Quick Navigation

Report Overview

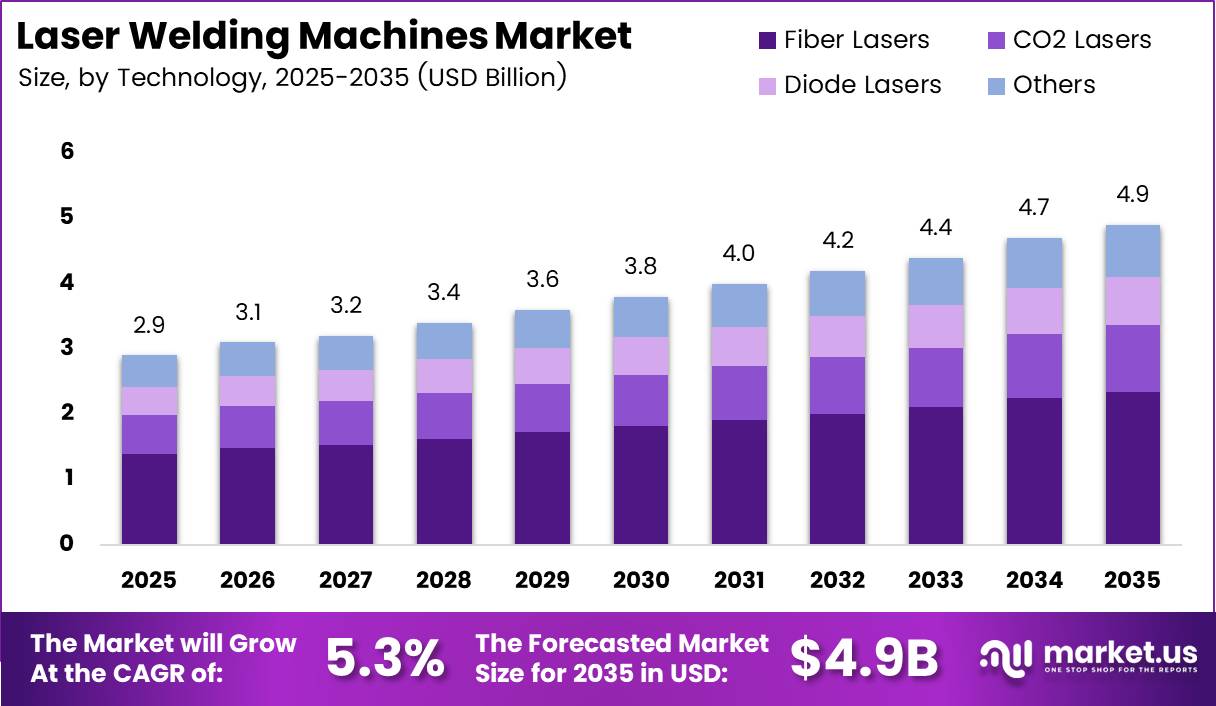

Global Laser Welding Machines Market size is expected to be worth around USD 4.9 Billion by 2035 from USD 2.9 Billion in 2025, growing at a CAGR of 5.3% during the forecast period 2026 to 2035.

Laser welding machines use focused light beams to join metals with precise heat control and minimal distortion. Unlike conventional arc welding, these systems deliver concentrated energy directly to the weld zone. This precision makes them the joining technology of choice across automotive, electronics, aerospace, and medical device manufacturing.

The automotive sector drives a substantial portion of global demand, particularly as electric vehicle production scales. EV battery module assembly requires consistent, defect-free busbar joints across hundreds of cells per pack. Laser systems meet this requirement where resistance welding and conventional arc processes cannot match the combination of speed, repeatability, and joint quality.

Fiber laser technology now holds 47.2% of the market by technology type, reflecting a structural shift away from CO2 and diode platforms. Fiber lasers offer higher wall-plug efficiency, lower maintenance overhead, and better beam quality at elevated power levels. This positions them as the default platform for new industrial installations across multiple end-use sectors.

The 3 kW–6 kW output range commands 39.6% of the by-output segment, confirming that mid-power systems balance versatility with cost for the broadest range of production tasks. These systems handle thin-gauge automotive stampings, medical implant components, and consumer electronics housings — sectors that collectively represent the largest installed base of laser welding cells globally.

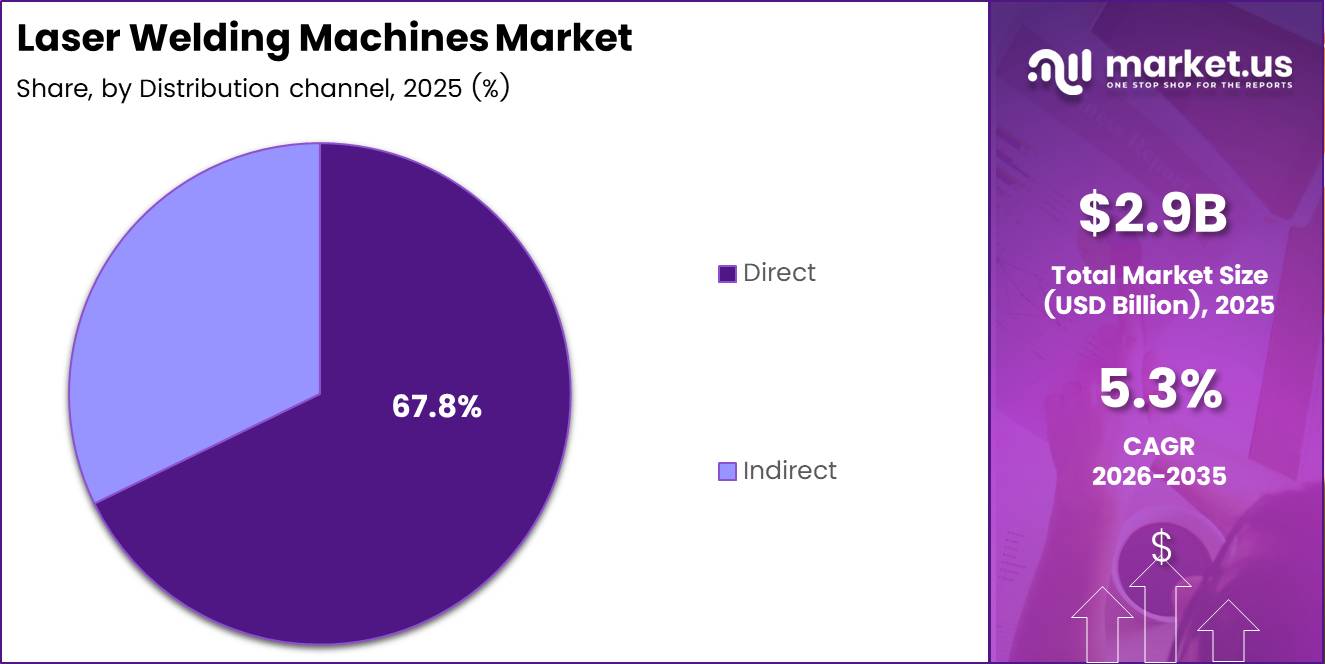

Direct sales channels account for 67.8% of distribution, which signals that buyers treat laser welding systems as capital investments requiring application engineering support, not commodity purchases. This distribution dynamic rewards vendors with strong field application teams and penalizes those relying on reseller networks lacking technical depth.

According to a 2025 AMRC case study on EV battery assembly, aluminium-to-busbar laser welds achieved shear loads between 850 N and 1,016 N, confirming structural reliability for high-cycle automated production. These load figures establish a performance benchmark that procurement engineers can now reference when specifying laser systems for battery module assembly lines.

In the same study, electrical resistance across aluminium-to-busbar joints ranged from 0.03 mΩ to 0.08 mΩ — well below the 0.1 mΩ threshold for high-power battery modules. This margin directly reduces thermal losses in service and supports the energy density targets that EV manufacturers cannot compromise on.

Key Takeaways

- The global laser welding machines market was valued at USD 2.9 Billion in 2025 and is forecast to reach USD 4.9 Billion by 2035.

- The market advances at a CAGR of 5.3% over the forecast period 2026 to 2035.

- By technology, Fiber Lasers lead with 47.2% market share in 2025.

- By output, the 3 kW–6 kW segment holds 39.6% share, the largest within the output category.

- By end-use industry, Automotive dominates with 34.1% share.

- By distribution channel, Direct sales account for 67.8% of the market.

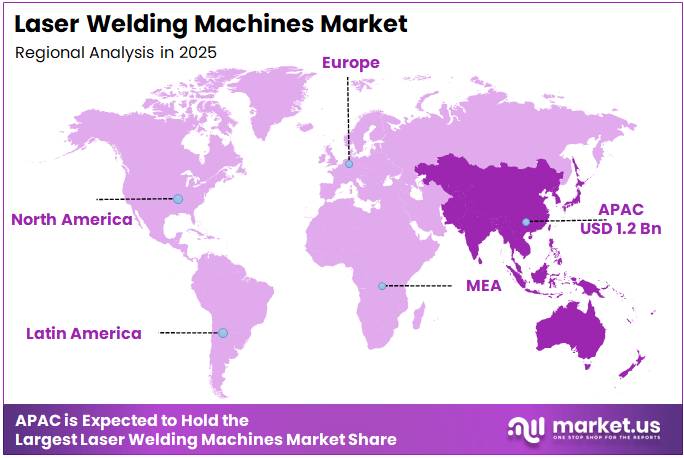

- Asia Pacific leads all regions with 43.70% share, valued at USD 1.2 Billion in 2025.

Technology Analysis

Fiber Lasers dominate with 47.2% due to superior beam quality and wall-plug efficiency.

In 2025, Fiber Lasers held a dominant market position in the By Technology segment of the Laser Welding Machines Market, with a 47.2% share. Their lower operating cost per watt and maintenance-free fiber delivery system make them the preferred platform for high-volume automated lines, particularly in automotive and electronics manufacturing where uptime is non-negotiable.

CO2 Lasers retain relevance in applications requiring longer wavelengths for non-metallic substrate welding. However, their bulkier optical delivery systems and higher maintenance requirements place them at a structural cost disadvantage relative to fiber platforms for most new metal-joining installations. Their installed base persists in legacy production environments rather than new builds.

Diode Lasers differentiate through compact form factors and direct diode beam delivery, eliminating the need for fiber coupling in certain configurations. They serve heat-sensitive joining tasks in medical device and thin-foil electronics assembly, where spot size control and low thermal input matter more than raw power output.

Others in the technology segment include disk lasers and pulsed Nd:YAG systems. Disk lasers compete with fiber at the very high end of the power range for thick-section aerospace weld jobs. Pulsed Nd:YAG systems remain specified in jewellery and precision micro-welding applications where pulse-on-demand energy control outweighs throughput considerations.

Output Analysis

3 kW–6 kW dominates with 39.6% due to versatile mid-power range across multiple industries.

In 2025, the 3 kW–6 kW output segment held a dominant market position in the By Output segment of the Laser Welding Machines Market, with a 39.6% share. This power band covers automotive body-in-white, battery tab welding, and electronics enclosure sealing within a single configurable platform, which directly reduces capital expenditure for multi-product manufacturers.

Below 3 kW systems serve precision micro-welding in medical implants, fine jewellery, and miniaturized electronics. Their lower power draw and compact footprint make them accessible to small-scale fabrication shops and R&D laboratories that cannot justify the capital and space requirements of higher-power installations.

Above 6 kW systems address heavy-gauge metal joining in aerospace structural components, thick-plate shipbuilding sections, and large-format automotive stampings. Their higher acquisition cost narrows the buyer pool to tier-one manufacturers and specialist contract welders. However, per-joint productivity at this power level often justifies the premium for large-batch production programs.

End Use Industry Analysis

Automotive dominates with 34.1% due to high-volume EV battery and body assembly demand.

In 2025, Automotive held a dominant market position in the By End Use Industry segment of the Laser Welding Machines Market, with a 34.1% share. EV battery module assembly alone creates a structural pull for laser systems, as manufacturers require hundreds of repeatable busbar joints per pack that only laser welding can deliver at production speeds with consistent joint quality.

Medical device manufacturing relies on laser welding for implant-grade hermetic seals on pacemaker housings, surgical instruments, and endoscopic components. Regulatory traceability requirements in this sector incentivize laser systems because their process parameters can be logged, monitored, and validated to ISO 13485 standards more readily than conventional thermal joining methods.

Electronics manufacturing uses laser welding for micro-scale joining of connectors, sensor housings, and battery terminals in consumer devices. The demand for miniaturization in smartphones, wearables, and IoT hardware continues to push tolerance requirements beyond what conventional soldering or resistance welding can consistently achieve.

Aerospace & Defense specifies laser welding for titanium structural assemblies, fuel system components, and avionics enclosures where weld integrity standards leave no margin for defects. These programs often require AS9100-certified processes, which creates a qualification barrier that consolidates purchasing among a small number of approved system vendors.

Jewellery manufacturers use laser welding for repair work, chain linking, and setting fine metalwork in gold, platinum, and silver. Pulsed laser systems dominate this application because they deliver controlled energy pulses that prevent discoloration and distortion of polished surfaces adjacent to the weld zone.

Others include tooling repair, energy sector component fabrication, and general industrial metalworking. These applications collectively represent a heterogeneous tail of the market that absorbs mid-range systems displaced from primary sector use as manufacturers upgrade to higher-power platforms.

Distribution Channel Analysis

Direct sales dominate with 67.8% due to capital investment complexity requiring application engineering.

In 2025, Direct distribution held a dominant market position in the By Distribution Channel segment of the Laser Welding Machines Market, with a 67.8% share. Buyers purchasing laser welding systems expect pre-sales application support, system integration assistance, and post-installation training — services that direct sales teams provide but reseller networks typically cannot replicate at the same depth.

Indirect distribution covers resellers, distributors, and agent networks that serve geographically dispersed smaller buyers. This channel gains relevance in emerging markets where vendors lack direct sales infrastructure, though its share reflects a constrained position relative to the technical complexity buyers expect vendors to handle directly. In April 2024, Accurl USA LLC partnered with Complete Machine Tools of Australia to extend its distribution reach into new markets, illustrating how indirect channel partnerships address geographic gaps that direct teams cannot cost-effectively cover alone.

Key Market Segments

By Technology

- Fiber Lasers

- CO2 Lasers

- Diode Lasers

- Others

By Output

- Below 3 kW

- 3 kW–6 kW

- Above 6 kW

By End Use Industry

- Automotive

- Medical

- Electronics

- Aerospace & Defense

- Jewellery

- Others

By Distribution Channel

- Direct

- Indirect

Drivers

Electric Vehicle Battery Manufacturing and Industrial Automation Create Structural Demand for Precision Laser Welding

EV battery module production requires defect-free busbar connections at speeds that only automated laser welding can sustain. According to the AMRC’s 2025 EV battery case study, laser beam welding achieved electrical-to-thermal conversion efficiencies of 25% to 40% — significantly above conventional arc processes. This efficiency advantage reduces energy cost per joint, which matters at the volume scales automotive manufacturers operate.

High-speed automated welding in industrial production lines replaces manual and semi-automated processes where throughput bottlenecks limit output. Laser systems integrate directly with robotic arms and conveyor-based production cells, enabling duty cycles that human operators cannot sustain. Moreover, non-contact welding eliminates tool wear costs and reduces consumable expenditure relative to MIG and TIG processes.

Aerospace and electronics manufacturers require micro-welding capabilities that only focused laser beams can deliver at the tolerance levels their components specify. In February 2024, DN Solutions entered a strategic agreement with ModuleWorks to develop next-generation machine tool software, signaling that system-level digital integration — combining laser hardware with software-driven process control — is becoming a key procurement criterion, not an optional upgrade.

Restraints

High Acquisition Costs and Operator Skill Requirements Limit Adoption Beyond Large Manufacturers

Advanced fiber laser welding systems carry acquisition costs that small and mid-size manufacturers cannot absorb within standard capital expenditure cycles. System integration — including robotic handling, vision alignment, and process control software — adds further cost beyond the laser source itself. Consequently, adoption concentrates among tier-one manufacturers and large contract welders with budgets to absorb multi-year payback periods.

Laser welding systems require trained operators with knowledge of beam optics, parameter optimization, and safety protocols that general welders do not possess. This skills gap forces buyers to either invest in dedicated training programs or hire specialists at premium rates. For manufacturers evaluating laser adoption, the total cost of workforce transition often equals or exceeds the hardware investment itself.

Maintenance requirements for fiber laser systems — including periodic fiber inspection, chiller servicing, and protective window replacement — demand structured maintenance schedules that smaller operations struggle to implement consistently. Downtime during unplanned maintenance directly reduces the productivity advantage that justified the system purchase, undermining the business case for cost-sensitive buyers evaluating laser welding against lower-maintenance alternatives.

Growth Factors

Medical Device Manufacturing, Portable Solutions, and Green Energy Infrastructure Expand the Addressable Market

Medical device manufacturers increasingly specify laser welding for hermetic seals on implantable devices, where joint integrity tolerances are defined by regulatory approval requirements rather than cost optimization. This creates a captive, high-margin segment where system vendors can price on performance rather than compete solely on acquisition cost. Consequently, medical applications represent a durable growth channel insulated from commodity pricing pressure.

Portable laser welding solutions address small-scale fabrication workshops that previously could not justify fixed industrial installations. Compact systems with self-contained cooling and simplified parameter interfaces lower the operator skill threshold, opening laser welding to metal fabrication shops, custom vehicle builders, and precision repair operations. This market tier is structurally underpenetrated and represents incremental unit volume beyond the established large-manufacturer base.

Green energy infrastructure projects — including wind turbine component fabrication, solar frame assembly, and hydrogen electrolyser manufacturing — require precision metal joining at scale. In January 2024, ModuleWorks announced a partnership with DN Solutions to develop integrated machine tool software, reinforcing that AI-based weld inspection and process optimization are becoming prerequisites for qualifying laser welding systems in regulated infrastructure programs. According to the 2025 AMRC study, copper-to-busbar laser welds maintained resistance values between 0.03 mΩ and 0.04 mΩ, demonstrating the electrical consistency that energy infrastructure applications demand.

Emerging Trends

Fiber Laser Adoption, Real-Time Vision Systems, and Robotic Integration Redefine Industrial Welding Cells

Fiber laser technology consolidates its position as the default platform for new industrial installations because it delivers higher efficiency, longer service intervals, and better beam quality than CO2 or diode alternatives at comparable power levels. Vendors that lead fiber laser adoption capture displacement demand as manufacturers retire aging CO2 systems and upgrade production lines to current performance standards.

Real-time vision systems integrated directly into laser welding heads enable automated weld seam tracking, defect detection, and in-process quality logging without slowing cycle times. This capability addresses the quality documentation requirement that automotive and aerospace OEMs impose on their supplier base. According to the 2025 AMRC EV battery study, copper-to-busbar joints achieved shear loads between 735 N and 986 N, a 251 N strength band that process monitoring systems must reliably flag when outside this envelope during production.

Hybrid laser-arc welding techniques combine laser speed with arc gap-bridging capability for heavy manufacturing applications where joint fit-up tolerances are wider than laser-only processes tolerate. Robotic and cobot integration brings fully automated laser welding cells within reach of mid-size manufacturers, as collaborative robots reduce the integration complexity and floor space previously required for hard-guarded industrial robot cells.

Regional Analysis

Asia Pacific Dominates the Laser Welding Machines Market with a Market Share of 43.70%, Valued at USD 1.2 Billion

Asia Pacific leads global demand with a 43.70% share valued at USD 1.2 Billion, driven by the concentration of automotive, electronics, and EV manufacturing capacity across China, Japan, South Korea, and India. China’s domestic EV production scale alone generates structural demand for laser welding systems at a volume that no other region currently replicates.

North America Laser Welding Machines Market Trends

North America holds a strong position anchored by aerospace and defense procurement, where laser welding qualifications for titanium structural components create long-cycle, high-value supply relationships. The accelerating domestic EV manufacturing buildout — supported by federal incentive programs — adds battery module assembly demand that is beginning to replicate the scale dynamics already established in Asia Pacific.

Europe Laser Welding Machines Market Trends

Europe’s automotive industry, particularly Germany’s premium vehicle segment, applies laser welding extensively in body-in-white and powertrain component assembly. EU industrial decarbonization commitments accelerate the replacement of energy-intensive conventional welding processes with higher-efficiency laser systems, making European manufacturers early adopters of energy-benchmarked laser welding specifications.

Middle East and Africa Laser Welding Machines Market Trends

The Middle East and Africa region shows adoption primarily in oil and gas pipeline fabrication and defense equipment manufacturing, where infrastructure investment programs fund capital equipment upgrades. The GCC’s industrial diversification agenda supports equipment procurement in sectors beyond hydrocarbons, creating entry points for laser welding system vendors targeting government-backed manufacturing projects.

Latin America Laser Welding Machines Market Trends

Latin America’s adoption centers on Brazil and Mexico, where established automotive assembly operations supply both domestic markets and North American OEM programs. Mexico’s proximity to US manufacturing supply chains creates demand for laser welding systems that meet the same quality and process documentation standards required by North American OEM contracts, pulling capability investment upward.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Amada Weld Tech concentrates on precision micro-welding applications across medical, electronics, and battery manufacturing, where its application engineering expertise secures long-term supply relationships with OEMs. This specialization protects margins by positioning Amada Weld Tech as a process solutions provider rather than a commodity hardware vendor, reducing exposure to price-only procurement decisions common in general industrial markets.

CHIRON Group integrates laser welding functionality within its machining center platforms, enabling customers to combine metal removal and joining operations on a single machine. This integration strategy targets manufacturers seeking to reduce floor space and work-in-progress handling costs, a positioning that differentiates CHIRON from standalone welding system vendors competing purely on beam parameters.

Coherent operates across the full photonics stack — from laser sources to beam delivery and process optics — giving it a vertical integration advantage that most laser welding competitors cannot replicate. This breadth allows Coherent to offer optimized system-level solutions where source, optics, and control are engineered together, reducing integration risk for buyers deploying laser welding in new production applications.

Emerson Electric brings automation and process control infrastructure to laser welding through its motion control and sensor portfolios. Its strategic value lies in connecting laser welding hardware to plant-wide manufacturing execution systems, positioning it to capture demand from manufacturers prioritizing data-driven production quality management over standalone equipment procurement.

Key Players

- Amada Weld Tech

- CHIRON Group

- Coherent

- Emerson Electric

- Han’s Laser Technology Industry Group

- Huagong Laser Engineering

- IPG Photonics

- Jenoptik

- KEYENCE

- Laser Technologies

- Laser Line

- Laser Star Technologies

- Penta Laser

- Precitec

- TRUMPF

Recent Developments

- April 2026 — Mills CNC showcased the HELLER HF 5500 5-axis machining centre at MACH 2026, featuring a direct-drive rotary tilting table and Siemens One control system, following DN Solutions’ acquisition of HELLER and signaling continued consolidation within the precision machine tool sector.

- April 2025 — Citizen Machinery Co., Ltd. introduced the third-generation Cincom L20-LFV series sliding-head lathes, expanding its CNC automatic lathe lineup with low-frequency vibration cutting technology designed to improve chip control and surface finish in precision turning applications.

- October 2024 — Kapitus acquired Ten Oaks Commercial Capital and launched a dedicated equipment finance arm to accelerate funding access for U.S. manufacturing businesses, with on-balance-sheet transactions commencing in early 2025 to support capital equipment investment in industrial sectors including precision metalworking.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.9 Billion |

| Forecast Revenue (2035) | USD 4.9 Billion |

| CAGR (2026-2035) | 5.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology (Fiber Lasers, CO2 Lasers, Diode Lasers, Others), By Output (Below 3 kW, 3 kW–6 kW, Above 6 kW), By End Use Industry (Automotive, Medical, Electronics, Aerospace & Defense, Jewellery, Others), By Distribution Channel (Direct, Indirect) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Amada Weld Tech, CHIRON Group, Coherent, Emerson Electric, Han’s Laser Technology Industry Group, Huagong Laser Engineering, IPG Photonics, Jenoptik, KEYENCE, Laser Technologies, Laser Line, Laser Star Technologies, Penta Laser, Precitec, TRUMPF |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |