects rising institutional interest in owning training infrastructure as UAV and manned aviation operations scale across the region.

- June 2024 — Redbird Flight Simulations launched a UAV Mission-Specific Training Module focused on BVLOS (Beyond Visual Line of Sight) operations, designed to help commercial operators meet new FAA regulatory standards. The product directly addressed a compliance gap created by updated FAA rules, converting a regulatory mandate into a structured commercial training opportunity.

- March 2025 — CAE Inc. announced a strategic investment to integrate AI-driven swarm training into its UAV simulation platforms, allowing operators to practice managing multiple autonomous drones simultaneously. This development moves CAE’s simulation offering from single-operator flight training into multi-asset mission management — a capability that defense and large commercial fleet buyers have identified as a critical readiness requirement.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.7 Billion |

| Forecast Revenue (2035) | USD 12.0 Billion |

| CAGR (2026-2035) | 16.1% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (HALE UAV, MALE UAV, SUAV), By Application (Defense & Military, Civil & Commercial, Homeland Security) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | CAE Inc., Textron Inc., ELBIT SYSTEMS LTD., Boeing, General Atomics Aeronautical Systems Inc., Lockheed Martin Corporation, L3Harris Technologies Inc., Northrop Grumman Corporation, Thales Group, Kratos Defense & Security Solutions Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |