Quick Navigation

Report Overview

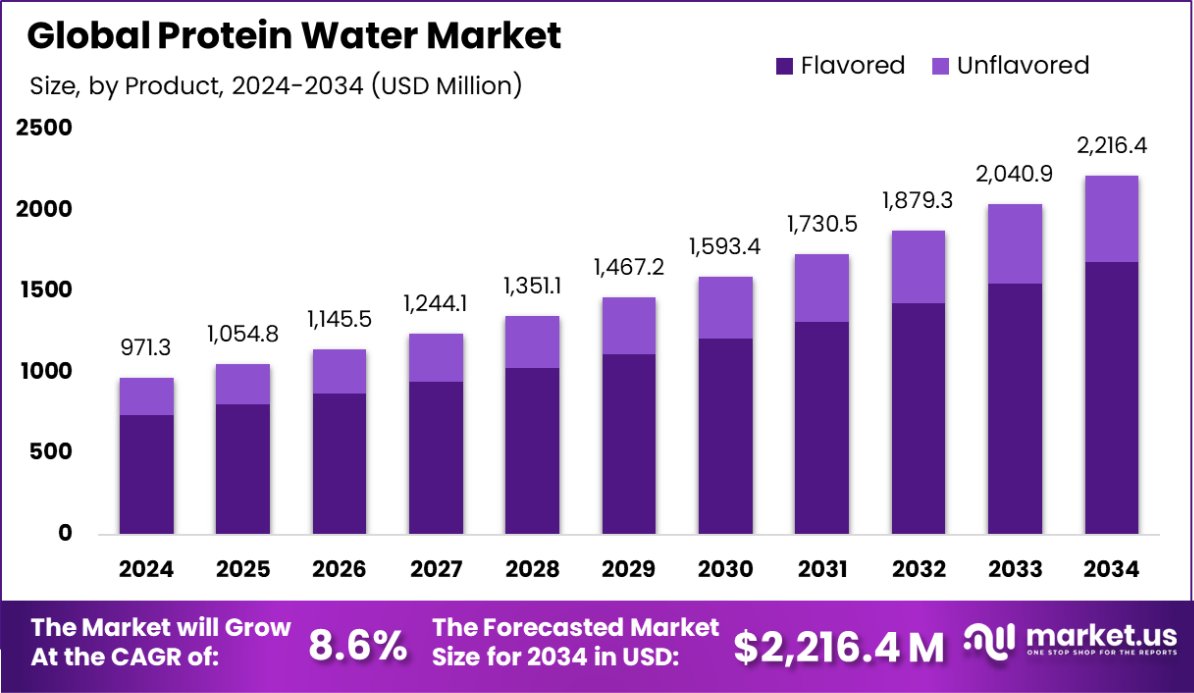

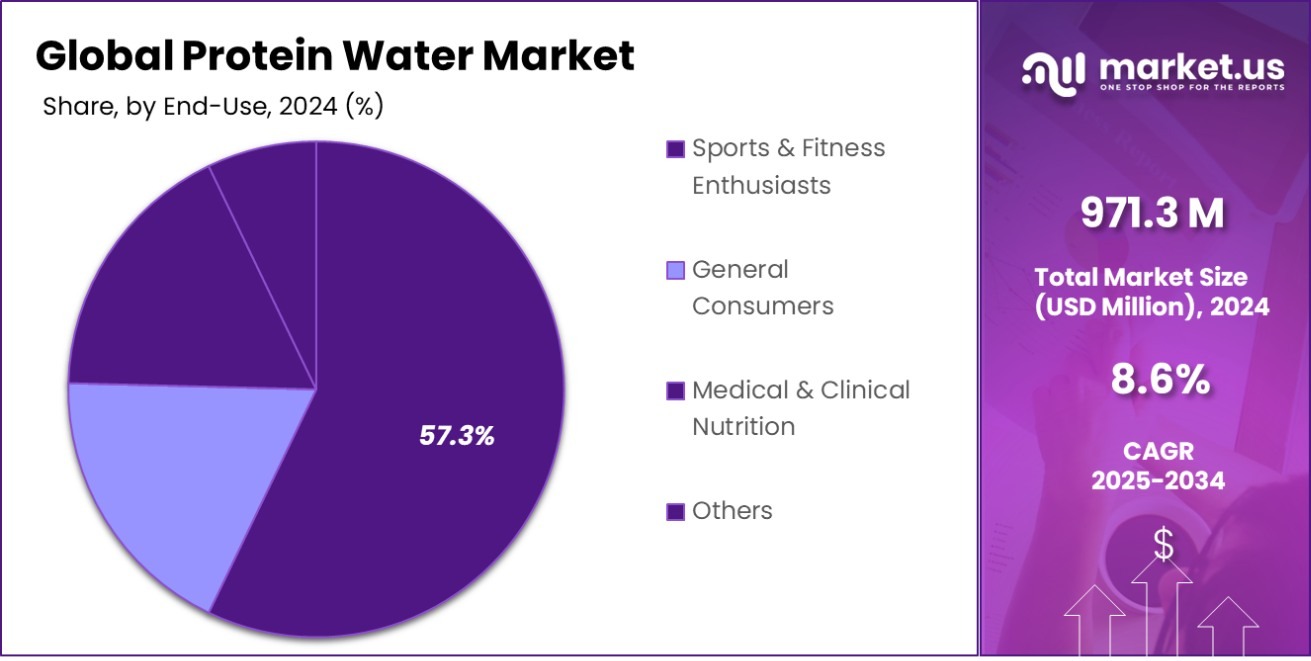

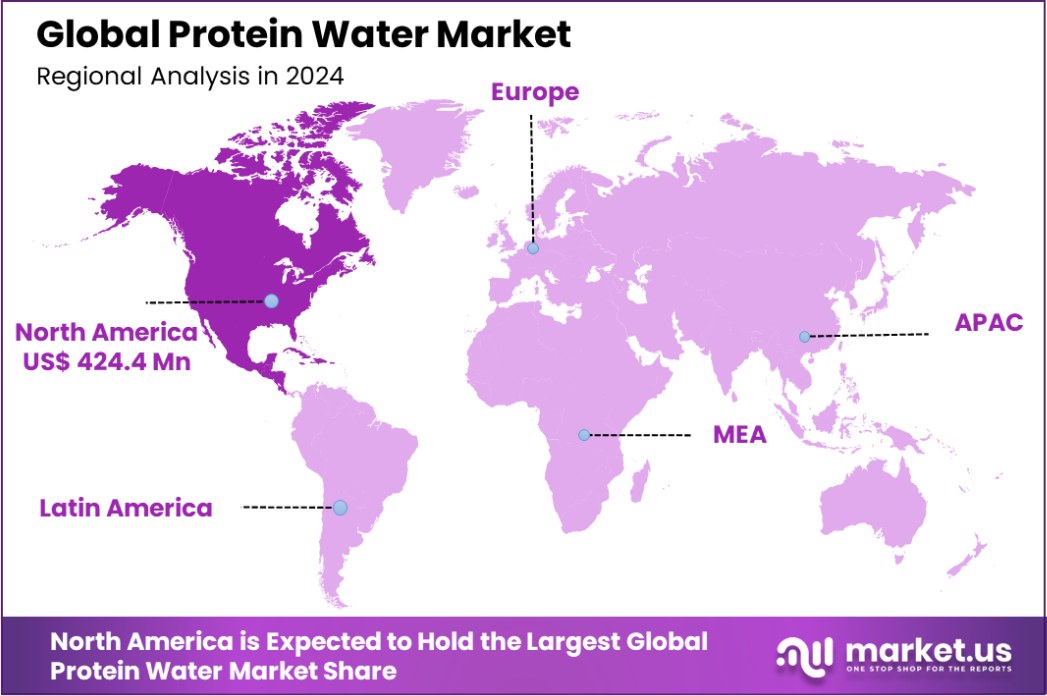

Global Protein Water Market is expected to be worth around USD 2,216.4 Million by 2034, up from USD 971.3 Million in 2024, and grow at a CAGR of 8.6% from 2025 to 2034. North America leads the Protein Water Market with 43.7%, USD 424.4 million.

Protein Water is a type of beverage that combines water with high-quality protein, offering a refreshing and hydrating way to supplement protein intake. It is typically low in calories and sugar, making it a popular option for fitness enthusiasts, athletes, and health-conscious individuals looking to support muscle recovery and maintain a balanced diet. Protein water is often formulated with whey or plant-based proteins and is available in various flavors.

The Protein Water Market has been experiencing steady growth as consumers increasingly prioritize health and wellness. The demand for functional beverages, including those with added protein, has surged as more individuals seek convenient ways to meet their nutritional needs. Protein water is seen as a healthier alternative to traditional sugary drinks, and its appeal extends beyond fitness circles, attracting people interested in weight management and overall well-being.

Growth Factors in the protein water market are driven by the rising awareness of the importance of protein in daily nutrition, along with the increasing preference for low-calorie, high-protein beverages. As consumers become more health-conscious, they are opting for protein water to support muscle repair, weight loss, and overall health.

Demand for protein water is further fueled by the growing trend of fitness culture, as athletes and gym-goers seek easy-to-consume sources of protein. The expanding availability of these beverages in retail outlets and online platforms has also contributed to their increasing popularity.

Opportunities in the protein water market lie in product innovation, such as the development of plant-based protein variants to cater to vegan and lactose-intolerant consumers. Additionally, targeting emerging markets and collaborating with health and fitness influencers for marketing could further boost demand.

De Novo Foodlabs, a biotech startup focused on developing animal-free protein, has raised a $1.5 million seed investment round led by Joyful VC. This funding increases the company’s total investment to $4 million, supporting their efforts in sustainable protein innovation.

Key Takeaways

- Global Protein Water Market is expected to be worth around USD 2,216.4 Million by 2034, up from USD 971.3 Million in 2024, and grow at a CAGR of 8.6% from 2025 to 2034.

- The flavored segment dominates the protein water market, accounting for 76.8% of the total market share.

- Whey protein leads as the most popular source, representing 48.2% of protein water consumption.

- Sports and fitness enthusiasts are the primary consumers, contributing 57.3% of the protein water market.

- Hypermarkets and supermarkets are the leading distribution channels, capturing 43.4% of protein water sales.

- North America dominates the Protein Water Market with a 43.7% share, valued at USD 424.4 million.

By Product Analysis

The Protein Water Market is dominated by flavored products, accounting for 76.8%.

In 2024, Flavored held a dominant market position in the By Product segment of the Protein Water Market, with a 76.8% share. This significant share reflects the growing consumer preference for protein water that offers both nutritional benefits and an enjoyable taste.

Flavored protein waters are popular among consumers due to their ability to provide a variety of tastes without compromising on the essential protein content. This trend is particularly prominent among fitness enthusiasts and health-conscious individuals who seek functional beverages that also satisfy taste preferences.

The popularity of flavored protein water can be attributed to its appeal as a convenient and refreshing alternative to traditional protein shakes or powders. As consumers become more discerning about the taste and experience of protein-based beverages, companies have increasingly focused on offering a range of flavors to cater to different preferences. This has driven the demand for flavored variants, which in turn has supported their dominant market position.

Moreover, the rise in health-conscious consumer behavior, coupled with the growing demand for on-the-go nutrition, has further propelled the adoption of flavored protein water. As innovation continues in flavor offerings, the segment is expected to maintain its stronghold in the coming years, with the development of new and exotic flavors to meet evolving consumer tastes.

By Source Analysis

Whey protein holds the largest market share, contributing 48.2% of the segment.

In 2024, Whey Protein held a dominant market position in the By Source segment of the Protein Water Market, with a 48.2% share. Whey protein’s market leadership is driven by its well-established benefits in the fitness and wellness industry, where it is regarded as a complete protein with all nine essential amino acids. This makes it particularly popular among athletes, bodybuilders, and individuals seeking efficient muscle recovery post-workout.

Whey protein is highly digestible and quickly absorbed by the body, which adds to its appeal as an ideal protein source in functional beverages like protein water. The presence of whey protein in protein water also aligns with the growing demand for convenient, high-protein products that are easy to consume on the go, making it an attractive choice for busy, health-conscious consumers.

The dominance of whey protein is further supported by its broad consumer acceptance and its proven track record in supporting muscle growth, fat loss, and overall health. As consumer awareness regarding the importance of protein intake continues to rise, whey protein’s established reputation is likely to maintain its leading position in the market.

Additionally, ongoing product innovations, such as flavor enhancements and the development of more specialized formulations, are expected to drive further growth in this segment.

By End-Use Analysis

Sports and fitness enthusiasts represent the primary consumers, comprising 57.3% of sales.

In 2024, Sports and Fitness Enthusiasts held a dominant market position in the By End-Use segment of the Protein Water Market, with a 57.3% share. This segment’s significant share is driven by the increasing demand for protein-enriched beverages among athletes and individuals who regularly engage in physical activities. Protein water offers a convenient and effective way for this demographic to meet their daily protein requirements, particularly post-workout, where muscle recovery and repair are essential.

The appeal of protein water to sports and fitness enthusiasts stems from its quick absorption and hydration properties, offering a dual benefit of protein intake and fluid replenishment. As exercise routines become more intense and varied, there is an escalating need for functional beverages that not only support muscle growth but also promote faster recovery. The growing popularity of gym culture and fitness-focused lifestyles further fuels the demand for these products.

Additionally, sports and fitness enthusiasts are increasingly seeking low-calorie, low-sugar alternatives to traditional protein shakes and smoothies, making protein water a preferred choice. The strong market position of this segment is expected to persist, with product innovations and flavor variations catering to the evolving needs of active consumers, ensuring continued growth in the coming years.

By Distribution Channel Analysis

Hypermarkets and supermarkets remain key distribution channels, controlling 43.4% of the market share.

In 2024, Hypermarkets and Supermarkets held a dominant market position in the By Distribution Channel segment of the Protein Water Market, with a 43.4% share. This substantial share reflects the convenience and accessibility that large retail chains offer to consumers seeking protein water. Hypermarkets and supermarkets are key players in the distribution of functional beverages, as they provide wide-reaching product availability and a convenient shopping experience for health-conscious consumers.

The dominance of this distribution channel can be attributed to the extensive reach of hypermarkets and supermarkets, which are frequented by a broad consumer base, including both fitness enthusiasts and general consumers looking to incorporate more protein into their diet. The physical presence of these stores allows customers to easily browse a range of protein water options, compare prices, and make informed purchasing decisions on the spot.

Furthermore, promotional activities and in-store placements, such as dedicated health beverage aisles or discounted bundles, enhance the visibility of protein water products, driving further sales. As consumers continue to prioritize health and wellness, hypermarkets and supermarkets are expected to maintain a stronghold in the market, with ongoing efforts to expand product offerings and cater to growing consumer demand for convenient, nutritious beverages.

Key Market Segments

By Product

- Flavored

- Unflavored

By Source

- Whey Protein

- Collagen Protein

- Plant-Based Protein

- Others

By End-Use

- Sports and Fitness Enthusiasts

- General Consumers

- Medical and Clinical Nutrition

- Others

By Distribution Channel

- Hypermarkets and Supermarkets

- Convenience Stores

- Online

- Others

Driving Factors

Increasing Health Consciousness Drives Protein Water Demand

One of the key driving factors in the Protein Water Market is the rising health consciousness among consumers. As people become more aware of the importance of maintaining a balanced diet and staying fit, the demand for products that support these goals is growing. Protein water, known for its high protein content and low-calorie, low-sugar profile, is seen as a healthy alternative to sugary beverages like sodas and juices.

This trend is particularly noticeable among fitness enthusiasts, athletes, and individuals pursuing weight management or muscle recovery goals. The convenience of protein water also appeals to busy consumers looking for an easy way to incorporate additional protein into their diet, further boosting its popularity and market growth.

Restraining Factors

High Cost Limits Wider Adoption of Protein Water

A significant restraining factor for the Protein Water Market is the high cost associated with these products. Compared to traditional beverages like bottled water or regular sports drinks, protein water tends to be more expensive due to its specialized formulation and the premium ingredients used, such as whey or plant-based proteins. For many consumers, particularly those on a budget, this higher price point can make protein water less accessible, limiting its widespread adoption.

While health-conscious individuals may prioritize the nutritional benefits, the cost can still deter potential buyers, especially in emerging markets where price sensitivity is higher. To address this challenge, manufacturers may need to find ways to reduce production costs or offer more affordable options without compromising quality.

Growth Opportunity

Expanding Plant-Based Protein Options Offers Growth

A significant growth opportunity in the Protein Water Market lies in the expansion of plant-based protein options. As more consumers adopt vegan and plant-based diets, the demand for non-dairy, plant-derived protein sources is growing. Currently, most protein water products are made with whey protein, which may limit their appeal to people who avoid animal-based products due to dietary preferences or lactose intolerance.

By introducing more plant-based protein options, such as pea, rice, or hemp protein, companies can tap into a broader, more diverse consumer base. This shift would not only environmentally conscious consumers but also those seeking more sustainable and cruelty-free protein sources, potentially driving significant market growth in the coming years.

Latest Trends

Flavored Protein Waters Gain Consumer Popularity

One of the latest trends in the Protein Water Market is the growing popularity of flavored protein waters. Consumers are increasingly seeking beverages that not only offer nutritional benefits but also taste good. Flavored protein water provides a refreshing and enjoyable way to consume protein, especially for those who may find the taste of unflavored protein waters too bland.

The addition of flavors such as fruit, citrus, or tropical blends has made protein water more appealing, particularly among younger, health-conscious consumers. This trend is expanding the market beyond traditional fitness enthusiasts, as more mainstream consumers are looking for delicious, low-calorie, high-protein alternatives to sugary drinks.

Regional Analysis

In 2024, North America dominated the Protein Water Market with a 43.7% share, valued at USD 424.4 million.

North America dominates the Protein Water Market with a share of 43.7%, valued at USD 424.4 million in 2024. The region’s strong market position is driven by a high level of health consciousness, coupled with a robust fitness culture. The growing demand for convenient, functional beverages, particularly among athletes, fitness enthusiasts, and health-conscious individuals, contributes significantly to market growth in North America.

Europe holds a notable share of the market, supported by increasing consumer awareness of health and wellness trends. The region is seeing rising adoption of protein-enriched products, particularly in countries like the UK, Germany, and France. The demand for plant-based protein options is particularly strong, driven by vegan and vegetarian diets.

In the Asia Pacific region, the Protein Water Market is experiencing rapid growth, driven by rising disposable incomes, urbanization, and an increasing focus on health and fitness. Countries like China, Japan, and India are becoming key contributors to market expansion. However, the market remains relatively nascent in comparison to North America and Europe.

Middle East & Africa and Latin America are emerging markets with a smaller but growing presence in the protein water sector. These regions are gradually adopting health-focused trends, although the market share remains limited due to price sensitivity and lower awareness.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global Protein Water Market in 2024 continues to be highly competitive, with several established players dominating the landscape. Agropur Inc. (BiPro USA), Glanbia PLC, and Nestlé are among the leading companies leveraging their strong brands and extensive distribution networks to capture significant market share.

These companies are investing heavily in innovation, introducing a variety of protein water products to cater to different consumer preferences, including plant-based and whey protein options.

Coca-Cola, PepsiCo, and Gatorade, well-known for their dominance in the beverage sector, are also making strong moves into the protein water market. Their robust marketing strategies, coupled with their global presence, give them an advantage in reaching a broad consumer base. Products like Powerade and Propel under the Coca-Cola umbrella and Gatorade from PepsiCo have been pivotal in driving awareness and accessibility of protein waters in various retail channels.

Companies like BioSteel, Muscle Milk, and Body Armor are highly focused on the health and fitness market, offering products that specifically cater to athletes and fitness enthusiasts. Their emphasis on premium-quality protein, particularly in ready-to-drink formats, has resonated well with a performance-driven audience.

Additionally, newer entrants such as Protein Water Co., Protein2o Inc., and Vieve are capitalizing on the increasing demand for functional beverages with low-calorie, high-protein content. These players are focusing on unique formulations and niche positioning, which presents significant growth potential in untapped segments.

Top Key Players in the Market

- Agropur Inc. (BiPro USA)

- Alani Nut

- Aquatein

- BioSteel

- Body Armor

- CocaCola

- CytoSport

- Danone

- Gatorade

- Glanbia PLC

- Musashi Nutrition

- Muscle Milk

- Muscle Nation

- Nestle

- Nexus Sports Nutrition

- NZ Muscle

- OWYN

- PepsiCo

- Powerade

- Premier Nutrition

- Propel

- Protein Water Co.

- Protein2o Inc.

- The Healthy Protein Co (Vieve)

- Vega

Recent Developments

- In February 2025, Coca-Cola launched Simply Pop, a new prebiotic soda brand, to compete in the growing prebiotic soda market. This move is part of Coca-Cola’s strategy to diversify its portfolio and offer healthier alternatives.

- In 2024, Danone reported that sales of their high-protein products reached 1 billion euros in 2023, up from 400 million euros in 2021. The company is focusing on healthy aging, flexitarianism, and protein as key trends for 2024.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 971.3 Million |

| Forecast Revenue (2034) | USD 2,216.4 Million |

| CAGR (2025-2034) | 8.6% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Flavored, Unflavored), By Source (Whey Protein, Collagen Protein, Plant-Based Protein, Others), By End-Use (Sports and Fitness Enthusiasts, General Consumers, Medical and Clinical Nutrition, Others), By Distribution Channel (Hypermarkets and Supermarkets, Convenience Stores, Online, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Agropur Inc. (BiPro USA), Alani Nut, Aquatein, BioSteel, Body Armor, CocaCola, CytoSport, Danone, Gatorade, Glanbia PLC, Musashi Nutrition, Muscle Milk, Muscle Nation, Nestle, Nexus Sports Nutrition, NZ Muscle, OWYN, PepsiCo, Powerade, Premier Nutrition, Propel, Protein Water Co., Protein2o Inc., The Healthy Protein Co (Vieve), Vega |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |