Quick Navigation

Report Overview

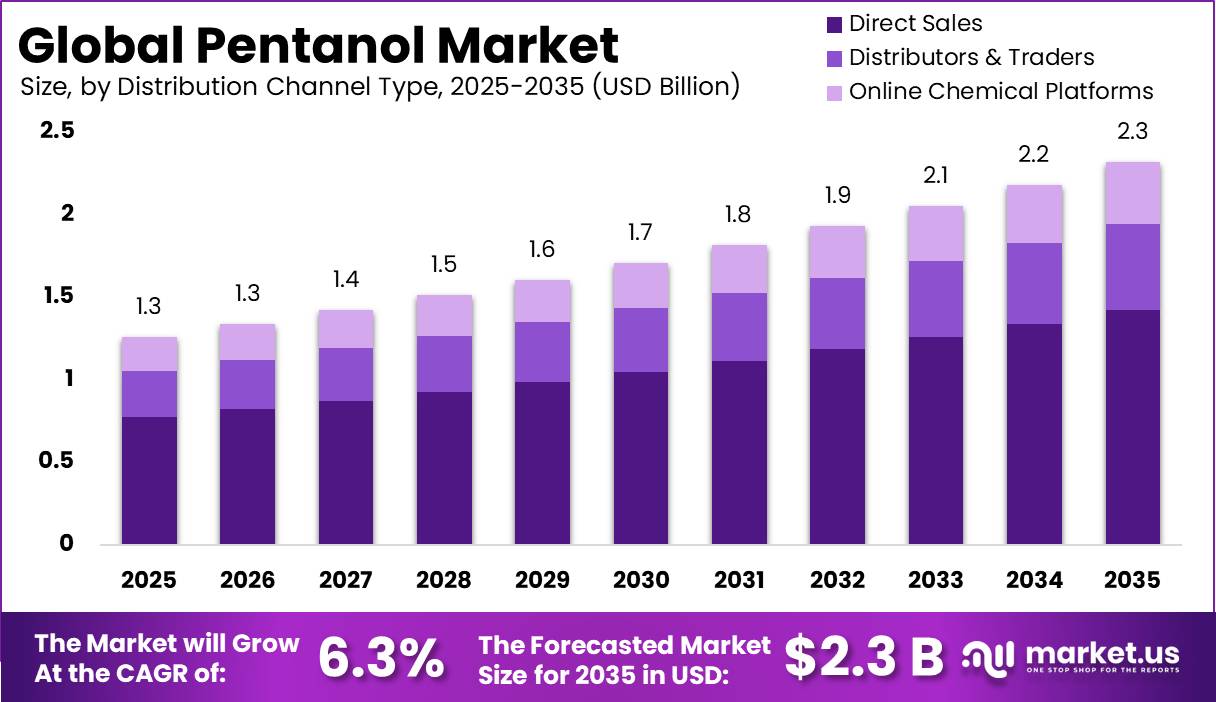

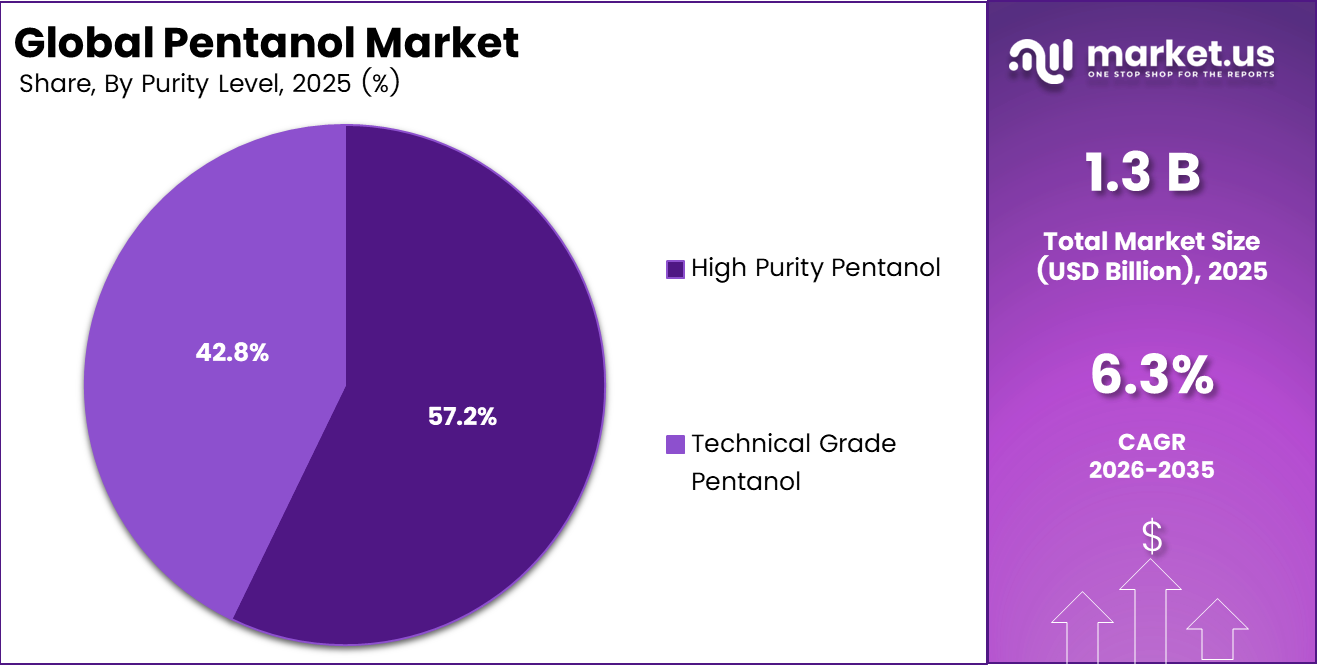

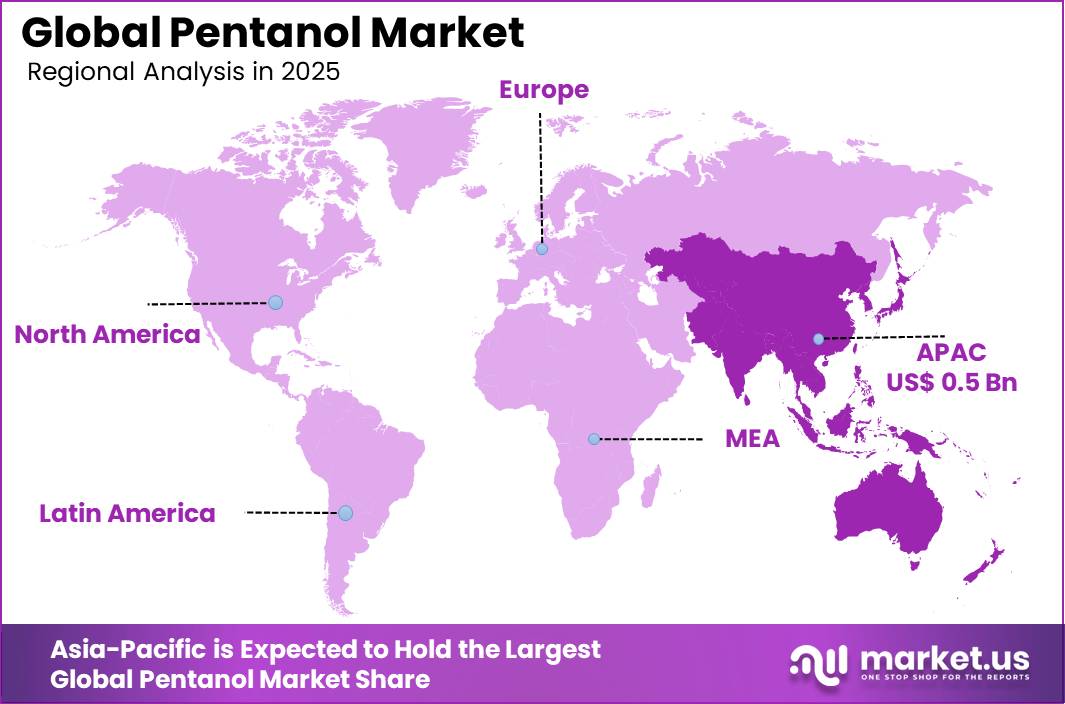

The Global Pentanol Market was valued at US$ 1.3 billion in 2025, and between 2026 and 2035, this market is estimated to register a CAGR of 6.3%, reaching about US$ 2.3 billion by 2035. Asia Pacific held a dominant market position, capturing more than a 41.2% share, holding USD 0.5 billion in revenue.

The global pentanol industry is a specialized segment of the C5 alcohol and oxygenated solvents value chain, comprising isomers such as 1-pentanol and isoamyl alcohol, which serve as high-boiling solvents and chemical intermediates in advanced industrial chemistry. Pentanol has a boiling point of approximately 137.9°C, flash point near 49°C, and water solubility of around 22 g/L at 25°C, making it suitable for controlled evaporation systems and precision formulation environments.

It is primarily consumed in downstream chemical transformation processes, where global production of oxygenated solvents is estimated to account for a significant portion of the broader USD 600+ billion global specialty chemicals industry, reflecting its embedded role in industrial synthesis networks.

From an industrial scenario perspective, pentanol is produced through conventional oxo-alcohol synthesis routes derived from petrochemical feedstocks, while emerging bio-based fermentation pathways using renewable carbohydrates are gaining traction under decarbonization strategies. Demand is structurally supported by the expansion of global manufacturing output, with the chemicals and materials sector contributing over USD 5 trillion annually to the world economy, reinforcing sustained consumption of intermediate alcohols in formulation chemistry.

Future growth opportunities are strongly associated with scale-up of bio-based pentanol technologies, expansion of green chemistry manufacturing clusters, and adoption in next-generation coating resins, advanced adhesives, and sustainable polymer systems, positioning pentanol as a strategically important mid-chain alcohol in the global transition toward low-emission industrial chemical processes.

Key Takeaways

- The global pentanol market was valued at US$1.3 billion in 2025.

- The global pentanol market is projected to grow at a CAGR of 6.3% and is estimated to reach US$2.3 billion by 2035.

- n-Pentanol (1-Pentanol) is the dominant product type with a 38.4% share.

- High Purity Pentanol leads the purity level at 57.2%.

- Chemical Manufacturing serves as the primary end-use industry at 34.2%.

- Direct Sales represents the leading distribution channel with 61.4%.

- Asia Pacific stands as the largest regional market, commanding a 41.2% share.

Product Type Analysis

n-Pentanol (1-Pentanol) represents the dominant Segment in the Market.

1-Pentanol is dominant in the pentanol market, which accounts for a 38.4% share of the total segment because of its wide applicability in the synthesis of drugs as a chemical intermediate, its use as a solvent, and the formation of esters. The linear chain structure of N-pentanol provides better solvency properties and has a higher boiling point of 138 degrees Celsius.

1-pentanol’s strong market position is reinforced by its wide application in coatings, adhesives, plasticizers, and specialized chemical formulations. Manufacturers like 1-pentanol because it is compatible with a wide range of resins and chemical compounds, resulting in consistent performance across industrial applications. Furthermore, rising demand for high-performance solvents and intermediates in emerging nations has contributed to the segment’s steady rise, reinforcing its position in the worldwide pentanol market.

The Isoamyl Alcohol market dynamics are majorly driven by the increasing use of isoamyl alcohol in natural flavor products such as isoamyl acetate, growing pipeline applications in cosmetics, and stringent requirements in pharmaceutical excipients. In addition, the growth in demand for Isoamyl Alcohol is being driven by the ability to scale production through bio-fermentation from fusel oil derived from yeasts that achieve carbon parity with petrochemicals by 40%.

Purity Level Analysis

High Purity Level is a significant level in the Pentanol Market.

High Purity Pentanol holds a 57.2% share of market volume by purity type. Synthesis of APIs, specialist coatings, and usage in analytical grade reagents necessarily demand an impurity content less than 100 ppm. Demand for high-purity n-pentanol has been growing steadily at about 4.8% each year, driven by new regulatory guidelines from ICH Q3C that categorize pentanol as Class 3 solvent due to low toxicity potential.

However, the fast-growing category in this spectrum is low/technical grade pentanol, which is fueled by a large volume demand by industries involved in blending, mining, and biofuel activities. Although high-grade products account for the majority of the value because of the high price of pharmaceuticals, the technical grades continue to show rapid growth.

End Use Industry Analysis

Pentanol is mostly utilized in the Chemical Manufacturing Sector.

Chemical Manufacturing industries contribute a hefty share of 34.2% to the total demand of pentanol in 2024-2025, thereby solidifying their position as the main source of demand pull. Pentanol is used as the key building block for C5 esters (amyl acetate and amyl acrylate), plasticizers, and other specialty surfactants.

Solvent uses in the industry alone contribute around 45% to total industrial expenditure on the product, with large-scale applications in paints, coatings, adhesives, and industrial cleaners. Vertical integration of large chemical manufacturing industries and the oxo-synthesis units upstream generates captive demand. Off-take agreements with long-term commitments and tiered pricing help protect large industrial customers from the vagaries of the spot market.

Distribution Channel Analysis

Direct Sales Are the Most Widely Used in the Pentanol Market.

The most dominant sales channel for pentanol products around the world is direct sales channels, accounting for 61.4% of total volumes sold, in recognition of the industrial-commodity nature of the procurement of bulk chemical products wherein corporate customers in the form of pharmaceutical CDMO companies, automotive OEM supply chains, and chemical manufacturing facilities place great importance on direct purchasing relationships.

Direct sales leadership in this market segment is sustained to ensure supply consistency, customization, and pricing based on volume levels. The reasons behind the success of this channel include the volatility associated with the cost of raw materials, which in pentanol constitutes up to 60%-70% of the total cost of manufacture, motivating end users to lock in prices with their suppliers in a direct B2B relationship.

Key Market Segments

By Product Type

- n-Pentanol (1-Pentanol)

- Isoamyl Alcohol (3-Methyl-1-Butanol)

- 2-Pentanol

- Others

By Purity Level

- High Purity Pentanol

- Technical Grade Pentanol

By End-use Industry

- Chemical Manufacturing

- Pharmaceuticals

- Paints & Coatings

- Food & Beverage

- Cosmetics & Personal Care

- Automotive

- Agrochemicals

- Others

By Distribution Channel:

- Direct Sales

- Distributors & Traders

- Online Chemical Platforms

Market Dynamics

Challenge

Pentanol production is highly dependent on petrochemical feedstocks, particularly 1-butene and propylene, making manufacturers vulnerable to fluctuations in crude oil and olefin prices. In Q1 2026, Brent crude was projected to average USD 60–65 per barrel, while propylene prices reached USD 930.60/MT FOB China, USD 1,022.98/MT CIF India, and USD 1,003.18/MT CIF USA, directly increasing pentanol production costs.

Geopolitical tensions have further disrupted feedstock availability through supply interruptions and logistics constraints, creating greater uncertainty than the absolute price level itself. Although propylene prices eased by around 1.3 to 3.5 percent in June 2026, manufacturers continue to face difficulty securing stable long-term supply contracts in a volatile market.

To reduce risk, producers are exploring alternative feedstock sources, including bio-based pathways, while strengthening long-term supply agreements and increasing working capital reserves by 15 to 20 percent to absorb 3- to 6-month feedstock price shocks. Nevertheless, feedstock price volatility remains a significant restraint on pentanol market growth and profitability.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Petrochemical Feedstock Price Volatility | -1.4% | Global; highest in APAC & EU import hubs | Medium term (2–4 years) |

| Bio-Pentanol Fermentation Yield Bottleneck | -1.1% | North America, EU bio-economy clusters, India | Long term (≥ 4 years) |

| Hazmat Logistics & Multi-Modal Compliance Friction | -0.9% | APAC logistics corridors, Gulf-Asia shipping lanes | Medium term (2–4 years) |

| Evolving VOC & REACH Regulatory Burden | -0.8% | EU regulatory hubs, North America (EPR states) | Medium term (2–4 years) |

| Isomer Separation & Purification Energy Intensity | -0.7% | Global — high-purity end-use markets | Long term (≥ 4 years) |

| Specialized Workforce & Process Engineering Deficit | -0.5% | North America, EU; emerging in APAC scale-up zones | Long term (≥ 4 years) |

Opportunity

Bio-based pentanol produced through engineered Clostridium and E. coli strains using lignocellulosic agricultural residues represents a major untapped opportunity beyond conventional petrochemical production routes. Advances in synthetic biology and fermentation technologies are improving the commercial viability of bio-pentanol, supported by an estimated 300 million metric tons of oil equivalent in global agricultural and forestry residue feedstock availability.

Currently, bio-pentanol production costs are estimated at USD 1,200–1,500/MT, compared with USD 900–1,100/MT for petrochemical production. However, continued genetic optimization and process improvements are expected to reduce this gap to within 10–15 percent by 2029–2031, making large-scale commercialization increasingly competitive.

Manufacturers investing in bio-pentanol production through licensing or joint ventures can secure 30–40 percent price premiums in regulated markets while reducing lifecycle carbon emissions by approximately 55–70 percent. Growing demand for low-carbon chemicals from sustainable aviation fuel, personal care, and specialty chemical industries further strengthens this long-term opportunity.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Alcohol-to-Jet (AtJ) SAF Feedstock Integration | +2.8% | EU, North America, APAC (India, Japan) | Medium term (2–4 years) |

| Bio-Pentanol via Synthetic Biology & Metabolic Engineering | +2.3% | North America, EU, APAC | Medium term (2–4 years) |

| High-Value Ester Derivatives (Amyl Acetate/Flavors & Fragrances) | +1.9% | APAC emerging, EU, North America | Short term (≤ 2 years) |

| Next-Gen Non-Phthalate Plasticizer Intermediate Pivot | +1.6% | China, APAC, EU regulatory markets | Medium term (2–4 years) |

| Pharmaceutical-Grade API Solvent & Contract Synthesis Vertical | +1.4% | India, EU, North America | Short–Medium term (1–3 years) |

| Agrochemical Formulation Carrier & Herbicide Synthesis Expansion | +1.2% | APAC, Latin America, Africa | Long term (≥ 4 years) |

Driver

The tightening of chemical regulations is creating new opportunities for pentanol as manufacturers replace restricted solvents with safer alternatives. Under Regulation (EU) 2025/1090, DMAC and NEP will be restricted at concentrations of 0.3 percent or higher from December 23, 2026, with limited exemptions until June 2029. Since these solvents are widely used in coatings, adhesives, wire enamels, and automotive products, pentanol is well positioned as a replacement due to its lower toxicity and suitable solvent properties.

For coatings manufacturers, replacing DMAC with pentanol typically requires 6 to 9 months of reformulation, safety documentation, and regulatory validation, creating a concentrated demand window through H2 2025 to Q3 2026. Similar regulatory changes in the United States and Vietnam are further encouraging the shift toward compliant solvent systems.

As a result, demand is expected to move beyond commodity-grade pentanol toward specification-grade products with documented regulatory compliance. Producers offering certified exposure and safety documentation can command 10 to 18 percent price premiums within regulated markets, particularly across European supply chains.

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 1. Biofuel Blending Mandates driving C5 alcohol adoption as diesel/gasoline additive | +1.4% | EU (RED III core), Brazil, India, Southeast Asia spill-over | Short-to-Medium term (1–3 years) |

| 2. REACH & Green Chemistry Regulation triggering substitution of banned solvents (DMAC, NEP) with pentanol-based alternatives | +1.1% | EU primary; North America secondary (EPA VOC rules) | Short term (≤ 2 years) |

| 3. Flavors & Fragrances (F&F) Industry Expansion on rising natural/clean-label ingredient demand; pentyl acetate (amyl acetate) as key ester | +0.8% | APAC dominant (47% F&F growth share), North America, EU | Medium term (2–4 years) |

| 4. APAC Industrialization & Coatings/Adhesives Demand lifting oxo-alcohol and solvent consumption in construction and automotive sectors | +1.2% | China, India, ASEAN (Vietnam, Indonesia); North America secondary | Medium term (2–4 years) |

| 5. Bio-Based Pentanol Scale-Up via metabolic engineering and fermentation, enabling renewable feedstock premiums and ESG-linked procurement | +0.6% | North America (US biorefinery corridor), EU (advanced biofuel corridors), emerging India scale | Long term (≥ 4 years) |

| 6. Pharmaceutical Solvent & API Intermediate Demand underpinned by generic drug manufacturing expansion and IPC solvent upgrade cycles | +0.7% | India (API hub), China, EU (GMP-compliant sourcing shift) | Medium-to-Long term (3–5 years) |

Restraint

The expanding EU REACH framework is increasing compliance costs and regulatory complexity for pentanol producers and exporters. The proposed REACH Recast introduces a 10-year registration validity period with mandatory renewals, expands registration requirements to additional substances, and requires more extensive toxicological and environmental data for producers supplying 100–1,000 tonnes and over 1,000 tonnes annually into the EU.

Compliance activities throughout 2026 include inventory reviews, Safety Data Sheet updates, product assessments, and final regulatory submissions, with estimated costs of EUR 150,000–500,000 per substance and registration tier for mid-sized producers. In parallel, regulatory review delays in the United States continue to slow the commercialization of new pentanol-based products.

Updated EU CLP classification requirements effective May 1, 2025 for new substances and November 1, 2026 for existing substances further increase documentation and labeling obligations. Together, these regulatory requirements add approximately USD 20–45/MT in compliance costs, reducing the competitiveness of exporters from India, China, and Southeast Asia supplying the European market.

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude oil & propylene feedstock price volatility (Strait of Hormuz disruption) | –1.8% | Global; acute in Asia-Pacific, Middle East-linked supply chains | Short term (≤ 2 years) |

| Escalating EU REACH & global chemical compliance burden | –1.2% | EU core, UK, APAC corridors (Japan, South Korea); exporters to EU | Medium term (2–4 years) |

| Chinese petrochemical overcapacity & low-cost export pressure | –1.0% | North America, EU, Southeast Asia import markets | Short–Medium term |

| Substitution threat from bio-based & green solvents | –0.9% | EU, North America; emerging in APAC sustainability corridors | Medium–Long term (3–6 years) |

| VOC emission regulations tightening traditional solvent demand | –0.7% | North America (California, Canada), EU (IED), APAC early adopters | Short–Medium term |

| Geopolitical tariff friction & US–China trade uncertainty on chemical imports | –0.5% | US–China bilateral, North America, Indo-Pacific trade corridors | Short term (≤ 2 years) |

Geopolitical Impact Analysis

Escalating Middle East Conflicts Shock Petrochemical Feedstock Supply Chains

In 2026, the world’s market for pentanol suffers greatly from the disruptive effects brought on by the escalating direct military conflict in the Middle East region. After blockages and damage were inflicted on the facilities in the Strait of Hormuz, which serves as a primary route of transportation of about 20% of the world’s liquefied natural gas (LNG) and crude oil, the availability of the key raw materials has been sharply reduced.

This has resulted in a 25% to 35% surge in prices of the base products used in oxo pentanol manufacturing. This geopolitical shock is especially damaging for European chemical clusters, leading to the collapse on a massive scale of chemical manufacturing in these areas due to competitive energy costs and forcing the closure of thousands of metric tons of chemical production facilities.

Freight companies have been forced to take detours in transporting their ISO tank containers of bulk liquids as an alternative to the congested shipping lanes. Insurance costs have quadrupled, while contracts have invoked clauses of force majeure, creating a supply gap for the early fuel blending and industrial paint purchasing industries. In light of this volatile situation, international customers are moving away from spot purchasing toward localized supply chains and bio-based fermentation processes.

Regional Analysis

Asia Pacific Held the Largest Share of the Pentanol Market.

Asia Pacific commands the lion’s share of the global pentanol market with a whopping 41.2% share. This dominance is due to the presence of a large number of downstream processing plants in the area. These factors arise from the fast-growing auto manufacturing industry, industrial coatings production, and chemical synthesis facilities in several emerging countries in the region.

In addition to that, the increasing consumer population base along with urbanization is leading to high growth in the personal care products, cosmetics, and beverages sectors, thereby creating significant demand for C5 intermediates.

Furthermore, the rest of the global market share will be occupied by developed and developing countries, which have completely different business dynamics. North America and Europe continue to be important players in the business through the production of high-grade, Class 3 solvent requirements for complex pharmaceutical manufacturing operations and CDMOs, despite increasing challenges posed by increasingly stringent VOC regulations and fluctuating prices of industrial energy in these regions.

Key Regions and Countries Covered in this Report

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The pentanol market is dominated by an oligopoly market, whereby a group of multi-national companies in the field of chemicals owns a majority of the global capacity share. The tier one players own more than 60% of the world’s capacity through their innovative oxo technology processes and huge infrastructure in production facilities. Such an oligopoly makes it extremely difficult for new entrants to compete on parity in costs, as the large players use wide geographical distributions to set prices worldwide and supply volume availability.

The Following are some of the Major Players in the Industry

- BASF AG

- LANXESS

- Huntsman Corporation

- DowDuPont

- Eastman Chemical Company

- Chevron Oronite Company LLC

- Lubrizol Corporation

- Afton Chemical Corporation

- Fuel Performance Solutions Inc

- Evonik Industries AG

- Tokyo Chemical Industry Co. Ltd.

- Intermodal Tank Transport Inc

- Merck KGaA

- Arkema Group

- Other Key Players

Key Development

- In March 2026, Ensus signed a deal with the UK government to restart its bioethanol factory in Wilton, Teesside, thereby bolstering local bio-based chemical and fuel supply chains. The invention is likely to benefit the entire renewable alcohol value chain, including higher alcohols like pentanol.

- In February 2026, the Ministry of Petroleum and Natural Gas (India) mandated the sale of fuel blended with up to 20% ethanol beginning April 2026. The strategy is expected to boost investment in biofuel infrastructure and renewable alcohol production technologies, hence improving conditions for advanced alcohol markets such as bio-pentanol.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 1.3 Bn |

| Forecast Revenue (2035) | US$ 2.3 Bn |

| CAGR (2026-2035) | 6.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (n-Pentanol (1-Pentanol), Isoamyl Alcohol (3-Methyl-1-Butanol), 2-Pentanol, Others), By Purity Level (High Purity Pentanol, Technical Grade Pentanol), By End-use Industry (Chemical Manufacturing, Pharmaceuticals, Paints & Coatings, Food & Beverage, Cosmetics & Personal Care, Automotive, Agrochemicals, Others), By Distribution Channel (Direct Sales, Distributors & Traders, Online Chemical Platforms) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC- China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- GCC, South Africa, & Rest of MEA |

| Competitive Landscape | BASF AG, LANXESS, Huntsman Corporation, DowDuPont, Eastman Chemical Company, Chevron Oronite Company LLC, Lubrizol Corporation, Afton Chemical Corporation, Fuel Performance Solutions Inc, Evonik Industries AG, Tokyo Chemical Industry Co. Ltd., Intermodal Tank Transport Inc, Merck KGaA, Arkema Group, Other Key Players. |

| Customization Scope | Customization for segments and region/country-level will be provided. Moreover, we can provide further customization to meet your requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |