Quick Navigation

- Report Overview

- Key Takeaways

- By Type Analysis

- By Materials Analysis

- By Thickness Range Analysis

- By Installation Method Analysis

- By Application Analysis

- By End User Analysis

- Key Market Segments

- Driving factors

- Restraining Factors

- Growth Opportunity

- Trending Factors

- Regional Analysis

- Key Players Analysis

- Recent Development

- Report Scope

Report Overview

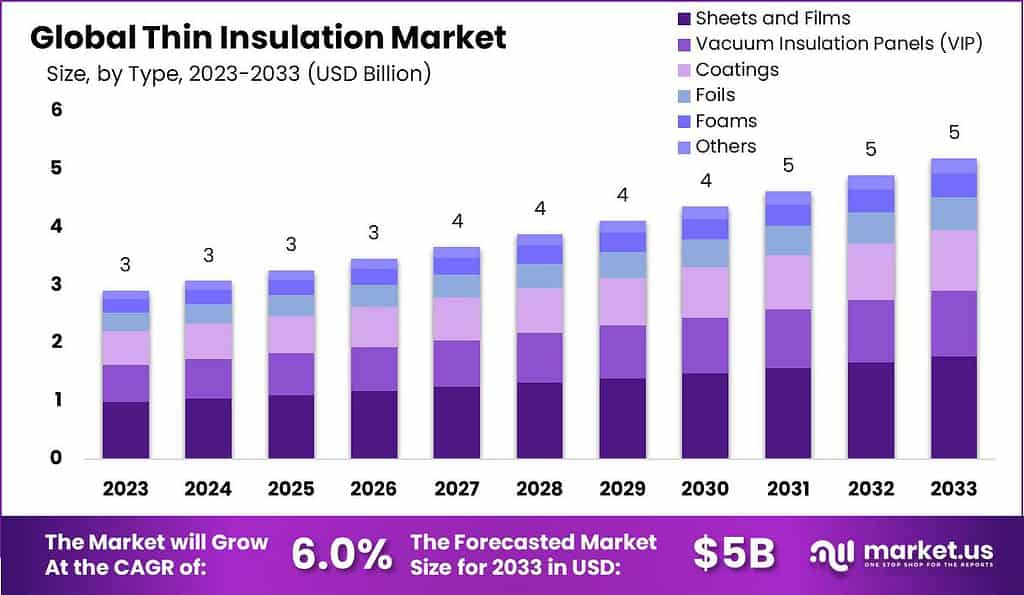

The Global Thin Insulation Market size is expected to be worth around USD 5.0 Billion by 2033, from USD 2.9 Billion in 2023, growing at a CAGR of 6.0% during the forecast period from 2024 to 2033.

The Thin Insulation Market refers to a segment of the industry that deals with the production, distribution, and use of insulation materials that are especially thin in comparison to traditional insulation products. This market is significant because thin insulation materials are designed to provide effective thermal resistance and energy efficiency even in spaces where thicker insulation cannot be used due to space constraints.

The market demand for thin insulation is on the rise, driven by the growing need for efficient energy use and space optimization in various sectors such as construction, automotive, and electronics. As buildings and vehicles are designed to be more energy-efficient, the need for effective insulation that doesn’t take up much space has increased. This has made thin insulation materials highly sought after.

Thin insulation materials are extensively utilized across various sectors due to their effective thermal properties and minimal spatial requirements. Notably, the construction industry, which accounted for approximately 45% of the global thin insulation market in 2022, benefits significantly from these materials for enhancing energy efficiency in buildings. Automotive manufacturing also integrates thin insulation for thermal management and noise reduction, comprising about 20% of the market share.

Governmental regulations play a pivotal role in shaping the thin insulation market. In the European Union, the Energy Performance of Buildings Directive (EPBD) mandates nearly zero-energy buildings by 2020 for new constructions, directly influencing the demand for efficient insulation solutions. Similarly, the U.S. Department of Energy has established stringent insulation standards, particularly for federal buildings, which must meet specific energy conservation criteria.

Trade dynamics for thin insulation materials reveal a significant flow from manufacturing powerhouses like Germany and China to high-demand regions such as North America and Western Europe. In 2022, China exported thin insulation materials valued at approximately $200 million to North America, highlighting the critical supply chain dynamics.

The global market for thin insulation is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% from 2021 to 2026, spurred by increasing adoption in residential and commercial buildings. The market’s valuation was estimated at $7.3 billion in 2021, with expectations to reach $9.1 billion by 2026.

Significant investments from both government and private sectors are bolstering the thin insulation industry. For instance, the U.S. government’s recent allocation of $500 million under the Infrastructure Investment and Jobs Act for green building initiatives includes provisions for advanced insulation materials. On the private front, major corporations like 3M and BASF have committed a combined total of over $300 million towards enhancing insulation technologies and production capacities.

The thin insulation sector is characterized by frequent innovations and strategic corporate actions. A noteworthy example includes a partnership between DuPont and Honeywell, launched in 2023, which focuses on developing next-generation thermal insulation solutions for the automotive and aerospace industries. Moreover, mergers and acquisitions are also prevalent, with Kingspan acquiring a smaller insulation player in 2022 for $100 million to consolidate its market position and expand its product portfolio.

Key Takeaways

- The Global Thin Insulation Market size is expected to be worth around USD 5.0 Billion by 2033, from USD 2.9 Billion in 2023, growing at a CAGR of 6.0% during the forecast period from 2024 to 2033.

- Sheets and Films led the Thin Insulation Market by type with a 34.4% share, driving industry innovations and diverse applications.

- Aerogels led the Thin Insulation Market Materials segment with a 28.7% share, showcasing diverse high-performance applications.

- The “Less Than 1 Inch” category dominated the Thin Insulation Market’s thickness range, holding a 27.7% share, vital for space-constrained applications.

- Spray Insulation led the Thin Insulation Market’s Installation Method segment with a 34.5% share, excelling in versatility and energy efficiency.

- Building Thermal Insulation led the Thin Insulation Market’s Application segment with a 37.5% share, essential for energy-efficient construction.

- Building and Construction led the Thin Insulation Market’s End User segment with a 35.6% share, pivotal for energy-efficient construction.

- Asia Pacific dominates the global thin insulation market with a 38.5% share at $1.1 billion.

By Type Analysis

Sheets and Films led the Thin Insulation Market by type with a 34.4% share, driving industry innovations and diverse applications.

In 2023, The Thin Insulation Market saw varied contributions from its different material segments. Sheets and Films held a dominant market position in the By Type segment, capturing more than a 34.4% share. This segment benefits from its broad application in building thermal insulation, where thin, flexible materials are essential for space-constrained installations. Vacuum Insulation Panels (VIP) followed, noted for their exceptional thermal resistance with a very thin profile, making them ideal for high-performance energy-efficient buildings and refrigeration systems.

Coatings and Foils also marked significant contributions. Coatings are increasingly favored for their ease of application and effectiveness in unusual or irregular spaces, enhancing energy efficiency without significant alterations. Foils, often used in conjunction with other insulation types, reflect heat and act as a barrier against heat transfer, which is particularly valuable in hot climates.

Foams, a versatile category within the Thin Insulation Market, accounted for substantial market uptake due to their adaptability and effectiveness in a variety of applications, from residential and commercial buildings to industrial installations.

By Materials Analysis

Aerogels led the Thin Insulation Market Materials segment with a 28.7% share, showcasing diverse high-performance applications.

In 2023, Aerogels held a dominant market position in the By Materials segment of the Thin Insulation Market, capturing more than a 28.7% share. This segment’s leadership is attributed to aerogels’ exceptional thermal resistance and lightweight, making them ideal for high-performance insulation applications across aerospace, automotive, and construction industries. Silica Aerogels, a subset of aerogels, also contributed significantly due to their superior insulative properties and increasing affordability, which broadens their application scope.

Metals, used primarily for reflective insulation in the form of foils, are essential in managing heat transfer, especially in hot climates and industrial settings. Plastic Foams, which include materials like expanded and extruded polystyrene, are prevalent due to their ease of installation, cost-effectiveness, and versatility, making them a popular choice in both residential and commercial construction.

Fiberglass, known for its sound absorption and thermal insulation capabilities, continues to be a staple in the market due to its durability and performance in a variety of climatic conditions.

By Thickness Range Analysis

The “Less Than 1 Inch” category dominated the Thin Insulation Market’s thickness range, holding a 27.7% share, vital for space-constrained applications.

In 2023, The “Less Than 1 Inch” segment held a dominant market position in the By Thickness Range segment of the Thin Insulation Market, capturing more than a 27.7% share. This segment’s leading status is underpinned by its widespread application in settings where space is at a premium, such as in urban residential and commercial buildings, and where streamlined solutions are paramount.

Following closely, the “1 Inch to 2 Inches” range is favored for its balanced insulation capabilities, suitable for a broad array of general construction applications, ensuring adequate thermal resistance without considerable space intrusion. The “2 Inches to 4 Inches” segment caters primarily to industrial and some commercial settings, where higher performance insulation is necessary to comply with stringent energy codes and handle extreme temperatures.

Lastly, the “More Than 4 Inches” thickness range is utilized in specialized applications that require maximum insulation properties, such as in cold storage and some industrial facilities. This segment, while smaller in market share, is critical for applications demanding the highest levels of thermal management.

By Installation Method Analysis

Spray Insulation led the Thin Insulation Market’s Installation Method segment with a 34.5% share, excelling in versatility and energy efficiency.

In 2023, Spray Insulation held a dominant market position in the By Installation Method segment of the Thin Insulation Market, capturing more than a 34.5% share. This method’s popularity stems from its versatility and effectiveness in providing seamless thermal barriers, making it ideal for both residential and commercial settings. Spray insulation’s ability to conform to any shape and fill gaps and cracks results in superior thermal performance and air sealing, which are critical in energy efficiency efforts.

Following spray insulation, Board Insulation is also a significant segment, valued for its rigidity and ease of installation. It is commonly used in both new construction and retrofit projects, providing excellent thermal resistance and structural integrity.

Batts and Rolls are preferred for their cost-effectiveness and simplicity in installation, making them a popular choice for DIY projects and traditional construction, especially in residential applications.

Lastly, Blown-In Insulation is crucial for retrofitting existing structures where it is impractical to remove interior finishes. This method is highly effective at increasing energy efficiency in older buildings by filling in hard-to-reach spaces and cavities.

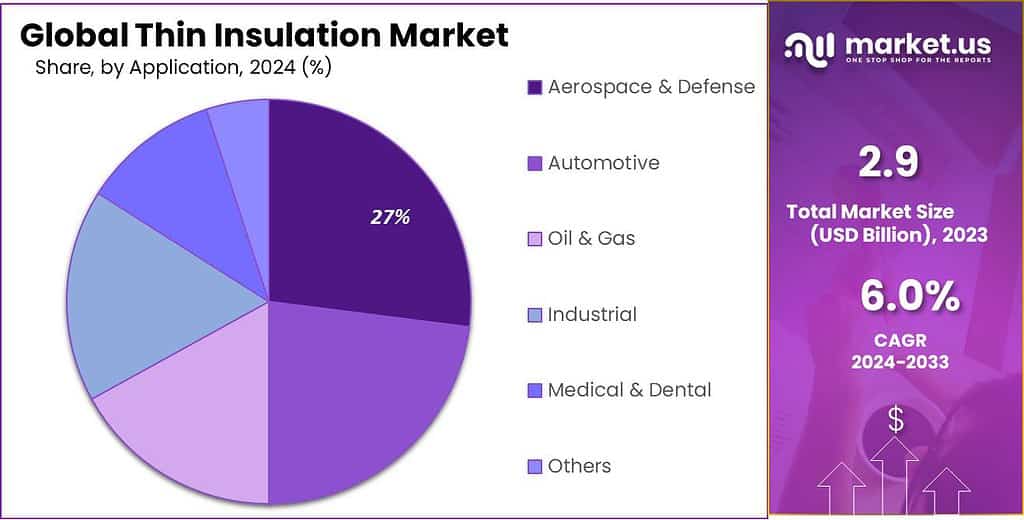

By Application Analysis

Building Thermal Insulation led the Thin Insulation Market’s Application segment with a 37.5% share, essential for energy-efficient construction.

In 2023, Building Thermal Insulation held a dominant market position in the By Application segment of the Thin Insulation Market, capturing more than a 37.5% share. This segment’s prominence is primarily due to the increasing global focus on energy efficiency within the residential and commercial sectors. Building thermal insulation is essential for reducing energy consumption, enhancing indoor environmental quality, and meeting stringent building regulations that mandate improved thermal performances in structures.

Following Building Thermal Insulation, Thermal Packaging is another significant category. This segment utilizes thin insulation materials to maintain temperature-sensitive goods during transport, which is crucial in industries like pharmaceuticals and food and beverage. The demand for effective thermal packaging solutions is driven by the growth of online grocery sales and the global expansion of cold chain logistics.

Wires and Cables, as well as Pipe Coatings, also form important parts of the thin insulation market. Insulation in wires and cables is critical for safety, efficiency, and functionality in various applications ranging from residential wiring to complex industrial machinery. Pipe Coatings are extensively used in industries such as oil and gas and manufacturing to prevent heat loss and protect against corrosion.

By End User Analysis

Building and Construction led the Thin Insulation Market’s End User segment with a 35.6% share, pivotal for energy-efficient construction.

In 2023, Building and Construction held a dominant market position in the end-user segment of the Thin Insulation Market, capturing more than a 35.6% share. This sector’s dominance underscores its critical role in integrating energy-efficient solutions to meet global sustainability targets and regulatory standards. As urbanization continues to increase, so does the need for effective insulation to reduce energy consumption and enhance building safety and comfort.

The Automotive sector also represents a significant portion of the market. Here, thin insulation is crucial for improving energy efficiency and reducing noise, which enhances the overall vehicle performance and passenger comfort. In Aerospace, thin insulation materials are valued for their ability to provide thermal management and reduce the overall weight of the aircraft, which is essential for fuel efficiency and safety.

The Oil and Gas industry utilizes thin insulation solutions to protect equipment from extreme temperatures and corrosion, thereby ensuring operational efficiency and safety.

Key Market Segments

By Type

- Sheets and Films

- Vacuum Insulation Panels (VIP)

- Coatings

- Foils

- Foams

- Others

By Materials

- Aerogels

- Silica Aerogels

- Metals

- Plastic Foams

- Fiberglass

- Others

By Thickness Range

- Less Than 1 Inch

- 1 Inch to 2 Inches

- 2 Inches to 4 Inches

- More Than 4 Inches

By Installation Method

- Spray Insulation

- Board Insulation

- Batts and Rolls

- Blown-In Insulation

By Application

- Building Thermal Insulation

- Thermal Packaging

- Wires and Cables

- Pipe Coatings

- Others

By End User

- Automotive

- Aerospace

- Building and Construction

- Oil and Gas

- Others

Driving factors

Regulatory Compliance and Energy Efficiency Standards

The thin insulation market is significantly driven by regulatory compliance and stringent energy efficiency standards. Governments and international bodies have introduced regulations that mandate improved insulation for energy conservation and reduced environmental impact. These standards are instrumental in promoting the use of advanced insulation materials to achieve greater energy efficiency in buildings and industrial applications.

For instance, the European Union’s directives on energy efficiency stipulate specific requirements for building insulation, propelling the demand for high-performance thin insulation solutions. This regulatory framework not only encourages the adoption of sustainable building practices but also increases the market penetration of innovative insulation technologies, supporting growth in diverse climates and construction standards.

Growth in Construction Activities

The expansion of construction activities globally acts as a catalyst for the growth of the thin insulation market. With urbanization and economic growth, especially in emerging economies, there is a heightened demand for residential and commercial buildings. This demand directly influences the need for effective insulation to enhance energy efficiency and comfort.

In regions experiencing significant construction growth, such as Asia-Pacific and the Middle East, the surge in building projects correlates with increased adoption of thin insulation materials. These materials are favored for their ability to provide superior insulation without compromising on space, aligning with the modern trends of maximizing usable area in construction.

Advancements in Material Technology

Advancements in material technology have revolutionized the thin insulation market by enabling the development of materials that offer superior insulative properties with minimal thickness. Innovations such as aerogels, vacuum insulation panels, and thin multifoil products have transformed the market landscape. These materials cater to the increasing demand for thin insulation solutions that do not compromise performance while being space-efficient.

The technological strides in material science not only enhance the functional attributes of insulation products but also extend their applicability across harsh and varied environmental conditions. This technological progression facilitates the integration of thin insulation in a broader array of applications, thereby broadening the market’s scope and potential for growth.

Restraining Factors

Technical Challenges in Installation

The thin insulation market faces notable growth constraints due to technical challenges associated with the installation of these advanced materials. Thin insulation products, while beneficial for their space-saving attributes, often require specialized knowledge and handling for effective installation. This complexity can deter adoption, particularly in regions where skilled labor is scarce or where traditional construction methods are preferred.

The necessity for precision in installation to achieve desired energy efficiency standards can increase the overall cost of construction projects, making thin insulation a less attractive option for budget-conscious builders and developers. Consequently, the market’s expansion is somewhat impeded by the higher initial cost and technical demands of these innovative insulation solutions.

Competition from Traditional Insulation

Competition from traditional insulation materials significantly restrains the growth of the thin insulation market. Materials such as fiberglass and mineral wool have long been established in the construction industry due to their cost-effectiveness, widespread availability, and familiar installation techniques.

Despite the superior performance of newer thin insulation materials in terms of space efficiency and thermal resistance, the entrenched market position and lower cost of traditional insulation continue to pose strong competition. This ongoing competition affects market penetration rates for thin insulation products, especially in markets that are sensitive to upfront material costs and are less regulated regarding energy efficiency.

Recycling and Disposal Issues

Recycling and disposal present significant challenges for the thin insulation market. Many advanced insulation materials, particularly those incorporating synthetic or composite materials, are difficult to recycle. This lack of eco-friendly disposal options can be a critical downside in a market that is increasingly driven by sustainability considerations.

Environmental regulations and consumer preference for sustainable building materials can thus restrain the adoption of certain thin insulation products, particularly in regions with stringent environmental protection standards. The market must navigate these issues carefully to maintain its growth trajectory, particularly as global emphasis on sustainability intensifies.

Growth Opportunity

Innovative Product Offerings

The global thin insulation market is poised for significant growth, driven by innovative product offerings. Manufacturers are increasingly focusing on developing advanced materials that offer superior thermal resistance with minimal thickness, catering to the modern demand for efficient, space-saving solutions.

These innovations are expected to capture new segments within both residential and commercial construction, particularly in markets emphasizing energy conservation and high-performance building envelopes.

Enhanced R&D Investments

Enhanced research and development (R&D) investments are key to unlocking new opportunities in the thin insulation market. Companies are channeling more resources into developing materials that are not only thinner and more effective but also easier to install and more environmentally friendly.

This surge in R&D is likely to result in breakthroughs that could resolve existing limitations related to recyclability and adaptability across diverse climatic conditions. As these new products enter the market, they are anticipated to drive growth by meeting stricter regulatory standards and evolving consumer expectations.

Integration with Renewable Energy Projects

Another significant growth opportunity lies in the integration of thin insulation materials with renewable energy projects. As the global push towards sustainability intensifies, there is increasing interest in ensuring that buildings are as energy-efficient as possible.

Thin insulation products are ideal for use in buildings equipped with solar panels, wind energy systems, and other renewable technologies due to their excellent insulative properties and minimal spatial footprint. This integration not only enhances the overall energy efficiency of such projects but also positions thin insulation as a critical component in the future of green building practices.

Trending Factors

Increased Focus on Indoor Environmental Quality

The thin insulation market is witnessing a heightened focus on improving indoor environmental quality (IEQ). As health and well-being continue to drive consumer and regulatory priorities, there is an increasing demand for insulation solutions that contribute positively to the indoor environment by enhancing thermal comfort and minimizing air leaks.

Thin insulation materials are crucial in achieving these goals without compromising space, particularly in urban settings where space efficiency is paramount. This trend is prompting manufacturers to innovate in ways that both insulate and contribute to healthier indoor air quality, making IEQ a central aspect of product development and marketing strategies.

Eco-friendly Materials

The shift towards eco-friendly materials is reshaping the thin insulation market significantly. With a global push towards sustainability, manufacturers are developing products that are both highly efficient and have a reduced environmental impact. This includes recyclable materials, made from renewable resources, or have lower levels of volatile organic compounds (VOCs).

The market is responding positively to these innovations, as green building certifications and consumer preferences increasingly favor materials that support environmental stewardship while delivering performance.

Data-driven Insulation Solutions

Advancements in technology have led to the emergence of data-driven insulation solutions within the thin insulation market. These solutions utilize sensors and IoT technology to optimize energy efficiency based on real-time environmental data.

The integration of these technologies enables buildings to adapt their insulation needs dynamically, maximizing energy savings and enhancing occupant comfort. This trend is set to expand as more buildings become ‘smart’, and as data integration becomes a standard feature of modern insulation products.

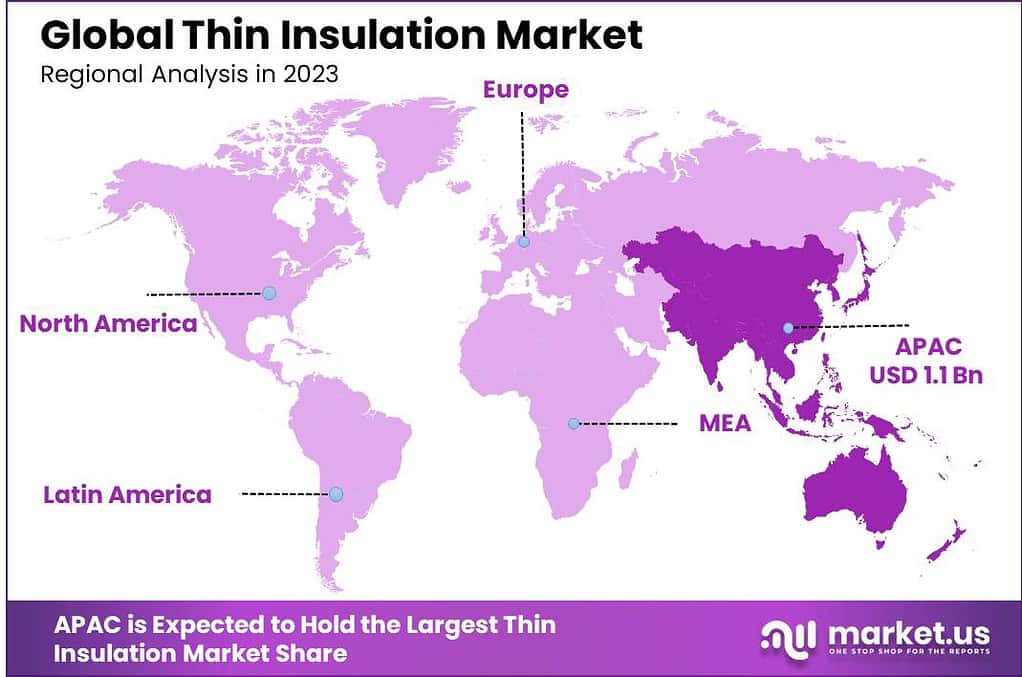

Regional Analysis

Asia Pacific dominates the global thin insulation market with a 38.5% share at $1.1 billion.

Asia Pacific (APAC) is the dominant region in the thin insulation market, accounting for 38.5% of the market share with revenues reaching $1.1 billion. This region’s robust growth is fueled by rapid urbanization, extensive construction activities, and increasing regulatory mandates for energy efficiency in countries like China, Japan, and India. APAC’s leadership in the market is further reinforced by significant investments in infrastructure and a strong inclination towards adopting innovative construction solutions.

North America follows, with a significant emphasis on upgrading aging building infrastructure and stringent regulations for energy efficiency, particularly in the U.S. and Canada. The region’s market is driven by the adoption of advanced materials in residential and commercial buildings to meet stricter codes for energy conservation and environmental impact.

Europe also presents a substantial market for thin insulation, driven by the EU’s aggressive targets for reducing energy consumption and greenhouse gas emissions. Northern European countries, with their colder climates, particularly emphasize high-performance insulation solutions to enhance heating efficiency and sustainability in building designs.

Middle East & Africa (MEA) and Latin America are emerging as potential growth areas for thin insulation. In MEA, the growth is propelled by the construction boom in Gulf Cooperation Council (GCC) countries, coupled with rising awareness about the benefits of energy-efficient buildings. Latin America shows promise with gradual shifts towards more energy-efficient building practices, influenced by increasing environmental awareness and economic development across the region.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

The global thin insulation market is significantly shaped by the activities and innovations of leading companies. Among them, 3M, BASF SE, Kingspan Group, and Saint-Gobain stand out for their strategic initiatives and expansive market reach.

3M is a pivotal player in the thin insulation market, known for its commitment to innovation and sustainability. The company’s ability to integrate advanced technologies into its insulation products allows it to meet diverse industry demands effectively. 3M will continue to leverage its strong R&D capabilities to enhance product performance and environmental sustainability, aligning with global trends toward energy-efficient building solutions.

BASF SE is another influential force, driving the market through its extensive portfolio of high-performance insulation materials. BASF’s focus on eco-friendly solutions and energy efficiency caters well to the regulatory demands across various regions. Its investments in technology to develop superior thin insulation materials that offer better thermal resistance and durability underscore its leadership in the sector.

Kingspan Group excels in the market with its innovative approach to building envelope solutions, including advanced thin insulation systems. Kingspan’s commitment to sustainable building practices and its global operational footprint make it a key contributor to the market’s expansion. The company’s focus on meeting the stringent fire safety and energy efficiency standards in Europe and North America positions it as a leader in high-performance insulation.

Saint-Gobain, with its broad range of insulation products, focuses on enhancing indoor environmental quality and energy efficiency. The company’s strategic acquisitions and focus on R&D have enabled it to offer cutting-edge, thin insulation solutions that are both effective and environmentally responsible. Saint-Gobain’s dedication to innovation and sustainability helps it maintain a strong market position and meet the evolving demands of the construction industry worldwide.

These key players not only drive competitive dynamics but also significantly influence the technological and regulatory landscape of the thin insulation market. Their efforts in innovation and sustainability are crucial in shaping the strategies and growth trajectories in this sector.

Market Key Players

- 3M

- Actis Insulation Ltd.

- Armacell International S.A.

- BASF SE

- BNZ Materials, Inc.

- Cabot Corporation.

- Celotax Saint Gobain

- ContiTech AG

- Dow Chemical Company

- Huntsman International LLC

- Johns Manville

- A Berkshire Hathaway Company

- Kingspan Group

- Owens Corning

- Rockwool Group

- Saint-Gobain

- UNILIN Insulation

- Xtratherm

Recent Development

- In July 2023, Kingspan Group announced plans to acquire the majority of shares in Steico SE, a major wood fiber insulation manufacturer. This acquisition is expected to be completed in early 2024, subject to regulatory approvals, and underscores Kingspan’s strategy to enhance its product portfolio and market reach in sustainable building materials.

- In February 2023, Saint-Gobain acquired U.P. Twiga Fiberglass Ltd., the leading manufacturer of glass wool insulation in India. This acquisition is part of Saint-Gobain’s strategy to strengthen its position in energy-efficient and façade solutions within the Indian market.

- In August 2022, Owens Corning acquired Natural Polymers, LLC, an Illinois-based manufacturer of spray polyurethane foam insulation. This acquisition helps Owens Corning expand its building and construction applications, enhancing its offerings in high-performance insulation solutions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 2.9 Billion |

| Forecast Revenue (2033) | USD 5.0 Billion |

| CAGR (2024-2032) | 6.0% |

| Base Year for Estimation | 2023 |

| Historic Period | 2016-2023 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Sheets and Films, Vacuum Insulation Panels (VIP), Coatings, Foils, Foams, Others), By Materials (Aerogels, Silica Aerogels, Metals, Plastic Foams, Fiberglass, Others), By Thickness Range (Less Than 1 Inch, 1 Inch to 2 Inches, 2 Inches to 4 Inches, More Than 4 Inches), By Installation Method (Spray Insulation, Board Insulation, Batts and Rolls, Blown-In Insulation), By Application (Building Thermal Insulation, Thermal Packaging, Wires and Cables, Pipe Coatings, Others), By End User (Automotive, Aerospace, Building and Construction, Oil and Gas, Others) |

| Regional Analysis | North America – The US, Canada, Rest of North America, Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America – Brazil, Mexico, Rest of Latin America, Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa |

| Competitive Landscape | 3M, Actis Insulation Ltd., Armacell International S.A., BASF SE, BNZ Materials, Inc., Cabot Corporation. , Celotax Saint Gobain, ContiTech AG, Dow Chemical Company, Huntsman International LLC, Johns Manville, A Berkshire Hathaway Company, Kingspan Group, Owens Corning, Rockwool Group, Saint-Gobain, UNILIN Insulation, Xtratherm |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |