Global Silicon Fertilizer Market Size, Share, And Industry Analysis Report By Form (Solid, Liquid), By Source (Calcium Silicate, Potassium Silicate, Sodium Silicate), By Crop Type (Cereals and Grains, Fruits and Vegetables, Sugar Crops, Oilseeds), By Application (Soil Amendment, Foliar Spray, Hydroponics/Controlled-Environment), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 181185

- Number of Pages: 212

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

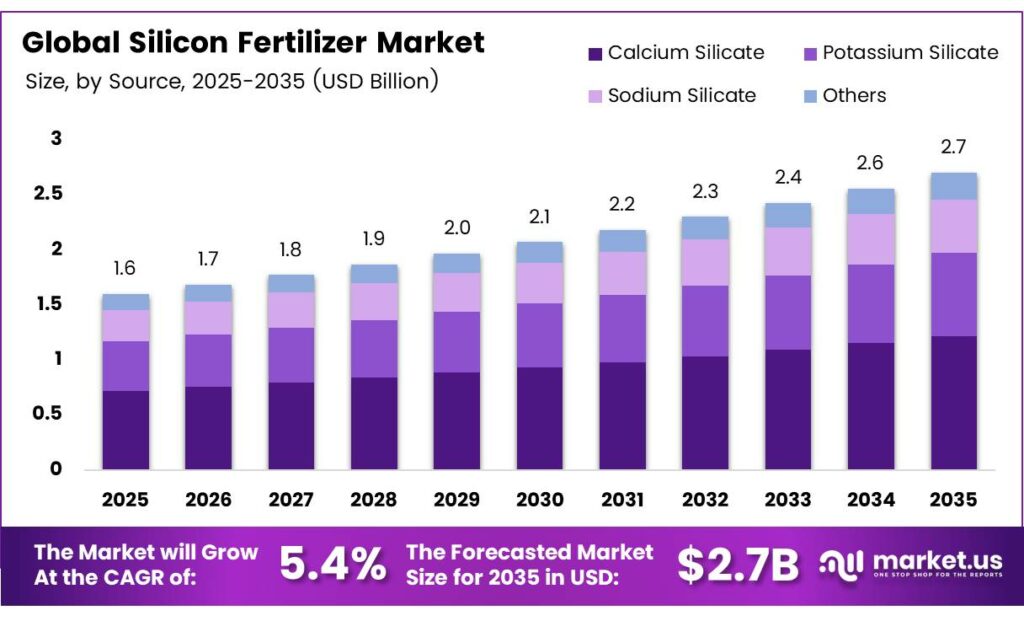

The Global Silicon Fertilizer Market size is expected to be worth around USD 2.7 billion by 2035 from USD 1.6 billion in 2025, growing at a CAGR of 5.4% during the forecast period 2026 to 2035.

Silicon fertilizers supply plant-available silicon to agricultural soils. Farmers apply these products to improve crop strength, stress resistance, and overall yield quality. Silicon acts as a beneficial element that reinforces plant cell walls and supports healthy root development.

Global food demand continues to rise alongside population growth. Farmers face pressure to produce more food per hectare using fewer chemical inputs. Silicon fertilizers offer a sustainable path forward by strengthening crops naturally while reducing dependence on conventional pesticides and synthetic nutrients.

- The United States was the largest 2024 importer of sodium silicates under HS 283919 at $39.09 million and 73,588,700 kg, ahead of Germany at $30.96 million and 68,754,000 kg. This reflects robust industrial and agricultural demand for silicate raw materials across North America and Europe.

Governments across Asia, Africa, and Latin America actively support soil health restoration programs. Regulatory bodies in several countries now recognize silicon as an essential plant nutrient. Moreover, public investment in food security initiatives accelerates the adoption of silicon-based soil amendments across large farming regions.

- The European Union exported $30.83 million and 47,879,800 kg of sodium silicates under HS 283919 in 2024, with Turkey and the United States among the top destinations. This export volume highlights Europe’s central role as a silicate supplier, reinforcing the market’s cross-regional supply chain strength and its growing integration with global agricultural input networks.

Agricultural soils globally face significant silicon depletion due to decades of intensive monocropping. Continuous harvesting removes silicon from the soil without adequate replacement. Consequently, farmers increasingly turn to silicon fertilizers as soil remineralizers to restore productive capacity and maintain long-term field health.

Key Takeaways

- The Global Silicon Fertilizer Market was valued at USD 1.6 billion in 2025 and is forecast to reach USD 2.7 billion by 2035 at a CAGR of 5.4% during the forecast period from 2026 to 2035.

- The Solid segment dominates with a 63.6% market share in 2025.

- Calcium Silicate leads the market with a 39.5% share.

- Cereals and Grains hold the highest share at 39.1%.

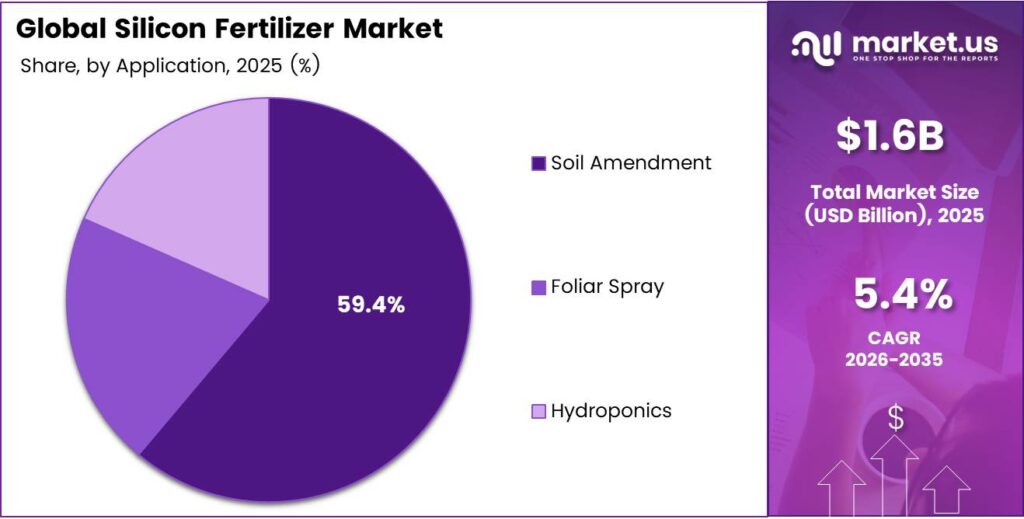

- The Soil Amendment segment accounts for 59.4% of the total market share.

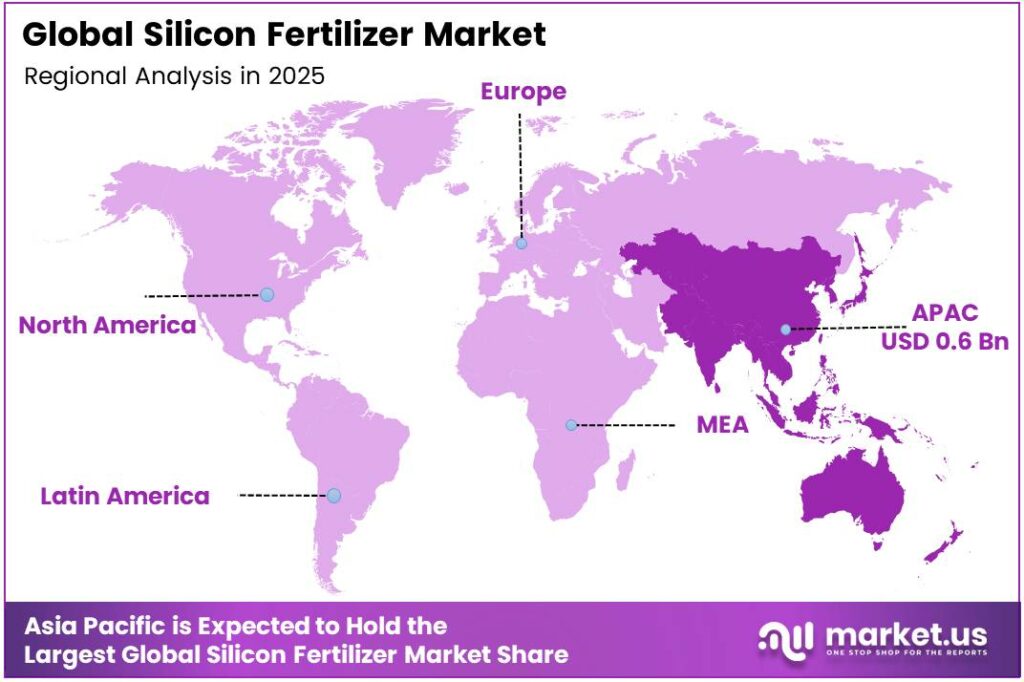

- Asia Pacific dominates the regional landscape with a 39.2% share, valued at USD 0.6 billion in 2025.

By Form Analysis

Solid dominates with 63.6% due to ease of storage, handling, and compatibility with conventional spreading equipment.

In 2025, Solid held a dominant market position in the By Form segment of the Silicon Fertilizer Market, with a 63.6% share. Solid silicon fertilizers offer practical advantages for large-scale field application. Farmers prefer granulated and powdered forms because they integrate seamlessly into existing blending and broadcasting infrastructure.

Liquid silicon fertilizers represent a growing segment driven by precision agriculture adoption. These formulations dissolve easily in water and support foliar spray and fertigation applications. Additionally, liquid forms enable faster nutrient uptake, making them preferred for high-value specialty crops and controlled-environment growing operations.

By Source Analysis

Calcium Silicate dominates with 39.5% due to its high silicon bioavailability, soil pH-buffering properties, and cost-effective production from industrial slag byproducts.

In 2025, Calcium Silicate held a dominant market position in the By Source segment of the Silicon Fertilizer Market, with a 39.5% share. Calcium silicate improves soil structure while simultaneously supplying silicon and calcium to crops. Its wide availability as a steel industry byproduct also keeps production costs competitive for farmers.

Potassium Silicate serves as a highly soluble silicon source suitable for foliar and fertigation use. It also supplies potassium, offering a dual-nutrient benefit. Moreover, potassium silicate products find strong uptake in greenhouse horticulture and fruit production systems that require precise nutrient management.

Sodium Silicate represents a widely available industrial silicate used in agriculture primarily as a soil conditioner. However, its high sodium content limits direct application rates in sensitive soils. Others in this segment include rice husk ash and alternative silicate minerals that serve regional niche markets in Asia and Latin America.

By Crop Type Analysis

Cereals and Grains dominate with 39.1% due to silicon’s proven ability to increase grain weight, reduce lodging, and protect against blast and fungal diseases.

In 2025, Cereals and Grains held a dominant market position in the By Crop Type segment of the Silicon Fertilizer Market, with a 39.1% share. Rice, wheat, and maize respond strongly to silicon supplementation. Silicon reduces water loss and improves light interception, directly boosting productivity in the world’s most essential food crops.

Fruits and Vegetables represent a fast-growing crop segment for silicon fertilizer adoption. Silicon strengthens fruit skin, extends shelf life, and improves resistance to post-harvest diseases. Consequently, growers of tomatoes, cucumbers, and berries increasingly integrate silicon into their nutrition programs to meet quality standards for export markets.

Sugar Crops benefit from silicon’s role in improving stalk strength and reducing pest attack in sugarcane. Oilseeds such as soybean and sunflower show improved drought tolerance with silicon applications. Others include plantation crops and specialty floriculture, where silicon supports structural integrity and disease resistance under intensive cultivation.

By Application Analysis

Soil Amendment dominates with 59.4% due to its ability to deliver sustained silicon release and restore long-term soil silicon pools depleted by intensive cropping.

In 2025, Soil Amendment held a dominant market position in the By Application segment of the Silicon Fertilizer Market, with a 59.4% share. Soil-applied silicon products improve overall soil health while correcting silicon deficiency at the root zone level. Farmers prefer this method for broad-acre field crops due to its simplicity and long-lasting effectiveness.

Foliar Spray application delivers silicon directly to plant leaves for rapid stress response. This method suits high-value crops facing acute pest pressure or drought conditions. Moreover, foliar silicon products are increasingly formulated for compatibility with existing pesticide and nutrient spray programs, reducing labor and operational costs.

Hydroponics and Controlled-Environment Agriculture represent a specialized but rapidly growing application segment. Silicon supplementation in nutrient solutions strengthens plant structures and reduces disease incidence in closed growing systems. Additionally, urban farming and vertical agriculture operations drive demand for soluble silicon formulations compatible with recirculating irrigation systems.

Key Market Segments

By Form

- Solid

- Liquid

By Source

- Calcium Silicate

- Potassium Silicate

- Sodium Silicate

- Others

By Crop Type

- Cereals and Grains

- Fruits and Vegetables

- Sugar Crops

- Oilseeds

- Others

By Application

- Soil Amendment

- Foliar Spray

- Hydroponics/Controlled-Environment

Emerging Trends

Liquid Silicate Formulations and Bio-Inoculants Reshape Silicon Fertilizer Innovation

Liquid potassium silicate formulations gain rapid traction among farmers using fertigation and controlled-environment systems. These products integrate directly into irrigation lines, reducing application labor. India imported $1.18 million of silicates from the Netherlands in 2024, confirming Europe’s role as a key supplier of advanced silicate inputs to emerging agricultural markets.

Scientists and agribusinesses increasingly explore silicon’s role in carbon sequestration through phytolith occlusion in soils. Silicon absorbed by plants eventually forms phytoliths that trap organic carbon in stable mineral forms. This carbon-locking function positions silicon fertilizers as dual-purpose tools for crop productivity improvement and climate-smart agriculture programs.

Multi-nutrient agro-mineral products combining silicon with calcium, magnesium, and micronutrients are gaining commercial momentum. These blended products offer farmers a simplified approach to correcting multiple soil deficiencies simultaneously. Moreover, microbial silicon solubilizers now complement bulk silicate applications by converting soil-bound silicon into plant-available forms, improving overall fertilizer efficiency.

Drivers

Rising Food Security Demands and Soil Depletion Drive Silicon Fertilizer Adoption Globally

Global population growth creates urgent pressure to raise crop yields per hectare without expanding agricultural land. Farmers and governments seek proven solutions to close yield gaps sustainably. Silicon fertilizers address this challenge directly by improving crop resistance to drought, pests, and salinity while reducing reliance on costly synthetic chemical inputs.

- Decades of intensive monocropping have severely depleted plant-available silicon in agricultural soils worldwide. Continuous crop harvests remove silicon without adequate replacement through conventional fertilization programs. Tata Chemicals booked ₹80 crore of FY2024-25 specialty-products revenue in Europe alone, reflecting strong demand for silicate-linked agricultural materials across mature markets.

Regulatory bodies in multiple countries now push farmers to reduce reliance on synthetic pesticides and chemical fertilizers. Silicon offers a nature-based alternative that strengthens plant defenses without harmful residues. Additionally, the proven efficacy of silicon against both fungal diseases and insect pests makes it an attractive addition to integrated crop protection strategies in regulated agricultural markets.

Restraints

Knowledge Gaps and Absent Regulatory Standards Slow Silicon Fertilizer Market Penetration

A significant knowledge gap exists among smallholder and subsistence farmers regarding silicon fertilizer benefits and correct application protocols. Many growers remain unaware of silicon’s agronomic role because traditional soil testing rarely measures plant-available silicon levels. This lack of technical awareness limits adoption even in regions where soils show measurable silicon deficiency.

The absence of standardized regulatory frameworks for silicon fertilizer classification creates significant market uncertainty. Different countries apply inconsistent definitions, quality standards, and registration requirements to silicon-based soil products. REC Silicon ended 2024 with 466 permanent employees, down from 495 in 2023, reflecting broader workforce contractions in the silicon materials supply chain that affect downstream agricultural input availability.

Product quality variation across different silicon fertilizer manufacturers further complicates farmer decision-making. Without harmonized quality certifications, buyers cannot easily compare efficacy between competing brands. Therefore, building farmer trust requires substantial investment in field demonstration programs and agronomic education, adding cost and time to market development efforts in price-sensitive agricultural regions.

Growth Factors

Nano-Formulations, Specialty Crops, and Circular Economy Models Accelerate Silicon Fertilizer Expansion

Manufacturers develop novel granulated and nano-formulated silicon products designed for precision agriculture equipment and fertilizer blending systems. These advanced formulations improve silicon release precision and nutrient uptake efficiency at the field level. Advance Agrolife Limited reported revenue from operations of ₹5,022.60 million in FY2024-25, up from ₹4,558.99 million in FY2023-24, demonstrating that agro-input platforms expanding crop-enhancement distribution generate measurable and sustained revenue growth.

Strategic expansion into high-value specialty crop sectors creates significant revenue opportunities for silicon fertilizer producers. Viticulture, horticulture, and floriculture producers show a strong willingness to pay premium prices for silicon products that improve fruit quality and extend shelf life. Advance Agrolife maintained a domestic presence across 19 states and 2 union territories with exports to 7 international markets, showing how agro-input companies scale geographically to capture specialty crop demand.

Public-private partnerships integrate silicon enrichment into government-subsidized soil health programs across Asia and Africa. These collaborations reduce farmer cost barriers and accelerate technology adoption at scale. Additionally, the extraction of silicon from waste streams such as rice husk ash and aluminum slag creates a circular economy model that lowers raw material costs and strengthens the sustainability credentials of silicon fertilizer products.

Regional Analysis

Asia Pacific Dominates the Silicon Fertilizer Market with a Market Share of 39.2%, Valued at USD 0.6 Billion

Asia Pacific leads the global silicon fertilizer market with a 39.2% share valued at USD 0.6 billion in 2025. The region’s dominance reflects its large rice cultivation base, where silicon plays a critical agronomic role in blast resistance and yield improvement. China, India, Japan, and South Korea drive the majority of regional demand. China is the largest disclosed supplier to India in this silicon-chemicals trade lane.

Europe maintains a strong position in the global silicon fertilizer market, supported by advanced agricultural practices and strict sustainability regulations. The Netherlands and Germany rank among the top sodium silicate importers globally, with the Netherlands importing. Tata Chemicals booked specialty-products revenue in Europe in FY2024-25, confirming active commercial engagement from major silicate suppliers in the region.

Latin America emerges as a high-potential growth market for silicon fertilizers, driven by large-scale sugarcane, soybean, and citrus cultivation. Brazil leads regional adoption due to its massive agricultural sector and ongoing soil health restoration programs. Indicating that global silicate suppliers increasingly prioritize the Latin American agricultural input market.

The Middle East and Africa region shows growing interest in silicon fertilizers as governments address food security challenges under arid and semi-arid conditions. Silicon improves crop tolerance to salinity and heat stress, making it directly relevant to farming systems across the GCC and Sub-Saharan Africa. Additionally, confirming that major silicate suppliers recognize and actively pursue the region’s emerging agricultural demand.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

PQ Corporation stands as a global leader in silicate chemistry with a broad portfolio of sodium and potassium silicate solutions serving agricultural and industrial markets. The company applies deep technical expertise in silicate formulation to support growers seeking high-performance soil amendment products. PQ Corporation’s established manufacturing network and R&D capabilities position it as a critical supplier to silicon fertilizer formulators worldwide.

MaxSil Pty Ltd. specializes in agricultural silicon solutions designed specifically for Australian and export markets. The company focuses on developing bioavailable silicon products proven effective across a range of soil types and crop categories. MaxSil’s agronomic approach combines scientific field research with practical product development, enabling it to offer growers evidence-based silicon nutrition programs that improve yields and crop quality.

Denka Corporation Ltd brings advanced Japanese materials science expertise to the silicon fertilizer sector. The company produces high-purity calcium silicate products used widely in paddy rice cultivation across East Asia. Denka’s strong technical reputation and quality standards make it a preferred supplier in markets where crop performance consistency and raw material reliability are essential for commercial farming operations.

Harsco Environmental operates at the intersection of industrial waste valorization and agricultural input supply. The company recovers and processes steelmaking slag into high-quality calcium silicate soil amendments. Harsco’s circular economy model delivers cost-competitive silicon fertilizer products while simultaneously addressing industrial byproduct management challenges, giving it a strong sustainability narrative that resonates with environmentally conscious buyers and regulators.

Top Key Players in the Market

- PQ Corporation

- MaxSil Pty Ltd.

- Denka Corporation Ltd

- Harsco Environmental

- Guangzhou Silicon Fertilizer

- Agripower Australia Ltd.

- Haifa Group International Chemical Co., Ltd.

- Chewachem Company Limited

- Plant Tuff, Inc.

- Aiva Limited

Recent Developments

- In 2025, MaxSil is actively seeking investment through the growAG platform. They are looking for a cornerstone investor involved in the global manufacture and distribution of agricultural inputs, a large agricultural conglomerate, or a company involved in waste management.

- In 2025, Harsco Environmental was named Outstanding Institutional Partner of the Year by Emater-MG (Technical Assistance and Rural Extension Company of the State of Minas Gerais) for its contribution to family farming through the AgroSilício donation program.

Report Scope

Report Features Description Market Value (2025) USD 1.6 Billion Forecast Revenue (2035) USD 2.7 Billion CAGR (2026-2035) 5.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Form (Solid, Liquid), By Source (Calcium Silicate, Potassium Silicate, Sodium Silicate, Others), By Crop Type (Cereals and Grains, Fruits and Vegetables, Sugar Crops, Oilseeds, Others), By Application (Soil Amendment, Foliar Spray, Hydroponics/Controlled-Environment) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape PQ Corporation, MaxSil Pty Ltd., Denka Corporation Ltd, Harsco Environmental, Guangzhou Silicon Fertilizer, Agripower Australia Ltd., Haifa Group International Chemical Co., Ltd., Chewachem Company Limited, Plant Tuff, Inc., Aiva Limited Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Silicon Fertilizer MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Silicon Fertilizer MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- PQ Corporation

- MaxSil Pty Ltd.

- Denka Corporation Ltd

- Harsco Environmental

- Guangzhou Silicon Fertilizer

- Agripower Australia Ltd.

- Haifa Group International Chemical Co., Ltd.

- Chewachem Company Limited

- Plant Tuff, Inc.

- Aiva Limited

Our Clients

- 181185

- March 2026