Quick Navigation

Report Overview

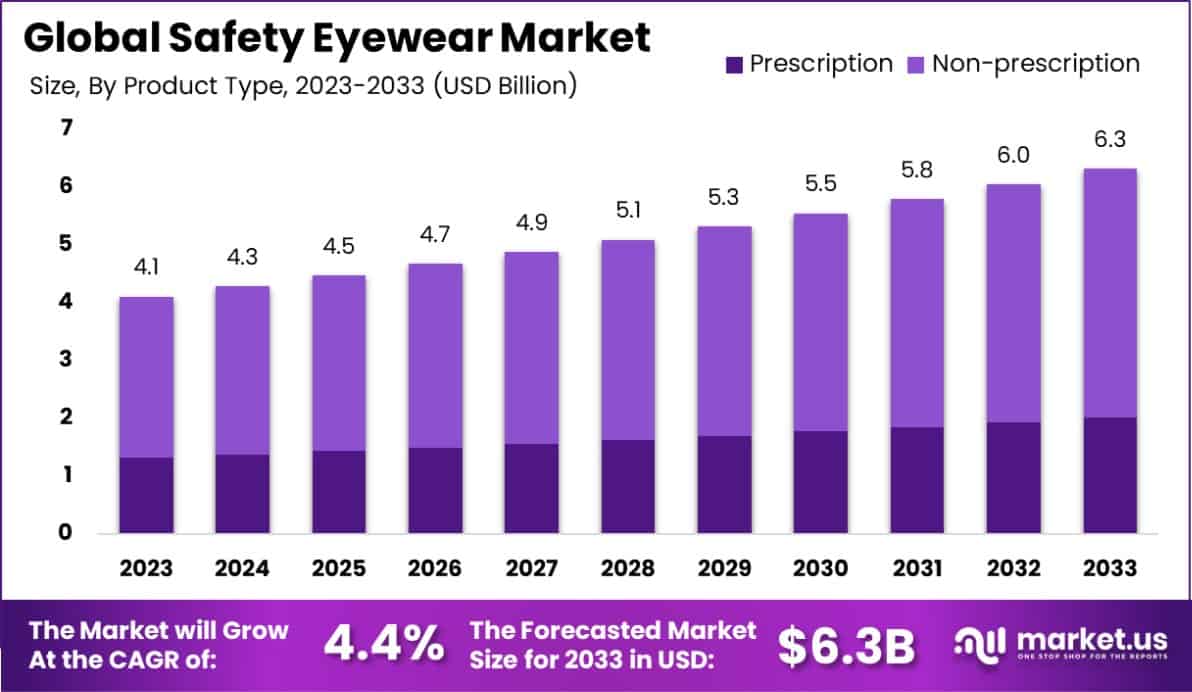

The Global Safety Eyewear Market is expected to be worth around USD 6.3 billion by 2033, up from USD 4.1 billion in 2023, growing at a CAGR of 4.4% during the forecast period from 2024 to 2033.

Safety eyewear consists of protective glasses or goggles designed to shield the eyes from hazardous materials, particles, or light exposures that occur in various work environments. These products are integral to industries where eye safety is a critical concern, including construction, manufacturing, and laboratory work.

The safety eyewear market encompasses the production, distribution, and sale of safety glasses and goggles. It is influenced by regulatory standards mandating eye protection in workplaces, technological advancements in eyewear design, and awareness of workplace safety.

Growth factors for the safety eyewear market include increasing awareness of workplace safety, stringent occupational health regulations, and technological advancements in eyewear materials and coatings. The demand for safety eyewear is driven by the expansion of industries with hazardous working conditions and the global emphasis on labor safety standards.

Opportunities within the market are expanding through innovations such as anti-fog, anti-scratch, and ultraviolet protection features, along with the rising adoption of prescription safety eyewear.

The safety eyewear market is increasingly recognized as a critical component of workplace safety protocols, driven by stringent regulatory frameworks and growing industrial activities across various sectors. The market’s relevance is underscored by the substantial need to protect workers in environments prone to eye hazards.

In 2020, despite a noticeable 15.6% decrease in eye-related injuries and illnesses from the previous year, there were still 18,510 cases reported that necessitated at least one day away from work, indicating a persistent demand for effective safety solutions. Notably, the majority of these incidents, approximately 64.7%, were due to contact with objects or equipment.

The data highlights the urgent need for robust safety eyewear that can mitigate risks from physical objects and other hazardous exposures, such as harmful substances and workplace violence, which collectively contribute to significant injury statistics.

Key Takeaways

- The Global Safety Eyewear Market is expected to be worth around USD 6.3 billion by 2033, up from USD 4.1 billion in 2023, growing at a CAGR of 4.4% during the forecast period from 2024 to 2033.

- In 2023, Non-prescription held a dominant market position in the By Product Type segment of the Safety Eyewear Market, with a 68.2% share.

- In 2023, Industrial Manufacturing held a dominant market position in the application segment of the Safety Eyewear Market, with a 33.1% share.

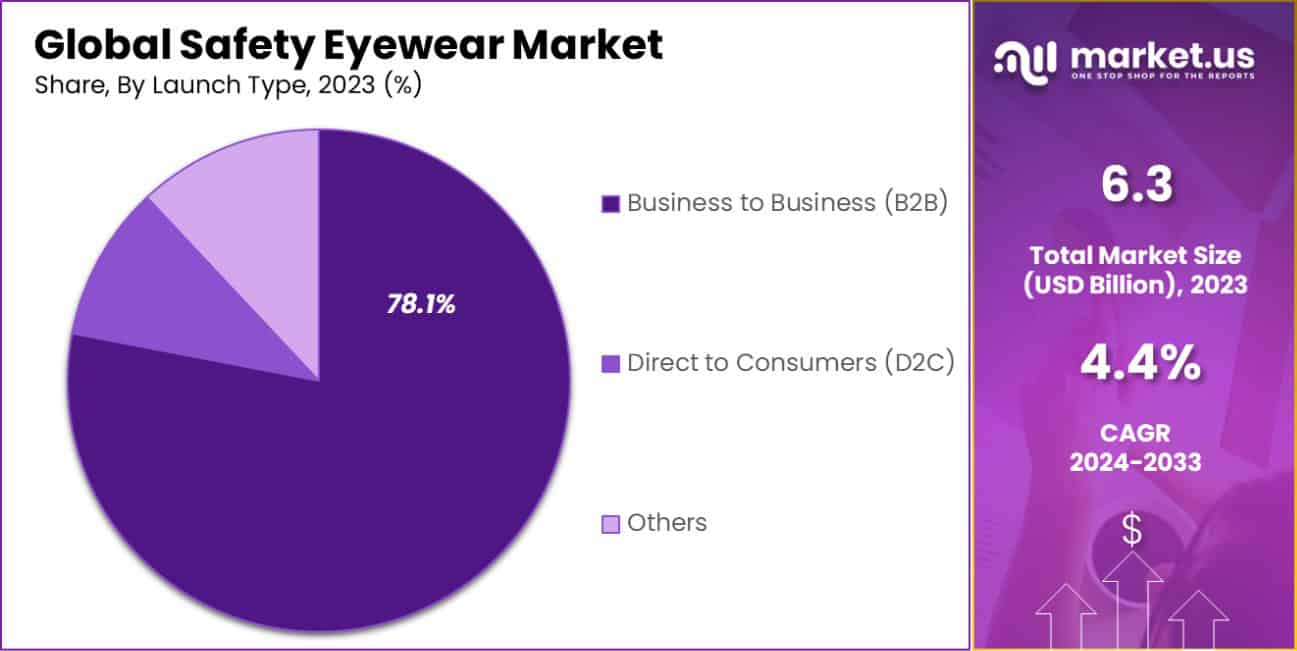

- In 2023, business-to-business (B2B) held a dominant market position in the By Distribution Channel segment of the Safety Eyewear Market, with a 78.1% share.

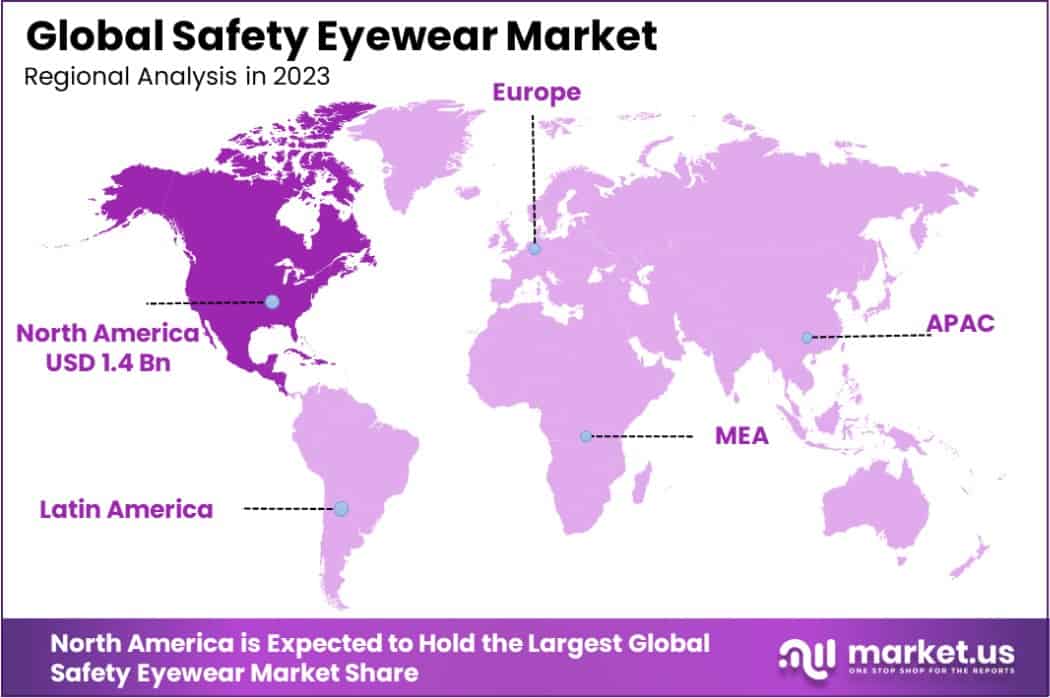

- North America dominated a 35.9% market share in 2023 and held USD 1.4 Billion in revenue from the Safety Eyewear Market.

By Product Type Analysis

In 2023, Non-prescription safety eyewear held a dominant market position in the By Product Type segment of the Safety Eyewear Market, accounting for a substantial 68.2% share. This segment’s prominence is largely due to its widespread adoption across various industries where quick and easy access to eye protection is essential, such as in manufacturing, construction, and chemical processing.

Non-prescription eyewear offers the advantage of immediate use without the need for customization, making it a practical choice for companies seeking to equip large workforces with protective gear efficiently.

On the other hand, the Prescription segment, though smaller, plays a crucial role in catering to the specific needs of workers who require vision correction combined with safety features. This segment is driven by advancements in personalized protective eyewear and is increasingly seen as an essential offering by employers aiming to enhance safety and vision accuracy for their employees.

Despite its lower market share, the demand for prescription safety eyewear is expected to grow, propelled by an aging workforce and increasing awareness of the benefits of tailored safety solutions. Together, these product segments underline the diverse requirements and opportunities within the Safety Eyewear Market, reflecting varying workplace needs and employee preferences.

By Application Analysis

In 2023, Industrial Manufacturing held a dominant market position in the By Application segment of the Safety Eyewear Market, with a 33.1% share. This sector’s leadership stems from the extensive need for eye protection against a myriad of hazards such as flying debris, splashes, and intense light, which are commonplace in manufacturing environments.

The consistent enforcement of stringent safety regulations across the globe has further cemented the demand for safety eyewear in this sector.

The other key sectors in this market include Oil & Gas, Construction, Mining, and Military, each with significant shares due to their specific safety requirements. For instance, the Construction and Mining industries require robust safety eyewear to protect against dust, particles, and chemical splashes, while the Oil & Gas sector needs specialized eyewear to prevent injuries from oil spills and gaseous emissions.

The Military segment also demands high-performance eyewear to safeguard against potential ballistic threats and environmental elements. Each of these sectors contributes to the dynamic expansion of the safety eyewear market, driven by industry-specific demands and ongoing advancements in eyewear technology designed to meet these diverse and challenging environments.

By Distribution Channel Analysis

In 2023, business-to-business (B2B) held a dominant market position in the By Distribution Channel segment of the Safety Eyewear Market, capturing a significant 78.1% share. This predominance is attributed to the established supply chains and procurement practices within industries where safety eyewear is mandated by occupational safety standards.

Large-scale enterprises and various industrial sectors prefer B2B transactions for bulk purchasing, benefiting from economies of scale and streamlined logistics.

Conversely, the Direct to Consumers (D2C) and Other segments cater to individual consumers and smaller business entities, accounting for the remainder of the market share. The D2C channel has been gradually expanding with the rise of e-commerce platforms that offer a diverse range of safety eyewear directly to end-users, promoting convenience and customization.

This channel is particularly appealing to freelancers, remote workers, and small businesses that might not have the same bulk needs as larger corporations but still prioritize workplace safety.

Each distribution channel reflects the evolving landscape of market demand and consumer behavior, with B2B remaining the cornerstone due to its integral role in fulfilling the extensive requirements of large-scale industrial consumers.

Key Market Segments

By Product Type

- Prescription

- Non-prescription

By Application

- Oil & Gas

- Construction

- Mining

- Industrial Manufacturing

- Military

By Distribution Channel

- Business to Business (B2B)

- Direct to Consumers (D2C)

- Others

Drivers

Safety Eyewear Market Growth Drivers

The Safety Eyewear Market is primarily driven by increasing regulations and awareness around workplace safety. Governments worldwide are implementing stricter safety standards to protect workers from eye injuries, which directly boosts the demand for safety eyewear across various industries such as construction, manufacturing, and mining.

Additionally, the rising awareness among companies about the financial and ethical implications of workplace injuries is prompting more businesses to invest in reliable safety equipment, including eyewear.

Technological advancements that improve the comfort and functionality of safety glasses also contribute to market growth, making it easier for workers to wear protective eyewear throughout their shifts without discomfort.

This combination of regulatory pressure, corporate responsibility, and product innovation is continuously expanding the market for safety eyewear.

Restraint

Challenges Facing Safety Eyewear Market

A significant restraint in the safety eyewear market is the issue of product discomfort and lack of user compliance. Despite technological advancements, many workers find safety eyewear uncomfortable for prolonged use, which can lead to reduced compliance with safety protocols.

This non-compliance is especially problematic in industries that require long hours in varying environmental conditions, where discomfort can decrease the likelihood of consistent eyewear usage.

Additionally, the economic burden of updating or customizing safety eyewear to meet individual needs can be a barrier for small to medium-sized enterprises (SMEs), hindering market penetration in these segments.

These factors collectively pose challenges to the widespread adoption and effectiveness of safety eyewear, impacting market growth negatively.

Opportunities

Expanding Opportunities in Safety Eyewear

The safety eyewear market presents numerous growth opportunities, particularly through technological innovations and emerging markets. As safety eyewear integrates more advanced materials and features like anti-fog, anti-scratch, and enhanced UV protection, consumer demand is likely to increase.

These innovations not only improve the functionality and comfort of eyewear but also boost its appeal across various industry sectors. Additionally, emerging markets in Asia and Africa, where industrial and construction sectors are expanding rapidly, offer new avenues for market penetration.

The growing awareness of workplace safety in these regions further enhances the potential for safety eyewear adoption, creating promising opportunities for manufacturers and distributors to expand their global footprint and meet the evolving needs of a broader customer base.

Challenges

Key Challenges in the Safety Eyewear Market

The safety eyewear market faces several challenges that could hinder its growth. One major challenge is the intense competition among manufacturers, which can lead to price wars and reduced profitability. Additionally, the variability in quality standards globally makes it difficult for manufacturers to maintain consistent product standards across different markets.

Compliance with diverse international safety regulations also imposes significant costs and complexities in design and manufacturing. Moreover, the prevalence of counterfeit products in the market poses a threat to both safety and brand reputation, potentially leading to decreased trust and demand for authentic safety eyewear products.

These challenges require manufacturers to strategically navigate market dynamics, regulatory environments, and competition to sustain growth and ensure the effectiveness of their safety solutions.

Growth Factors

Driving Forces in the Safety Eyewear Market

The growth of the safety eyewear market is largely propelled by the increasing enforcement of stringent workplace safety regulations worldwide. As governments intensify their focus on reducing occupational hazards, industries are mandated to equip their workers with appropriate safety gear, including safety eyewear.

This regulatory push is complemented by growing awareness among corporations about the importance of workplace safety, which not only helps protect employees but also reduces costs related to workplace accidents. Additionally, advancements in eyewear technology that enhance comfort and functionality are making safety glasses more appealing to users.

These factors, coupled with the expansion of industries where eye protection is critical, such as construction and manufacturing, continue to drive demand and encourage innovations within the safety eyewear market.

Emerging Trends

Emerging Trends in Safety Eyewear

Emerging trends in the safety eyewear market are shaping its future growth and innovation. One significant trend is the integration of smart technology into safety glasses, incorporating features like augmented reality (AR), which provides real-time data and enhances worker efficiency and safety.

Another trend is the increasing customization of safety eyewear to cater to individual preferences and requirements, enhancing comfort and increasing user compliance. There’s also a growing emphasis on stylish designs that appeal to a broader demographic, ensuring that users are more willing to wear safety eyewear as part of their regular attire.

Additionally, the market is seeing a rise in eco-friendly materials, responding to the increasing consumer demand for sustainable products. These trends highlight the evolving nature of safety eyewear, making it more effective, user-friendly, and aligned with modern workplace needs and environmental concerns.

Regional Analysis

The Safety Eyewear Market is segmented into several key regions: North America, Europe, Asia Pacific, Middle East & Africa, and Latin America. North America is the dominating region, holding 35.9% of the market share and valued at USD 1.4 billion, driven by stringent regulatory standards and a high level of awareness regarding workplace safety.

Europe follows closely, with a strong emphasis on occupational health standards across industries, coupled with advanced product offerings by leading manufacturers.

The Asia Pacific region presents significant growth potential due to rapid industrialization and increasing investments in the construction and smart manufacturing sectors, especially in emerging economies like China and India. Meanwhile, the Middle East & Africa region is experiencing gradual growth, supported by developing infrastructure and the oil & gas industry’s evolving safety practices.

Latin America, though smaller in comparison, is seeing an uptick in market demand fueled by improving regulatory landscapes and economic stabilization. Each region reflects unique market dynamics influenced by local regulations, industry presence, and technological advancements, contributing to the global expansion of the safety eyewear market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2023, the global Safety Eyewear Market continues to be shaped significantly by key players such as Kimberly-Clark Corp, MCR Safety, and Honeywell International Inc., each bringing unique strengths and strategic initiatives to the forefront of the industry.

Kimberly-Clark Corp, traditionally known for its strong presence in the personal care and professional industry sectors, leverages its extensive distribution networks and brand reputation to enhance its position in the safety eyewear market.

The company focuses on innovation and user comfort, developing eyewear that meets rigorous safety standards while ensuring wearer comfort, which is critical for user compliance.

MCR Safety stands out for its specialization in personal protective equipment, including safety eyewear. Known for its durable and reliable products, MCR Safety emphasizes customization and technical advancements in its eyewear solutions.

This approach caters effectively to specific industry needs, such as resistance to high impact and exposure to chemicals, making it a preferred choice for industries with harsh working conditions.

Honeywell International Inc. is a major player with a global footprint, known for integrating cutting-edge technology into its safety products. Honeywell’s safety eyewear is often equipped with advanced materials and smart technology features, such as anti-fog, anti-glare, and ultraviolet protection, catering to a broad range of industrial applications.

Their commitment to research and development continually sets industry standards higher, influencing market trends and consumer expectations.

Collectively, these companies not only drive competitive dynamics but also contribute to the market’s growth by addressing critical safety needs across various industries, enhancing user safety, and compliance through continuous product innovation and improvement.

Top Key Players in the Market

- Kimberly-Clark Corp

- MCR Safety

- Honeywell International Inc.

- UVEX Winter Holding GmbH & Co

- MEDOP SA

- 3M Company

- BOLLÉ Safety

- Radians, Inc

- Pyramex Safety Products LLC

- Other Key Players

Recent Developments

- In March 2024, 3M Company expanded its safety eyewear portfolio by integrating advanced UV protection technology. This new feature helps protect users from harmful ultraviolet rays, making the eyewear ideal for outdoor working conditions.

- In February 2024, MEDOP SA introduced a range of lightweight safety eyewear. These new products are crafted to offer superior protection without compromising comfort, aiming to increase wearability for longer periods.

- In January 2024, UVEX Winter Holding GmbH & Co. KG, a leader in protective gear, launched a new line of anti-fog safety goggles. These goggles are designed to provide clearer vision in humid and cold environments, enhancing safety and comfort for users.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 4.1 Billion |

| Forecast Revenue (2033) | USD 6.3 Billion |

| CAGR (2024-2033) | 4.4% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type(Prescription, Non-prescription), By Application(Oil & Gas, Construction, Mining, Industrial Manufacturing, Military), By Distribution Channel(Business to Business (B2B), Direct to Consumers (D2C), Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Kimberly-Clark Corp, MCR Safety, Honeywell International Inc., UVEX Winter Holding GmbH & Co, MEDOP SA, 3M Company, BOLLÉ Safety, Radians, Inc, Pyramex Safety Products LLC, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |