Global Pet Tech Market By Product Type (Wearable Devices, Smart Collars and Tags, Smart Cameras and Monitors, GPS Trackers, Smart Feeders and Water Fountains, Smart Toys and Others), By Application (Health and Wellness Monitoring, Safety and Tracking, Behavior Monitoring and Training, Communication and Interaction, Feeding and Nutrition Management and Others), By End User (Pet Owners, Veterinary Hospitals and Clinics, Pet Boarding and Daycare Facilities, Animal Shelters and Rescues and Others), By Animal Type (Dogs, Cats, Birds and Others), By Distribution Channel (Online Retail, Pet Specialty Stores, Veterinary Clinics and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: April 2026

- Report ID: 183809

- Number of Pages: 206

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Key Takeaways

- Product Type Analysis

- Application Analysis

- End-User Analysis

- Animal Type Analysis

- Distribution Channel Analysis

- Key Market Segments

- Drivers

- Restraints

- Opportunities

- Impact of Macroeconomic / Geopolitical Factors

- Latest Trends

- Regional Analysis

- Key Players Analysis

- Recent Developments

- Report Scope

Report Overview

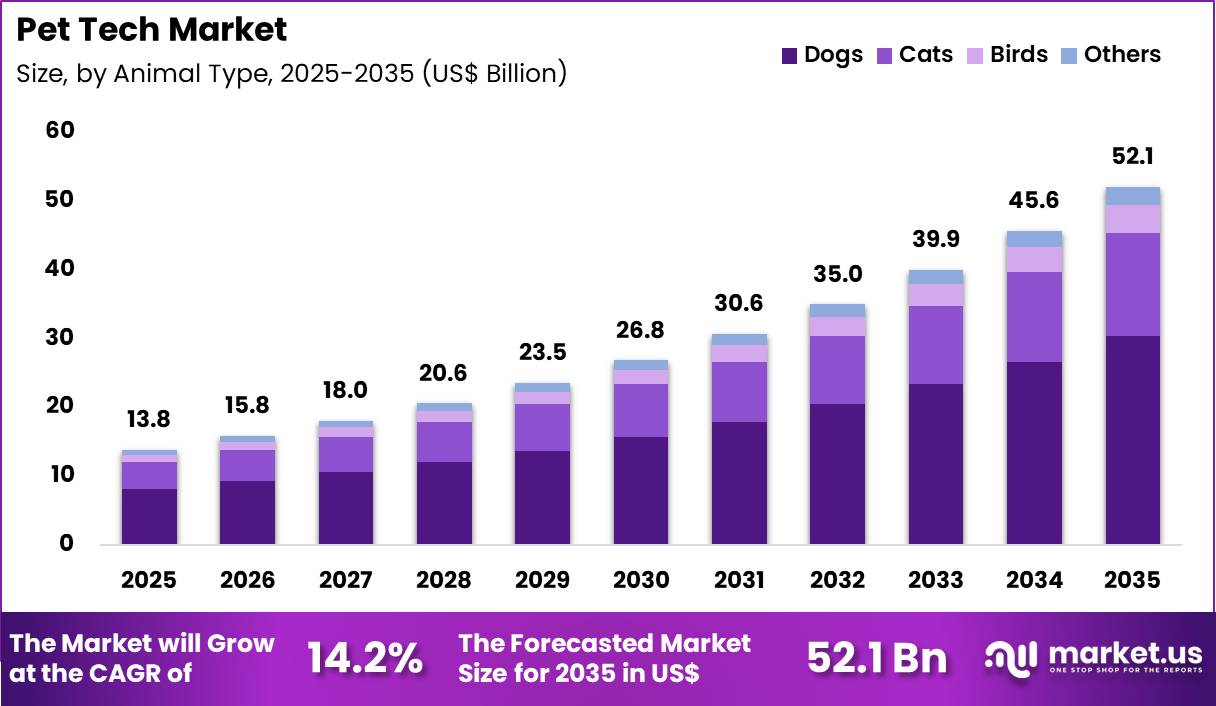

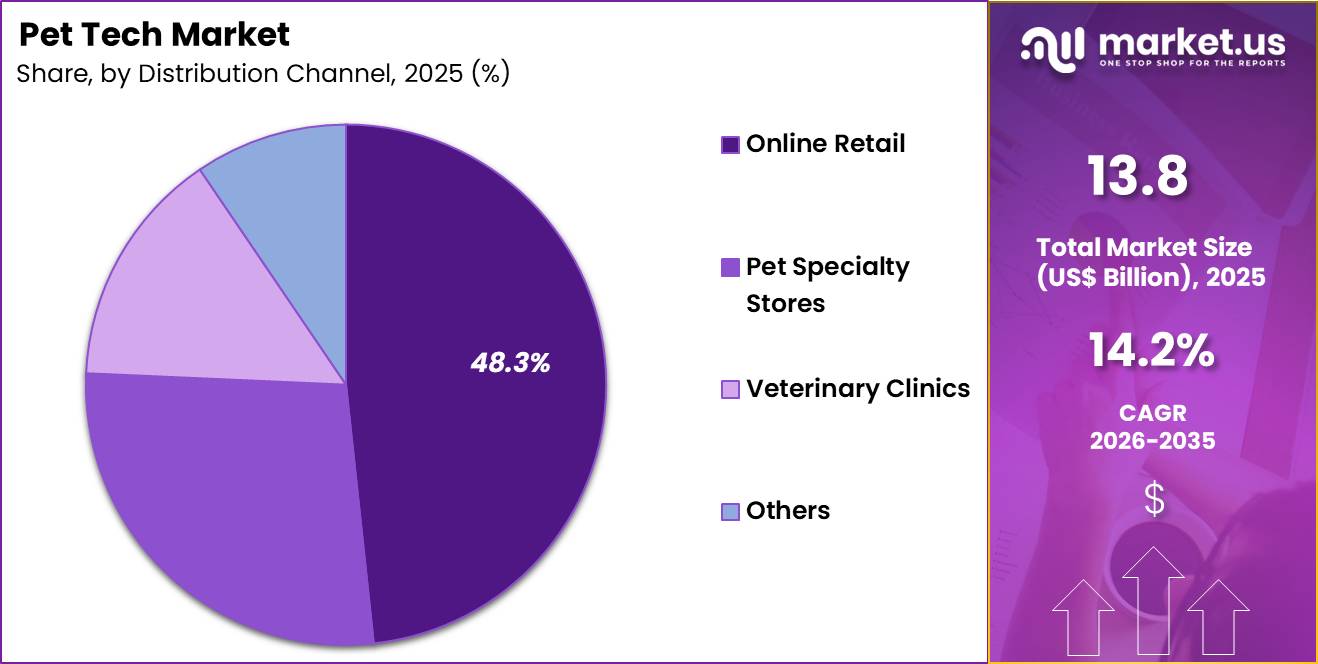

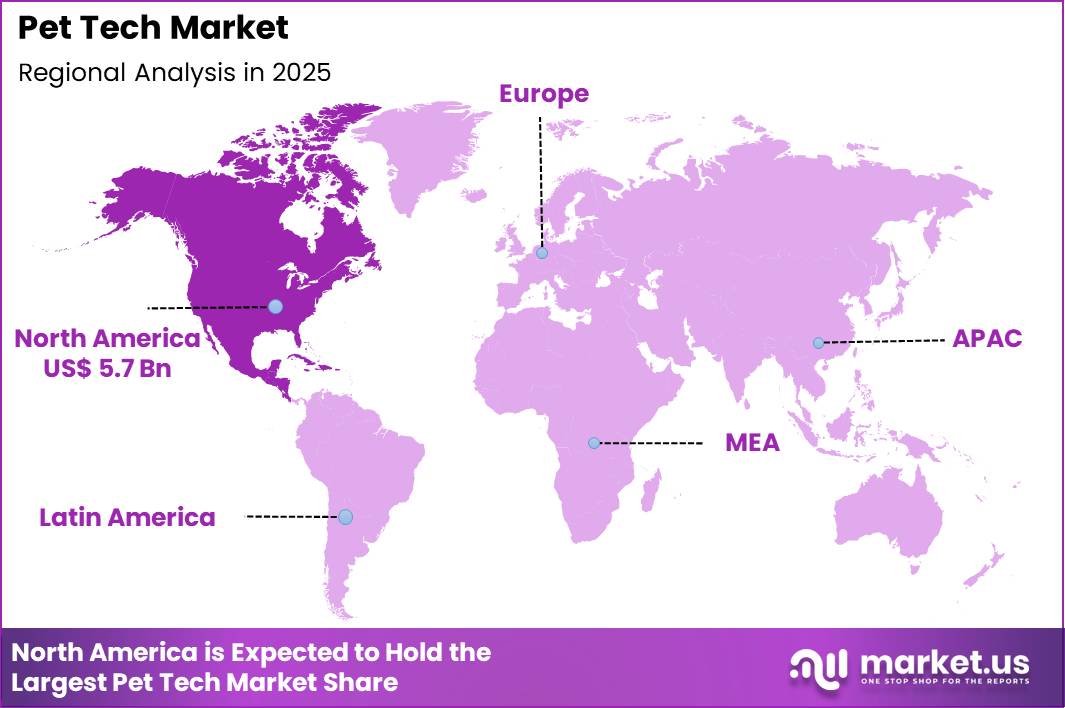

The Global Pet Tech Market size is expected to be worth around US$ 52.1 Billion by 2035 from US$ 13.8 Billion in 2025, growing at a CAGR of 14.2% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 41.5% share with a revenue of US$ 5.7 Billion.

Increasing integration of technology into everyday pet care propels the Pet Tech market as owners seek intelligent solutions that enhance monitoring, safety, and well-being of companion animals.

Pet owners increasingly utilize GPS-enabled trackers and smart collars to monitor location and activity levels in real time, ensuring the safety of dogs and cats that spend time outdoors or in large yards. These devices support health tracking by recording activity, sleep patterns, and rest quality, helping owners detect early signs of discomfort or reduced mobility in senior pets.

Smart feeders and automated dispensers enable precise portion control and scheduled feeding, supporting weight management and consistent nutrition for pets with dietary restrictions or diabetes.

Pet cameras with two-way audio and treat dispensers allow remote interaction, reducing separation anxiety and enabling owners to check on pets during work hours or travel. Wearable health monitors track vital signs such as heart rate and respiratory patterns, alerting owners to potential health issues before they escalate.

Technology developers pursue opportunities to create interconnected pet ecosystems that combine wearables, home automation, and mobile applications, expanding applications in preventive health and behavioral management. These platforms facilitate data sharing between pet wearables and owner fitness devices, offering a unified view of household wellness.

In February 2026, Garmin introduced a major software update across its fēnix and Venu smartwatch series. The update enhances gear tracking capabilities, enabling improved integration of pet wearable data within the Garmin Connect ecosystem.

This advancement allows pet owners to synchronize animal activity data alongside personal fitness metrics, supporting a more connected and data-driven pet care experience.

Recent trends emphasize AI-driven insights, multi-device interoperability, and user-friendly interfaces that transform pet care into a proactive, informed practice focused on prevention, safety, and strengthened human-animal bonds.

Key Takeaways

- In 2025, the market generated a revenue of US$ 13.8 Billion, with a CAGR of 14.2%, and is expected to reach US$ 52.1 Billion by the year 2035.

- The product type segment is divided into wearable devices, smart collars and tags, smart cameras and monitors, GPS trackers, smart feeders and water fountains, smart toys and others, with wearable devices taking the lead with a market share of 29.5%.

- Considering application, the market is divided into health and wellness monitoring, safety and tracking, behavior monitoring and training, communication and interaction, feeding and nutrition management and others. Among these, safety and tracking held a significant share of 35.4%.

- Furthermore, concerning the end user segment, the market is segregated into pet owners, veterinary hospitals and clinics, pet boarding and daycare facilities, animal shelters and rescues and others. The pet owners sector stands out as the dominant player, holding the largest revenue share of 72.1% in the market.

- The animal type segment is divided into dogs, cats, birds and others, with dogs taking the lead with a market share of 58.4%.

- The distribution channel segment is segregated into online retail, pet specialty stores, veterinary clinics and others, with the online retail segment leading the market, holding a revenue share of 48.3%.

- North America led the market by securing a market share of 41.5%.

Product Type Analysis

Wearable devices accounted for 29.5% of growth within product type and dominate the pet tech market due to their ability to provide real-time tracking, health monitoring, and activity insights. Pet owners increasingly adopt smart wearables to monitor location, fitness levels, and behavioral patterns, which enhances pet safety and well-being.

The segment is expected to expand as connected devices and IoT-based solutions become more advanced and affordable. Wearable devices are likely to gain traction because they integrate multiple features such as GPS tracking, health alerts, and activity tracking in a single platform.

The segment benefits from rising awareness of pet health and preventive care. Continuous innovation in sensors and mobile app integration is projected to improve functionality and user experience. As pet owners seek data-driven insights for better care, wearable devices are estimated to remain the leading product segment in this market.

Application Analysis

Safety and tracking accounted for 35.4% of growth within application and dominate the pet tech market due to increasing concerns about pet security and loss prevention. Pet owners rely on GPS-enabled devices and tracking systems to locate pets in real time and ensure their safety.

The segment is expected to grow as urbanization and outdoor pet activities increase the risk of pets getting lost. Safety-focused applications are likely to remain essential as they provide immediate alerts and location updates.

The segment benefits from advancements in tracking accuracy and mobile connectivity. Rising adoption of smart collars and wearable trackers is projected to support growth. As pet safety continues to be a priority, this application segment is estimated to maintain its dominant position in the market.

End-User Analysis

Pet owners accounted for 72.1% of growth within end user and dominate the pet tech market due to their direct involvement in pet care and increasing willingness to invest in advanced technologies. Owners actively adopt smart devices to monitor health, track location, and improve overall pet management.

The segment is expected to expand as pet humanization trends continue to strengthen globally. Pet owners are likely to seek innovative solutions that enhance convenience and pet well-being.

The segment benefits from rising disposable income and growing awareness of pet health. Increasing availability of user-friendly devices is projected to support adoption. As digital adoption increases among consumers, pet owners are estimated to retain their dominant position in this market.

Animal Type Analysis

Dogs accounted for 58.4% of growth within animal type and dominate the pet tech market due to their high adoption rate as companion animals and greater need for monitoring and tracking. Dogs often require regular outdoor activity, which increases the need for GPS tracking and safety solutions.

ers are likely to invest more in devices that track activity levels and health metrics. The segment benefits from strong emotional bonding and higher spending on dog care. Increasing awareness of canine health and fitness is projected to support device adoption.

As dogs remain the most common pets worldwide, this segment is estimated to maintain its dominant position in the market.

Distribution Channel Analysis

Online retail accounted for 48.3% of growth within distribution channel and dominate the pet tech market due to the convenience, wide product availability, and competitive pricing offered through digital platforms. Consumers increasingly prefer online channels for purchasing pet tech products due to easy access to product comparisons and reviews.

The segment is expected to grow as e-commerce adoption continues to rise globally. Online platforms are likely to benefit from faster delivery options and broader product selection. The segment also supports direct-to-consumer sales models, which enhances brand reach.

As digital shopping becomes more prevalent, online retail is anticipated to remain the leading distribution channel in this market.

Key Market Segments

By Product Type

- Wearable Devices

- Smart Collars and Tags

- Smart Cameras and Monitors

- GPS Trackers

- Smart Feeders and Water Fountains

- Smart Toys

- Others

By Application

- Health and Wellness Monitoring

- Safety and Tracking

- Behavior Monitoring and Training

- Communication and Interaction

- Feeding and Nutrition Management

- Others

By End User

- Pet Owners

- Veterinary Hospitals and Clinics

- Pet Boarding and Daycare Facilities

- Animal Shelters and Rescues

- Others

By Animal Type

- Dogs

- Cats

- Birds

- Others

By Distribution Channel

- Online Retail

- Pet Specialty Stores

- Veterinary Clinics

- Others

Drivers

Rising pet ownership and humanization trends are driving the Pet Tech market.

The substantial increase in the number of households owning pets has created sustained demand for technology-enabled solutions that enhance monitoring, care, and interaction.

According to the American Pet Products Association 2025 State of the Industry Report, 94 million U.S. households owned at least one pet in 2025, up from 82 million in 2023. The AVMA 2025 Pet Ownership and Demographics Sourcebook reports 87.3 million dogs and 76.3 million cats in the United States in 2025.

Total U.S. pet industry expenditures reached $152 billion in 2024 and were projected at $157 billion for 2025. Pet owners increasingly treat animals as family members, prompting investment in devices that support health tracking, safety, and daily management. This shift supports adoption of connected products such as wearables, cameras, and automated feeders.

Urban lifestyles and dual-income households further necessitate remote oversight capabilities. Enhanced awareness of preventive care encourages utilization of data-driven tools for early issue detection. Manufacturers respond by developing user-friendly interfaces compatible with mobile applications.

These demographic and behavioral factors generate consistent demand across consumer segments. Consequently, pet population growth and evolving owner priorities constitute a primary driver of market expansion during the 2022–2025 period.

Restraints

High device costs and variable consumer adoption rates are restraining the Pet Tech market.

Advanced pet technology products, including GPS-enabled collars and AI-integrated monitors, often carry premium pricing that limits accessibility for budget-conscious households. Average annual pet-related spending per U.S. household has increased, yet price sensitivity persists amid broader economic considerations.

Many owners trial basic solutions before committing to higher-value connected devices, resulting in slower conversion to full adoption. Integration complexities with existing home systems or smartphone platforms create additional barriers for less tech-savvy users.

Limited long-term data on device durability and battery performance contributes to hesitation in certain segments. Smaller or rural households encounter challenges with reliable internet connectivity required for optimal functionality. These economic and practical constraints moderate uptake despite recognized benefits.

Regional differences in disposable income and digital infrastructure further influence penetration levels. Persistent gaps in perceived value versus cost slow the overall replacement and expansion cycle. As a result, affordability issues impose measurable restraint on accelerated market growth throughout the 2022–2025 timeframe.

Opportunities

Integration of AI and IoT capabilities across monitoring and automation devices is creating growth opportunities in the Pet Tech market.

Advancements in artificial intelligence and connected sensors enable real-time health analytics, behavior insights, and automated care routines that deliver personalized support. Opportunities emerge for subscription-based models that combine hardware with ongoing data services and remote veterinary linkages.

Expansion into telehealth-compatible platforms allows seamless sharing of vital metrics with professionals. Potential exists for cross-category bundles encompassing feeders, cameras, and wearables that function within unified ecosystems.

Collaboration with established consumer electronics firms accelerates innovation and distribution reach. Alignment with preventive wellness trends supports value propositions centered on early intervention and improved quality of life.

Scalable cloud architectures facilitate global deployment while accommodating varying infrastructure levels. These features appeal to millennial and Gen Z owners who prioritize convenience and data transparency.

Enhanced customization options address breed-specific or age-related requirements effectively. Overall, intelligent connectivity unlocks substantial prospects for recurring revenue and diversified applications across household and professional settings.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions and geopolitical developments are significantly influencing investment patterns, consumer behavior, and supply chain resilience in the pet tech market.

Rising pet ownership and increasing humanization of pets are driving strong demand for connected devices such as smart collars, feeders, and health monitoring systems, while inflation is raising product prices and limiting discretionary spending on premium devices in cost-sensitive households.

Currency volatility and global trade disruptions are affecting the sourcing of semiconductors, sensors, and electronic components that form the backbone of pet tech products. Geopolitical tensions are also impacting cross-border technology partnerships and slowing innovation cycles in certain regions.

Current US tariffs on imported electronics and components are increasing manufacturing and procurement costs, which places pressure on pricing strategies and margins for device manufacturers. These cost increases may slow adoption in emerging markets where affordability remains a key barrier.

However, the industry is responding by investing in localized production, software-driven services, and subscription-based models to offset hardware costs. Overall, despite short-term economic and trade-related constraints, sustained demand for digital pet care solutions and continuous technological innovation are expected to support long-term market expansion.

Latest Trends

Proliferation of AI-powered wearables and smart monitoring solutions represents a recent trend in the Pet Tech market.

Throughout 2024 and 2025, the sector has witnessed accelerated development of wearables and connected devices incorporating artificial intelligence for activity tracking, health anomaly detection, and automated alerts.

North America maintained a leading position, accounting for approximately 40% of the market share in 2024, supported by high pet ownership and digital infrastructure. Industry implementations during this period emphasize seamless mobile integration that enables remote feeding, interaction via cameras, and behavioral analysis.

Subscription services for data insights and firmware updates have gained traction, shifting from one-time purchases toward continuous engagement models. The trend aligns with broader demands for preventive care and peace of mind among busy pet owners.

Refinements in sensor accuracy and battery efficiency have improved usability across daily routines. Prominent developments observed in 2024–2025 highlight a clear orientation toward intelligent, interconnected ecosystems that prioritize proactive management. This evolution continues to redefine consumer expectations for technology-assisted pet companionship and welfare.

Regional Analysis

North America is leading the Pet Tech Market

North America accounted for 41.5% of the pet tech market in 2025, driven by rapid integration of connected devices and digital platforms into everyday pet care practices. Households across the United States are increasingly adopting smart collars, GPS trackers, automated feeders, and health monitoring systems to enhance pet safety and well-being.

Data from the American Pet Products Association shows that overall U.S. pet industry spending surpassed USD 136 billion in 2022, indicating strong consumer investment that supports adoption of advanced pet technologies.

Technology-enabled solutions are gaining traction as pet owners seek real-time insights into activity levels, location tracking, and behavioral patterns. Companies are developing mobile applications that integrate with wearable devices to deliver personalized health alerts and preventive care recommendations.

The growing trend of pet humanization has encouraged demand for premium, convenience-driven solutions that mirror human digital lifestyles. Veterinary providers are also beginning to incorporate remote monitoring data into clinical assessments.

Continuous innovation in IoT, cloud connectivity, and data analytics is improving device functionality and user experience. These factors have collectively strengthened expansion of technology-driven pet care solutions across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to advance at a strong pace over the forecast period as rising disposable income and urbanization accelerate adoption of connected pet care solutions. Countries such as China, Japan, South Korea, and India are witnessing rapid growth in companion animal ownership, particularly among younger urban populations.

The Food and Agriculture Organization highlights the increasing role of companion animals in urban environments, which is influencing demand for digital management and monitoring tools. Pet owners across the region are embracing smart devices that offer convenience, safety, and real-time monitoring capabilities.

E-commerce platforms are playing a critical role in expanding access to innovative pet technology products. Local and international companies are introducing cost-effective devices tailored to diverse consumer segments. Integration of mobile applications and cloud-based services is enabling broader adoption across different income groups.

Veterinary professionals are also exploring digital tools to support preventive healthcare and remote consultations. These developments are expected to support sustained growth of connected pet care technologies across Asia Pacific.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the Pet Tech Market expand growth by developing connected pet devices, strengthening IoT integration, and enhancing data-driven platforms that monitor pet health, activity, and safety in real time. Companies invest in smart collars, GPS trackers, automated feeders, and AI-enabled cameras that provide continuous insights to pet owners.

They also focus on mobile app ecosystems and subscription-based services that support remote monitoring and personalized pet care management. Whistle Labs represents a prominent participant in the Pet Tech Market and operates as a U.S.-based technology company that develops GPS-enabled pet trackers and health monitoring devices for companion animals.

The company emphasizes real-time location tracking and activity analytics to improve pet safety and wellness. Industry competitors continue to introduce advanced wearable technologies, expand digital platforms, and strengthen partnerships with veterinary providers to drive adoption and sustain long-term market growth.

Top Key Players

- Garmin Ltd.

- Fitbit LLC (Google)

- PetSafe Brands

- Whistle Labs Inc. (Mars Petcare)

- Petcube Inc.

- SureFlap Ltd. (Sure Petcare)

- Nestlé Purina PetCare

- Mars Petcare

- Hill’s Pet Nutrition Inc.

- PetCo Health and Wellness Company Inc.

- Chewy Inc.

Recent Developments

- In January 2026, Mars Veterinary Health released its 2025 impact report, highlighting the progress of the MARS PETCARE BIOBANK, which has enrolled more than 4,500 pets. The initiative has recently identified a genetic marker, SLAMF1, associated with canine dermatitis. This discovery is expected to support the development of advanced DNA-based diagnostic technologies, strengthening precision diagnostics and personalized treatment approaches in veterinary care.

- In March 2026, Chewy Inc. reported fiscal 2025 net sales of $12.6 billion, reflecting steady growth supported by expanding demand in health and wellness categories. The company also recorded strong free cash flow performance, driven by increased adoption of digital health services and advertising-based revenue streams. Moving into 2026, Chewy is focusing on scaling high-margin, technology-enabled veterinary and wellness offerings to enhance customer engagement and long-term profitability.

Report Scope

Report Features Description Market Value (2025) US$ 13.8 Billion Forecast Revenue (2035) US$ 52.1 Billion CAGR (2026-2035) 14.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Wearable Devices, Smart Collars and Tags, Smart Cameras and Monitors, GPS Trackers, Smart Feeders and Water Fountains, Smart Toys and Others), By Application (Health and Wellness Monitoring, Safety and Tracking, Behavior Monitoring and Training, Communication and Interaction, Feeding and Nutrition Management and Others), By End User (Pet Owners, Veterinary Hospitals and Clinics, Pet Boarding and Daycare Facilities, Animal Shelters and Rescues and Others), By Animal Type (Dogs, Cats, Birds and Others), By Distribution Channel (Online Retail, Pet Specialty Stores, Veterinary Clinics and Others) Regional Analysis North America – The US, Canada; Europe – Germany, France, The U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America Competitive Landscape Garmin Ltd., Fitbit LLC, PetSafe Brands, Whistle Labs Inc., Petcube Inc., SureFlap Ltd., Nestlé Purina PetCare, Mars Petcare, Hill’s Pet Nutrition Inc., PetCo Health and Wellness Company Inc., Chewy Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Garmin Ltd.

- Fitbit LLC (Google)

- PetSafe Brands

- Whistle Labs Inc. (Mars Petcare)

- Petcube Inc.

- SureFlap Ltd. (Sure Petcare)

- Nestlé Purina PetCare

- Mars Petcare

- Hill's Pet Nutrition Inc.

- PetCo Health and Wellness Company Inc.

- Chewy Inc.

Our Clients

- 183809

- April 2026