Quick Navigation

Report Overview

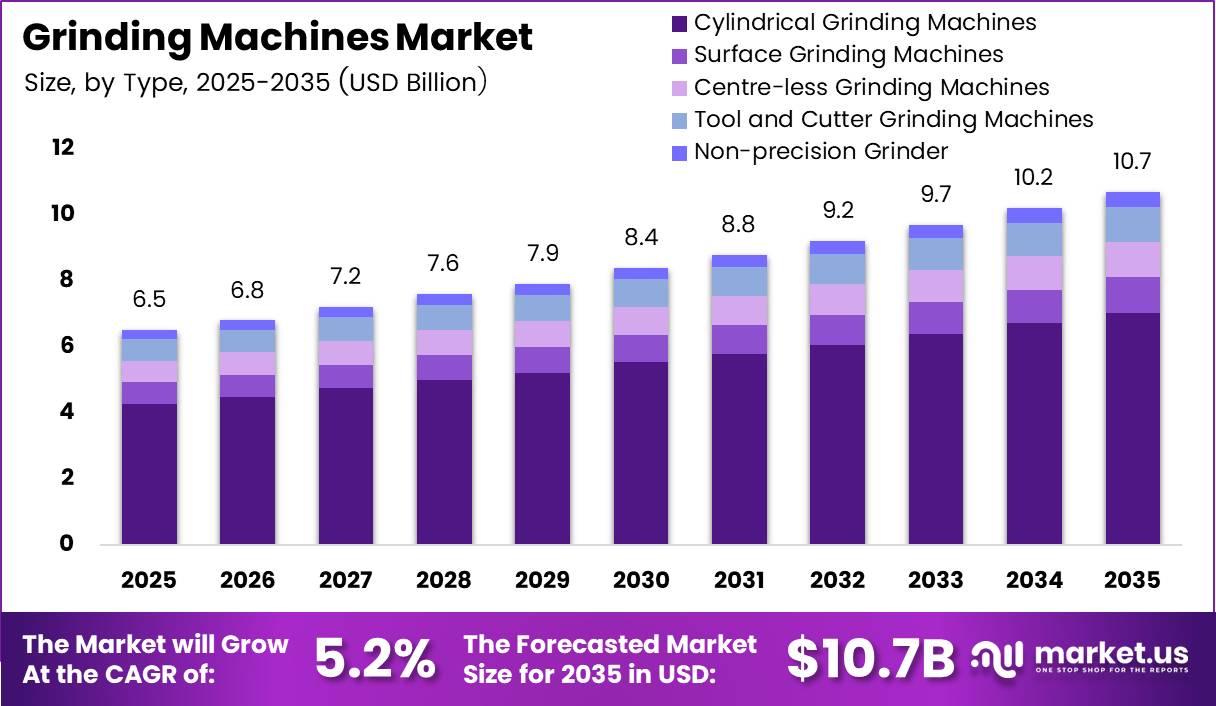

Global Grinding Machines Market size is expected to be worth around USD 10.7 Billion by 2035 from USD 6.5 Billion in 2025, growing at a CAGR of 5.2% during the forecast period 2026 to 2035. This trajectory reflects sustained capital investment in precision manufacturing across multiple end-use industries. Buyers and investors should treat this as a structurally driven market, not a cyclical one.

Grinding machines are precision material-removal tools that shape, finish, and size components to exact tolerances. The market spans cylindrical, surface, centerless, and tool and cutter grinding platforms. These machines serve industries where dimensional accuracy and surface quality are non-negotiable production requirements.

The market structure divides into precision and non-precision segments. Precision grinders serve high-tolerance sectors such as automotive, aerospace, and medical. Non-precision grinders, including bench, portable, and pedestal variants, serve general industrial and construction applications. This split means suppliers must maintain distinct go-to-market strategies for each buyer class.

Government investment in domestic manufacturing capacity is reshaping procurement patterns for grinding equipment. Industrial policy programs across Asia, Europe, and North America are directing capital toward high-value manufacturing infrastructure. Suppliers positioned near government-backed production clusters hold a structural sourcing advantage over distant competitors.

Regulatory pressure on energy consumption is tightening across major manufacturing economies. Equipment buyers now face mandatory efficiency benchmarks that older grinding platforms cannot meet. This creates a replacement cycle that benefits suppliers offering certified low-energy grinding solutions with documented performance data.

In February 2026, EMAG introduced the UG Series universal grinding machines, combining internal, external, and out-of-round grinding in one platform. This signals that the market is moving toward multi-function platforms that reduce floor space and changeover time. Buyers consolidating equipment lines will prioritize vendors offering this kind of platform versatility.

According to available research, quality-control automation in manufacturing, including robotic grinding and finishing cells, can lower quality costs by 20% or more and reduce defects by over 30%. This performance gap between automated and manual grinding lines is widening. Suppliers who integrate automation-ready interfaces into their grinding platforms will capture share from buyers managing tighter quality tolerances.

Key Takeaways

- Global Grinding Machines Market was valued at USD 6.5 Billion in 2025.

- Market forecast value reaches USD 10.7 Billion by 2035.

- CAGR of 5.2% is projected across the forecast period 2026 to 2035.

- Asia Pacific dominates with a 46.9% market share, valued at USD 3.0 Billion.

- By Type, Cylindrical Grinding Machines hold the dominant share at 65.8%.

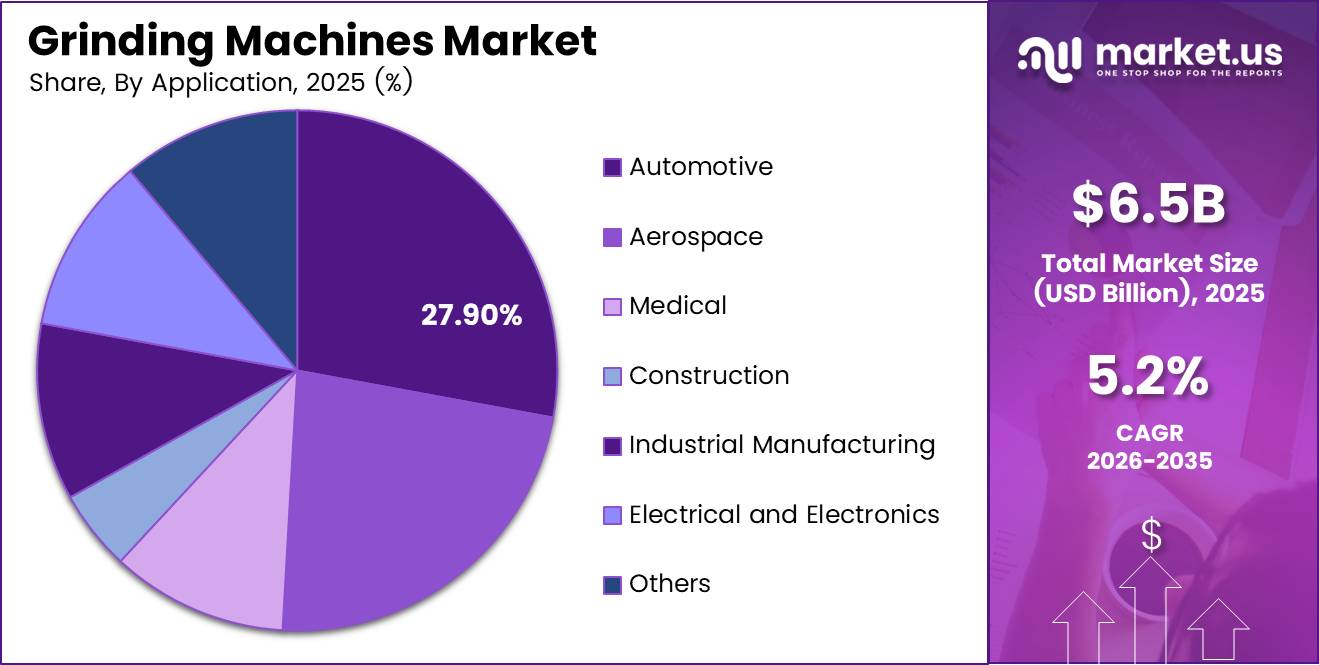

- By Application, Automotive leads with a 27.90% segment share.

- Intelligent drive systems reduce grinding machine energy consumption by approximately 25%.

- Quality-control automation in grinding and finishing operations reduces defects by over 30%.

Type Analysis

Cylindrical Grinding Machines dominates with 65.8% due to widespread use in automotive and aerospace precision finishing.

In 2025, Cylindrical Grinding Machines held a dominant market position in the By Type segment of the Grinding Machines Market, with a 65.8% share. This dominance reflects the machine type’s ability to finish round and tubular components to tight tolerances demanded by automotive and aerospace buyers. Research on D3 tool steel cylindrical grinding confirms achievable surface roughness values as low as 0.41177 µm under optimized parameters, a performance benchmark that sustains buyer preference for this platform over competing types.

Surface Grinding Machines serve flat-surface finishing requirements across tool and die, mold making, and precision component production. Buyers in these segments require consistent flatness and parallelism across large workpiece areas. This functional specificity limits cross-substitution with cylindrical platforms and supports a stable independent demand base for surface grinding equipment.

Centerless Grinding Machines enable high-volume finishing of cylindrical components without the need for centers or fixtures, which reduces setup time and labor cost per part. For applications where depth of cut optimization is the primary lever for improving material removal rate at fixed tool life, centerless platforms offer a direct productivity advantage. This positions centerless machines as the preferred choice in high-throughput industrial manufacturing environments.

Application Analysis

Automotive dominates with 27.90% due to high-volume precision component production requirements.

In 2025, Automotive held a dominant market position in the By Application segment of the Grinding Machines Market, with a 27.90% share. Automotive production requires tight-tolerance grinding for engine components, transmission parts, and brake systems across very high production volumes. The expansion of electric vehicle manufacturing is now adding new precision finishing requirements for motor shafts, rotor cores, and battery housing components, which extends the total addressable demand for grinding equipment within this segment.

Aerospace applications require grinding of advanced alloys, composites, and ceramic materials that conventional tooling cannot process reliably. Aerospace buyers apply stringent surface integrity standards that make machine selection a qualification decision, not purely a cost decision. This creates a high-barrier, low-churn customer base where suppliers with certified process capability hold durable pricing power.

Medical device manufacturing demands sub-micron surface finish quality on implant components, surgical tools, and diagnostic equipment parts. Buyers in this segment prioritize machine repeatability and traceability over throughput speed. Suppliers offering grinding platforms with integrated measurement and process documentation capabilities are better positioned to win and retain medical sector contracts.

Key Market Segments

By Type

- Cylindrical Grinding Machines

- Surface Grinding Machines

- Centre-less Grinding Machines

- Tool and Cutter Grinding Machines

- Non-precision Grinder

- Bench Grinder

- Portable Grinder

- Pedestal Grinder

- Flexible Grinder

- Precision Grinder

By Application

- Automotive

- Aerospace

- Medical

- Construction

- Industrial Manufacturing

- Electrical and Electronics

- Marine Industry

- Others

Regional Analysis

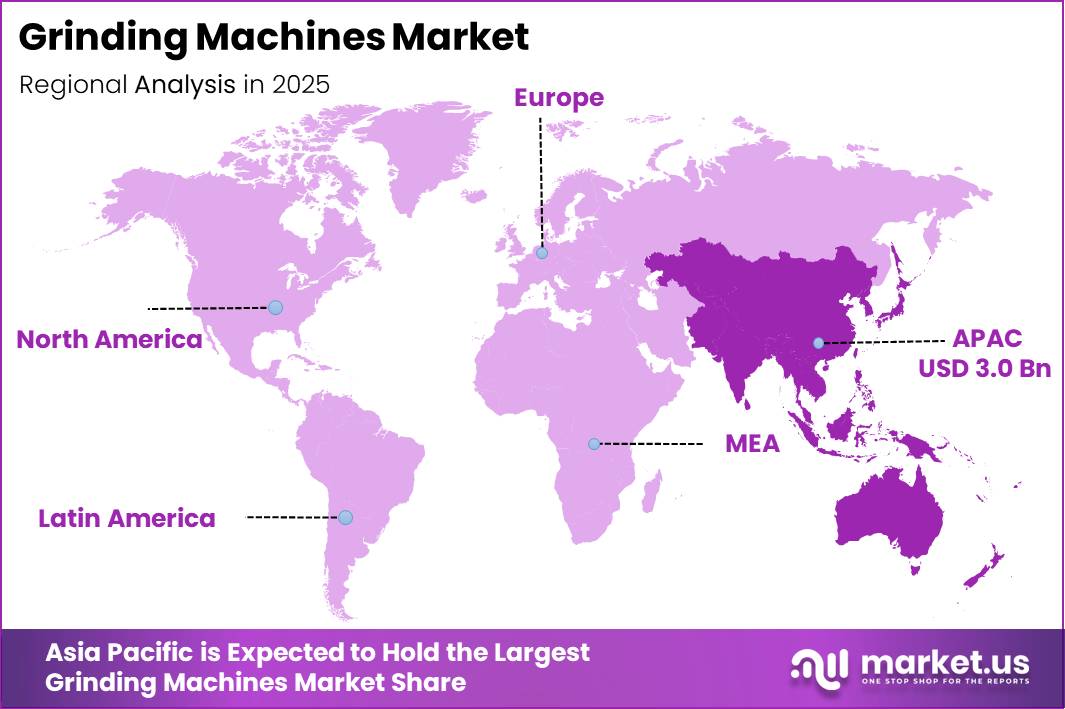

Asia Pacific Dominates the Grinding Machines Market with a Market Share of 46.9%, Valued at USD 3.0 Billion

Asia Pacific commands 46.9% of the global Grinding Machines Market, valued at USD 3.0 Billion in 2025. The region’s dominance is anchored by large-scale automotive and industrial manufacturing bases in China, Japan, South Korea, and India. Government-backed industrial expansion programs and high machine tool consumption rates sustain the region’s structural lead over all other geographies.

North America holds a significant share driven by demand from aerospace, automotive, and medical device manufacturing sectors. The United States remains the primary consumption center, supported by reshoring initiatives and capital investment in domestic precision manufacturing capacity. Buyers in this region increasingly specify energy-efficient and automation-compatible grinding platforms as part of facility upgrade programs.

Europe maintains a strong position supported by Germany’s established machine tool industry and the region’s concentration of high-precision automotive and aerospace suppliers. European buyers apply strict surface quality and environmental standards that favor advanced grinding platforms over older equipment. This regulatory environment accelerates equipment refresh cycles across the region’s manufacturing base.

Latin America represents a smaller but developing market, with Brazil and Mexico serving as primary consumption centers tied to their automotive assembly and general industrial sectors. Infrastructure investment gaps and import dependency on grinding equipment limit faster expansion. However, nearshoring trends in Mexico are beginning to attract precision manufacturing investment that will support grinding machine demand.

Middle East and Africa show early-stage grinding machine adoption concentrated in GCC countries pursuing industrial diversification under national economic development programs. South Africa contributes demand from its mining and metals processing sectors, where grinding equipment plays a direct role in mineral processing operations. Growth in this region depends heavily on continued public investment in non-oil industrial capacity.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

AMADA MACHINERY CO., LTD. positions itself through a broad precision machinery portfolio that spans sheet metal and grinding applications across Asian and global manufacturing markets. In July 2025, UNITED GRINDING completed its acquisition of GF Machining Solutions to form UNITED MACHINING SOLUTIONS, signaling sector-wide consolidation pressure. AMADA’s multi-category presence provides revenue diversification, but concentrated exposure to Asian manufacturing cycles creates downside sensitivity.

Danobat builds its competitive position around custom grinding solutions for demanding aerospace, railway, and energy sector applications. This specialization allows Danobat to command premium pricing and maintain long-term customer relationships in technically complex segments. However, dependence on capital-intensive end markets means order books are vulnerable to procurement pauses during economic slowdowns, creating revenue visibility risk for mid-cycle planning.

Key Players

- AMADA MACHINERY CO., LTD.

- Danobat

- ANCA

- Junker

- Körber AG

- Fives

- Rieter

- Saurer Intelligent Technology AG

- Murata Machinery USA

- LMW Limited

- Trützschler Group SE

Recent Developments

- June 2025 – UNITED GRINDING launched the WALTER VISION LASER machine, a new tool-processing platform combining laser technology with the HELITRONIC architecture for high-precision processing of PCD, CVD, diamond, and carbide tools.

- September 2025 – TECHCO Group acquired GST Grinder GmbH, a manufacturer of grinding machinery and precision metalworking solutions, supporting future expansion and investment in grinding machine technologies.

- September 2026 – STUDER unveiled the S23 universal cylindrical grinding machine, featuring the company’s C.O.R.E. architecture, automated B-axis functionality, and enhanced precision for cylindrical grinding operations.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 6.5 Billion |

| Forecast Revenue (2035) | USD 10.7 Billion |

| CAGR (2026-2035) | 5.2% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Cylindrical Grinding Machines, Surface Grinding Machines, Centre-less Grinding Machines, Tool and Cutter Grinding Machines, Non-precision Grinder, Precision Grinder); By Application (Automotive, Aerospace, Medical, Construction, Industrial Manufacturing, Electrical and Electronics, Marine Industry, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | AMADA MACHINERY CO., LTD., Danobat, ANCA, Junker, Körber AG, Fives, Rieter, Saurer Intelligent Technology AG, Murata Machinery USA, LMW Limited, Trützschler Group SE |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |