Global Soybean Market Size, Share, And Industry Analysis Report By Source Type (Conventional, Genetically Modified Organisms, Non-Genetically Modified Organism, Organic), By Application (Food and Beverages, Pharmaceutical, Dietary Supplements, Biofuel, Personal Care, Lubricants), By Distribution Channel (Online, Offline), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: April 2026

- Report ID: 183754

- Number of Pages: 388

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

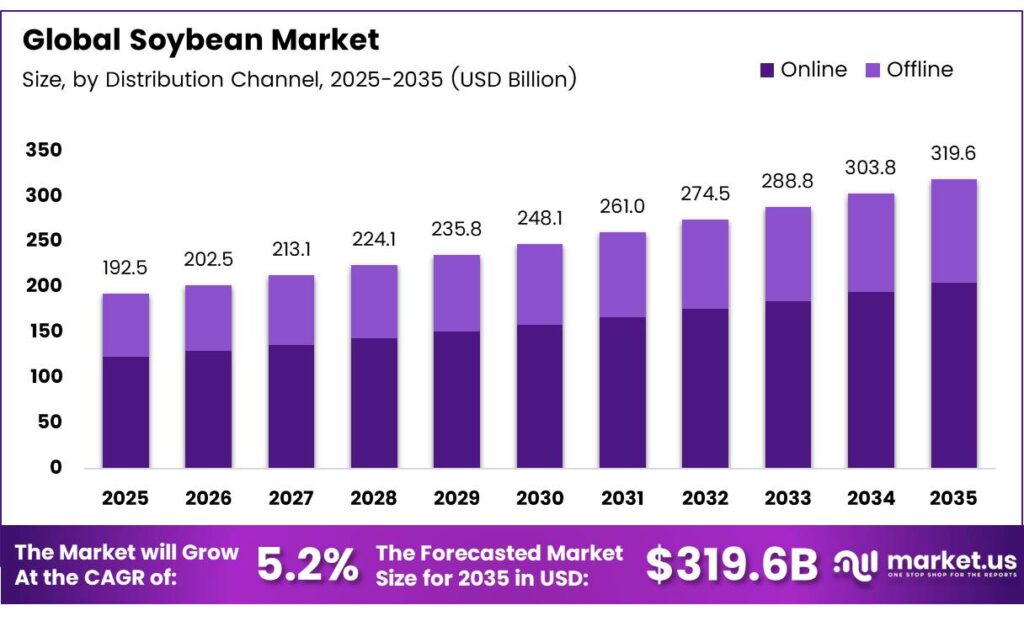

The Global Soybean Market size is expected to be worth around USD 319.6 billion by 2035 from USD 192.5 billion in 2025, growing at a CAGR of 5.2% during the forecast period 2026 to 2035.

The global soybean market represents one of the largest agricultural commodity sectors worldwide. Soybeans serve as a primary source of plant-based protein and edible oil, supporting food production, animal feed, biofuel, and industrial applications across every major region.

Soybean-derived products include soy meal, soy oil, soy protein isolates, and lecithin. These ingredients power industries ranging from livestock nutrition to personal care. Consequently, soybean demand remains deeply tied to global population growth, dietary shifts, and energy transition policies.

Soybean-derived products include soy meal, soy oil, soy protein isolates, and lecithin. These ingredients power industries ranging from livestock nutrition to personal care. Consequently, soybean demand remains deeply tied to global population growth, dietary shifts, and energy transition policies.Brazil soybean production reached 180.0 million metric tons in MY 2025/26, accounting for 42% of global soybean production. This dominance reflects Brazil’s large-scale farming investments and favorable climate, making it the world’s leading soybean supplier by volume.

According to the USDA’s World Agricultural Production circular, global soybean production is estimated at 428.2 million metric tons for MY 2025/26. This record output underscores the crop’s central importance to global food security and its expanding role in energy and industrial markets.

Rising consumer interest in plant-based diets accelerates soy ingredient adoption globally. Food manufacturers increasingly reformulate products using soy protein concentrates and textured soy protein. Therefore, the food and beverages segment remains the single largest application area within the soybean value chain.

Key Takeaways

- The Global Soybean Market is projected to reach USD 319.6 billion by 2035, up from USD 192.5 billion in 2025 at a CAGR of 5.2% during the forecast period 2026 to 2035.

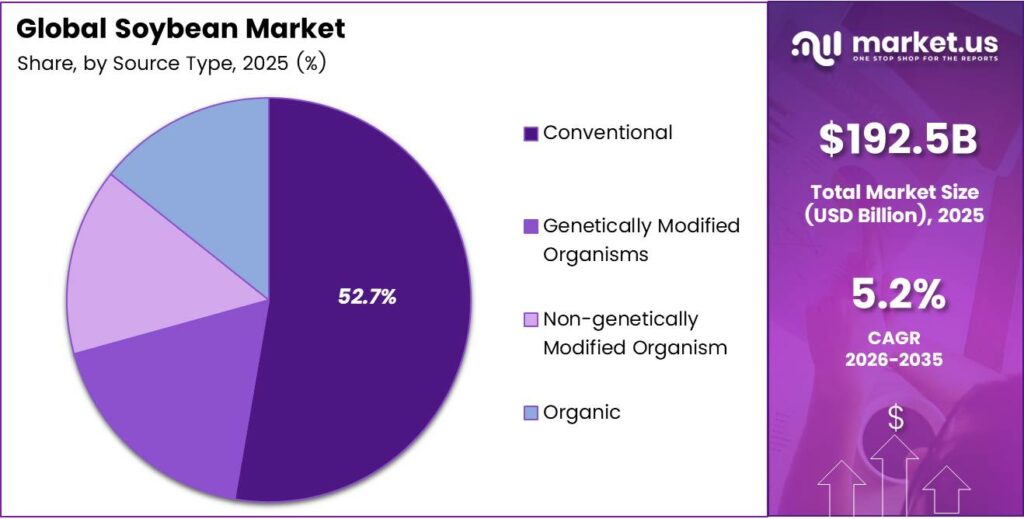

- Conventional soybeans hold the dominant share at 52.7% in 2025.

- Food and Beverages leads with a 43.6% market share in 2025.

- Online channels account for 79.4% of distribution in 2025.

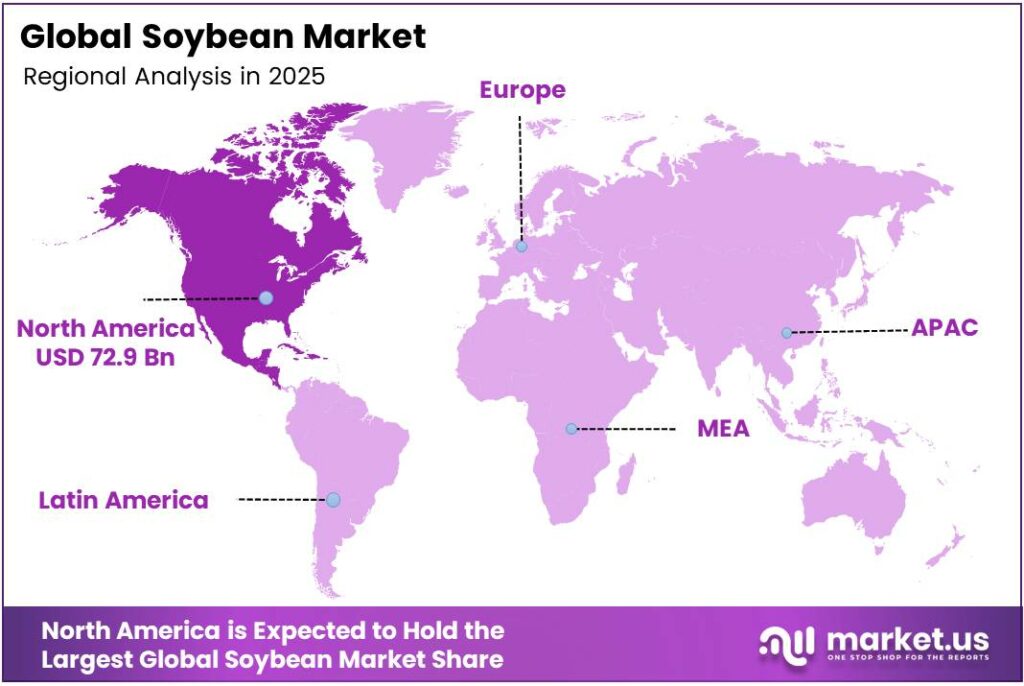

- North America dominates the regional landscape with a 37.9% share, valued at USD 72.9 billion.

Distribution Channel Analysis

Online channels dominate with 79.4% due to expanding digital procurement platforms and direct-to-buyer sourcing models.

In 2025, Online distribution held a dominant market position in the By Distribution Channel segment of the Soybean Market, with a 79.4% share. Digital trading platforms, commodity exchanges, and agri-tech procurement tools allow buyers to source soybeans directly from producers. Consequently, online channels reduce intermediary costs and improve supply chain transparency for food, feed, and industrial buyers.

Offline distribution retains relevance for small-scale buyers, regional cooperatives, and markets with limited digital infrastructure. Traditional brokers, physical auctions, and local agri-retailers continue serving buyers who require personal negotiation and spot-market flexibility. However, offline channels are gradually losing volume share as digital adoption accelerates across commodity supply chains.

Application Analysis

Food and Beverages dominate with 43.6% due to soybeans’ role as a versatile, affordable, and high-protein food ingredient.

In 2025, Food and Beverages held a dominant market position in the By Application segment of the Soybean Market, with a 43.6% share. Soy protein, tofu, soy milk, and edible oil remain staple products across global food systems. Moreover, plant-based food trends have intensified soy ingredient integration in meat alternatives and functional beverages.

Pharmaceutical applications utilize soy-derived lecithin and isoflavones in drug formulations and nutraceuticals. Soy isoflavones attract interest for their role in hormone health and cardiovascular support. Consequently, pharmaceutical companies maintain a steady demand for high-purity soy extracts to support product development pipelines.

Dietary Supplements represent a high-growth application area driven by fitness and wellness consumer segments. Soy protein isolates appear widely in protein powders, meal replacement shakes, and sports nutrition products. Therefore, supplement manufacturers continue expanding soy-based formulations to meet clean-label and plant-based protein demand.

Source Type Analysis

Conventional soybeans dominate with 52.7% due to wide availability, established supply chains, and lower production costs.

In 2025, Conventional soybeans held a dominant market position in the By Source Type segment of the Soybean Market, with a 52.7% share. Conventional varieties benefit from well-developed agronomic systems, broad farmer adoption, and compatibility with existing processing infrastructure. Moreover, their cost efficiency makes them the preferred choice for large-scale feed and food manufacturing globally.

Genetically Modified Organism (GMO) soybeans represent a significant and growing portion of the global supply. These varieties offer enhanced pest resistance, drought tolerance, and higher yield stability. Consequently, farmers across Brazil, the United States, and Argentina increasingly adopt GMO cultivars to manage input costs and reduce crop loss risks.

Non-Genetically Modified Organism (Non-GMO) soybeans attract premium buyers in regulated markets. Food companies in Europe and Japan specifically source non-GMO varieties to meet labeling requirements and consumer preferences. Therefore, non-GMO production commands price premiums and supports niche but expanding specialty supply chains.

Key Market Segments

By Distribution Channel

- Online

- Offline

By Source Type

- Conventional

- Genetically Modified Organisms

- Non-Genetically Modified Organism

- Organic

By Application

- Food and Beverages

- Pharmaceutical

- Dietary Supplements

- Biofuel

- Personal Care

- Lubricants

- Others

Emerging Trends

Record Global Soybean Demand, Tightening Stocks, and Supporting Price Resilience

Record-high global soybean demand continues to tighten commodity stocks across major producing nations. United States soybean production reached 115.99 million metric tons in MY 2025/26, representing 27% of global output. This substantial U.S. share signals strong planting momentum driven by biofuel market signals and crop rotation incentives, keeping supply conditions competitive.

Sustainability Regulations and High-Oleic Cultivars Reshaping Soybean Trade Practices

Rapid adoption of high-oleic soybean cultivars improves oil stability for both food and fuel applications. Sustainability regulations simultaneously reshape international sourcing practices and trade compliance standards. Consequently, buyers across Europe and Asia now demand verified, deforestation-free supply chains. These twin forces push producers toward premium certified programs that command higher prices in regulated import markets.

Drivers

Rising Meat Consumption and Biofuel Mandates Drive Soybean Demand Globally

Escalating global demand for soybean meal in the livestock feed sector directly reflects rising meat consumption in emerging economies. Additionally, policy-driven biofuel mandates in major economies expand soybean oil use in renewable diesel production. The U.S. soybean exports totaled USD 24.58 billion and 52.40 million metric tons in calendar year 2024, confirming robust global buyer appetite for American soybeans.

Plant-Based Protein Growth and GMO Yield Gains Reinforce Market Expansion

Surging consumer interest in plant-based proteins fuels widespread soy ingredient adoption across food manufacturing and retail segments. Moreover, advanced genetically modified soybean varieties boost yield stability and improve farmer profitability. These combined forces create a self-reinforcing demand cycle where higher yields support lower prices, broader market access, and accelerating consumption in both developed and developing markets.

Restraints

Geopolitical Trade Tensions Disrupt Key Soybean Export Flows from Major Producers

Geopolitical trade tensions and tariffs significantly disrupt established soybean export flows from the United States and South America. Japan imported USD 1.07 billion of U.S. soybeans, making it one of the top three destination markets. Trade policy uncertainty threatens these import relationships, forcing buyers to consider alternative suppliers and increasing procurement costs across the global soybean value chain.

Crop Vulnerability to Weather Extremes and Pest Outbreaks Limits Yield Predictability

Heightened vulnerability to pest outbreaks and weather extremes reduces global soybean crop yields in key production regions. Climate variability affects planting windows, soil moisture levels, and disease pressure across Brazil, the United States, and Argentina. Therefore, yield uncertainty raises insurance costs and challenges both farmer profitability and the long-term supply reliability that food manufacturers and feed processors depend upon.

Growth Factors

Deforestation-Free Supply Chains and Precision Agriculture Unlock Premium Soybean Markets

Certified deforestation-free and traceable soybean supply chains are unlocking access to premium European and Asian buyer markets. Simultaneously, precision agriculture technologies enhance resource efficiency on soybean farms, reducing water, fertilizer, and pesticide use. Global soybean trade is projected at 186.2 million metric tons for MY 2025/26, representing 88.2% of total oilseed trade volume — confirming soybeans’ dominance in global agricultural commodity flows.

Industrial Oleochemicals and Asia-Pacific Snacking Segments Drive New Growth Opportunities

Rising demand for soy-based industrial oleochemicals and high-value processed applications creates diversified revenue streams beyond traditional food and feed markets. Additionally, the expansion of soy food products into health-focused convenience and snacking segments in the Asia-Pacific presents substantial volume growth potential. Consequently, soybean processors and food brands are investing in product innovation to capture these fast-evolving consumption opportunities.

Regional Analysis

North America Dominates the Soybean Market with a Market Share of 37.9%, Valued at USD 72.9 Billion

North America holds the largest share of the global soybean market, accounting for 37.9% of total revenue, valued at USD 72.9 billion in 2025. The United States drives this dominance through large-scale commercial farming, advanced processing infrastructure, and deep integration with global commodity trade networks. Moreover, strong domestic biofuel policy and livestock feed demand sustain year-round soybean consumption and export volumes across the region.

Europe represents a mature but evolving soybean market shaped by strict sustainability regulations and growing plant-based food demand. European buyers actively seek certified non-GMO and deforestation-free soybean supplies to comply with regulatory requirements. Additionally, the EU’s renewable energy directives continue to support soybean oil use in biodiesel blending programs across member states.

Asia Pacific is one of the fastest-growing soybean import regions, led by China, Japan, Indonesia, and India. Regional demand for soy-based food products, animal feed, and industrial ingredients expands steadily with rising incomes and dietary transitions.

Middle East and Africa present an emerging opportunity for soybean market participants. Growing populations and rising protein consumption drive feed and food ingredient imports across the region. Consequently, soybean meal demand from poultry and aquaculture sectors is accelerating, particularly in Egypt, Saudi Arabia, South Africa, and Nigeria, as regional agri-food industries expand their processing capacity.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Kerry Group plc is a global taste and nutrition company headquartered in Ireland with a strong presence in soy-based food ingredient manufacturing. The company develops soy protein concentrates, isolates, and functional blends for food and beverage manufacturers. Moreover, Kerry’s extensive R&D network allows it to deliver tailored soy solutions that align with clean-label and plant-based food trends across global markets.

Fuji Oil Group, based in Japan, specializes in plant-based fats, oils, and proteins with deep expertise in soybean processing. The company serves confectionery, dairy alternative, and foodservice sectors globally. Additionally, Fuji Oil has invested substantially in sustainable soybean sourcing, establishing long-term supply partnerships with South American producers to ensure consistent quality and traceability for its international customer base.

House Foods Corporation is a leading Japanese food manufacturer with a focused portfolio in tofu, soy beverages, and plant-based food products. The company commands a significant share of the domestic Japanese soy food market and continues expanding its footprint in North American plant-based food retail. Consequently, House Foods leverages growing health-conscious consumer demand to introduce innovative soy-based convenience food products.

Danone North America operates in the soybean market through its plant-based dairy alternative brands, utilizing soy as a core protein ingredient. The company serves health-focused consumers with soy milk, yogurt alternatives, and protein-enriched beverages. Furthermore, Danone integrates sustainability commitments into its soybean sourcing strategy, prioritizing suppliers with verified environmental and social standards across its North American supply chain.

Top Key Players in the Market

- Kerry Group plc

- Fuji Oil Group

- House Foods Corporation

- Danone North America

- DuPont de Nemours, Inc.

- Cargill, Inc.

- Scoular

- Archer-Daniels-Midland Co.

- Nordic Soya Oy

Recent Developments

- In 2025, Kerry Group maintains a formal Soy Policy committing to 100% Deforestation and Conversion-Free (DCF) sourcing for all direct-sourced soybeans and soy derivatives by the end of 2025. This aligns with its broader DCF Policy and the Accountability Framework.

- In 2025, Fuji Oil’s Responsible Soybeans and Soy Products Sourcing Policy commits to zero deforestation, zero exploitation, and legal compliance across its global soybean supply chain. The policy applies to whole soybeans, defatted soybeans, and isolated soy proteins, with ongoing supplier dialogues in North America and China.

Report Scope

Report Features Description Market Value (2025) USD 192.5 Billion Forecast Revenue (2035) USD 319.6 Billion CAGR (2026-2035) 5.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Source Type (Conventional, Genetically Modified Organisms, Non-Genetically Modified Organisms, Organic), By Application (Food and Beverages, Pharmaceutical, Dietary Supplements, Biofuel, Personal Care, Lubricants, Others), By Distribution Channel (Online, Offline) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Kerry Group plc, Fuji Oil Group, House Foods Corporation, Danone North America, DuPont de Nemours, Inc., Cargill, Inc., Scoular, Archer-Daniels-Midland Co., Nordic Soya Oy Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Kerry Group plc

- Fuji Oil Group

- House Foods Corporation

- Danone North America

- DuPont de Nemours, Inc.

- Cargill, Inc.

- Scoular

- Archer-Daniels-Midland Co.

- Nordic Soya Oy

Our Clients

- 183754

- April 2026