Quick Navigation

Report Overview

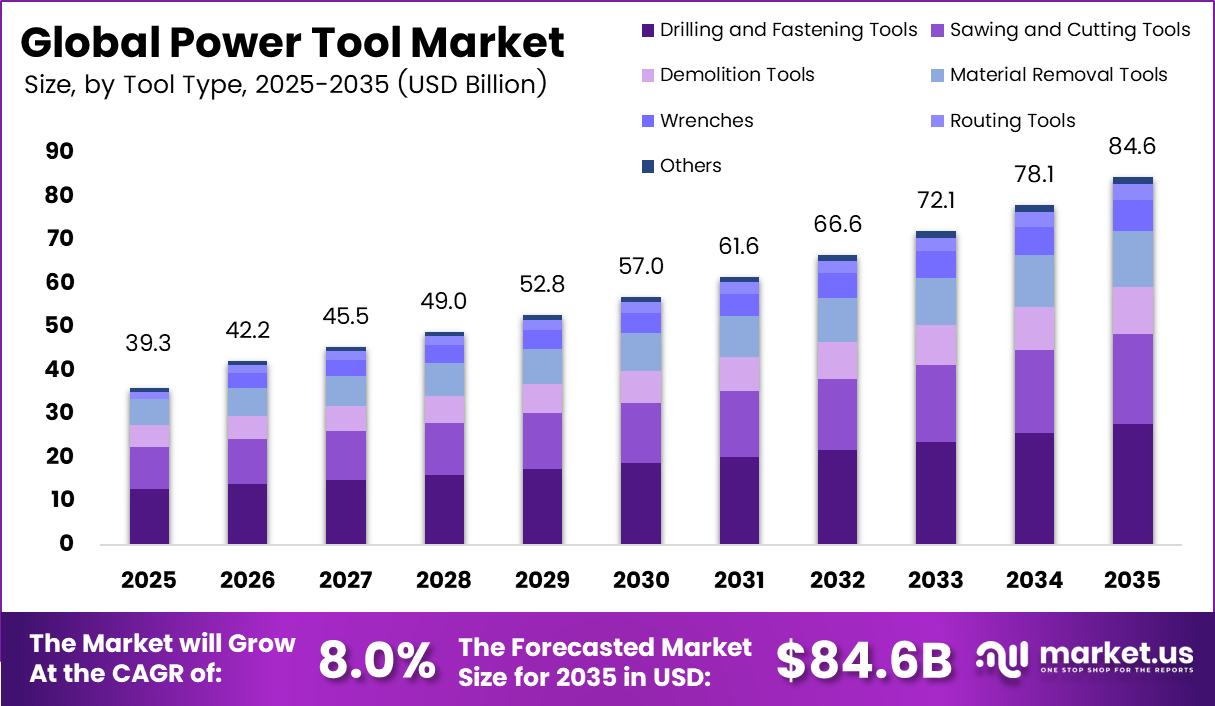

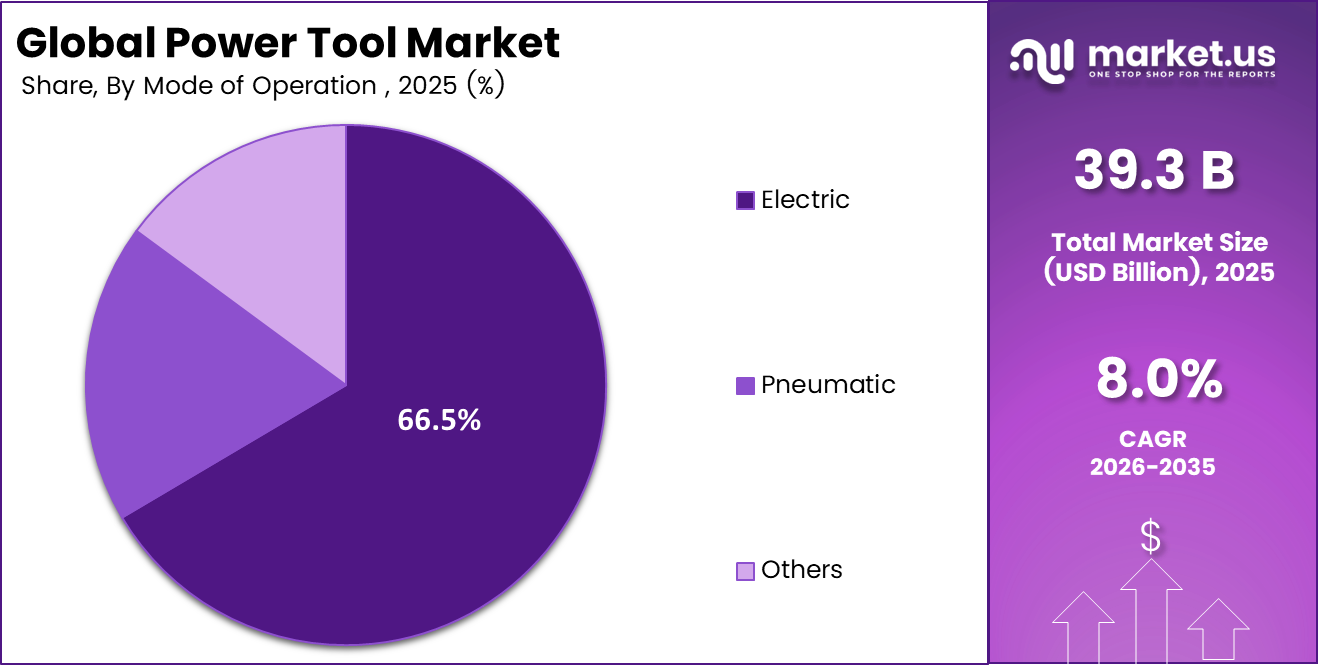

The Global Power Tools Market was valued at USD 39.3 billion in 2025 and is projected to reach USD 84.6 billion by 2035, growing at a steady CAGR of 8.0% over the 2026–2035 period. North America leads the global landscape, holding a commanding 33.0% market share. This growth is not incidental; it is directly backed by the rapid expansion of the two largest end-use industries: construction and automotive manufacturing.

On the construction side, the U.S. Census Bureau reported total construction spending at a seasonally adjusted annual rate of USD 2.17 trillion in April 2026, with residential construction alone running at USD 909.9 billion. This massive volume of active building and renovation work requires millions of drills, grinders, circular saws, and impact tools on job sites every day.

The U.S. Bipartisan Infrastructure Investment and Jobs Act (IIJA) further committed USD 1.2 trillion in federal infrastructure spending, including USD 550 billion in new outlays for roads, bridges, water systems, and the power grid, all of which are heavy consumers of professional-grade power tools. According to the American Society of Civil Engineers (ASCE), this law introduced 21 new DOT grant programs, sustaining long-term tooling demand across public works projects nationwide.

On the automotive front, the International Organization of Motor Vehicle Manufacturers (OICA) recorded global vehicle production rising from 92.7 million units in 2024 to 96.4 million units in 2025, a year-on-year jump of 3.9%. The U.S. alone registered 16.67 million vehicle sales in 2025. Every vehicle assembled on a factory floor relies on power tools, torque wrenches, pneumatic drills, and electric screwdrivers at every stage of production. This direct cause-and-effect link between rising vehicle output and power tool consumption is a key structural driver of market growth.

Key Takeaways

- The global power tools market size was valued at US$ 39.3 billion in 2025.

- The global power tools market is expected to register a CAGR of 8.0%, reaching US$ 84.6 billion by 2035.

- By Tool type, drilling and fastening tools accounted for a significant share of the market, representing 32.8% of the overall market share.

- By mode of operation, electric power tools represented a significant market share of about 66.5%

- By application, the industrial/ professional category was a significant share of the power tools market, contributing 68.0% of the overall market share.

- By distribution channel, offline retail was a significant share of the market, contributing approximately 58.0% of the overall revenue share.

- In 2025, North America was a significant share of the global power tools market, contributing 33.0% of the overall market share.

Tool Type Analysis

Tools used for drilling and fastening dominate the market share of power tools

Drilling and fastening tools hold a 32.8% share of the global power tools market, driven by heavy usage in construction, automotive, manufacturing, and maintenance sectors. Their high precision, efficiency, and durability reduce manual labor demands. Ongoing infrastructure projects and industrial automation further bolster the strong demand for these essential tools.

This market segment is also experiencing growth due to constant innovations in technology, including the use of wireless tools, lithium-ion battery-powered tools, ergonomic design of products, lightweight designs, and energy efficiency, among others. Innovations in this sector have led to increased ease of use, productivity, and convenience in both industrial and residential sectors. For instance, the usage of wireless drills and fasteners has become widespread in construction sites and automobile manufacturing plants.

Mode of Operation

Electric Power Tools Retain Dominance Due to Increased Efficiency and User-Friendliness

The Electric mode of operation became the dominant one within the global power tools market, occupying 66.5% of the overall market share. The dominance of the segment is primarily attributed to its high operational efficiency, ease of handling, lower maintenance requirements, and extensive utilization across industrial, commercial, construction, automotive, and residential applications. Increasing demand for portable, durable, and high-performance tools is further supporting the widespread adoption of this equipment across professional and household sectors globally.

For Instance, Cordless drills, impact drivers, angle grinders, and rotary hammers with lithium-ion batteries are favored in construction for their portability and efficiency. As for other modes of operation, they occupy only 14.9% of the overall market share. In particular, they include hydraulic and engine-driven power tools, which are mostly used in industrial and outdoor operations. It should be noted that growing

Power tools using pneumatic operation represent 18.6% of the overall market share, while being in demand within heavy-duty industries because of the high performance and reliability of such tools. However, they are less preferred than electric tools because of their high dependence on air compressors and complicated process of using them.

By Application

Power Tools Market Primarily Driven by Industrial/Professional Applications

Industries and professional applications form the major part of the worldwide power tools market share with a 68.0% contribution. The dominance of this application sector can be attributed to the wide use of power tools in construction, automotive, manufacturing, aerospace, and other heavy industries. Of the industrial/professional applications, construction contributes the most with 14.0%, due to the rapid pace of infrastructural development, urbanization, and commercial/ residential construction activities.

Automotive and manufacturing sectors contribute 6.0% and 5.0%, respectively, owing to higher vehicle production rates and increasing assembly line automation and industrialization. These industries depend on sophisticated electric and cordless power tools to increase their efficiency and speed up the manufacturing process.

Residential/DIY applications form the next category in terms of power tool usage, contributing 4.0% to the overall market share. Home improvement activities, together with easy availability of inexpensive power tools, are responsible for increased sales in this category. The aerospace industry contributes 1.5% to the market share because of the importance of power tools in aerospace maintenance and assembly operations, whereas the remaining applications contribute 1.5%.

Distribution Channel

Offline Retail Leads the Distribution Channel for Power Tools Market

The offline retail segment holds a significant 58.0% share of the global power tools market, driven by the prevalence of hardware stores and specialty distributors. Customers value physical product evaluation, leading professional contractors and industrial buyers to favor offline channels for reliability, immediate availability, technical support, and warranty services. Large industrial clients also prefer offline procurement for bulk buys and sustained supplier partnerships.

For Instance, Construction contractors acquire tools like rotary hammers and impact drivers through authorized dealers due to live demos, training, and maintenance support. Likewise, manufacturing firms use offline networks for specialized tools needing technical guidance and tailored agreements. The growth of dealer networks and partnerships has enhanced offline retail in the industrial and construction sectors.

Online retail is growing steadily, fueled by e-commerce, competitive pricing, diverse product offerings, and delivery services. Digital procurement, better internet access, and a DIY culture are further expanding online channels, while manufacturers utilize omnichannel strategies to enhance customer reach and convenience.

Key Market Segments

By Tool Type

- Drilling and Fastening Tools

- Sawing and Cutting Tools

- Demolition Tools

- Material Removal Tools (Grinders, Sanders)

- Wrenches

- Routing Tools

- Others

By Mode of Operation

- Electric

- Pneumatic

- Others

By Application

- Industrial/Professional

- Construction

- Automotive

- Manufacturing

- Aerospace

- Residential/DIY

- Others

By Distribution Channel

- Direct Sales

- Offline Retail

- Online Retail

- Others

Market Dynamics

Opportunity

The global tool rental and Equipment-as-a-Service model represents one of the most immediately executable growth opportunities in the power tools industry. The wider equipment rental market was valued at approximately USD 240.58 billion in 2026 and is projected to reach USD 411.55 billion by 2035, expanding at a 6.16% CAGR. However, dedicated subscription platforms for SME contractors, independent tradespeople, and urban DIY consumers remain underdeveloped.

Most manufacturers still depend on one-time hardware sales for 65%–75% of their revenue, leaving limited scope for recurring post-sale income. A professional cordless drill priced at USD 350–450 could generate USD 180–240 annually through a USD 15–20 monthly subscription while reducing customer acquisition costs by an estimated 30%–40%. Although power tools account for 33.7% of the tool rental product segment, large generalist rental companies continue to control this channel.

An OEM-operated platform combining connected fleet management, included maintenance, and accessory cross-selling could achieve gross margins of 55%–60%, compared with 38%–42% from conventional hardware sales. This model would allow manufacturers to capture recurring revenue, serve price-sensitive users, and reduce their dependence on intermediaries.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Tool-as-a-Service (TaaS) / Rental Monetization | +1.8% | North America, EU, Urban APAC | Short term (≤ 2 years) |

| Smart & IoT-Connected Tool Ecosystem | +2.2% | North America, EU, South Korea, Japan | Medium term (2–4 years) |

| Untapped DIY Consumer Segment in APAC & MEA | +1.5% | India, SEA, Middle East, GCC | Short–Medium term |

| AI-Integrated Predictive Maintenance Platform | +1.6% | EU industrial corridors, North America | Medium term (2–4 years) |

| Green/Circular Economy Tool Re-commerce | +1.2% | EU (regulatory mandate), North America | Medium term (2–4 years) |

| M&A Roll-Up of Regional Mid-Market Brands | +2.0% | APAC, Latin America, MEA | Long term (≥ 4 years) |

Drivers

Infrastructure and construction investment across emerging economies remains the strongest structural demand driver for professional power tools. India’s construction output is expected to rise by as much as 4.4% in 2026 after recording 7.4% growth in 2025. This expansion is supported by government capital expenditure of nearly INR 11.1 trillion and approximately USD 134 billion allocated to infrastructure projects covering highways, airports, metro systems, and industrial corridors. Such spending can create a 1.3–1.7 times multiplier effect on demand from construction-related trades.

The Middle East is also entering a major investment cycle, with its power tools market valued at USD 1.5 billion in 2024. Saudi Vision 2030, the UAE’s AED 4.5 trillion long-term development pipeline, and Qatar’s continuing urban maintenance requirements are supporting regional tool purchases. Worldwide construction output is forecast to increase by 2.3%, with emerging markets growing by 3.1% compared with 1.5% in advanced economies. This difference is increasing demand for durable and cost-efficient tools designed for dusty environments, high temperatures, and locations with unreliable electricity access.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure & Construction Boom in Emerging Markets | +1.9% | India, Southeast Asia, Middle East, GCC | Medium term (2–4 years) |

| Cordless & Brushless Motor Technology Adoption | +1.5% | Global (North America, EU, APAC lead) | Short term (≤ 2 years) |

| Residential Renovation & DIY Culture Expansion | +1.2% | North America, EU, Australia, Urban APAC | Short–Medium term |

| Industrial Automation & MRO Demand Surge | +1.0% | EU industrial corridors, North America, China | Medium term |

| Battery Technology Advancement (Li-ion/LFP Transition) | +0.9% | Global (APAC manufacturing core, North America) | Medium–Long term |

| E-commerce & Digital Distribution Channel Growth | +0.8% | APAC, Latin America, MEA | Short term (≤ 2 years) |

Restraints

Raw material price volatility is creating immediate cost pressure across the power tools supply chain. Steel prices increased by 8.2%, while aluminum prices averaged 10% above earlier benchmarks. Together, these materials can represent approximately 45%–55% of the bill of materials for a standard corded or pneumatic tool. Cordless tool manufacturers also remain exposed to cobalt supply risks, as nearly 70% of global production originates from the Democratic Republic of the Congo.

In June 2026, rising energy and logistics expenses linked to the Iran conflict added further pressure across battery mining, refining, and manufacturing operations. Current input inflation could reduce gross margins by 4.5–5.5 percentage points before mitigation measures are applied. Price increases are particularly difficult in the USD 40–120 entry-professional category, where low-cost Asian suppliers maintain strong competitive positions. Manufacturers may therefore absorb 50%–65% of higher expenses.

Risk-management strategies include steel contracts covering 6–9 months of procurement and redesign programs that lower metal content by 10%–15% through greater use of polymers and composites. Premium brushless and connected tools provide stronger pricing flexibility, allowing companies to pass through 70%–80% of additional costs.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material Price Volatility (Steel, Aluminum, Cobalt) | -1.2% | Global (APAC manufacturing core, North America) | Short term (≤ 2 years) |

| US-China Tariff & Trade Policy Disruption | -1.0% | North America, APAC export corridors | Short–Medium term |

| High Mortgage Rates Suppressing New Construction | -0.8% | North America, EU residential markets | Short term (≤ 2 years) |

| Regulatory Compliance Cost Burden (RoHS, ESPR, REACH) | -0.7% | EU, UK, and all EU-export markets | Medium term (2–4 years) |

| Proliferation of Counterfeit & Sub-Standard Tools | -0.6% | APAC (India, SEA), MEA, Latin America | Medium–Long term |

| Semiconductor Allocation Constraints for Smart Tools | -0.5% | Global (North America, EU, East Asia) | Short term (≤ 2 years) |

Challenges

The skilled trades workforce shortage is a long-term challenge because professional tool demand depends directly on construction, maintenance, and repair activity. The United States could face a deficit of 500,000 skilled workers by 2030, limiting project execution and slowing tool replacement and accessory consumption. Electricians, plumbers, and carpenters in developed markets have an average age of approximately 43–47 years, while vocational recruitment remains insufficient to replace retiring workers.

Restoring the labor pipeline may require 8–12 years of sustained enrollment growth in technical education and apprenticeship programs. Each unfilled position can defer an estimated USD 180,000–240,000 in annual construction activity, producing a potential output gap of USD 90–120 billion.

Applying a power tool expenditure coefficient of 3.5%–4.5% indicates direct demand deferral of approximately USD 3.5–5.5 billion. Manufacturers are responding with lighter designs, vibration control, one-handed operation, automatic speed adjustment, and torque-sensing systems. These features can add USD 15–25 to the bill of materials, but they help older tradespeople remain productive and enable less-experienced workers to perform more complex tasks.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Skilled Trade Workforce Deficit | -1.1% | North America, EU, Australia | Long term (≥ 4 years) |

| Battery Supply Chain Geopolitical Concentration Risk | -0.9% | Global (China refining dominance) | Long term (≥ 4 years) |

| Rapid Technology Obsolescence & Platform Fragmentation | -0.8% | Global (North America, EU core) | Medium term (2–4 years) |

| Price War & Margin Erosion from Low-Cost Asian Entrants | -0.9% | APAC, Latin America, MEA | Medium term (2–4 years) |

| Logistics Cost Inflation & Last-Mile Complexity | -0.6% | APAC logistics corridors, Latin America, MEA | Short–Medium term |

| Talent Deficit in R&D and IoT Engineering | -0.7% | North America, EU, South Korea | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Geopolitical Impact Assessment: Supply Chain Interruptions, Trade Regulations, and Local Manufacturing Changes Transforming the Worldwide Power Tools Market

There are many reasons why geopolitics, trade policies, and logistical problems play important roles in determining the development of the global power tools market, since they impact manufacturing processes, logistics operations, and pricing strategies. The escalation of geopolitical tensions and restrictions associated with international trade have led companies to seek diversification through decentralization of manufacturing facilities from areas with heavy concentrations of manufacturing operations to countries like Southeast Asia.

The industry’s market is affected by tariffs on imports and changes in the prices of raw materials, thus increasing production costs for manufacturers. Due to increases in the cost of production of steel, aluminum, batteries, and electronics, there has been pressure on prices, which leads to high costs for products in the global market. Furthermore, the issues that exist in terms of logistics, transportation, and shortage of crucial materials in the global supply chain have led to the development of the “China+1” approach.

Companies are prioritizing localized production, regional supply networks, and nearshoring to enhance supply chain stability and reduce risks. This includes expanding manufacturing and supplier partnerships to cut lead times, addressing cost volatility and complexity while fostering resilient production ecosystems in the power tools industry.

Regional Analysis

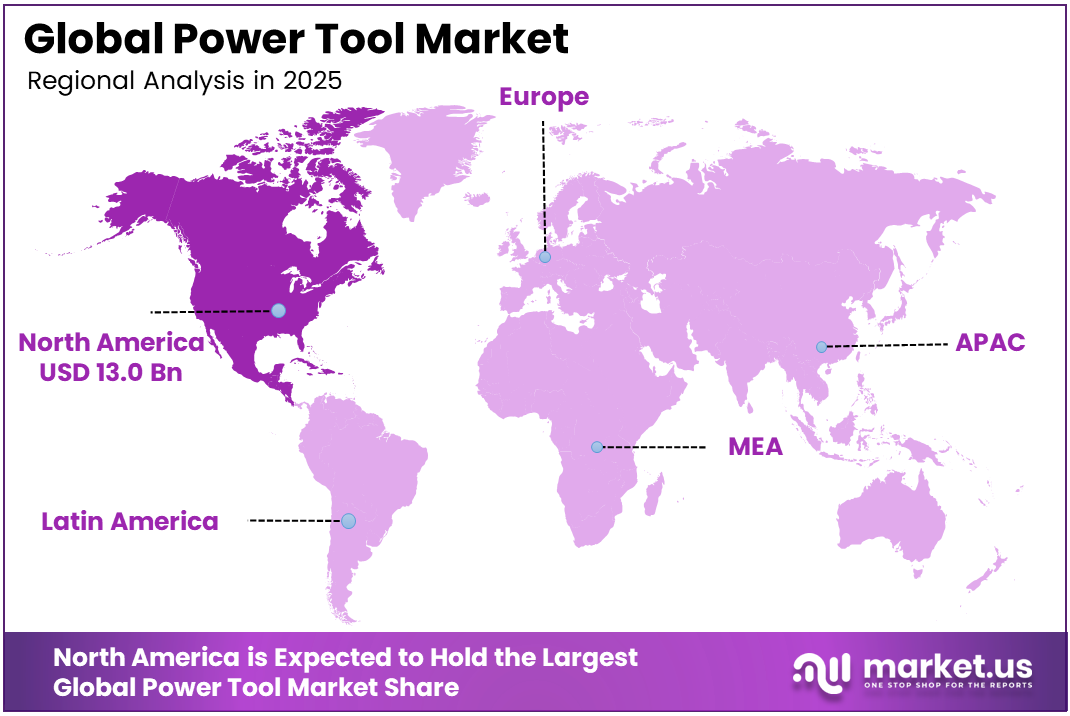

North America led the worldwide power tools market with a regional share of about 33.0%. The predominance of the region can be attributed to its sophisticated industrial base, higher use of electric and cordless power tools, and the presence of growing construction, automotive, aerospace, and manufacturing sectors. The growing requirement for superior performance and productivity from equipment in industrial applications drives market growth in the region.

The region experiences growth from investments in infrastructure, construction, and industrial automation. The U.S. contributes through manufacturing, home improvement, and advanced cordless tools. Labor shortages in construction and industry boost automation and battery-powered equipment. Lithium-ion tools are favored for portability, runtime, and flexibility, replacing traditional corded options.

Europe takes 27.0% of the market share globally. Some of the factors that contribute to the success of Europe are the availability of infrastructure, technological advancement of precision engineering, and an increasing demand for energy-efficient and ergonomic power tools. The Asia-Pacific region takes up 25.0% of the market because of industrialization and urbanization, development of infrastructure in countries such as China and India, and manufacturing.

The Latin America and the Middle East & Africa regions account for 8.0% and 7.0% of the market share, respectively. Factors leading to growth in these regions are industrialization, construction activities, and infrastructure development. Even though at present they have low shares in the global market, they are forecasted to grow in the coming years.

Key Regions and Countries Covered in this Report

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

There is high concentration within the global power tools market, with leading firms occupying a sizable chunk of total revenue. The main players continue to focus on growing their presence in the market through acquisitions, mergers, and collaborations to develop product lines and bolster their competitiveness. Some of the main firms dominating the global power tools market include Stanley Black & Decker, Inc., Techtronic Industries (TTI), Robert Bosch GmbH, Makita Corporation, and Hilti Corporation.

These companies lead the market because of their extensive distribution networks, innovation, and diverse product lines. Apart from using acquisitions and mergers as means of growth, firms are investing more in the research and development of technologically advanced and energy-efficient power tools, such as cordless power tools.

The increase in demand for smart and connected tools has heightened competition among manufacturers, leading them to embrace digitization. Robert Bosch GmbH has introduced smart tool solutions where users can monitor and control the performance of the tools using mobile applications, hence increasing accuracy, customization, and efficiency.

The Following are some of the Major Players in the Industry

- Stanley Black & Decker, Inc.

- Techtronic Industries (TTI)

- Robert Bosch GmbH

- Makita Corporation

- Hilti Corporation

- Snap-on Incorporated

- Atlas Copco AB

- Emerson Electric Co.

- Apex Tool Group, LLC

- Koki Holdings Co., Ltd.

- Ingersoll Rand Inc.

- Festool Group GmbH & Co. KG

- Husqvarna AB

- Chevron Corporation (Enerpac)

- Hitachi Koki Co., Ltd.

- Others

Key Development

- In November 2024, Makita U.S.A. launched the 18V LXT Brushless 4-Speed Impact Driver (XDT20) to enhance fastening precision and efficiency, featuring multiple speed modes, easy rear controls, and assist modes to reduce cam-out and cross-threading, emphasizing cordless technology trends in the industry.

- In October 2024, Makita U.S.A. launched the 40V max XGT 9-inch Power Cutter (GEC03), enhancing its cordless cutting lineup to replace gas-powered tools. It offers 45% more power, 55% less vibration, and aligns with the shift towards battery equipment for better productivity and lower emissions.

- In October 2024, Milwaukee Tool introduced the next-gen M18 FUEL Deep Cut Band Saws with enhanced cordless electronics, better ergonomics, and 20% faster cutting. They provide up to 78 cuts per charge and are lighter, boosting productivity and demonstrating commitment to high-performance cordless systems.

- In August–October 2024, Milwaukee Tool expanded its M18 platform with high-density battery architecture, enhancing grinders and heavy-duty cutting tools. Improved battery tech and brushless motors boost power, runtime, and efficiency, reducing reliance on corded tools.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 39.3 Bn |

| Forecast Revenue (2035) | USD 84.6 Bn |

| CAGR (2026-2035) | 8.0% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Tool Type (Drilling and Fastening Tools, Sawing and Cutting Tools, Demolition Tools, Material Removal Tools, Wrenches, Routing Tools, Others), By Mode of Operation (Electric, Pneumatic, Others), By Application (Industrial/Professional, Construction, Automotive, Manufacturing, Aerospace, Residential/DIY, Others), By Distribution Channel (Direct Sales, Offline Retail, Online Retail, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC- China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Stanley Black & Decker, Inc., Techtronic Industries (TTI), Robert Bosch GmbH, Makita Corporation, Hilti Corporation, Snap-on Incorporated, Atlas Copco AB, Emerson Electric Co., Apex Tool Group, LLC, Koki Holdings Co., Ltd., Ingersoll Rand Inc., Festool Group GmbH & Co. KG, Husqvarna AB, Chevron Corporation (Enerpac), Hitachi Koki Co., Ltd., Others |

| Customization Scope | Customization for segments and region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |