Quick Navigation

Report Overview

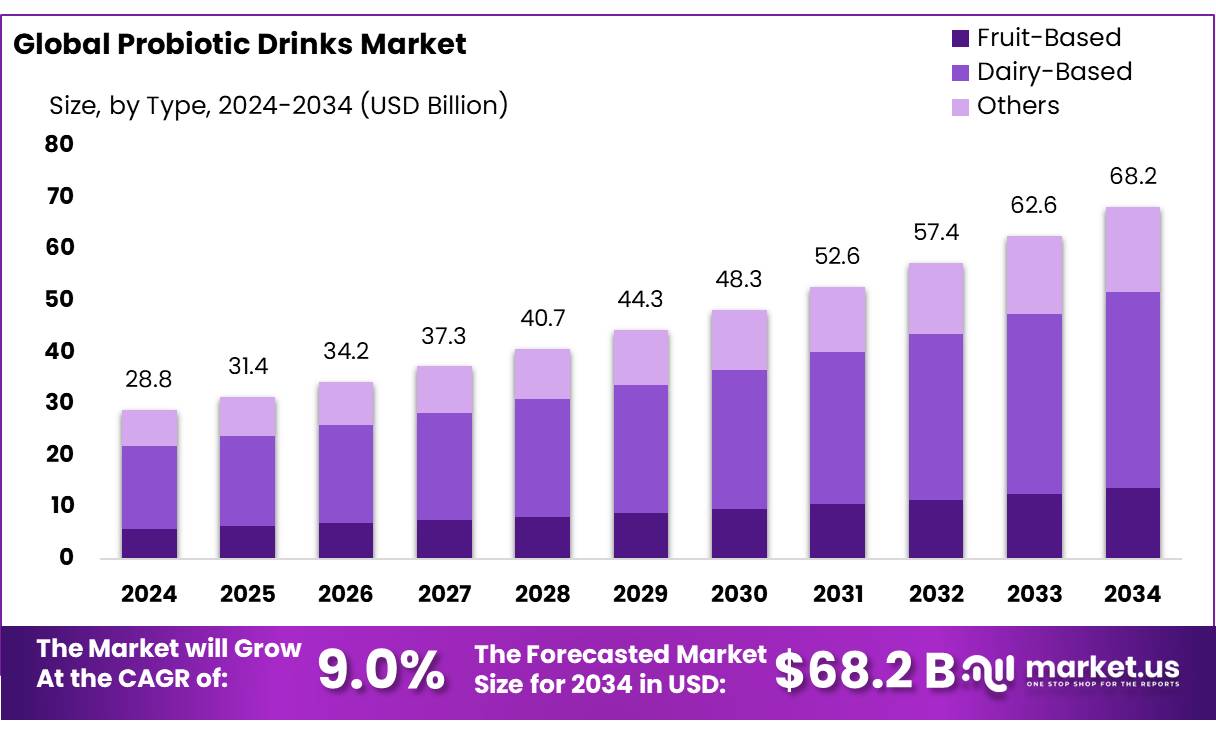

The Global Probiotic Drinks Market size is expected to be worth around USD 68.2 Bn by 2034, from USD 28.8 Bn in 2024, growing at a CAGR of 9.0% during the forecast period from 2025 to 2034.

Probiotic drinks, primarily categorized under functional beverages, contain live microorganisms intended to confer health benefits to the host. These beverages are typically fermented with strains of beneficial bacteria and yeast, which are purported to improve gut health, enhance immune function, and contribute to overall wellness. The growing consumer awareness regarding health and well-being, coupled with increasing disposable incomes, has led to a surge in the popularity of these drinks across various demographics.

The global probiotic drinks market is on an upward trajectory, driven by robust consumer demand for healthier beverage alternatives. According to the Food and Agriculture Organization of the United Nations, the sector has witnessed a compound annual growth rate (CAGR) of approximately 8% over the past five years, underscoring the growing shift towards health-centric products. Major players in the beverage industry, such as Yakult Honsha Co., Ltd and Danone, report annual sales growths reflecting increasing consumer preferences for probiotic-rich products. For instance, in the fiscal year 2023, Yakult reported a 12% increase in global sales, largely fueled by expanding markets in Asia and North America.

Governments worldwide have recognized the potential health benefits of probiotics and have initiated various programs to support the industry. In the European Union, the Horizon Europe program allocated €100 million in 2024 to research and develop functional foods, including probiotic beverages. This funding aims to support scientific studies that validate the health claims of probiotics, thus bolstering consumer trust and industry growth.

In the United States, the National Institutes of Health (NIH) has funded numerous projects under its Human Microbiome Project, focusing on understanding the impact of probiotics on human health. As of 2024, this initiative has directed over $200 million towards research in microbiota, which has significantly propelled forward the scientific backing for probiotic products.

Key Takeaways

- The global probiotic drinks market is projected to grow from USD 28.8 billion in 2024 to USD 68.2 billion by 2034, registering a CAGR of 9.0%.

- Dairy-based probiotic drinks led the market, holding a dominant share of over 56.70% in 2024.

- Lactobacillus emerged as the top probiotic strain, accounting for more than 59.30% of the global market.

- Flavored probiotic drinks captured the largest segment, representing over 67.30% of total market share.

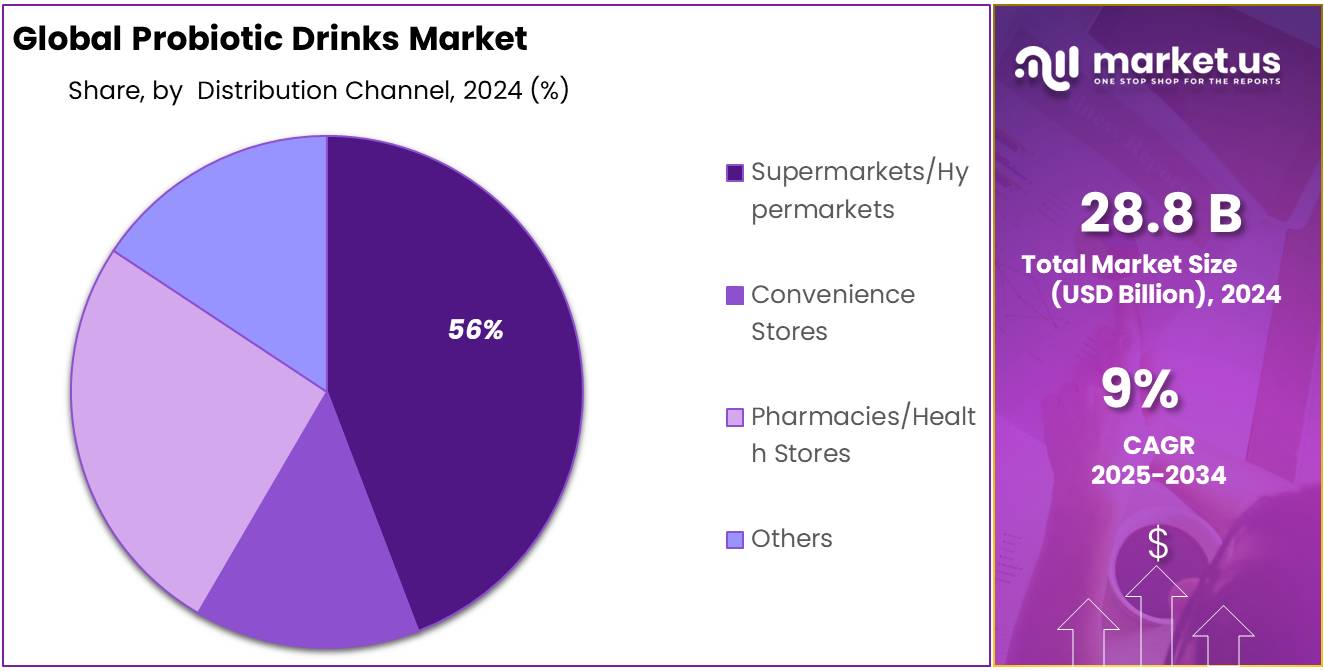

- Supermarkets and hypermarkets were the leading distribution channels, contributing over 56.30% to the overall sales.

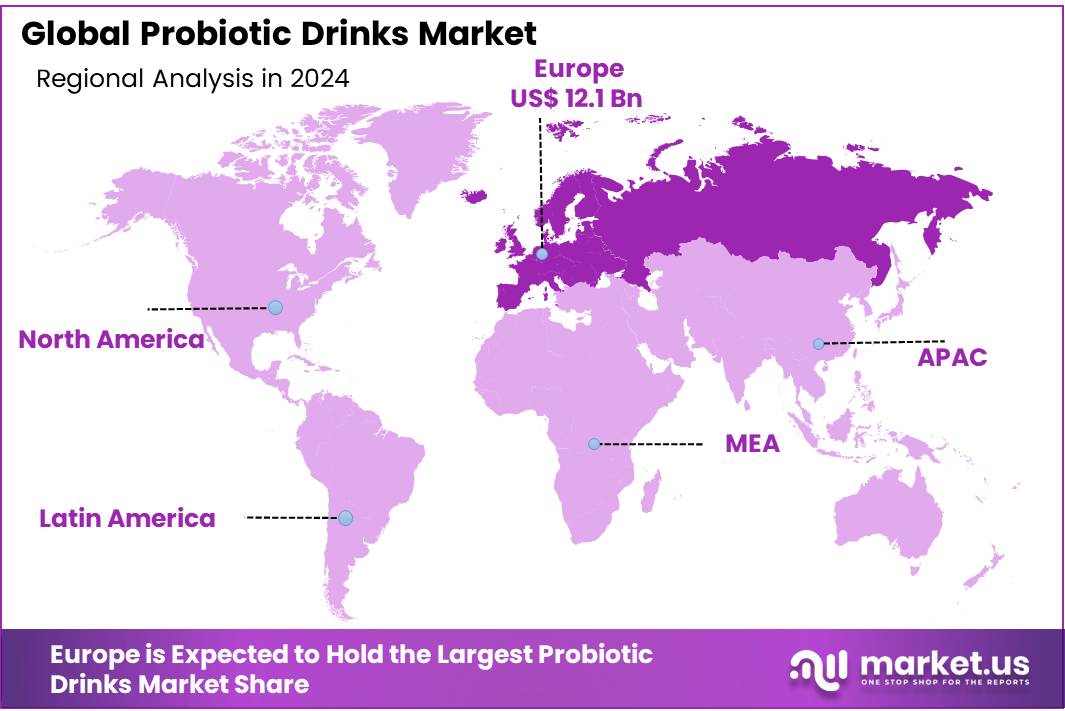

- Europe remained the largest regional market, contributing 42.20% to global revenue, equaling approximately USD 12.1 billion in 2024.

Analysts’ Viewpoint

From an investment perspective, the probiotic drinks market presents a diverse array of opportunities and risks that cater to a global audience increasingly conscious of health and wellness. This growth is driven by rising consumer demand for natural and healthy food and beverage options, with a notable trend towards dairy-based probiotic drinks, which are expected to hold the largest market share. These drinks, often containing lactobacillus, are sought after for their health benefits, such as improving gut health and boosting immunity

The market is not without its challenges, however. The variability in the efficacy of probiotic strains can confuse consumers and hinder market growth. This highlights a crucial investment risk, as it can lead to consumer skepticism about the effectiveness of probiotic products. . Moreover, the competitive landscape is quite fragmented with key players like Yakult Honsha Co. Ltd., PepsiCo, and Danone leading the charge, often through strategies such as new product development and geographic expansion to harness this growing demand

On the regulatory front, the market is influenced by the global push towards more stringent health and safety standards, which can impact market entry and product development. Technologically, the integration of e-commerce and digital marketing strategies is becoming essential for reaching consumers directly and enhancing market penetration, particularly in developing regions where internet usage is rising.

By Type

Dairy-Based probiotic drinks lead the market with 56.7% share, thanks to strong consumer trust and tradition.

In 2024, Dairy-Based held a dominant market position, capturing more than a 56.70% share. Consumers continue to prefer traditional probiotic sources like yogurt drinks and fermented milk due to their familiarity and natural taste. The nutritional profile, which includes calcium, protein, and live cultures, adds to their popularity. Countries in Europe and Asia, where dairy-based probiotic drinks are widely consumed, contributed heavily to this share. In 2025, the demand is expected to stay strong, especially with growing awareness around gut health and immunity. Dairy-based options are likely to retain their lead, supported by innovations in flavor, packaging, and low-sugar formulations that appeal to health-conscious buyers.

By Bacteria

Lactobacillus tops the chart with 59.3% share, driven by its proven digestive health benefits.

In 2024, Lactobacillus held a dominant market position, capturing more than a 59.30% share. It remains the most trusted strain in probiotic drinks, known for supporting digestion and improving gut balance. Its strong reputation, backed by years of clinical use, keeps it a go-to ingredient for manufacturers. Consumers easily recognize the name, making it a popular choice in both traditional and modern drink formats. Moving into 2025, the trend is expected to continue as more people turn to daily probiotics for immunity and wellness. With growing interest in functional beverages, Lactobacillus-based drinks are likely to maintain their lead across global markets.

By Flavor

Flavored probiotic drinks lead with 67.3% share, thanks to taste variety and better consumer appeal.

In 2024, Flavored held a dominant market position, capturing more than a 67.30% share. Taste plays a big role in attracting regular drinkers, especially kids and young adults. Options like strawberry, mango, and mixed berries make probiotics more enjoyable, helping brands widen their audience. Many consumers prefer these drinks not just for health benefits but also as a tasty alternative to sugary sodas. In 2025, flavored probiotic drinks are expected to see steady growth, with companies launching new blends and low-sugar versions. This flavor-first approach keeps them ahead of unflavored varieties in both retail shelves and online platforms.

By Distribution Channel

Supermarkets and hypermarkets dominate with 56.3% share, fueled by easy access and wide product variety.

In 2024, Supermarkets/Hypermarkets held a dominant market position, capturing more than a 56.30% share. These stores remain the top choice for buying probiotic drinks due to their strong shelf presence and convenience. Shoppers prefer seeing and comparing products in person, especially when it comes to health-based drinks. Attractive discounts, bundle offers, and organized chillers make these outlets ideal for weekly or monthly purchases. In 2025, this channel is expected to maintain its lead as more brands expand their physical presence and invest in eye-catching in-store displays. The trust and routine of supermarket shopping continue to give it an edge over other formats.

Key Market Segments

By Type

- Fruit-Based

- Dairy-Based

- Others

By Bacteria

- Lactobacillus

- Streptococcus

- Bifid Bacterium

- Others

By Flavor

- Original

- Flavored

- Strawberry

- Vanilla

- Blueberry

- Mango

- Raspberry

- Others

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Pharmacies/Health Stores

- Others

Drivers

Rising Focus on Gut Health and Immunity is Fueling the Demand for Probiotic Drinks

One major driving factor behind the growth of probiotic drinks is the increasing consumer focus on gut health and stronger immunity. Over the last few years, people have become more aware of how a healthy gut impacts overall well-being, not just digestion. This awareness spiked especially after the COVID-19 pandemic, when boosting immunity became a daily priority for many households.

According to the International Food Information Council (IFIC), nearly 52% of U.S. consumers in a 2023 survey said they actively look for foods and beverages that support digestive health. This shows a clear shift in how people view their daily nutrition—not just for taste or energy, but also for long-term health and immune support.

Probiotic drinks, especially those containing strains like Lactobacillus and Bifidobacterium, have proven benefits for maintaining the balance of good bacteria in the gut. These drinks are not just a trend—they are becoming a daily routine for many. Functional drinks with added probiotics offer a convenient and enjoyable way to take care of gut health without the need for supplements.

Even global health authorities are paying attention. The World Health Organization (WHO) has recognized the role of probiotics in improving gastrointestinal health and reducing the risk of some infections. This has encouraged local governments and food agencies in regions like the EU and Japan to support probiotic-friendly policies in food labeling and product approvals.

Restraints

Cold Chain Dependency and Short Shelf Life Limit Market Reach for Probiotic Drinks

One major challenge slowing down the growth of probiotic drinks is their need for a strict cold chain and relatively short shelf life. These products contain live bacteria that must remain active to offer health benefits. If the temperature isn’t maintained properly from production to consumption, the bacteria can die, making the product less effective or even useless.

According to the Food and Agriculture Organization (FAO) and the World Health Organization (WHO), probiotics must be kept at specific temperatures—usually between 2°C and 8°C—to maintain their potency and health benefits. Any break in this temperature range during storage or transit can harm the live cultures. This is a serious concern, especially in developing countries where cold storage facilities are limited or unreliable.

For small manufacturers and rural distributors, setting up a consistent cold supply chain is costly and logistically tough. This limits the availability of probiotic drinks in non-urban areas. Even in large cities, stores without proper refrigeration might hesitate to stock these drinks, especially when cheaper, non-refrigerated beverages are more convenient to handle.

Additionally, the shelf life of most probiotic drinks is just 4 to 6 weeks, compared to several months or more for typical soft drinks or juices. Retailers need to move the stock quickly, or they risk spoilage and loss. Consumers also worry about expiry dates, and many avoid buying these drinks in bulk for the same reason.

Opportunity

Plant-Based and Non-Dairy Probiotic Drinks Open New Doors for Market Growth

A major growth opportunity in the probiotic drinks market lies in the rising demand for plant-based and non-dairy alternatives. As more people adopt vegan lifestyles or face lactose intolerance, the need for dairy-free probiotic options is growing fast. This shift is not just a trend—it’s becoming a long-term movement driven by both health concerns and ethical choices.

According to the U.S. National Institutes of Health (NIH), around 68% of the world’s population has some degree of lactose malabsorption. This means a huge portion of people are actively looking for probiotic sources that don’t involve dairy.

To cater to this demand, companies are launching drinks made from almond milk, soy, oat, coconut, and even kombucha-style fermented teas. These products offer the same digestive benefits as traditional dairy-based probiotics but are gentler on the stomach and fit well with plant-based diets.

Governments are also supporting this movement through clean labeling laws and incentives for plant-based innovation. For example, the European Union has supported the “Smart Protein Project”, which aims to develop sustainable and nutritious alternatives to animal-based products, including beverages. This initiative promotes the use of plant proteins and fermentation technologies in food and drinks.

In 2025 and beyond, this space is expected to expand as more consumers look for allergy-friendly, cruelty-free, and environmentally sustainable options. Non-dairy probiotic drinks not only address dietary restrictions but also attract eco-conscious shoppers. With better taste, shelf life improvements, and strong support from both consumers and governments, this category could become one of the biggest game changers in the probiotic drinks market.

Trends

Functional Beverages with Added Health Benefits Are Gaining Popularity

A notable trend in the beverage industry is the increasing consumer demand for functional drinks that offer health benefits beyond basic nutrition. Probiotic drinks, known for promoting digestive health, are at the forefront of this movement. Consumers are seeking beverages that not only quench thirst but also contribute to overall well-being.

Major beverage companies are responding to this trend by expanding their portfolios to include health-focused options. For instance, in early 2025, PepsiCo acquired Poppi, a brand specializing in low-calorie, probiotic-infused sodas, in a deal valued at $1.65 billion. This acquisition aligns with PepsiCo’s strategy to cater to health-conscious consumers seeking functional beverages.

Similarly, Coca-Cola introduced “Simply Pop,” a prebiotic soda line designed to support digestive health and boost the immune system. These beverages contain Vitamin C, Zinc, and prebiotic fiber, reflecting the company’s commitment to offering products that align with current health and wellness trends.

Consumer behavior further underscores this trend. A 2023 survey by the International Food Information Council (IFIC) revealed that 52% of U.S. consumers actively seek foods and beverages that support digestive health, highlighting the growing emphasis on functional benefits in dietary choices.

As awareness of the link between diet and health continues to grow, the demand for functional beverages like probiotic drinks is expected to rise, driving innovation and expansion in this sector.

Regional Analysis

In 2024, Europe continued to assert its dominance in the global probiotic drinks market, accounting for a substantial 42.20% share, equivalent to USD 12.1 billion in revenue. This significant market share is driven by a robust consumer awareness of health and wellness, particularly regarding digestive health and immunity support. European consumers show a strong preference for probiotic products, including drinks, which are commonly incorporated into daily diets across the region.

Countries like Germany, France, and the United Kingdom lead within Europe, both in terms of consumption and innovation in probiotic drink offerings. This regional market thrives due to several key factors including high consumer awareness, extensive availability of products, and strong marketing by leading dairy and non-dairy producers. The European market is also bolstered by stringent food safety regulations that ensure product quality and efficacy, thereby increasing consumer trust and demand.

Moreover, Europe’s focus on sustainable and organic food production aligns well with the growing consumer preference for natural and environmentally friendly products. This has led to a surge in organic and vegan probiotic drink options, catering to a diverse audience looking for ethical and health-conscious choices.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Bio-K+ International Inc. is renowned for its clinically tested probiotic products that promote digestive health and immunity. Their drinks are uniquely formulated with specific probiotic strains to ensure high efficacy. Bio-K+ actively invests in scientific research to validate the benefits of their formulations, distinguishing their offerings in the competitive wellness market.

Cargill Incorporated has expanded its footprint in the functional beverage industry by offering probiotic products that cater to health-conscious consumers. They focus on sustainable practices and the development of innovative probiotic formulations, leveraging their global supply chain to enhance food safety and nutritional value.

Royal DSM is a global science-based company that emphasizes innovation in health, nutrition, and materials. In the probiotic drinks market, DSM offers tailor-made solutions that enhance gastrointestinal health and overall well-being. Their commitment to sustainability and cutting-edge research underpins their development of new, effective probiotic products.

Gujarat Cooperative Milk Marketing Federation Ltd (Amul) is a major player in India’s dairy sector and has ventured into probiotic beverages with an emphasis on affordability and accessibility. Their products are geared towards improving gut health and are widely accepted for their quality and health benefits, making them a trusted name in Indian households.

Top Key Players

- Bio-K

- Cargill Incorporated

- DSM

- Fonterra Co-op Group Ltd

- GCMMF

- Groupe Danone SA

- Harmless Harvest Inc.

- Lala Branded Products LLC

- Lifeway Foods, Inc

- Nestlé

- Obi Probiotic Soda

- PepsiCo Inc.

- Yakult U.S.A. Inc.

Recent Developments

Cargill’s strategy includes tapping into both dairy-based and plant-based probiotic drink segments, catering to a wide array of consumer preferences that include traditional dairy lovers as well as those opting for vegan or lactose-free alternatives.

In 2024, DSM, a global leader in health and nutrition, has effectively leveraged its expertise to innovate within the probiotic drinks market, primarily focusing on enhancing the health benefits of its probiotic offerings.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 28.8 Bn |

| Forecast Revenue (2034) | USD 68.2 Bn |

| CAGR (2025-2034) | 9.0% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Fruit-Based, Dairy-Based, Others), By Bacteria (Lactobacillus, Streptococcus, Bifid Bacterium, Others), By Flavor (Original, Flavored, Strawberry, Vanilla, Blueberry, Mango, Raspberry, Others), By Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Pharmacies/Health Stores, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Bio-K, Cargill Incorporated, DSM, Fonterra Co-op Group Ltd, GCMMF, Groupe Danone SA, Harmless Harvest Inc., Lala Branded Products LLC, Lifeway Foods, Inc, Nestlé, Obi Probiotic Soda, PepsiCo Inc., Yakult U.S.A. Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |