Quick Navigation

Report Overview

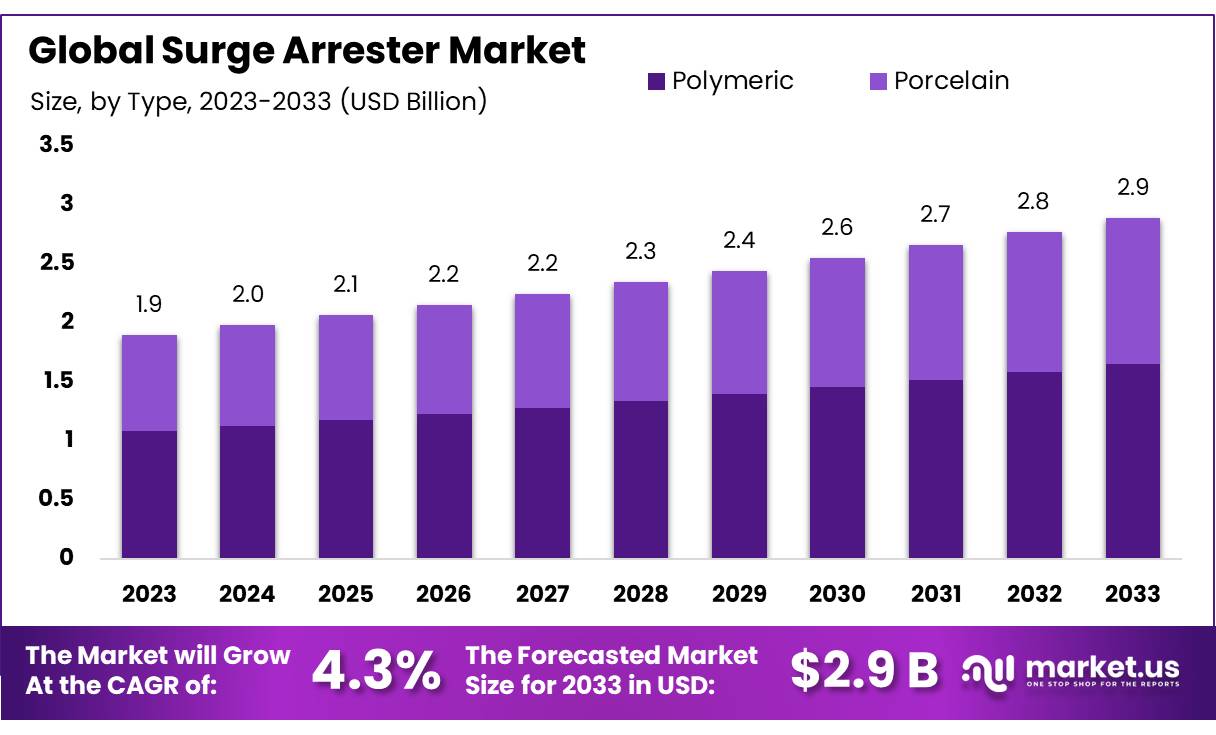

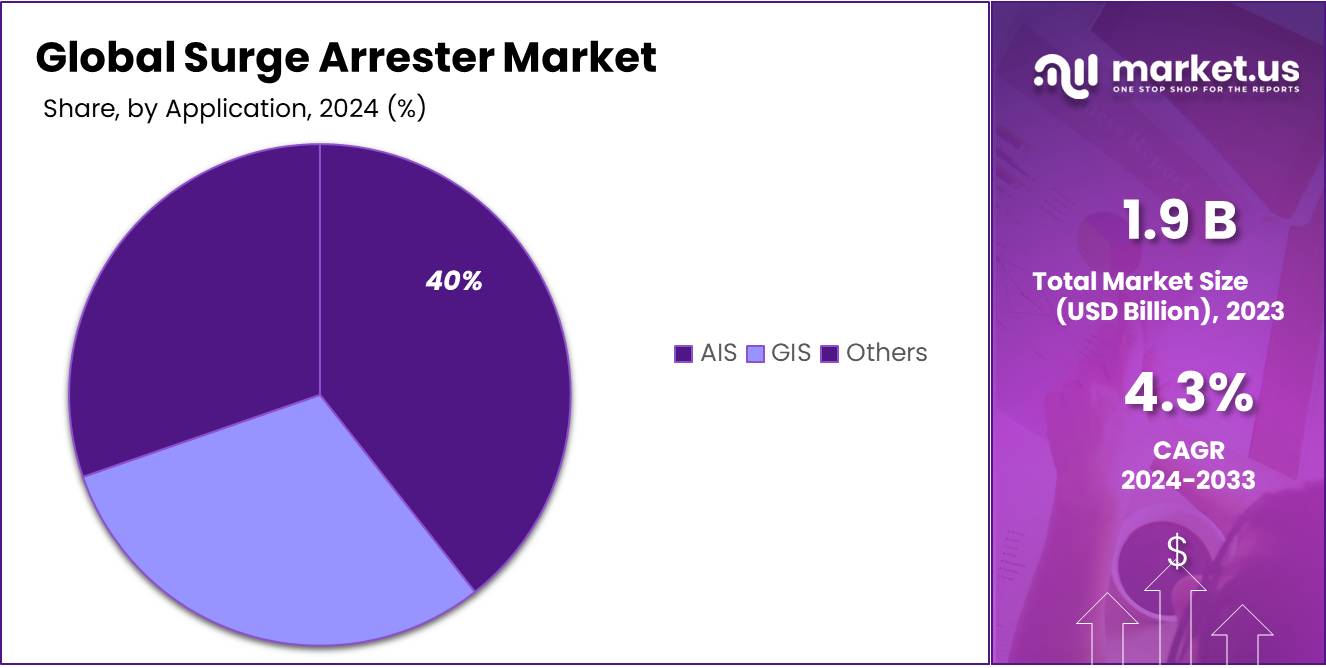

The Global Surge Arrester Market size is expected to be worth around USD 2.9 Bn by 2033, from USD 1.9 Bn in 2023, growing at a CAGR of 4.3% during the forecast period from 2024 to 2033.

A surge arrester is a protective device used in electrical systems to prevent damage from transient voltage surges, often caused by lightning strikes, switching operations, or other electrical disturbances. The surge arrester works by diverting excess voltage to the ground, ensuring that sensitive equipment and infrastructure are not damaged by these high-voltage spikes.

Surge arresters are typically used in power transmission and distribution systems, as well as in industrial and commercial electrical setups, to protect transformers, circuit breakers, and other critical equipment.

In the chemical industry, surge arresters are widely used in petrochemical plants, refineries, and manufacturing facilities, where electrical disturbances can disrupt sensitive machinery and production processes. For instance, the chemical manufacturing sector in the United States reported an increase in demand for surge arresters due to stringent regulations surrounding electrical safety.

According to the U.S. Chemical Safety and Hazard Investigation Board (CSB), electrical equipment failures, including those caused by surge events, are responsible for around 12% of chemical plant incidents. In response, the chemical industry has focused on enhancing safety by investing in surge protection systems.

From a regulatory perspective, the International Electrotechnical Commission (IEC) has introduced guidelines, such as the IEC 61643-11 standard, to ensure the quality and reliability of surge arresters in critical applications.

Additionally, governments in regions like North America, Europe, and Asia Pacific are pushing for safer industrial operations. For instance, the European Union’s CE marking and IEC standards mandate the use of certified surge arresters in certain industrial applications, encouraging manufacturers to adopt advanced surge protection technologies.

Companies like Schneider Electric and Siemens have expanded their portfolios by acquiring surge protection technologies, with Siemens investing €10 million in the development of new surge arresters specifically designed for industrial settings.

Additionally, global chemical companies, such as Dow Chemical and BASF, have entered into partnerships with electrical protection firms to improve safety measures, with BASF reported to have allocated €2 million toward upgrading surge protection systems in its global facilities.

In 2023, China exported $300 million worth of surge arresters, with a significant portion going to North America and Europe, where industries are increasingly reliant on surge protection for manufacturing and chemical processing plants.

Similarly, Germany’s surge arrester exports reached approximately €150 million in 2023, as European chemical plants continue to modernize their electrical systems to comply with stricter safety standards.

Key Takeaways

- Surge Arrester Market size is expected to be worth around USD 2.9 Bn by 2033, from USD 1.9 Bn in 2023, growing at a CAGR of 4.3%.

- Polymeric surge arresters held a dominant market position, capturing more than 57.6% of the global market share.

- High Voltage segment held a dominant market position in the surge arrester market, capturing more than a 49.2% share.

- Distribution Class segment held a dominant market position in the surge arrester market, capturing more than a 51.3% share.

- AIS (Air Insulated Switchgear) held a dominant market position in the surge arrester market, capturing more than a 39.3% share.

- Utilities sector held a dominant market position in the surge arrester market, capturing more than a 57.4% share.

By Type

In 2023, Polymeric surge arresters held a dominant market position, capturing more than 57.6% of the global market share. Polymeric surge arresters are widely favored for their lightweight design, high resistance to environmental factors, and long service life. Made from advanced polymer materials, these arresters offer better performance in harsh environments compared to traditional porcelain models.

Their ability to withstand extreme temperatures and humidity has made them particularly popular in industries such as power transmission and chemical manufacturing. Additionally, the growing trend of adopting energy-efficient and cost-effective solutions has fueled the demand for polymeric surge arresters in emerging markets.

Porcelain surge arresters account for a smaller share of the market. While porcelain arresters are known for their robustness and long track record in the industry, their relatively heavier weight and lower resistance to environmental wear have limited their widespread use compared to polymeric variants.

They are, however, still widely used in regions with stable weather conditions and in applications where the arresters are exposed to fewer extreme environmental factors. The demand for porcelain surge arresters remains steady, especially in established infrastructure where these systems have been in use for many years.

By Voltage

In 2023, the High Voltage segment held a dominant market position in the surge arrester market, capturing more than a 49.2% share. This dominance is primarily due to the critical role high voltage surge arresters play in protecting electrical equipment in substations, power plants, and transmission lines from voltage spikes. Their ability to safeguard high-value assets from over-voltage events makes them indispensable in high voltage applications, where the potential damage and resulting cost from electrical surges can be substantial.

High voltage surge arresters are designed to handle voltages typically ranging from 69 kV and above. This capability is essential in settings where reliable power distribution and transmission are critical, including industrial and large-scale commercial environments. The growing demand for electricity and the expansion of the renewable energy sector drive the need for robust power infrastructure, further bolstering the market for high voltage surge arresters.

By Class

In 2023, the Distribution Class segment held a dominant market position in the surge arrester market, capturing more than a 51.3% share. This class of surge arresters is typically used in systems where the voltage levels range from 1 kV to 36 kV, making them a fundamental component in local distribution networks. Their widespread use is largely due to their critical role in protecting distribution infrastructure and equipment from the damaging effects of electrical surges caused by lightning and switching operations.

The prevalence of Distribution Class surge arresters is supported by the extensive expansion and upgrading of electrical distribution networks globally. As urban areas expand and the demand for reliable electricity supply increases, utilities are investing in surge protection to ensure system reliability and to reduce the frequency and severity of power disruptions.

By Application

In 2023, AIS (Air Insulated Switchgear) held a dominant market position in the surge arrester market, capturing more than a 39.3% share. This significant market share is due to AIS’s widespread adoption in electrical grids for medium to high voltage applications.

AIS technology is preferred for its reliability and cost-effectiveness, making it a staple in both urban and industrial settings. It’s especially valued for its ease of maintenance and robustness in harsh environmental conditions, which reduces downtime and extends the service life of electrical components.

The prevalence of AIS is also bolstered by the ongoing expansion of power generation and distribution networks worldwide. As countries invest in upgrading their power infrastructure to meet growing energy demands and improve grid reliability, AIS systems equipped with surge arresters play a critical role in safeguarding equipment from voltage spikes and ensuring uninterrupted power supply.

By End-use

In 2023, the Utilities sector held a dominant market position in the surge arrester market, capturing more than a 57.4% share. This substantial market share is attributed to the critical role surge arresters play in protecting utility infrastructure from over-voltage incidents caused by lightning strikes and switching operations. Utilities, which include electric power providers, are foundational to national infrastructures and require robust protection mechanisms to ensure reliable service delivery and grid stability.

The demand for surge arresters in this sector is driven by the need to minimize power outages and equipment failures that can result in significant economic losses and reduced public confidence in utility services. Surge arresters help mitigate these risks by safeguarding transformers, transmission lines, and other critical components against voltage surges.

Key Market Segments

By Type

- Polymeric

- Porcelain

By Voltage

- Medium Voltage

- High Voltage

- Extra High Voltage

By Class

- Distribution Class

- Intermediate Class

- Station Class

By Application

- AIS

- GIS

- Others

By End-use

- Utilities

- Industries

- Transportation

Drivers

Increased Adoption of Renewable Energy Sources

In 2023, renewable energy generation accounted for 29.4% of global electricity production, with wind and solar energy growing at rates of 14% and 20% annually, respectively. This rise in renewable energy capacity has led to an increased demand for surge protection devices.

For instance, the International Energy Agency (IEA) predicts that global renewable power generation will expand by an additional 50% by 2025, further driving the need for surge arresters. The adoption of advanced surge protection technologies is crucial for ensuring the reliability and longevity of renewable energy systems, especially in regions that experience high electrical disturbances.

Stringent Government Regulations and Standards

For instance, the International Electrotechnical Commission (IEC) has developed standards, such as the IEC 61643-11, which defines the performance and safety requirements for surge arresters used in low-voltage power systems. Compliance with these standards is mandatory in many countries, particularly in Europe, where electrical safety regulations are stringent.

In addition to IEC standards, national and regional regulations in countries like the U.S., Germany, and China are pushing for more reliable surge protection systems. In 2023, the U.S. government allocated $3.5 billion to enhance grid resilience and protection systems, including surge arresters, in critical infrastructure.

Similarly, the European Union has committed €100 billion to modernize its energy grid, with a significant portion allocated to improving surge protection. These investments not only drive demand for surge arresters but also push the market toward more innovative, high-performance solutions.

Rising Industrialization and Infrastructure Development

As industrialization continues to expand, especially in emerging markets, the demand for surge arresters has been steadily increasing. The surge arrester market is closely tied to the growth of industries such as manufacturing, chemical production, and oil and gas, where electrical infrastructure is crucial for production processes.

For example, in China, the manufacturing sector grew by 8.5% in 2023, contributing to a significant increase in energy demand. The expansion of industrial parks and energy-intensive facilities requires reliable power protection systems.

The U.S. Chemical Safety and Hazard Investigation Board (CSB) reports that electrical equipment failures, including those caused by surge events, account for about 12% of industrial accidents. As a result, there has been a rise in investments in surge arresters to mitigate these risks.

Moreover, in India, the government allocated $20 billion to infrastructure development in 2023, which is expected to further boost the demand for surge protection systems as new industrial hubs are built.

Restraints

High Initial Cost of Surge Arresters

The cost factor becomes a significant barrier, especially for industries or regions with budget constraints. In 2023, the average cost of a high-voltage surge arrester was estimated at $1,500 to $3,000 per unit, depending on the voltage level and capacity. For large-scale operations, these costs can quickly accumulate, making the initial investment a concern.

For example, in the food processing industry, which operates energy-intensive systems and relies heavily on continuous operations, the initial capital expenditure for surge arresters can be substantial. The industry also faces tight margins, and any additional costs are carefully scrutinized.

According to World Bank data, the global food processing market was valued at $3.5 trillion in 2023. As food manufacturers invest in automation and advanced systems, the need for surge arresters rises to protect sensitive equipment. However, the high upfront cost of surge arresters remains a challenge for smaller food production companies or those in emerging markets with limited capital.

Maintenance and Replacement Costs

For instance, in developing economies where surge arresters are less commonly used, the need for regular servicing of these devices can lead to unforeseen expenses.

According to the International Finance Corporation (IFC), the cost of electrical infrastructure maintenance in sub-Saharan Africa alone is estimated to be around $8 billion annually, a significant portion of which is spent on the upkeep of electrical protection systems like surge arresters.

Lack of Awareness and Technical Expertise

A third restraining factor is the lack of awareness and technical expertise regarding the importance of surge arresters, particularly in industries like food processing and agriculture. In many parts of the world, companies may not be fully aware of the risks posed by electrical surges and the potential damage they can cause to their operations. In regions with less robust infrastructure, companies may delay investing in surge arresters, opting for cheaper, less effective solutions.

For example, in certain rural areas of India, a large portion of food processing operations lack proper surge protection systems due to the high cost and limited technical knowledge. According to the Food Processing Division of the Indian Ministry of Food Processing Industries, the sector is still developing in terms of technological adoption, with only 40% of food processing units equipped with modern electrical protection systems.

Regulatory Barriers and Slow Adoption in Emerging Markets

The slow pace of regulatory enforcement in emerging markets also contributes to the restraint on surge arrester adoption. While developed regions like Europe and North America have well-established electrical safety regulations, some developing nations still lack stringent guidelines or delay their implementation. In these regions, companies may not be legally compelled to use surge arresters, leading to lower demand.

For example, in Latin America, several countries are still in the process of enhancing their energy infrastructure standards. According to the Inter-American Development Bank (IDB), only 50% of electrical infrastructure projects in Latin America comply with advanced safety standards, compared to 85% in Europe.

The lack of regulatory pressure in these regions means that many businesses, particularly in the food and agriculture sectors, do not prioritize surge protection, further limiting the overall market growth of surge arresters in the region.

Opportunity

Growing Demand for Surge Protection in Industrial Automation

One of the major growth opportunities for the surge arrester market is the increasing demand for surge protection in industrial automation systems. As industries around the world, including food processing, invest heavily in automation to improve productivity, efficiency, and safety, the need for surge protection has escalated.

Surge arresters are essential in safeguarding sensitive electrical and electronic systems in automated production lines from power surges, which could otherwise lead to expensive downtime or equipment damage. In 2023, the global industrial automation market was valued at approximately $200 billion, with projections to grow by 9% annually over the next decade.

The food processing industry, which is a significant part of industrial automation, plays a crucial role in this trend. With an annual growth rate of 3.4% globally, the food processing market is increasingly reliant on automated technologies.

The Food and Agriculture Organization (FAO) highlighted that the global food processing sector is expected to grow at a compounded annual growth rate (CAGR) of 5.1% until 2027. As more automated processes are introduced to meet the rising demand for processed food, the need for surge arresters to ensure the smooth functioning of machinery in these plants will continue to rise.

Government Initiatives Supporting Automation and Safety

Another major growth opportunity stems from government initiatives aimed at improving industrial safety standards and promoting energy efficiency, particularly in food manufacturing. Governments are increasingly mandating stricter safety regulations in industries that are vulnerable to electrical faults, especially as automation systems become more widespread.

For instance, in the European Union, regulations under the EU Machinery Directive require food manufacturers to ensure that their electrical systems are protected from power surges. This mandates the use of surge protection equipment, including arresters, in all major production plants.

In China, the Ministry of Industry and Information Technology has introduced policies to promote advanced manufacturing and energy efficiency, which will directly influence the surge arrester market. The government has earmarked over $1.4 billion in subsidies and incentives for companies investing in smarter, safer, and more energy-efficient manufacturing technologies.

Increasing Electrification and Smart Grid Adoption

The increasing shift towards electrification and the adoption of smart grid technologies also presents significant growth opportunities for the surge arrester market. The push towards smarter, more connected grids, particularly in urban areas, is creating a need for surge arresters to protect the infrastructure from high-voltage transients that could result from sudden surges or lightning strikes.

According to the International Energy Agency (IEA), smart grids are expected to represent 50% of the global grid infrastructure by 2030, representing an investment of over $100 billion annually in infrastructure upgrades.

Trends

Increasing Adoption of Smart Surge Arresters

The trend toward smarter surge protection is driven by the increasing demand for predictive maintenance, enhanced reliability, and greater integration with the Internet of Things (IoT). In 2023, the global market for smart grid technologies was valued at approximately $52 billion and is expected to grow at a 14% CAGR through 2028, indicating a shift towards more connected and intelligent electrical systems.

In the food processing industry, the use of smart surge arresters is becoming more prevalent as manufacturers adopt more sophisticated automation and smart technologies. The International Food Information Council (IFIC) reports that 80% of food manufacturers are implementing or planning to implement smart factory technologies to enhance operational efficiency.

Shift Toward Sustainable Energy and Green Manufacturing

The transition to clean energy is supported by government incentives and policies such as the EU Green Deal, which aims to make Europe climate-neutral by 2050. These initiatives are driving significant investments in renewable energy infrastructure, increasing the demand for surge arresters.

In the food processing sector, companies are increasingly turning to renewable energy to power operations. According to the Food and Agriculture Organization (FAO), the global demand for organic food products has been rising steadily, with the organic food market reaching a value of $110 billion in 2023.

As more food manufacturers switch to renewable energy sources like solar and wind, the need for surge arresters to protect sensitive electrical systems in these energy-efficient facilities also rises. In regions such as North America and Europe, where renewable energy adoption is higher, the surge arrester market is seeing significant growth.

Government Policies and Regulations Driving Market Growth

For instance, in 2023, the U.S. Department of Energy launched initiatives to support the modernization of electrical infrastructure, with a focus on enhancing grid resilience against extreme weather events. These initiatives include funding for surge protection systems in vulnerable areas, leading to an increase in demand for surge arresters.

Similarly, the European Union continues to impose stricter electrical safety standards, encouraging manufacturers to adopt surge protection solutions to meet regulatory requirements.

The food industry is particularly affected by these policies, as it relies heavily on consistent, uninterrupted power for manufacturing processes. The increased government focus on electrical infrastructure resilience has led to higher investments in surge arresters across the sector.

The World Bank reports that the global food processing sector saw an investment surge of 8% in 2023, with much of the funding directed toward improving energy efficiency and power quality, including the installation of surge protection equipment.

Regional Analysis

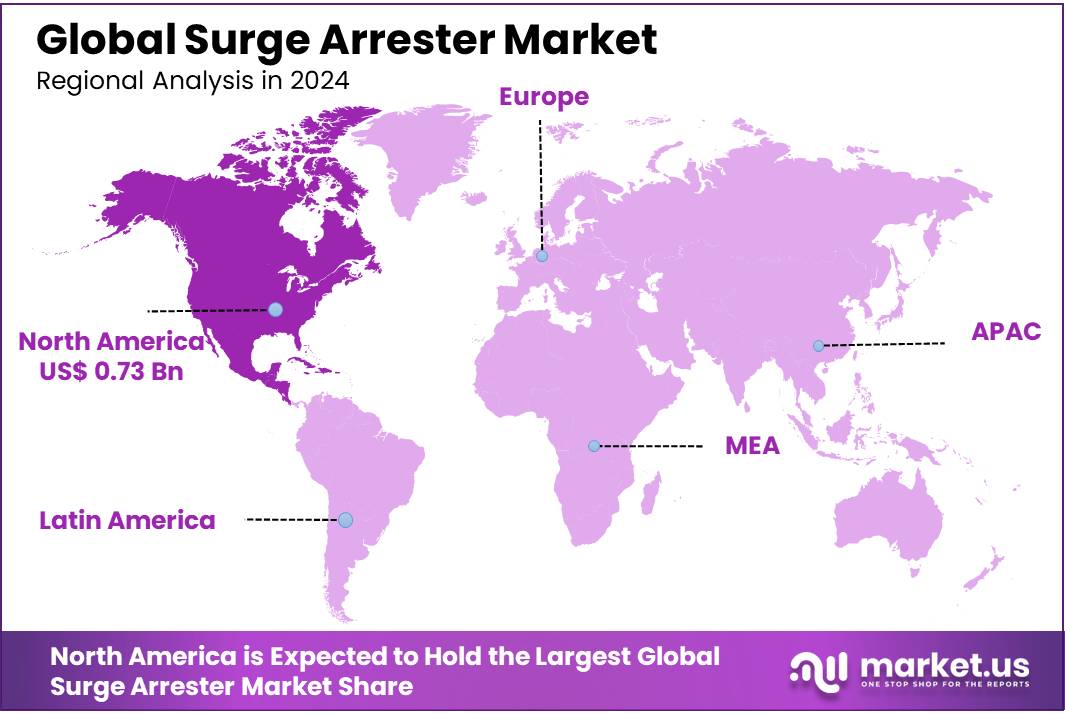

In the global surge arrester market, the Asia Pacific (APAC) region holds a dominant position with a 37.8% market share, amounting to USD 0.73 billion. This leadership is driven by significant investments in electrical infrastructure development and upgrades across major economies like China and India, where rapid urbanization and industrial growth fuel demand for reliable power distribution systems.

The region’s focus on integrating renewable energy sources further boosts the need for effective surge protection to safeguard these increasingly complex grid systems.

In contrast, North America and Europe also represent substantial markets, each characterized by advanced grid technologies and a high penetration of renewable energy sources. In North America, the surge arrester market is propelled by ongoing investments in grid modernization and renewable integrations, as well as stringent standards for electrical system safety and reliability. Europe’s market is similarly driven, with additional impetus from regulatory frameworks emphasizing energy efficiency and system security across the EU.

The Middle East & Africa (MEA) and Latin America are emerging as significant growth areas within the surge arrester market. In MEA, the development of both conventional and renewable power generation projects, particularly in Gulf Cooperation Council (GCC) countries, necessitates robust grid protection mechanisms.

Latin America’s market growth is spurred by the modernization of aging power infrastructure and increasing investments in renewable energy, which require advanced surge protection solutions to handle the intermittency and volatility associated with renewable sources.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The surge arrester market features a robust lineup of key players, each contributing to the sector’s innovation and growth. Companies like ABB, General Electric, and Siemens Energy are renowned for their leadership in power management technologies and have been pivotal in advancing surge protection solutions globally. These industry giants are complemented by specialized firms such as Raycap Corporation S.A., and Hakel, which provide niche products and services tailored to specific market needs.

Furthermore, firms like Eaton and Schneider Electric enhance the market with their comprehensive range of electrical components that include surge protection devices, reflecting their commitment to electrical safety and reliability.

Companies like Mitsubishi Electric and Toshiba continue to innovate in the electrical and electronic manufacturing spaces, broadening the applications for surge arresters across various industries, including utilities, transportation, and industrial sectors.

Together, these companies drive forward the development of the surge arrester market through extensive R&D, strategic mergers and acquisitions, and global expansion strategies. Their efforts are crucial for meeting the evolving demands of modern electrical systems and ensuring resilience against transient voltages and power surges in increasingly complex network environments.

Top Key Players

- ABB

- CG Power

- E. Connectivity

- E. Oil & Gas

- Eaton

- Emerson Electric

- G. Power

- General Electric

- Hakel

- HAKEL spol. Sr.

- Hitachi

- Hubbell

- INAEL Electrical Systems

- Izoelektro D.O.O.

- Lamco

- Legrand S.A

- Leviton Manufacturing

- Meidensha

- Mitsubishi Electric

- NGK Insulators

- Raycap Corporation S.A.

- Schneider Electric

- Siemens Energy

- TE Connectivity Ltd.

- Toshiba

- Vertiv

Recent Developments

In 2023 ABB’s strong presence in regions like Europe, Asia, and North America helped drive a 9% year-over-year growth in surge arrester sales.

In 2023, CG Power reported a 7.8% growth in its electrical products segment, which includes surge arresters, contributing to overall revenue of $1.2 billion.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 1.9 Bn |

| Forecast Revenue (2033) | USD 2.9 Bn |

| CAGR (2024-2033) | 4.3% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Polymeric, Porcelain), By Voltage (Medium Voltage, High Voltage, Extra High Voltage), By Class (Distribution Class, Intermediate Class, Station Class), By Application (AIS, GIS, Others), By End-use (Utilities, Industries, Transportation) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | ABB, CG Power, E. Connectivity, E. Oil & Gas, Eaton, Emerson Electric, G. Power, General Electric, Hakel, HAKEL spol. Sr., Hitachi, Hubbell, INAEL Electrical Systems, Izoelektro D.O.O., Lamco, Legrand S.A, Leviton Manufacturing, Meidensha, Mitsubishi Electric, NGK Insulators, Raycap Corporation S.A., Schneider Electric, Siemens Energy, TE Connectivity Ltd., Toshiba, Vertiv |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |