Quick Navigation

Report Overview

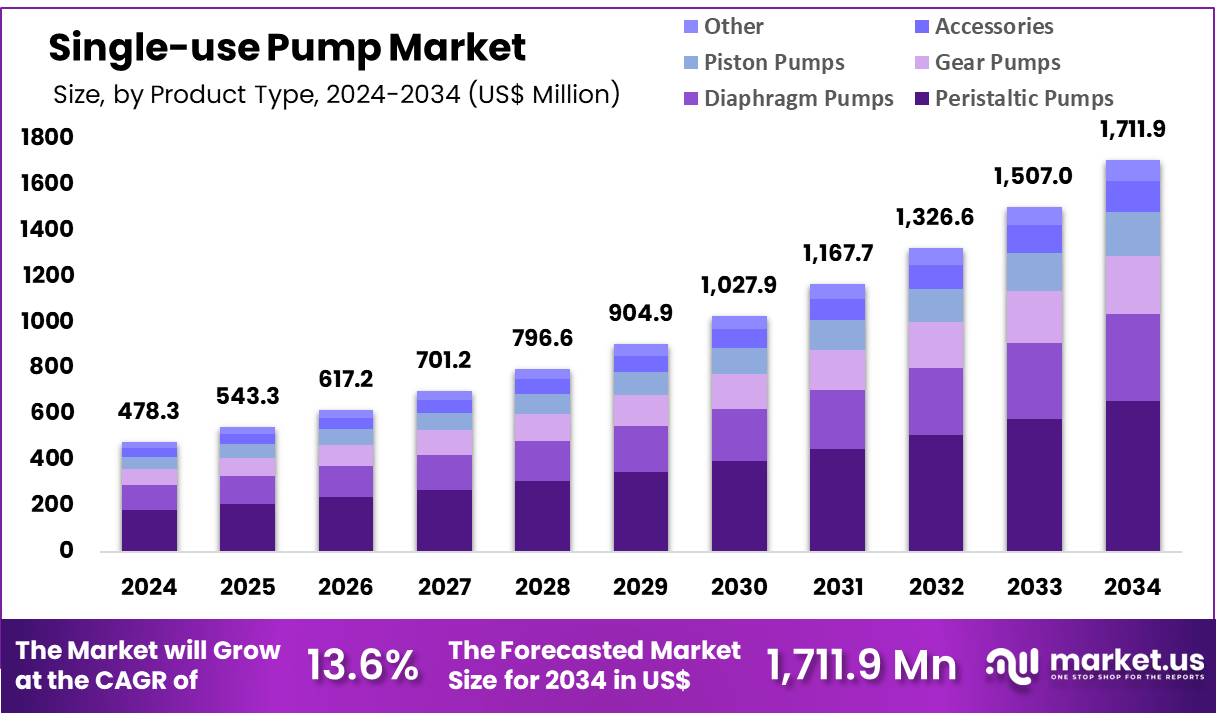

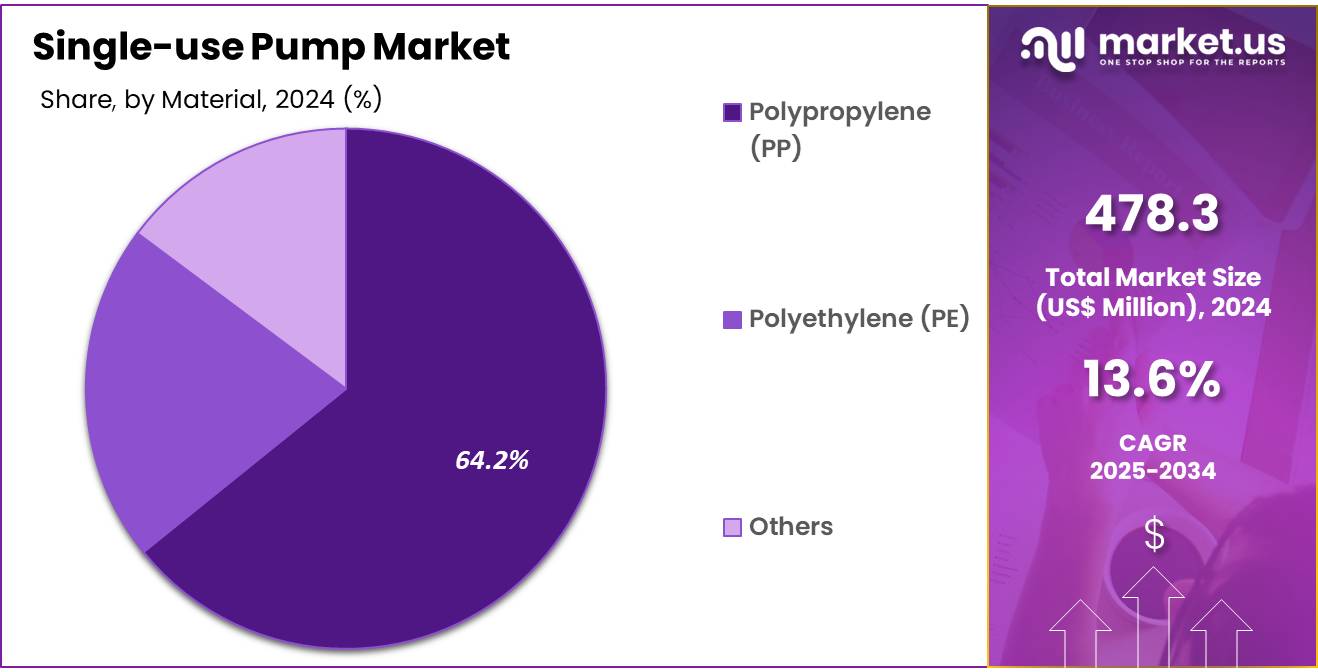

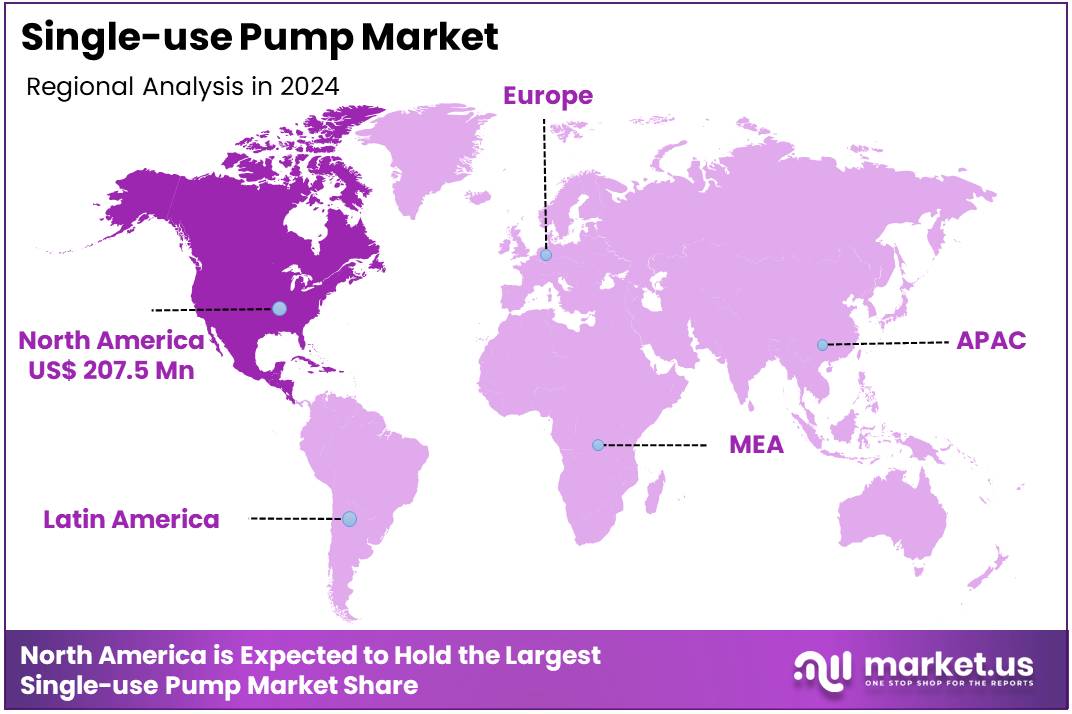

Global Single-use Pump Market size is expected to be worth around US$ 1711.9 Million by 2034 from US$ 478.3 Million in 2024, growing at a CAGR of 13.6% during the forecast period from 2025 to 2034. In 2024, North America led the market, achieving over 43.4% share with a revenue of US$ 207.5 Million.

The global single-use pump market is growing steadily due to the rising use of single-use technologies in biopharmaceutical production, clinical research, and lab processes. These pumps, also called disposable pumps, are ready-to-use, sterile devices designed for one-time use. They help reduce contamination risks and save time by eliminating cleaning and sterilization steps.

Single-use pumps are widely used in bioprocessing, especially in upstream and downstream operations like transferring media, handling buffers, and filling final products. Their simple design and sterile pathways make them suitable for handling sensitive items such as biologics, vaccines, and cell-based therapies. The shift toward modular and scalable production methods is also increasing demand for these systems.

A growing elderly population and rising disease rates are pushing up the need for pharmaceuticals. Since drug manufacturing relies heavily on single-use tools, the need for single-use pumps is also increasing. Rising disposable incomes are further driving growth in industries like food and beverages, cosmetics, and chemicals, where these pumps are also being used more often.

Chronic diseases continue to increase healthcare needs. As per the CDC, 60% of adults in the U.S. have at least one chronic disease. WHO data shows that 74% of deaths worldwide in 2023 were due to noncommunicable diseases, mostly in low- and middle-income countries.

The push for safer products, higher efficiency, and regulatory compliance is boosting adoption in pharmaceuticals and biotech. Rising investment in personalized medicine and new biologic drugs is also supporting this market’s growth. North America currently leads due to its strong biopharma base, while Asia-Pacific is expected to grow fastest, driven by healthcare expansion and biomanufacturing development.

Key Takeaways

- Market Size: Global Single-use Pump Market size is expected to be worth around US$ 1711.9 Million by 2034 from US$ 478.3 Million in 2024.

- Market Growth: The market growing at a CAGR of 13.6% during the forecast period from 2025 to 2034.

- Product Analysis: The Peristaltic Pumps segment dominates the market, accounting for approximately 38.5% of the total revenue share.

- Material Analysis: Polypropylene dominates the market, accounting for approximately 64.2% of the total revenue share.

- End-Use Analysis: The Pharmaceutical & Biopharmaceutical segment holds the largest market share, accounting for approximately 31.9%.

- Regional Analysis: In 2024, North America led the market, achieving over 43.4% share with a revenue of US$ 207.5 Million.

Product Type Analysis

The single-use pump market is segmented by product type into Peristaltic Pumps, Diaphragm Pumps, Gear Pumps, Piston Pumps, Accessories, and Others (including Centrifugal, Screw, and similar pumps). Among these, the Peristaltic Pumps segment dominates the market, accounting for approximately 38.5% of the total revenue share. This leadership is primarily driven by their suitability for sterile and contamination-free fluid transfer in biopharmaceutical manufacturing, especially in upstream and downstream processing.

Diaphragm Pumps follow as a widely used type due to their compatibility with viscous fluids and chemicals, making them ideal for applications in biotechnology and laboratory settings. Gear Pumps and Piston Pumps offer precise flow control and are increasingly adopted in high-pressure and dosing applications, particularly in cell therapy and vaccine production.

The Accessories segment comprises tubing, pump heads, and connectors that support pump functionality and is expected to grow steadily with the rise in demand for integrated single-use systems. The Others category includes centrifugal and screw pumps, which are niche but important in specialized industrial and research processes.

Material Analysis

By material type Segmented into Polypropylene (PP), Polyethylene (PE), and Others. Among these, Polypropylene dominates the market, accounting for approximately 64.2% of the total revenue share. Its dominance is attributed to its excellent chemical resistance, high thermal stability, and cost-effectiveness, making it the preferred material for manufacturing disposable pump components used in biopharmaceutical and laboratory applications. Polypropylene’s compatibility with sterilization techniques such as gamma irradiation and autoclaving further enhances its adoption in aseptic environments.

Polyethylene (PE) follows as the second most utilized material due to its flexibility, durability, and non-reactive nature. It is particularly favored in applications requiring lower mechanical strength but high fluid compatibility, such as buffer and media transfer.

The Others category includes materials such as polyvinyl chloride (PVC) and ethylene-vinyl acetate (EVA), which are used in niche applications where specific fluid interaction or mechanical properties are required. However, their overall market presence remains limited compared to polypropylene and polyethylene.

End User Analysis

By end-user types segmented into Pharmaceutical & Biopharmaceutical, Food & Beverages, Chemicals, Water & Wastewater, Cosmetics & Personal Care, and Others (including Healthcare, Diagnostics, etc.). Among these, the Pharmaceutical & Biopharmaceutical segment holds the largest market share, accounting for approximately 31.9%. This dominance is driven by the increasing adoption of single-use technologies in drug development, biologics manufacturing, and vaccine production, where sterile fluid handling and contamination control are critical.

The Food & Beverages industry represents a significant segment, leveraging single-use pumps for hygienic fluid transfer in dairy, beverage, and liquid food processing. The Chemicals sector utilizes these pumps for transferring sensitive or hazardous fluids, benefiting from their disposable and contamination-free design. Water & Wastewater applications involve chemical dosing and fluid treatment, particularly in modular and remote systems.

The Cosmetics & Personal Care industry adopts single-use systems for handling active ingredients and ensuring batch purity. The Others category includes diagnostic laboratories and healthcare facilities where sterile, single-use fluid handling is essential.

Key Market Segments

By Product Type

- Peristaltic Pumps

- Diaphragm Pumps

- Gear Pumps

- Piston Pumps

- Accessories

- Other (Centrifugal, Screw, etc.)

By Material

- Polypropylene (PP)

- Polyethylene (PE)

- Others

By End User Industry

- Pharmaceutical & Biopharmaceutical

- Food & Beverages

- Chemicals

- Water & Wastewater

- Cosmetics & Personal Care

- Other (Healthcare, Diagnostics, etc.)

Market Driver

Rising Adoption in Biopharmaceutical Manufacturing

The growth of the single-use pump market is primarily driven by the increasing adoption of single-use technologies in biopharmaceutical and biotechnology industries. These pumps are essential in upstream and downstream bioprocessing operations, such as media transfer, buffer management, and final fill-finish procedures. Their sterile, disposable nature minimizes cross-contamination risk and eliminates the need for time-consuming cleaning and sterilization, thus improving operational efficiency.

Furthermore, the surge in demand for personalized medicines, monoclonal antibodies, and vaccines—especially post-COVID-19—has accelerated the shift toward flexible, scalable manufacturing platforms where single-use systems are preferred. This shift, supported by regulatory flexibility and reduced validation requirements, has positioned single-use pumps as a cornerstone of modern biologics production.

Market Trend

Increasing Integration of Modular and Scalable Systems

A significant trend reshaping the single-use pump market is the integration of modular and scalable systems in bioprocessing facilities. Manufacturers are increasingly opting for single-use pumps that can be easily integrated into modular cleanroom setups, allowing for quick configuration changes and rapid batch turnovers. These flexible designs support multi-product facilities and reduce capital investment associated with stainless-steel systems.

Additionally, automation and digital monitoring features are being incorporated to enhance process control and data tracking. This evolution is being supported by the pharmaceutical industry’s move toward continuous manufacturing and decentralized production models, especially for personalized therapies and low-volume biologics, which require high customization and rapid deployment.

Market Restraint

Limited Pressure and Flow Rate Capabilities

Despite their advantages, single-use pumps face limitations in pressure and flow rate capacity, which restrict their application in high-intensity industrial processes. Compared to traditional stainless-steel pumps, disposable variants often lack the mechanical robustness required for operations involving high-pressure fluid transfer or abrasive materials. This constraint affects their adoption in segments like large-scale chemical processing and certain pharmaceutical manufacturing processes where continuous, high-volume transfer is necessary.

Moreover, concerns related to the durability and performance consistency of polymer-based materials under extreme conditions hinder market penetration. These limitations can result in higher operational risk, particularly in processes that demand absolute reliability and repeatability.

Market Opportunity

Expansion into Non-Pharma Sectors

While pharmaceutical and biopharmaceutical industries remain the primary users, emerging applications in food & beverages, cosmetics, and specialty chemicals present substantial opportunities for market expansion. Increasing demand for hygienic and contamination-free processing in these industries supports the adoption of single-use pumps.

For instance, in food manufacturing, these pumps ensure clean handling of ingredients such as flavorings, enzymes, and liquid additives. In cosmetics, they enable sterile mixing of sensitive formulations without cross-contact. As regulatory requirements for product safety become more stringent across consumer goods sectors, single-use technologies offer a cost-effective, compliant alternative. This cross-industry applicability is expected to fuel diversified revenue streams for pump manufacturers.

Regional Analysis

In 2024, North America held a dominant market position, capturing more than a 43.4% share and holds US$ 207.5 million market value for the year. This strong position is primarily driven by the region’s well-established biopharmaceutical manufacturing infrastructure. Increased investment in biologics, cell therapies, and personalized medicine has accelerated the demand for sterile and contamination-free fluid handling systems.

The presence of leading pharmaceutical and biotechnology companies across the U.S. and Canada further supports market growth. These companies have increasingly adopted single-use pumps for upstream and downstream processing to meet stringent regulatory requirements and ensure process efficiency. Additionally, the high frequency of clinical trials and FDA-approved drug manufacturing facilities has reinforced the preference for disposable technologies.

Strong government support for pharmaceutical R&D, combined with the region’s advanced healthcare ecosystem, continues to promote adoption. Rising demand for flexible and scalable production systems in the wake of pandemic preparedness has also been a contributing factor. As a result, North America remains a critical growth engine for the global single-use pump market.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the single-use pump market are focusing on product innovation, strategic collaborations, and global expansion to strengthen their market presence. Emphasis is being placed on developing pumps with higher flow accuracy, better chemical compatibility, and enhanced operational safety. Leading manufacturers are investing in automated and modular solutions to meet the growing demand from biopharmaceutical production and sterile fluid handling applications.

Many companies are also enhancing their production capacities to address rising supply needs across North America, Europe, and Asia Pacific. Furthermore, partnerships with contract manufacturing organizations (CMOs) and bioprocessing firms are enabling broader adoption of single-use technologies. This strategic focus on innovation and scalability continues to shape the competitive landscape of the market.

Market Key Players

- Dover Corporation

- Spirax Group plc

- Xylem

- Levitronix

- Watson-Marlow Fluid Technology Solutions

- Fluid Flow Products, Inc.

- SMC Corporation

- Stobbe Group

- Getinge (High Purity New England)

- Ace Sanitary

- Verder Group (Verder Liquids)

- Sartorius AG

- Avantor Inc.

- Parker Hannifin Corporation

- Watson-Marlow Fluid Technology Group

Recent Developments

- Dover Corporation: In November 2023, Dover’s PSG Biotech division introduced the QB2-SD single-use micropump, designed for precise fluid handling in biopharmaceutical applications.

- Spirax Group plc: As of September 2024, Spirax Group’s Watson-Marlow Fluid Technology Solutions showcased their newly launched WMArchitect™ single-use solutions at CPHI Milan 2024, emphasizing advancements in peristaltic pump technology for the life sciences sector.

- Xylem: In January 2024, Xylem launched the Jabsco PureFlo 21 single-use pump, featuring a first-of-its-kind safety valve, enhancing safety and efficiency in bioprocessing applications.

- Levitronix: Levitronix continues to expand its PuraLev® line of low-shear single-use pumps, including models like the i100SU and 600SU, catering to the bioprocessing industry’s demand for gentle fluid handling solutions.

- Watson-Marlow Fluid Technology Solutions: In September 2024, the company introduced the WMArchitect™ single-use solutions, offering customizable fluid path technologies for the life sciences industry, as presented at CPHI Milan 2024.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | US$ 478.3 Million |

| Forecast Revenue (2034) | US$ 1711.9 Million |

| CAGR (2025-2034) | 13.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Peristaltic Pumps, Diaphragm Pumps, Gear Pumps, Piston Pumps, Accessories, Other (Centrifugal, Screw, etc.) By Material (Polypropylene (PP), Polyethylene (PE), Others, By End User (Industry, Pharmaceutical & Biopharmaceutical, Food & Beverages, Chemicals, Water & Wastewater, Cosmetics & Personal Care, Other (Healthcare, Diagnostics, etc.)) |

| Regional Analysis | North America-US, Canada, Mexico;Europe-Germany, UK, France, Italy, Russia, Spain, Rest of Europe;APAC-China, Japan, South Korea, India, Rest of Asia-Pacific;South America-Brazil, Argentina, Rest of South America;MEA-GCC, South Africa, Israel, Rest of MEA |

| Competitive Landscape | Dover Corporation, Spirax Group plc, Xylem, Levitronix, Watson-Marlow Fluid Technology Solutions, Fluid Flow Products, Inc., SMC Corporation, Stobbe Group, Getinge (High Purity New England), Ace Sanitary, Verder Group (Verder Liquids), Sartorius AG, Avantor Inc., Parker Hannifin Corporation, Watson-Marlow Fluid Technology Group |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |