Quick Navigation

- Report Overview

- Key Takeaways

- Tool Type Analysis

- Material Grade Analysis

- Production Process Analysis

- End-user Analysis

- Distribution Channel Analysis

- Key Market Segments

- Drivers

- Restraints

- Growth Factors

- Emerging Trends

- Regional Analysis

- Key Regions and Countries

- Key Company Insights

- Recent Developments

- Report Scope

Report Overview

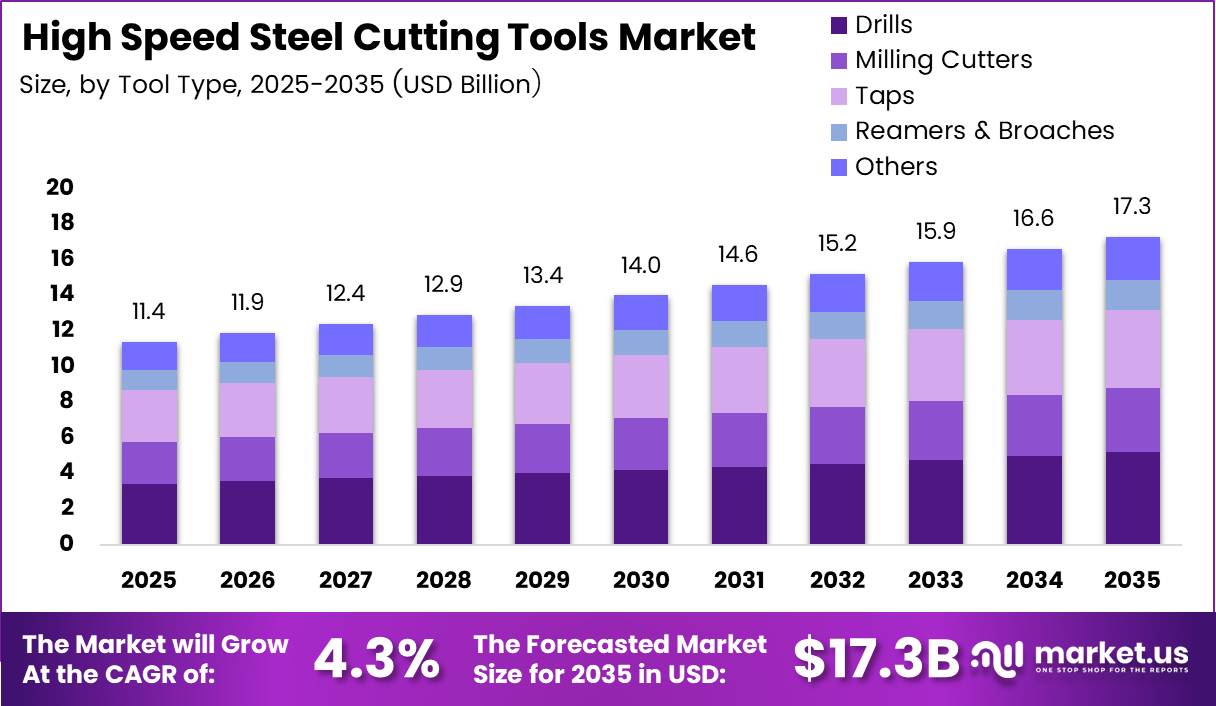

Global High Speed Steel Cutting Tools Market size is expected to be worth around USD 17.3 Billion by 2035 from USD 11.4 Billion in 2025, growing at a CAGR of 4.3% during the forecast period 2026 to 2035.

High speed steel cutting tools form the backbone of general-purpose machining across automotive, aerospace, and industrial manufacturing sectors. These tools offer a practical balance of toughness, heat resistance, and re-sharpenability. Their durability under variable load conditions makes them a default choice for small and medium manufacturers running mixed-material production lines.

The 4.3% CAGR reflects steady, structurally supported expansion rather than a speculative spike. Manufacturing output growth across Asia, Africa, and Latin America is pulling new volumes of HSS tooling into markets where carbide alternatives remain cost-prohibitive. This dynamic creates durable demand that resists the kind of cyclical correction seen in premium tooling segments.

Government investment in domestic manufacturing infrastructure directly benefits HSS tool producers. India’s Production Linked Incentive schemes for engineering goods and China’s continued expansion of precision machining capacity both increase tool consumption volumes. These policy-backed production floors reduce demand volatility for HSS suppliers serving those regions.

The expansion of small and medium-sized manufacturing enterprises further reinforces this market’s resilience. SMEs consistently prefer HSS tools over carbide alternatives due to lower per-unit cost and compatibility with general-purpose machines. This buyer segment is structurally price-sensitive, and HSS tools hold a competitive advantage at this end of the market.

According to Zhonghuantools, M35 cobalt HSS drills enabled a 50% increase in operational cutting speed when machining stainless steel, raising throughput from 12 meters per minute to 18 meters per minute. This performance gap versus standard M2 HSS confirms that premium HSS grades retain a strong technical case in demanding applications, justifying continued investment in cobalt-alloyed tool development.

According to Zhonghuantools, standard M2 HSS drill bits achieve an optimal cutting speed of 80 meters per minute when machining aluminum. This figure signals that HSS tooling remains technically competitive for non-ferrous applications, which represent a substantial share of automotive component machining. Buyers operating in these segments have limited incentive to migrate fully to carbide at current price differentials.

Key Takeaways

- The Global High Speed Steel Cutting Tools Market was valued at USD 11.4 Billion in 2025 and will reach USD 17.3 Billion by 2035.

- The market advances at a CAGR of 4.3% from 2026 to 2035.

- Asia Pacific leads all regions with a 43.70% market share, valued at USD 4.9 Billion.

- By Tool Type, Drills dominate with a 37.5% share in 2025.

- By Material Grade, Conventional HSS (M-Series) holds the largest share at 45.2%.

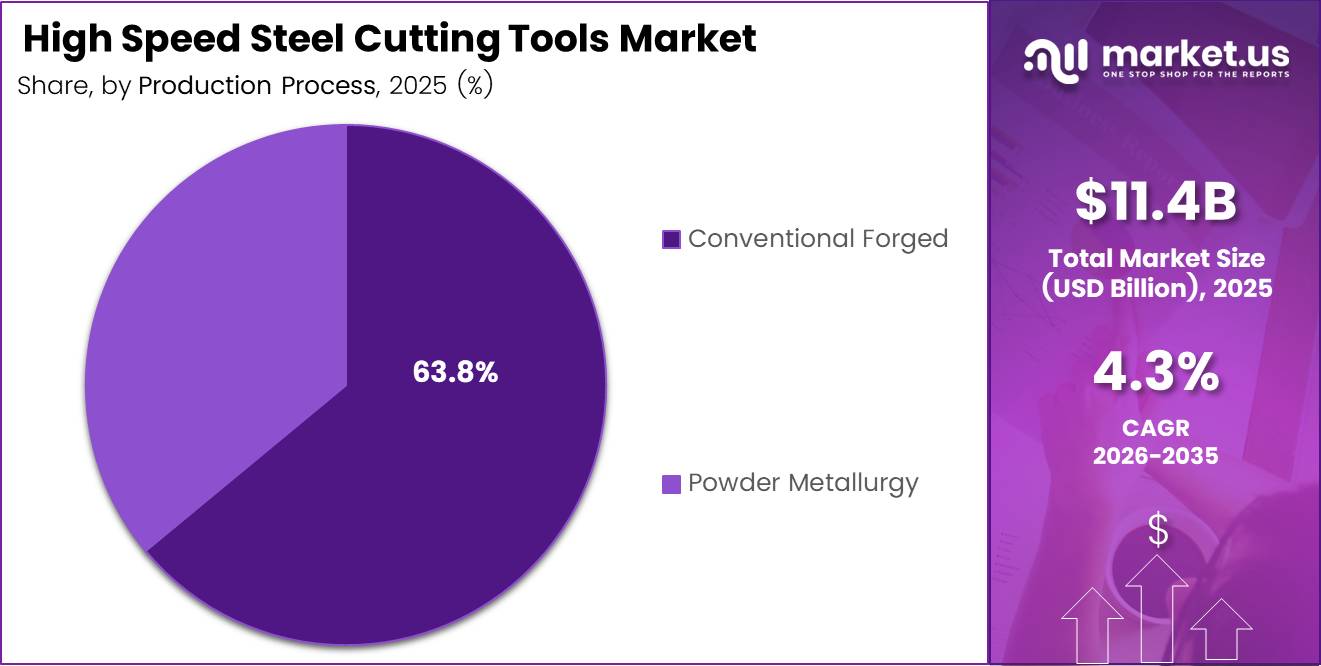

- By Production Process, Conventional Forged leads with a 63.8% share.

- By End-user, Manufacturing & Automotive accounts for 49.6% of total demand.

Tool Type Analysis

Drills dominate with 37.5% due to universal use across all machining operations.

In 2025, Drills held a dominant market position in the By Tool Type segment of the High Speed Steel Cutting Tools Market, with a 37.5% share. Drilling is the most fundamental metalworking operation, performed across every manufacturing sector regardless of production scale. This universal applicability locks in consistent HSS drill demand that other tool categories cannot match.

Milling Cutters serve face milling, slotting, and contouring operations across aerospace and automotive body manufacturing. These tools handle complex geometric profiles that drills cannot address. HSS milling cutters remain preferred for lower-volume production runs where carbide tooling costs are difficult to justify against per-part economics.

Taps produce internal threads in workpieces across a broad range of materials and component sizes. Thread-cutting volumes scale directly with fastener-intensive assembly industries such as automotive and heavy equipment manufacturing. HSS taps maintain relevance due to their toughness in interrupted cuts, where brittle carbide alternatives carry a higher breakage risk.

Reamers & Broaches address precision finishing and complex profile cutting requirements that standard drilling cannot achieve. Reamers enlarge and finish pre-drilled holes to tight tolerances, while broaches cut internal keyways and gear profiles. Both tool types serve specialized manufacturing applications where dimensional accuracy directly affects component assembly quality.

Others in the Tool Type segment include form tools, thread chasers, and countersinks serving niche finishing and assembly applications. These tools generate smaller aggregate volumes but carry higher per-unit value due to custom geometry requirements. Specialty toolmakers serving this sub-segment typically operate on shorter production runs with stronger margin profiles.

Material Grade Analysis

Conventional HSS (M-Series) dominates with 45.2% due to lowest cost and widest machine compatibility.

In 2025, Conventional HSS (M-Series) held a dominant market position in the By Material Grade segment of the High Speed Steel Cutting Tools Market, with a 45.2% share. M-Series grades offer a well-understood performance profile at a price point accessible to general manufacturing. Their compatibility with standard grinding equipment means machine shops can maintain and regrind tools in-house, reducing total tooling cost.

High-Cobalt HSS (T-Series/M42/M35) targets applications where standard M-Series grades fail under elevated heat and cutting stress. The cobalt addition raises red hardness, allowing these grades to sustain performance in stainless steel, titanium, and heat-resistant alloy machining. According to Zhonghuantools, M35 cobalt HSS enables a 50% increase in cutting speed over standard M2 when machining stainless steel, confirming the grade’s technical superiority in demanding applications.

Powder-Metallurgy HSS (PM-HSS) represents the premium tier within the HSS category. The PM process delivers a more uniform carbide distribution, producing tools with superior toughness and wear resistance compared to conventionally melted grades. PM-HSS commands higher unit pricing but extends tool life significantly in high-volume production environments, improving cost-per-part economics for large manufacturers.

Production Process Analysis

Conventional Forged dominates with 63.8% due to lower production cost and established toolmaker infrastructure.

In 2025, Conventional Forged held a dominant market position in the By Production Process segment of the High Speed Steel Cutting Tools Market, with a 63.8% share. Traditional forging and machining infrastructure is well-established across toolmaking regions in Europe and Asia. Conventional forged tools satisfy the performance requirements of the majority of general machining applications at lower production cost than PM alternatives.

Powder Metallurgy production delivers superior microstructure uniformity not achievable through conventional melting and forging. PM-produced HSS tools show better dimensional stability, higher toughness, and longer operational life. According to JLCCNC, HSS tools in CNC mild steel machining operate at 30 to 40 meters per minute, and PM-HSS variants sustain this performance range more consistently over longer production cycles than conventionally forged equivalents.

End-user Analysis

Manufacturing & Automotive dominates with 49.6% due to highest volume of repetitive metal cutting operations.

In 2025, Manufacturing & Automotive held a dominant market position in the By End-user segment of the High Speed Steel Cutting Tools Market, with a 49.6% share. Automotive production lines consume HSS cutting tools at scale for engine block drilling, gear cutting, and body component machining. The sector’s relentless focus on cost-per-part efficiency reinforces HSS’s position against premium tooling alternatives in high-volume general machining.

Oil & Gas operations require cutting tools capable of machining pressure vessels, valve bodies, and pipeline fittings from tough alloy steels. According to Otaisteel, the recommended HSS cutting speed for 4140 steel falls between 60 and 100 Surface Feet per Minute, confirming HSS’s technical suitability for the tough alloy steels central to this sector’s component base.

Mining & Quarrying uses HSS cutting tools for equipment maintenance, component fabrication, and spare parts machining in remote locations where supply chains for premium tooling are unreliable. HSS tools’ re-sharpenability makes them operationally practical where regrinding facilities are available on-site. This operational resilience sustains HSS demand in extractive industries globally.

Agriculture, Fishing & Forestry equipment manufacturers use HSS cutting tools in the production of wear-resistant components for tractors, harvesters, and marine equipment. Machining volumes in this segment are lower than automotive, but tool life demands are high due to the abrasive materials processed. HSS tools with surface coatings serve this segment’s durability requirements at competitive cost.

Construction equipment manufacturing consumes HSS tooling in the machining of structural components, hydraulic parts, and ground-engaging attachments. Construction sector output directly correlates with infrastructure spending cycles, making HSS tool demand in this end-user segment sensitive to government capital expenditure programs in developing economies.

Healthcare & Pharmaceutical equipment manufacturers use HSS cutting tools in precision machining of surgical instruments, implant components, and equipment housings from stainless steel and titanium alloys. Tolerances in this segment are tight and surface finish requirements are strict. High-cobalt HSS grades serve this segment by maintaining cutting edge integrity through hardened biomedical-grade materials.

Energy Generation (Turbines & Nuclear) requires precision machining of turbine blades, rotor shafts, and reactor vessel components from nickel superalloys and specialty steels. HSS tools serve maintenance and repair operations in this segment, where replacement component volumes are lower but precision requirements are critical. PM-HSS grades with cobalt additions are the preferred choice for these demanding applications.

Others in the end-user segment include defense, electronics manufacturing, and rail transport sectors with specialized machining requirements. These sectors represent smaller individual volumes but collectively contribute meaningful demand for specialty HSS grades. Defense procurement cycles, in particular, generate periodic high-volume tool consumption during equipment production programs.

Distribution Channel Analysis

Direct OEM Sales connects major tool manufacturers directly to large industrial buyers such as automotive OEMs, aerospace primes, and industrial equipment producers. This channel delivers the highest per-transaction value and enables customized tooling solutions negotiated at the account level. Direct relationships also allow tool manufacturers to gather application data that informs product development for specialized grades.

Industrial Distributors serve the mid-market and SME manufacturing base that lacks the volume to qualify for direct OEM pricing. Distributors maintain local inventory positions across tool types, grades, and sizes, reducing lead times for buyers with variable demand patterns. This channel accounts for a large share of HSS tool transactions by volume due to the fragmented nature of the SME manufacturing segment.

E-commerce/DIY Retail channels supply HSS tools to small workshops, maintenance operations, and individual fabricators. Online platforms have reduced friction in tool procurement for low-volume buyers, expanding the addressable retail market for standard HSS drill bits, taps, and end mills. Growth in this channel reflects broader digitization of industrial procurement among micro and small enterprises.

Key Market Segments

By Tool Type

- Drills

- Milling Cutters

- Taps

- Reamers & Broaches

- Others

By Material Grade

- Conventional HSS (M-Series)

- High-Cobalt HSS (T-Series/M42/M35)

- Powder-Metallurgy HSS (PM-HSS)

By Production Process

- Conventional Forged

- Powder Metallurgy

By End-user

- Manufacturing & Automotive

- Oil & Gas

- Mining & Quarrying

- Agriculture, Fishing & Forestry

- Construction

- Healthcare & Pharmaceutical

- Energy Generation (Turbines & Nuclear)

- Others

By Distribution Channel

- Direct OEM Sales

- Industrial Distributors

- E-commerce/DIY Retail

Drivers

Aerospace, Automotive, and Industrial Precision Machining Requirements Sustain High-Volume HSS Tool Consumption

Precision machining volumes in aerospace and automotive manufacturing directly set the consumption floor for HSS cutting tools. These sectors demand consistent dimensional accuracy across millions of components per production cycle. HSS tools deliver the toughness and re-sharpenability required for sustained high-output drilling, tapping, and milling across diverse alloy families.

According to MIT OpenCourseWare, HSS cutting tools lose their hardness when operational temperatures reach 600 degrees Celsius. This thermal limit is a critical engineering parameter for process engineers. Manufacturers designing cutting parameters below this threshold can operate HSS tools reliably across general machining tasks, sustaining demand in applications where cutting speeds remain within the tool’s thermal range.

In Q2 2024, Kennametal launched its KOR 5™ High-Speed Steel End Mills engineered for aerospace manufacturing applications. This product release confirms that leading toolmakers continue investing in HSS-grade innovation for high-value sectors rather than abandoning the category to carbide. The aerospace sector’s continued acceptance of advanced HSS confirms that well-engineered HSS grades retain a defensible position in precision manufacturing.

Restraints

Carbide, Ceramic, and CBN Tool Penetration Displaces HSS in High-Performance Machining Applications

Advanced cutting tool materials are displacing HSS in applications demanding higher speed, longer tool life, and tighter tolerances. Carbide, ceramic, and CBN tools operate at cutting speeds and temperatures far beyond the thermal limits of HSS. This technical gap is widening as manufacturers upgrade their machine tools to higher-speed platforms that carbide tooling is better positioned to exploit.

According to Zhonghuantools, standard M2 HSS tools demonstrate a recommended cutting speed of 25 meters per minute on carbon and mild steel. At this speed ceiling, carbide equivalents operate at multiples of this figure on the same materials. The speed differential creates a direct productivity disadvantage for HSS in high-throughput production environments where cycle time reductions translate directly into cost savings.

Tungsten, molybdenum, and vanadium price volatility adds a second layer of structural pressure. These elements are essential to HSS alloy composition, and their commodity pricing is subject to supply disruptions from a concentrated set of producing countries. Input cost instability compresses manufacturer margins and can make HSS tools less price-competitive against carbide at certain points in the commodity cycle.

Growth Factors

Powder Metallurgy HSS Innovation and Emerging Market Manufacturing Expansion Create New Revenue Opportunities

Advanced powder metallurgy HSS grades with improved wear resistance open new application territory for HSS in segments previously dominated by carbide. PM-HSS tools close the performance gap with carbide in interrupted cutting, hard materials, and precision finish applications. This technical convergence allows HSS suppliers to compete in higher-value segments without abandoning their core cost-competitive position.

According to a 2025 academic study published in IJSATE, an HSS cutting tool operating at 255 rpm achieved a material removal rate of 35,342.4 cubic millimeters per minute in mild steel turning. This figure demonstrates that optimized HSS process parameters deliver competitive productivity. Process engineers who fine-tune HSS cutting conditions can extract manufacturing output comparable to more expensive tooling categories.

According to Tirapid, milling 304 stainless steel with HSS tooling at 70 to 100 Surface Feet per Minute preserves tool life and machining efficiency. Emerging manufacturing hubs in Southeast Asia and Africa increasingly process stainless steel components for export markets. These regions represent new consumption centers for HSS tools operating within technically validated speed ranges for high-demand engineering materials.

Emerging Trends

Surface-Coated HSS Tools and Smart Monitoring Technologies Are Redefining Tool Life Economics

Surface coatings such as TiN, TiAlN, and AlCrN are substantially extending HSS tool life by reducing friction and heat transfer at the cutting edge. Coated HSS tools address one of the category’s primary limitations without requiring a full migration to carbide. This coating technology allows manufacturers to extract greater output per tool, improving cost-per-part performance without capital investment in new tooling platforms.

According to IJSATE, under optimal 2025 machining parameters, an HSS cutting tool restricted tool wear to just 0.04 mm while maintaining a cutting zone temperature of 40.56 degrees Celsius. This level of wear control at a low operating temperature signals that process optimization and coating technology together can extend HSS tool life significantly. Manufacturers who invest in process discipline reduce tooling consumption and total cost of ownership.

In October 2024, nLIGHT unveiled its n finity and ProcessGUARD products targeting high-precision advanced metal fabrication and cutting solutions. Smart monitoring integration into machining environments allows operators to track tool wear in real time, enabling predictive replacement before quality degradation occurs. This capability reduces scrap rates and unplanned downtime, strengthening the business case for HSS tools in production environments where process control is a priority.

Regional Analysis

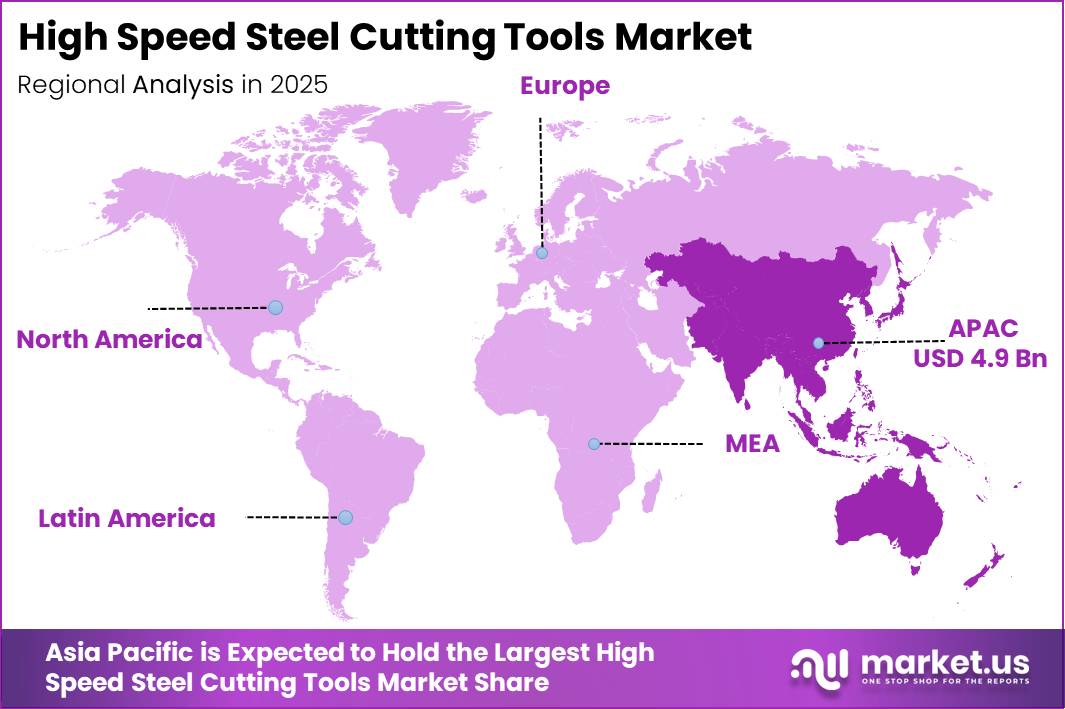

Asia Pacific Dominates the High Speed Steel Cutting Tools Market with a Market Share of 43.70%, Valued at USD 4.9 Billion

Asia Pacific commands 43.70% of global HSS cutting tool demand, generating USD 4.9 Billion in 2025. China, Japan, South Korea, and India collectively drive this concentration through their combined output in automotive, precision engineering, and general industrial manufacturing. Government-backed industrial expansion programs in China and India sustain tool consumption volumes that no other region can match in scale.

North America maintains a substantial share of global HSS tool demand through its aerospace, defense, and advanced manufacturing sectors. The US remains a significant consumer of premium HSS grades for precision component production. Reshoring trends in semiconductor equipment and defense manufacturing are sustaining domestic tooling procurement above pre-pandemic levels.

Europe houses a concentration of high-precision toolmaking and machining industries in Germany, Italy, and Sweden. German automotive and mechanical engineering sectors consume large HSS tool volumes in component manufacturing. European toolmakers also supply advanced PM-HSS and coated tool variants to global markets, positioning the region as both a consumer and a leading producer of premium HSS tooling.

Latin America’s HSS tool demand centers on Brazil and Mexico, driven by automotive assembly, mining equipment manufacturing, and agricultural machinery production. Both countries host large-scale manufacturing facilities supplying domestic and export markets. Ongoing investment in local manufacturing capacity by multinational automotive groups sustains predictable tooling consumption in these two leading markets.

The Middle East and Africa region shows structured demand in oil and gas equipment maintenance, infrastructure construction, and agricultural machinery fabrication. GCC countries consume HSS tooling in the maintenance and fabrication of hydrocarbon processing equipment. Sub-Saharan African manufacturing hubs are building out metalworking capacity, creating early-stage but structurally growing demand for cost-effective HSS cutting tools.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Sandvik AB operates as a vertically integrated cutting tool supplier with deep capabilities across HSS, carbide, and indexable tooling categories. Its February 2025 acquisition of shares in Suzhou Ahno and September 2025 full consolidation of Yongpu reflect a deliberate strategy to deepen manufacturing presence in China. These moves position Sandvik to serve Asia Pacific’s dominant demand base directly from within the region, reducing supply chain exposure and improving cost competitiveness.

Kennametal Inc. holds a strong position in advanced HSS and carbide tooling for aerospace and defense manufacturing. Its Q2 2024 launch of the KOR 5™ HSS End Mills signals continued commitment to premium HSS product development rather than a full pivot to carbide. This product strategy targets aerospace buyers who require tougher, more resilient cutting tools than carbide can offer in interrupted or variable-hardness machining environments.

OSG Corporation anchors its competitive positioning in high-precision threading, drilling, and end milling tools for automotive and electronics manufacturers. OSG’s Japanese engineering heritage gives it deep process knowledge in tight-tolerance applications across Asia’s densest manufacturing corridors. The company’s ability to serve both mass-production and specialty machining buyers across multiple tool categories reduces its exposure to segment-specific demand cycles.

Sumitomo Electric Industries Ltd. competes across HSS, carbide, and CBN tooling with a materials science foundation built through its broader advanced materials business. This cross-material capability allows Sumitomo to offer customers technically optimized solutions across the full cutting tool spectrum. Its position in energy generation and healthcare manufacturing segments gives it exposure to technically demanding end-users who prioritize tool performance over unit price.

Key Players

- Sandvik AB

- Kennametal Inc.

- OSG Corporation

- Sumitomo Electric Industries Ltd.

- Nachi-Fujikoshi Corp.

- Walter AG

- Erasteel SAS

- Mitsubishi Materials Corp.

- Guhring KG

- Dormer Pramet

- Niagara Cutter LLC

- Arch Cutting Tools

Recent Developments

- July 2024 – ARCH Cutting Tools Corp. acquired O-D Tool & Cutter Inc. for an undisclosed amount, significantly expanding its product offerings in the high-performance precision tooling market.

- July 2024 – Yamawa officially launched a new line of high-speed steel threading taps to address diverse machining requirements and deliver advanced threading solutions to its global customer base.

- February 2025 – Sandvik AB strengthened its strategic market presence by utilizing call options to acquire shares in the tooling manufacturing company Suzhou Ahno, deepening its China manufacturing base.

- September 2025 – Sandvik AB further consolidated its industrial tooling operations by acquiring the remaining 28% of shares in Yongpu, completing full ownership of the Chinese tooling producer.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 11.4 Billion |

| Forecast Revenue (2035) | USD 17.3 Billion |

| CAGR (2026-2035) | 4.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Tool Type (Drills, Milling Cutters, Taps, Reamers & Broaches, Others), By Material Grade (Conventional HSS (M-Series), High-Cobalt HSS (T-Series/M42/M35), Powder-Metallurgy HSS (PM-HSS)), By Production Process (Conventional Forged, Powder Metallurgy), By End-user (Manufacturing & Automotive, Oil & Gas, Mining & Quarrying, Agriculture, Fishing & Forestry, Construction, Healthcare & Pharmaceutical, Energy Generation (Turbines & Nuclear), Others), By Distribution Channel (Direct OEM Sales, Industrial Distributors, E-commerce/DIY Retail) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Sandvik AB, Kennametal Inc., OSG Corporation, Sumitomo Electric Industries Ltd., Nachi-Fujikoshi Corp., Walter AG, Erasteel SAS, Mitsubishi Materials Corp., Guhring KG, Dormer Pramet, Niagara Cutter LLC, Arch Cutting Tools |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |