Quick Navigation

Report Overview

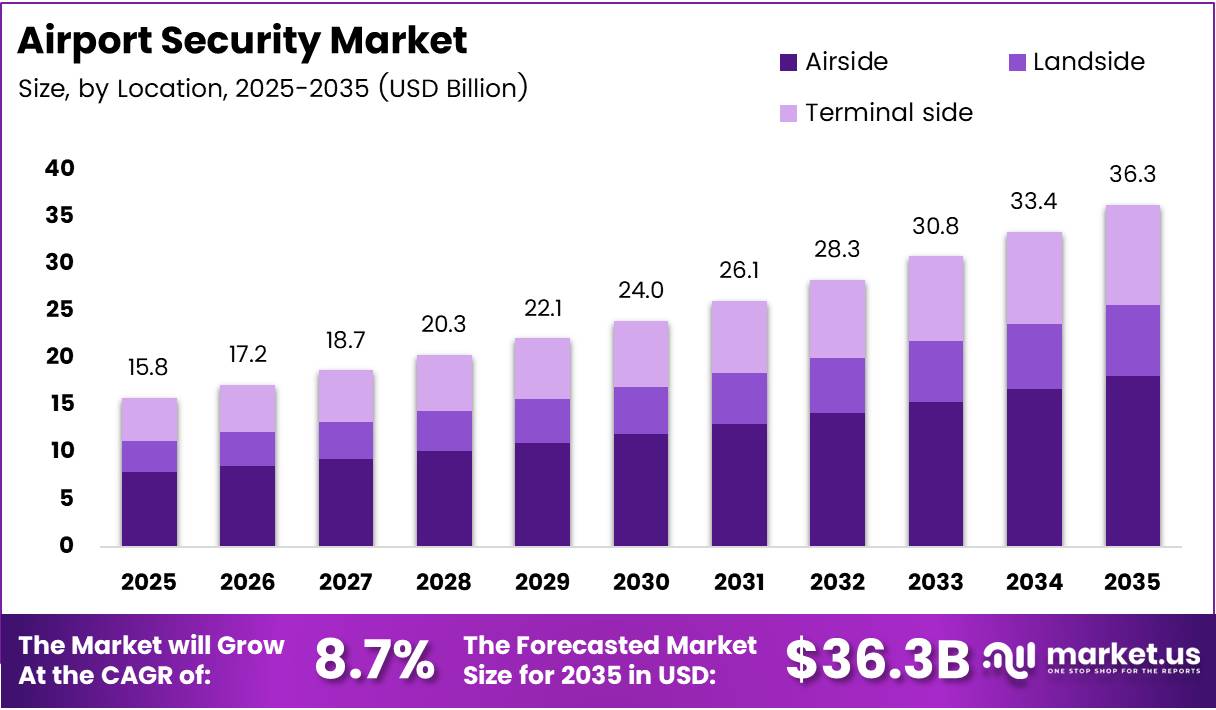

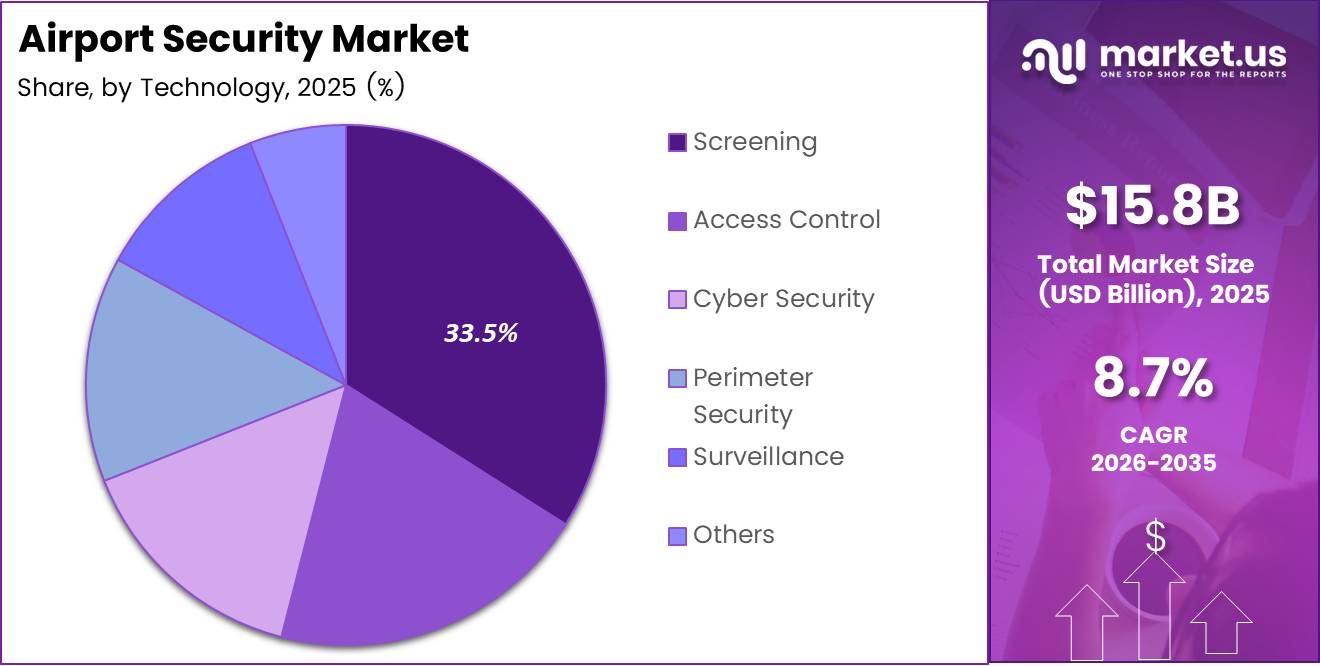

Global Airport Security Market size is expected to be worth around USD 36.3 Billion by 2035 from USD 15.8 Billion in 2025, growing at a CAGR of 8.7% during the forecast period 2026 to 2035.

Airport security encompasses the systems, technologies, and protocols airports deploy to protect passengers, aircraft, and infrastructure from threats. The market spans cabin baggage screening, perimeter intrusion detection, access control, biometric identification, and cybersecurity platforms. Collectively, these systems form the operational backbone of safe air travel worldwide.

Air traffic volumes continue to recover and expand beyond pre-pandemic levels, placing sustained pressure on airports to upgrade their security infrastructure. Each additional flight processed represents a new screening event. Airports that cannot scale their security throughput without adding staff face a structural capacity problem — one that only technology can solve.

Governments across major aviation markets have introduced mandatory screening standards that require airports to deploy certified detection equipment within defined timelines. These regulatory mandates function as a procurement forcing mechanism. Airports cannot defer upgrades when non-compliance carries operational penalties or route suspensions.

The threat environment in aviation has also shifted. Cybersecurity risks now sit alongside physical screening as a top operational priority for airport operators. Airports that treat physical and digital security as separate procurement categories face compounding vulnerability — a gap that integrated platform vendors are specifically engineering to close.

According to a 2025 human-machine performance study published via Taylor & Francis, explosives detection systems for cabin baggage (EDSCB) achieved a hit rate of 75% and an overall correct decision rate of 91%. These figures confirm that current screening technology, when paired with trained operators, delivers operationally reliable performance — and establishes the performance baseline that next-generation CT-based systems must exceed to justify replacement cycles.

According to IATA’s 2025 safety data, 51 accidents occurred across 38.7 million flights, producing an all-accident rate of 1.32 per million flights. For IATA member airlines specifically, that rate drops to 0.72 per million — a gap that illustrates why security and safety investment among certified carriers commands a structural premium and why airports serving those carriers represent the highest-value procurement segment.

Key Takeaways

- The global Airport Security Market is valued at USD 15.8 Billion in 2025 and is forecast to reach USD 36.3 Billion by 2035, at a CAGR of 8.7%.

- By Location, Airside leads with a 47.9% share, reflecting concentrated investment in controlled-access zones directly adjacent to aircraft.

- By System, Cabin Baggage Screening Systems holds the largest share at 34.6%, driven by mandatory regulatory compliance requirements globally.

- By Airport Model, Airport 3.0 dominates with a 48.2% share, representing the current standard for integrated digital-physical security architecture.

- By Airport Class, Class A airports account for 53.7% of market share due to higher passenger volumes and stricter compliance mandates.

- By Technology, Screening holds the largest share at 33.5%, underpinned by government-mandated deployment timelines across international airports.

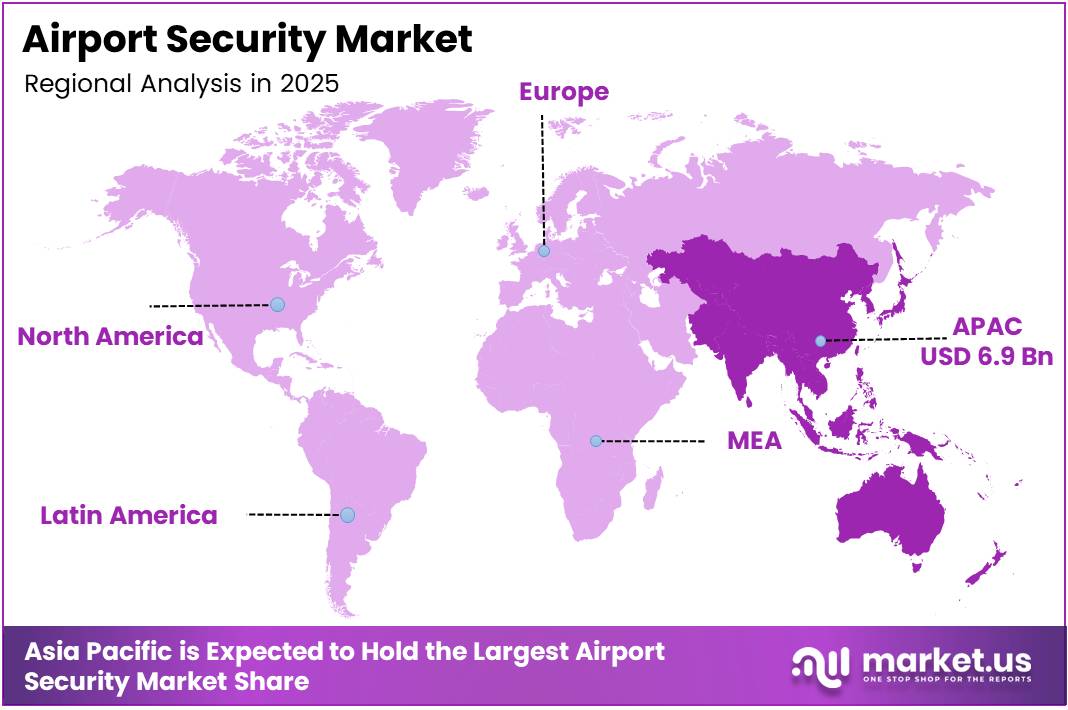

- Asia Pacific is the leading region with a 43.70% share, valued at USD 6.9 Billion, supported by rapid airport expansion across China, India, and Southeast Asia.

Product Analysis

Cabin Baggage Screening Systems dominate with 34.6% due to mandatory regulatory compliance at every passenger checkpoint.

In 2025, Cabin Baggage Screening Systems held a dominant market position in the By System segment of the Airport Security Market, with a 34.6% share. Every commercial airport processing international passengers must operate certified baggage screening at each boarding gate. This non-discretionary requirement makes cabin baggage screening the single largest procurement line item for airport security budgets globally.

Metal Detectors serve as the foundational access layer at nearly every passenger entry point. Their low acquisition cost, high throughput capability, and simple maintenance profile make them the default first-line screening tool. However, the inability to detect non-metallic threats limits their standalone effectiveness, pushing airports toward layered system configurations where metal detectors complement advanced imaging technologies.

Fiber Optic Perimeter Intrusion detection systems address the airside boundary security problem that camera-based solutions cannot reliably solve in low-visibility or adverse weather conditions. Fiber optic cables buried along fence lines deliver real-time vibration alerts without power interruption risk. This positions them as the preferred perimeter technology for Class A airports where a single unauthorized access event carries regulatory and reputational consequences.

Backscatter X-Ray Systems carry a unique position in the market: they deliver high-resolution threat imagery but face active regulatory restrictions in several European markets due to privacy concerns over body imaging. This regulatory asymmetry means vendors must maintain separate product lines for different jurisdictions, increasing supply chain complexity and limiting the addressable market compared to CT-based alternatives.

Others in the system category includes explosive trace detectors, body scanners, and document verification platforms. While individually smaller in revenue contribution, these systems increasingly integrate with primary screening workflows. Their growth reflects airports investing in multi-layer detection rather than relying on a single technology to carry the entire security burden.

Location Analysis

Airside dominates with 47.9% due to direct aircraft proximity and highest-consequence access control requirements.

In 2025, Airside held a dominant market position in the By Location segment of the Airport Security Market, with a 47.9% share. Airside zones sit between the final passenger screening checkpoint and the aircraft itself. Any security failure in this zone carries the most severe consequence — direct threat access to aircraft — which forces airport operators to deploy the highest specification systems at higher unit cost than anywhere else in the terminal.

Landside security covers all public-facing areas before passenger screening, including entrances, check-in halls, and ground transport connections. Landside threats have escalated as soft targets, making video analytics, crowd density monitoring, and explosive trace detection at entry points a budget priority for major hub airports. The challenge is that landside volumes are exponentially higher than airside, making cost-per-screening a critical procurement metric.

Terminal side encompasses the passenger processing zone between landside public access and airside boarding areas. This is where biometric identity verification, automated document checking, and e-gate technologies concentrate. In April 2024, Amadeus acquired Vision-Box for approximately USD 320 million, integrating biometric hardware directly into airport management platforms — a transaction that confirms terminal-side technology as the highest-value integration point in the current airport infrastructure investment cycle.

Airport Model Analysis

Airport 3.0 dominates with 48.2% due to widespread adoption of integrated digital-physical security architecture.

In 2025, Airport 3.0 held a dominant market position in the By Airport Model segment of the Airport Security Market, with a 48.2% share. Airport 3.0 represents the current operational standard — an architecture where digital management systems coordinate physical security hardware across a unified platform. Most major international airports completed or are completing this transition, making Airport 3.0 the reference configuration for security technology procurement today.

Airport 2.0 describes legacy airports still operating with siloed, hardware-dependent security systems that lack central data coordination. These facilities represent a significant retrofit opportunity for technology vendors, as regulatory pressure and rising threat complexity force even lower-budget operators to upgrade. The cost of doing nothing — a compliance failure or security incident — increasingly outweighs the investment required to modernize.

Airport 4.0 describes the next operational frontier, characterized by fully autonomous screening, AI-driven threat prediction, and seamless biometric passenger flow from curb to gate. While early deployments exist in select hub airports, the investment scale and systems integration complexity required means Airport 4.0 adoption will remain concentrated among the largest, best-capitalized operators through the forecast period.

Airport Class Analysis

Class A dominates with 53.7% due to highest passenger volumes and strictest international compliance mandates.

In 2025, Class A airports held a dominant market position in the By Airport Class segment of the Airport Security Market, with a 53.7% share. Class A airports process the largest passenger volumes and serve international routes subject to ICAO and TSA-equivalent standards. The combination of high throughput and non-negotiable compliance timelines creates the largest per-airport security spend, concentrating market revenue at the top of the airport hierarchy.

Class B airports occupy a structurally interesting middle position — large enough to require certified screening across multiple checkpoints, but often without the capital budget of major hubs. This creates a segment where leasing and managed-service models for security equipment are gaining commercial traction. Vendors that can offer outcome-based contracts rather than upfront hardware sales find Class B airports a more accessible entry point than premium Class A procurement cycles.

Class C airports represent the largest number of facilities globally but the smallest share of security market revenue. Their purchasing decisions are highly price-sensitive, favoring standardized, low-maintenance systems over advanced integrated platforms. However, as national aviation authorities extend mandatory screening requirements to smaller facilities, Class C airports are entering a multi-year procurement cycle that will progressively expand the addressable market for entry-tier security system vendors.

Technology Analysis

Screening dominates with 33.5% due to government-mandated deployment at every certified passenger checkpoint.

In 2025, Screening technology held a dominant market position in the By Technology segment of the Airport Security Market, with a 33.5% share. Government-mandated screening requirements at international airports create non-deferrable procurement demand. Every airport that expands capacity or upgrades throughput must install certified screening equipment — making this the most regulation-insulated revenue segment in the entire market.

Access Control technology governs which personnel and vehicles enter restricted airport zones. As airports adopt biometric-based identity verification to replace physical credential systems, access control is transitioning from a passive hardware category into a data-driven platform service. This shift increases recurring software revenue potential for vendors who embed identity management into their access control offerings.

Cyber Security now represents a distinct procurement category within airport security budgets. Airport operational technology — from baggage handling to runway lighting — connects to networked systems that carry real attack surface exposure. Airports that treat cyber security as an IT department cost rather than an operational security investment face the same vulnerability gap that physical perimeter neglect created a decade ago.

Perimeter Security addresses the physical boundary between public land and restricted airfield areas. Advanced radar, thermal imaging, and fiber optic intrusion detection are displacing camera-only perimeter solutions as airports recognize that visual monitoring alone cannot reliably detect low-visibility incursions at scale across extended fence lines.

Surveillance infrastructure has evolved from passive CCTV recording to active AI-assisted behavior analytics. Modern surveillance platforms flag anomalous crowd behavior, unattended objects, and unauthorized zone access in real time. This functional shift from documentation to prevention changes the business case — airports now justify surveillance investment on incident prevention, not retrospective investigation.

Others in the technology category includes communication systems, emergency response platforms, and integrated operations center software. These components tie together the physical and digital security layers. Their procurement is typically bundled into major terminal construction or refurbishment contracts, making them a reliable revenue indicator for vendors tracking large-scale airport capital expenditure programs.

Key Market Segments

By Location

- Airside

- Landside

- Terminal side

By System

- Cabin Baggage Screening Systems

- Metal Detectors

- Fiber Optic Perimeter Intrusion

- Backscatter X-Ray Systems

- Others

By Airport Model

- Airport 2.0

- Airport 3.0

- Airport 4.0

By Airport Class

- Class A

- Class B

- Class C

By Technology

- Screening

- Access Control

- Cyber Security

- Perimeter Security

- Surveillance

- Others

Drivers

Rising Air Traffic Volumes and Mandatory Screening Regulations Force Continuous Airport Security Upgrades

Global air traffic growth directly multiplies the number of passengers, bags, and vehicles that airports must screen per day. Each new route or terminal expansion triggers a corresponding requirement to scale certified screening capacity. Airports that cannot increase throughput without proportional staffing increases face an operational bottleneck that drives technology investment on a structural basis.

Government regulators in aviation — including ICAO member states, the TSA, and equivalent European authorities — have consistently tightened minimum standards for baggage screening, perimeter protection, and access control. These mandates convert what might otherwise be discretionary capital expenditure into a compliance obligation. Non-compliant airports risk route suspensions, which for commercial operators is a direct revenue threat.

The threat environment further amplifies regulatory urgency. Terrorism and cybersecurity risks in aviation have pushed governments to act faster on screening technology certification cycles. In August 2025, Menzies Aviation completed a USD 305 million acquisition of G2 Secure Staff, doubling its security and ground service footprint across 110 U.S. locations — a transaction that reflects how large operators are using consolidation to scale certified security capacity ahead of anticipated volume growth. According to a 2025 study, CT-based EDSCB systems achieve hit rates of 80% or more with false alarm rates at or below 5%, establishing a clear performance benchmark that is accelerating the replacement of older detection equipment at regulated checkpoints.

Restraints

High System Deployment Costs and Biometric Privacy Concerns Slow Security Upgrade Decisions at Mid-Tier Airports

Advanced airport security systems carry substantial upfront capital costs. CT-based baggage scanners, integrated biometric access platforms, and AI-driven surveillance infrastructure require significant per-unit investment, plus installation, integration, and staff retraining. For Class B and Class C airports operating on constrained capital budgets, the cost of full compliance-grade upgrades can exceed available annual infrastructure spend.

Maintenance costs compound the deployment barrier. Security systems require regular certification testing, software updates, and hardware servicing to remain compliant. Airports that stretch procurement cycles to manage costs often operate with aging systems that carry higher failure risk — creating a paradox where budget constraints simultaneously delay investment and increase operational exposure.

Biometric surveillance technologies introduce a separate category of resistance: regulatory and public privacy concerns. Several European jurisdictions have imposed restrictions on facial recognition in public spaces, directly limiting the commercial deployment window for biometric security platforms in some of the world’s highest-traffic aviation markets. Vendors targeting these markets must navigate legal compliance complexity that increases product development cost and slows sales cycles — a structural friction that does not apply in less regulated markets and therefore creates uneven global adoption rates.

Growth Factors

AI-Driven Threat Detection, Smart Airport Expansion, and Contactless Processing Create New Revenue Layers for Security Vendors

Artificial intelligence integration into threat detection changes the economics of airport screening. AI-assisted systems process imaging data faster than human review, flag anomalies with greater consistency, and reduce false alarm rates — the persistent operational cost of legacy screening. According to a 2025 human-machine performance study, when 115 professional screeners worked with EDSCB systems, their combined hit rate ran at least 15 percentage points above the system’s 7% false alarm rate. This human-machine performance gap confirms that AI-augmented workflows outperform either humans or machines operating independently — directly justifying the investment case for next-generation integrated platforms.

Smart airport construction across Asia, the Middle East, and Africa represents a greenfield opportunity for security vendors. New terminals built from the ground up can embed integrated security architecture from the design stage, eliminating the retrofit complexity and legacy system constraints that limit upgrades at existing facilities. In August 2025, Smiths Detection acquired Med Graphix Inc. to extend the lifecycle of critical X-ray and screening components through advanced refurbishment — positioning the company to serve both new installations and the large installed base of aging equipment at mid-tier airports globally.

Contactless and automated security systems address a passenger experience priority that airport operators now treat as a commercial differentiator. Faster throughput, reduced physical contact, and seamless biometric boarding reduce queue times and increase gate-area dwell time — a metric directly linked to retail revenue. Airports that frame security investment as a revenue enabler rather than a compliance cost unlock a second business case that strengthens the justification for premium system procurement.

Emerging Trends

Touchless Screening, Facial Recognition Deployment, and Cybersecurity Investment Define the Next Phase of Airport Security Infrastructure

Post-pandemic operational priorities permanently elevated contactless passenger processing from a convenience feature to an infrastructure standard. Airports that invested in automated screening lanes and touchless e-gate systems during the recovery period now hold a throughput and health-compliance advantage over facilities that deferred those upgrades. This first-mover separation is widening as passenger volumes recover, reinforcing the case for continued investment.

Facial recognition deployment is accelerating across major hub airports globally, with implementations spanning check-in, lounge access, boarding, and security clearance. The technology reduces identity verification time per passenger and eliminates the document-handling friction points that create queue bottlenecks. According to IATA’s 2025 data, the Asia-Pacific all-accident rate improved to 0.91 accidents per million sectors, down from 1.08 in 2024 — a safety trajectory that reinforces the region’s investment commitment to aviation infrastructure, including security technology, as a sustained operational priority.

Aviation cybersecurity investment is transitioning from reactive patching to proactive threat architecture. Airports managing networked operational technology — air traffic systems, baggage automation, passenger data platforms — now treat cyber security as a physical operations risk, not an IT budget line. Vendors that can deliver unified physical-and-digital security management under a single platform contract are positioned to capture the largest share of this converging procurement category.

Regional Analysis

Asia Pacific Dominates the Airport Security Market with a Market Share of 43.70%, Valued at USD 6.9 Billion

Asia Pacific holds 43.70% of the global airport security market, valued at USD 6.9 Billion. The region’s dominance reflects simultaneous drivers: China, India, and Southeast Asian nations are all executing large-scale airport construction programs while expanding existing hub capacity. Greenfield terminals built to current standards embed advanced security architecture from design, generating procurement volume that mature markets cannot replicate through retrofit cycles alone.

North America Airport Security Market Trends

North America operates the world’s most advanced airport security regulatory framework, with TSA mandates creating a baseline of certified screening equipment across all commercial airports. This regulatory depth sustains consistent replacement-cycle procurement even without new construction. The market’s maturity means growth comes from technology upgrades — AI integration, biometric adoption, and cybersecurity expansion — rather than new system deployment.

Europe Airport Security Market Trends

Europe holds a significant market share supported by EASA compliance requirements and high international passenger volumes at hub airports. However, the region faces a structural constraint: GDPR and national privacy laws restrict biometric deployment in public-facing security applications across several member states. This regulatory friction slows the adoption of facial recognition and biometric access platforms that are advancing faster in less regulated markets.

Middle East and Africa Airport Security Market Trends

The Middle East is executing the world’s most ambitious airport infrastructure programs, with Gulf Cooperation Council nations investing heavily in new terminal capacity designed to serve long-haul hub transfer volumes. These greenfield projects specify integrated security platforms at the design stage, making the region a high-value market for turnkey security system providers. Africa represents an earlier-stage growth opportunity tied to aviation network expansion and regulatory maturation.

Latin America Airport Security Market Trends

Latin America’s airport security market reflects uneven development across the region. Brazil and Mexico operate major international hubs subject to ICAO compliance requirements, sustaining demand for certified screening and perimeter security systems. Smaller regional airports across the continent present a retrofit opportunity as national aviation authorities progressively extend mandatory security standards to facilities that previously operated below international certification thresholds.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

SITA occupies a structurally unique position in airport security because it operates at the intersection of air transport IT and physical security infrastructure. Its access to airline and airport operational data gives it an integration advantage that pure-play security hardware vendors cannot replicate. In a market where the convergence of cyber and physical security is the defining procurement trend, that data position represents a durable competitive asset.

Bosch Sicherheitssysteme GmbH brings a building security and industrial systems background that translates directly into large-scale airport perimeter and surveillance contracts. Its established relationships with construction and facilities management contractors give it early-stage access to new terminal projects — a procurement entry point that competitors who sell only to security departments frequently miss. This positions Bosch as a recurring beneficiary of greenfield airport investment programs globally.

Thales operates across defense, aerospace, and digital security — a combination that makes it one of the few vendors capable of bidding on integrated physical-digital security contracts that span screening, access control, and cybersecurity within a single procurement vehicle. Its defense-grade technology certifications allow it to meet the highest-specification national security requirements at major international hub airports, creating a contract retention barrier that commercially focused competitors struggle to match.

Honeywell International Inc. leverages its building automation and industrial IoT platform to deliver airport security as a managed service rather than a discrete hardware sale. This outcome-based commercial model appeals to airport operators facing capital budget constraints — it converts large upfront system costs into predictable operating expenditure. Honeywell’s ability to bundle security with broader facility management contracts gives it a cross-selling advantage in accounts where procurement decisions sit above the security department level.

Key Players

- SITA

- Bosch Sicherheitssysteme GmbH

- Thales

- Honeywell International Inc.

- Leidos

- Siemens

- Amadeus IT Group SA

- IBM

- Elbit Systems Ltd.

- Genetec Inc.

Recent Developments

- August 2025 – Smiths Detection announced the acquisition of Med Graphix Inc. (MGI) to strengthen its sustainable service capabilities, focusing specifically on the refurbishment and lifecycle extension of critical X-ray and screening components. This move extends Smiths Detection’s revenue model beyond hardware sales into recurring service contracts tied to the large installed base of existing screening equipment globally.

- August 2025 – Menzies Aviation completed a USD 305 million acquisition of G2 Secure Staff, doubling its security and ground handling footprint across 110 locations in the United States. The transaction signals how large airport services operators are consolidating certified security capacity to meet rising volume demand ahead of anticipated passenger traffic growth through the remainder of the decade.

- April 2024 – Amadeus acquired Vision-Box for approximately USD 320 million, integrating biometric hardware and security software into its airport management portfolio. The acquisition repositions Amadeus from a travel technology provider into a full-stack airport security and operations platform vendor, with biometric passenger processing as the core integration differentiator.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 15.8 Billion |

| Forecast Revenue (2035) | USD 36.3 Billion |

| CAGR (2026-2035) | 8.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Location (Airside, Landside, Terminal side), By System (Cabin Baggage Screening Systems, Metal Detectors, Fiber Optic Perimeter Intrusion, Backscatter X-Ray Systems, Others), By Airport Model (Airport 2.0, Airport 3.0, Airport 4.0), By Airport Class (Class A, Class B, Class C), By Technology (Screening, Access Control, Cyber Security, Perimeter Security, Surveillance, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | SITA, Bosch Sicherheitssysteme GmbH, Thales, Honeywell International Inc., Leidos, Siemens, Amadeus IT Group SA, IBM, Elbit Systems Ltd., Genetec Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |