Quick Navigation

Report Overview

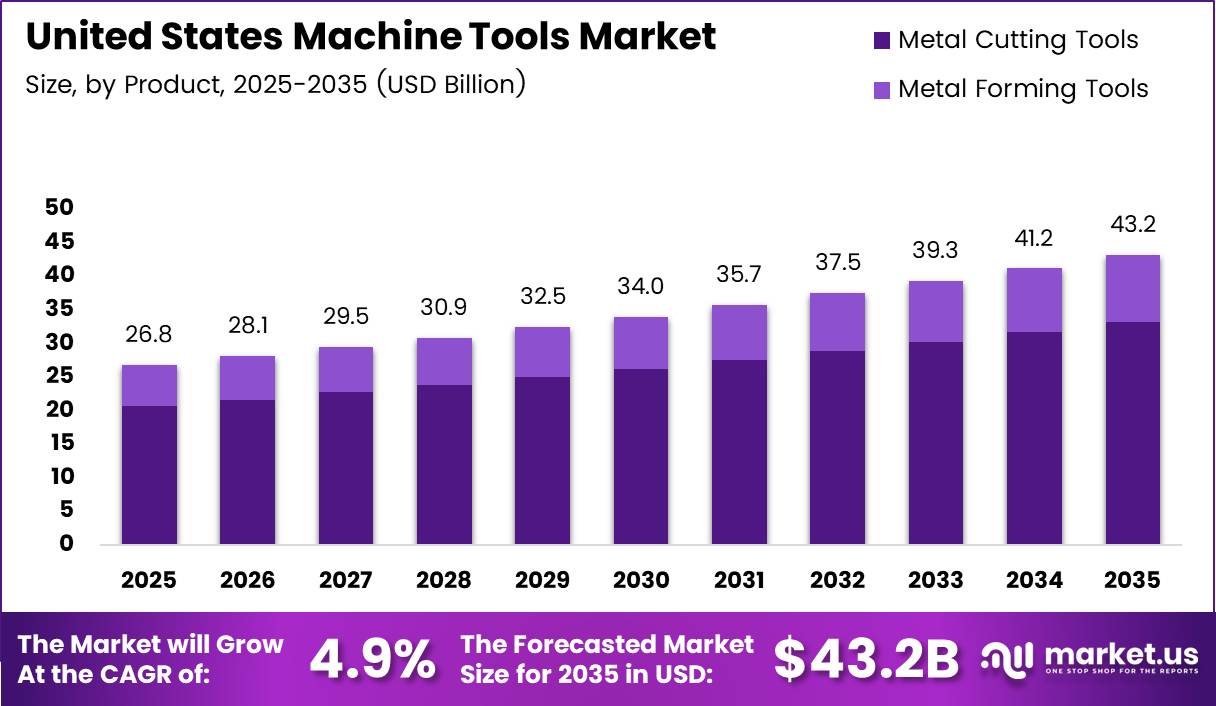

The United States Machine Tools Market size is expected to be worth around USD 43.2 Billion by 2035 from USD 26.8 Billion in 2025, growing at a CAGR of 4.9% during the forecast period 2026 to 2035.

The U.S. machine tools market covers precision equipment used to cut, form, grind, and shape metal and composite materials across industrial production. This includes CNC machining centers, lathes, milling machines, presses, and laser cutting systems deployed across automotive, aerospace, electronics, and industrial manufacturing facilities nationwide.

Reshoring of industrial production has restructured domestic capital equipment spending. U.S. manufacturers now prioritize advanced machining systems to replace offshore capacity, and this shift is creating sustained order volume for domestic and imported machine tool suppliers alike. The competitive advantage now belongs to vendors who can deliver precision and throughput simultaneously.

Electric vehicle manufacturing has introduced a distinct demand profile for machine tools. EV powertrain components — battery housings, motor casings, and structural chassis parts — require tighter tolerances than traditional internal combustion engine parts. This forces automotive buyers to upgrade entire machining lines, accelerating CNC adoption at scale.

Federal investment in domestic semiconductor and defense manufacturing has added a second procurement wave alongside EV-driven demand. Semiconductor fabrication equipment and precision aerospace components both require multi-axis CNC systems, creating order pipelines that extend well beyond the current forecast period.

In April 2026, Mills CNC showcased the HELLER HF 5500 5-axis machining centre at MACH 2026, featuring a direct-drive rotary tilting table and Siemens One control. This launch signals that 5-axis capability is becoming a baseline expectation for production-floor buyers, not a premium option.

According to AMT – The Association For Manufacturing Technology, cumulative new orders of metalworking machinery in the U.S. through June 2025 totaled USD 2.52 Billion, a 13.7% increase over the first half of 2024. This double-digit order growth confirms that manufacturers are committing capital, not just planning upgrades.

According to labor data compiled in 2025, 187,670 CNC tool operators were employed in the U.S. as of May 2023, with machine shops alone employing 40,520 of these operators. This embedded workforce creates structural inertia favoring CNC over conventional machines and signals long-term maintenance and tooling revenue for machine tool suppliers.

Key Takeaways

- The U.S. Machine Tools Market was valued at USD 26.8 Billion in 2025 and is forecast to reach USD 43.2 Billion by 2035.

- The market grows at a CAGR of 4.9% during the forecast period 2026 to 2035.

- By Product, Metal Cutting Tools dominate with a 76.3% share in 2025.

- By Technology, CNC Machines hold the largest share at 84.1% in 2025.

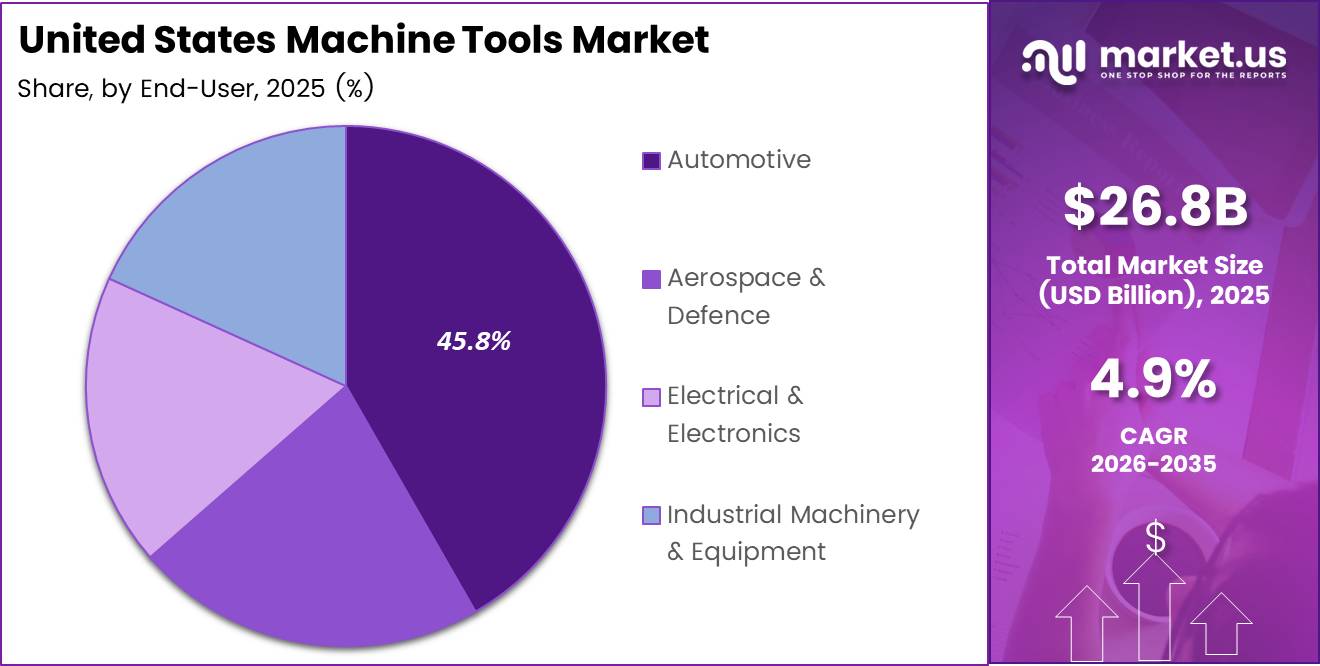

- By End-User, Automotive leads with a 45.8% share in 2025.

- Cumulative U.S. metalworking machinery orders through June 2025 reached USD 2.52 Billion, up 13.7% year-over-year.

- CNC machine tools account for 84.1% of technology adoption, reflecting the near-complete displacement of conventional machining in production environments.

Product Analysis

Metal Cutting Tools dominates with 76.3% due to broad multi-industry precision machining requirements.

In 2025, Metal Cutting Tools held a dominant market position in the By Product segment of the U.S. Machine Tools Market, with a 76.3% share. This dominance reflects the fundamental role of subtractive machining across automotive, aerospace, and electronics production, where dimensional accuracy drives component qualification and cannot be substituted by forming alternatives.

Metal Forming Tools serve high-volume, low-cycle-time production environments where speed outweighs the need for complex geometry. Press lines and forging machines operate at throughput rates that cutting machines cannot match, making forming tools the preferred choice for structural and body components in automotive and heavy equipment manufacturing.

Technology Analysis

CNC Machines dominate with 84.1% due to precision requirements across automotive and aerospace production.

In 2025, CNC Machines held a dominant market position in the By Technology segment of the U.S. Machine Tools Market, with an 84.1% share. According to data compiled in 2025, average CNC machine utilization stood at only 23.9% in Q4 2022, with monthly utilization ranging between 22% and 30%. This substantial idle capacity signals that productivity optimization — not capacity addition — is the primary commercial opportunity for CNC technology providers today.

Conventional Machines (manually or semi-manually operated) retain a presence in maintenance, repair, and low-volume custom work where CNC programming overhead exceeds the production benefit. However, their share is structurally declining as the skilled manual machinist workforce ages out and facilities favor automated systems that are less dependent on individual operator expertise.

Additive Manufacturing / Hybrid Machines combine subtractive and additive processes in a single platform, enabling net-shape metal deposition followed by precision CNC finishing within one machine cycle. Their adoption in aerospace and defense for near-net-shape complex parts is accelerating, but high per-unit cost and limited post-processing standards constrain near-term volume share.

End-User Analysis

Automotive dominates with 45.8% due to high-volume precision component machining requirements.

In 2025, Automotive held a dominant market position in the By End-User segment of the U.S. Machine Tools Market, with a 45.8% share. The shift to electric vehicle platforms has extended this dominance rather than disrupted it — EV powertrain components demand tighter tolerances than internal combustion parts, forcing automotive manufacturers to invest in higher-specification CNC machining lines across existing and new facilities.

Aerospace & Defence carries the highest per-machine revenue within the end-user mix. Titanium and nickel superalloy components for airframes, turbine blades, and structural assemblies require multi-axis CNC centers capable of sustained precision over long cutting cycles. Defense production mandates domestic sourcing, which concentrates aerospace machine tool demand within U.S. facilities and limits import substitution risk.

Electrical & Electronics manufacturing represents the fastest-shifting end-user segment as semiconductor facility construction accelerates under CHIPS Act provisions. Precision machining demand for wafer handling equipment, precision enclosures, and semiconductor tooling is creating a procurement wave that does not follow traditional automotive or aerospace buying cycles.

Industrial Machinery & Equipment manufacturers consume machine tools to produce their own equipment, creating a recursive demand relationship where industrial output growth amplifies machine tool orders. This segment’s appetite for general-purpose machining centers and flexible automation cells makes it the primary market for mid-tier machine tool vendors competing outside the high-precision aerospace tier.

Key Market Segments

By Product

- Metal Cutting Tools

- Milling Machines

- Drilling Machines

- Turning (Lathe) Machines

- Grinding Machines

- Laser Cutting Machines

- Electrical Discharge Machines (EDM)

- Waterjet Cutting Machines

- Plasma Cutting Machines

- Multi-Axis Machining Centres

- Others

- Metal Forming Tools

- Presses (Mechanical, Hydraulic, Servo)

- Forging Machines

- Bending Machines

- Others

By Technology

- CNC Machines

- Conventional Machines (Manually or Semi-Manually)

- Additive Manufacturing / Hybrid Machines

By End-User

- Automotive

- Aerospace & Defence

- Electrical & Electronics

- Industrial Machinery & Equipment

Drivers

Reshoring, EV Production, and Defense Spending Converge to Drive CNC Machine Tool Demand

U.S. manufacturers are accelerating reshoring across automotive, aerospace, and electronics sectors, directly increasing domestic capital equipment procurement. Each new production facility requires a full machining line, and buyers are specifying CNC systems rather than conventional machines from the outset. This procurement pattern creates durable, multi-year order pipelines for machine tool suppliers. In April 2024, Accurl USA LLC partnered with Complete Machine Tools to expand its U.S. portfolio, reflecting supplier-side repositioning to capture this reshoring-driven demand.

Electric vehicle production has reshaped machine tool specifications across automotive supply chains. EV battery enclosures, motor housings, and structural castings require tighter dimensional tolerances than conventional drivetrain components, compelling manufacturers to replace legacy machining lines with higher-precision CNC systems. According to data compiled in 2025, AI applications in CNC machining cut cycle times by approximately 20%, directly increasing throughput per machine — a critical advantage for automotive buyers managing high-volume production targets.

Expansion of aerospace and defense manufacturing sustains demand for multi-axis precision machining systems that no conventional machine can substitute. Defense contracts mandate domestic production, concentrating this demand within U.S. facilities. Additionally, automation in metal fabrication reduces reliance on skilled manual labor, making CNC investment a workforce risk management strategy as much as a productivity decision.

Restraints

High CNC Procurement Costs and Component Supply Vulnerabilities Limit Broad Market Penetration

Multi-axis CNC machining centers carry six-figure price tags that place them beyond the capital budgets of most small and mid-sized manufacturers. This cost barrier fragments the market — large automotive and aerospace primes upgrade continuously while smaller job shops delay replacement cycles for five to ten years. The result is a bifurcated installed base where productivity gains concentrate at the top of the market.

Supply chain disruptions affecting critical machine tool components — precision ball screws, linear guides, spindle bearings, and CNC control units — introduce lead time uncertainty that undermines project planning for facility operators. When component availability is unreliable, buyers defer procurement decisions or hold aging equipment longer than intended, creating gaps in order flow that machine tool manufacturers cannot offset through pricing alone.

The combination of high upfront cost and component supply risk compounds the adoption barrier for smaller manufacturers. Without access to equipment financing or government incentive programs, SME manufacturers face a structural disadvantage versus larger peers who can absorb capital expenditure across wider revenue bases. This restraint is most acute in secondary manufacturing regions where supplier networks are thinner and financing options are fewer.

Growth Factors

Industry 4.0 Integration, Additive Hybrid Technologies, and Semiconductor Expansion Create New Revenue Streams

Smart manufacturing investment is embedding connectivity and data analytics directly into machine tool procurement requirements. Buyers now specify IoT-ready CNC systems as standard, creating aftermarket opportunities in sensors, software platforms, and predictive maintenance services. According to a 2025 AI-driven maintenance benchmark, deploying predictive maintenance on manufacturing equipment reduces downtime by up to 50% and cuts maintenance costs by 10–40% — quantifying the ROI that drives smart machine tool adoption.

Additive manufacturing hybrid machines open a new product tier that did not exist in the conventional machine tool market five years ago. These systems enable manufacturers to deposit near-net-shape metal and finish-machine in a single setup, reducing material waste and fixturing cost on complex aerospace components. In January 2024, ModuleWorks announced a partnership with DN Solutions to develop integrated machine tool software enabling digital transformation of manufacturing — signaling that software-hardware convergence is accelerating in this segment.

Semiconductor fabrication facility expansion under CHIPS Act provisions is generating precision equipment demand that differs from automotive or aerospace buying patterns. Wafer handling equipment and semiconductor tooling require extreme cleanliness and dimensional control, creating a high-specification niche for machine tool suppliers with cleanroom-compatible product lines. Medical device manufacturing is adding parallel demand for customized machining solutions across implant and surgical instrument production.

Emerging Trends

Digital Twin Integration and Cloud-Based CNC Monitoring Redefine Machine Tool Performance Management

Digital twin technology is shifting machine tool performance management from reactive maintenance to continuous virtual simulation. Manufacturers use digital replicas of CNC machines to test process parameters, predict wear patterns, and validate toolpaths before committing cutting time. According to a 2025 review, optimizing machining parameters — cutting speed, feed rate, and depth of cut — reduces machine tool energy consumption by 10–30%, and digital twin platforms are the primary mechanism manufacturers use to identify these optimization windows at scale.

Cloud-based CNC monitoring platforms enable remote diagnostic access across distributed machine fleets, shifting machine tool service models from scheduled visits to continuous remote oversight. This creates a recurring revenue opportunity for machine tool OEMs and independent service providers who embed monitoring contracts alongside equipment sales. The operational implication is that machine tool vendors who offer connected service platforms will retain customers beyond the initial sale.

Energy-efficient and compact machining systems address dual pressures from rising industrial electricity costs and urban factory footprint constraints. Buyers in dense manufacturing zones favor machines that deliver equivalent output within smaller floor envelopes. Collaborative robotics integration in automated machining environments extends this compact-factory trend by replacing dedicated transfer equipment with flexible robot arms that serve multiple machines from a single installation.

Key Company Insights

Haas Automation holds a structural advantage in the U.S. machine tools market through its domestic manufacturing model — every machine is built in Oxnard, California. This positions Haas favorably amid reshoring-driven procurement policies and defense supply chain requirements that favor U.S.-origin capital equipment. Its vertically integrated production also insulates the company from the component lead time disruptions that affect import-dependent competitors.

TRUMPF Inc. competes at the premium end of laser cutting and sheet metal fabrication systems, where its technology depth in fiber laser power and automation integration justifies price premiums versus mid-market alternatives. TRUMPF’s strength in connected manufacturing platforms aligns directly with industrial buyers prioritizing Industry 4.0 compliance, giving it an advantage in enterprise accounts that evaluate total operational cost rather than capital price alone.

DMG MORI USA leverages its global parent’s R&D scale to deliver a comprehensive portfolio spanning horizontal machining centers, turning centers, and ultrasonic hybrid systems. Its combination of German engineering pedigree and Japanese manufacturing precision targets the aerospace and medical device segments where material removal consistency determines component qualification outcomes. DMG MORI’s service infrastructure across North America supports its installed base retention strategy.

Mazak Corp. differentiates through its multi-tasking machine platform — Integrex series machines that combine turning, milling, and grinding in a single setup. For aerospace and energy sector buyers managing complex part geometries, this capability reduces in-process handling and fixturing cost, directly lowering per-part cost. Mazak’s Florence, Kentucky manufacturing facility also positions it as a domestically produced option in an environment where supply chain origin increasingly influences procurement decisions.

Key Players

- Haas Automation

- TRUMPF Inc.

- DMG MORI USA

- Mazak Corp.

- Okuma America

- Amada America

- Lincoln Electric

- Hardinge Inc.

- Hurco Companies

- Fives Machining Systems

Recent Developments

- February 2024 — DN Solutions entered a strategic agreement with ModuleWorks, a leading CAD/CAM software provider, involving investment and collaborative business efforts to develop next-generation machine tool software, accelerating the digital transformation of CNC manufacturing workflows.

- October 2024 — Kapitus acquired Ten Oaks Commercial Capital and launched its equipment finance arm to accelerate funding support for U.S. manufacturing industries, with on-balance-sheet transactions commencing in early 2025, expanding capital access for machine tool procurement across small and mid-sized manufacturers.

- April 2025 — Citizen Machinery Co., Ltd. introduced the third-generation Cincom L20-LFV series sliding-head lathes within its CNC automatic lathe lineup, delivering enhanced low-frequency vibration cutting capability for precision small-diameter component production in medical and electronics manufacturing.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 26.8 Billion |

| Forecast Revenue (2035) | USD 43.2 Billion |

| CAGR (2026-2035) | 4.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Metal Cutting Tools, Metal Forming Tools), By Technology (CNC Machines, Conventional Machines, Additive Manufacturing / Hybrid Machines), By End-User (Automotive, Aerospace & Defence, Electrical & Electronics, Industrial Machinery & Equipment) |

| Competitive Landscape | Haas Automation, TRUMPF Inc., DMG MORI USA, Mazak Corp., Okuma America, Amada America, Lincoln Electric, Hardinge Inc., Hurco Companies, Fives Machining Systems |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |