Quick Navigation

Report Overview

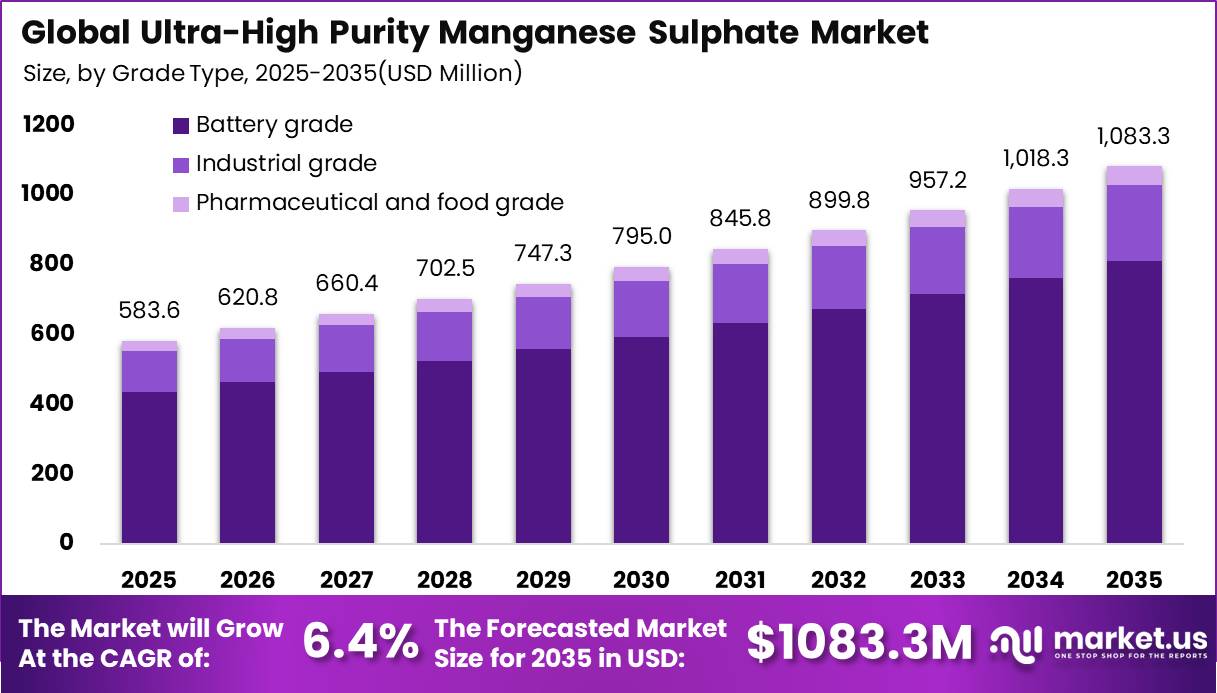

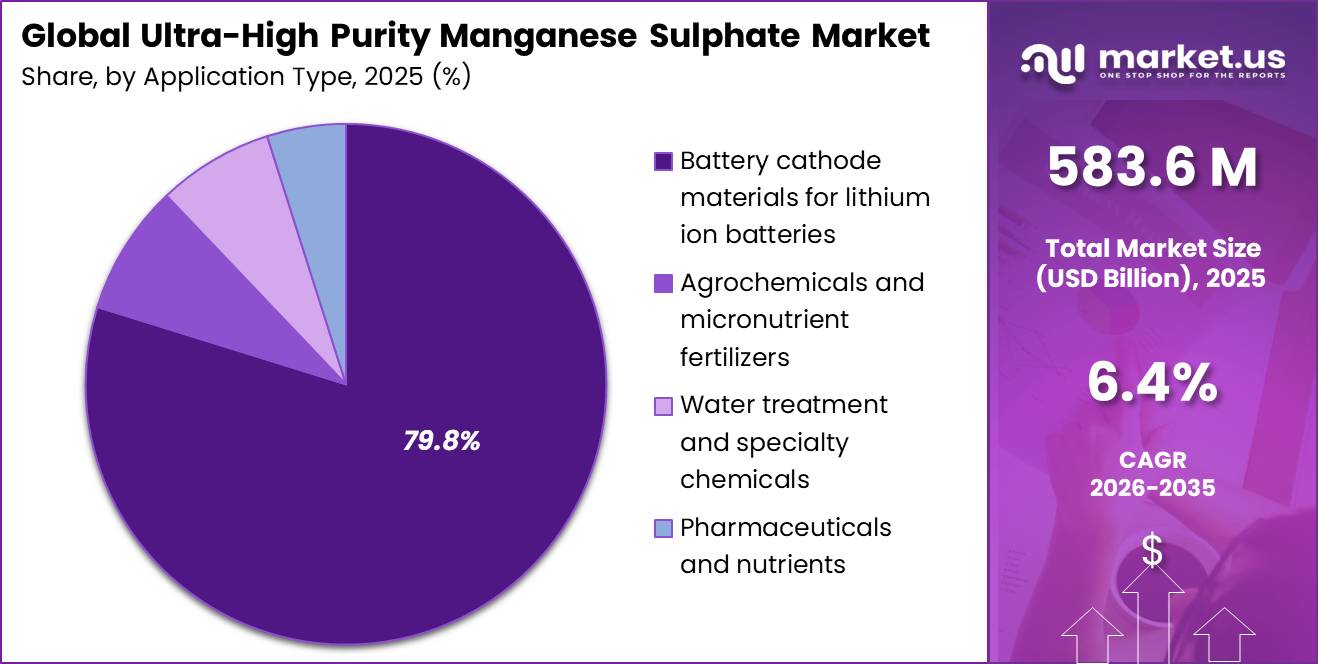

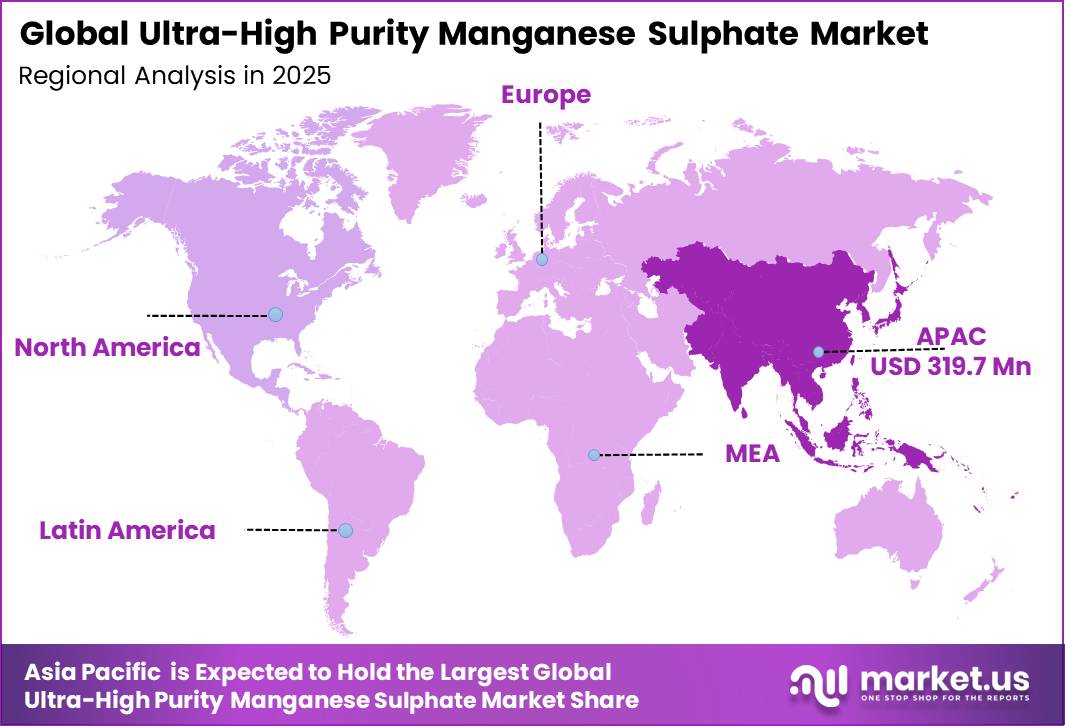

The Global Ultra-High Purity Manganese Sulphate Market size is expected to be worth around USD 1,083.3 Million by 2035, from USD 583.6 Million in 2025, growing at a CAGR of 6.4% during the forecast period from 2025 to 2035. Asia Pacific held a dominant market position, capturing more than a 54.8% share, holding USD 319.7 million in revenue.

The Ultra-High Purity Manganese Sulphate Market refers to the global marketplace for manganese sulfate with exceptionally high purity levels. Manganese sulfate is a chemical compound composed of manganese, sulfur, and oxygen, commonly used in various industrial applications, including agriculture, pharmaceuticals, ceramics, and batteries.

Ultra-high-purity manganese sulfate is produced through advanced purification processes that remove impurities and enhance product quality. It is widely used in battery manufacturing, agriculture, and pharmaceuticals. The market covers its production, distribution, consumption, pricing, supply-demand dynamics, and regulatory factors. While high-grade natural manganese ores contain about 40–45% manganese, common crustal rocks typically contain only 0.1–0.2%.

Key Takeaways

- The global market was valued at US$ 583.6 billion in 2026.

- The global market is projected to grow at a CAGR of 6.4% and is estimated to reach US$ 1,083.3 billion by 2035.

- On the basis of grade, Battery Grade dominated the market, constituting 74.9% of the total market share.

- Based on the application, Battery Cathode Materials for Lithium-Ion Batteries led the market, with a substantial market share of 79.8%.

- Based on the form, Crystalline or Powder led the market, comprising 59.8% of the total global consumption.

- Among the end-users, the Electric Vehicle and Energy Storage Battery segment held a major share in the market, accounting for 55.4% of the market.

- Among the applications, Agrochemicals and Micro-nutrient Fertilizers is the second most significant segment within the market, accounting for around 8.1% of the revenue.

- In 2024, the Asia Pacific was the most dominant region in the market, accounting for 54.8% of the total global consumption.

Grade Analysis

Battery Grade Dominates the Global Ultra-High Purity Manganese Sulphate Market Due to Rising EV Battery Demand

Battery Grade ultra-high purity manganese sulfate led the market with a dominant share of over 71.5%. This substantial market presence is primarily due to the growing demand for lithium-ion batteries in electric vehicles (EVs) and various electronic devices. Battery-grade manganese sulfate is crucial for producing cathode materials in lithium-ion batteries, offering high performance and efficiency.

The push towards electrification and sustainable energy solutions has significantly driven the demand for EVs, subsequently increasing the need for high-quality battery components. This trend has positioned battery-grade manganese sulfate as a key ingredient in the battery manufacturing industry.

Industrial-grade ultra-high-purity manganese sulfate also holds an essential place in the market. While it captures a smaller market share compared to the battery grade, its applications across agriculture, animal feed, water treatment, and industrial chemical processes remain vital. Industrial-grade manganese sulfate is utilized for its nutritional benefits in feedstock and its role as a micronutrient in fertilizers, enhancing crop yield and quality.

By Application

Battery Cathode Materials Lead Application Segment Driven by Lithium-Ion Battery Growth and Electrification Trend

In 2025, the Battery cathode materials for lithium-ion batteries segment held a dominant position in the ultra-high purity manganese sulfate market, capturing more than a 79.8% share. This dominance is primarily driven by the surging demand for lithium-ion batteries in the electric vehicle (EV) sector and various portable electronic devices.

Ultra-high purity manganese sulfate is a critical component in the cathode material of lithium-ion batteries, contributing to their efficiency, durability, and performance. The global push towards electrification, coupled with the rapid growth in the consumer electronics market, has significantly fueled the demand for high-quality battery components, placing the Batteries segment at the forefront of the market.

In the Chemical sector, ultra-high-purity manganese sulfate is utilized in various chemical reactions and processes. Its role in synthesizing other chemicals and in water treatment applications highlights its versatility and utility across a broad range of industrial and environmental applications.

By Form Analysis

Crystalline or powder form dominates the global ultra-high purity manganese sulphate market

Crystalline or powder form dominates the global ultra-high purity manganese sulphate market, accounting for 59.8% share. This dominance is mainly due to its high stability, easy handling, and strong suitability for lithium-ion battery cathode production, where precise composition and high purity are critical. It is widely preferred in electric vehicle and energy storage applications, making it the most important form in industrial usage.

Liquid solution form holds a smaller share and is mainly used in limited chemical and industrial processes where direct application or easier mixing is required. However, its adoption remains lower due to storage limitations and reduced stability compared to the crystalline or powder form, restricting its use in large-scale battery manufacturing.

End User Analysis

Electric Vehicle and Energy Storage Segment Dominates End-User Demand in the Global Ultra-High Purity Manganese Sulphate Market

The electric vehicle and energy storage battery segment dominates the global ultra-high purity manganese sulphate market, accounting for 55.4% share. This dominance is driven by the rapid expansion of the EV industry and renewable energy storage systems, where ultra-high purity manganese sulphate is a key material used in lithium-ion battery cathodes.

Other end-use industries collectively contribute the remaining market demand, including automotive and transportation OEMs, pharmaceuticals and healthcare, agriculture and agrochemicals, and other industrial users. These sectors use manganese sulphate in smaller but stable quantities for applications such as nutrients, fertilizers, chemical processing, and industrial formulations, supporting overall market balance beyond the battery sector.

Key Market Segments

By Grade

- Battery grade

- Industrial grade

- Pharmaceutical and food-grade

By Application

- Battery cathode materials for lithium-ion batteries

- Agrochemicals and micronutrient fertilizers

- Water treatment and specialty chemicals

- Pharmaceuticals and nutrients

By Form

- Liquid solution

- Crystalline or powder

By End-user

- Electric vehicle and energy storage battery

- Automotive and transportation OEMs

- Pharmaceuticals and healthcare

- Agriculture and agrochemicals

- Other industrial users

Market Dynamics

Challenges

China’s dominance in battery-grade manganese sulphate refining remains a key restraint on market expansion. The country accounted for approximately 95% of HPMSM production in 2024 and is estimated to control 85–90% of global refining capacity. This concentration increases sourcing dependence, extends supplier qualification timelines, and limits procurement flexibility for manufacturers outside China.

It also creates pricing asymmetry across regional markets and reduces the availability of qualified alternative suppliers during periods of trade or policy uncertainty. As a result, downstream manufacturers face elevated supply-chain risk and reduced bargaining power. For 2026, the imbalance is estimated to reduce achievable market CAGR by roughly 2.2 percentage points as OEMs and precursor producers maintain higher inventories and pursue dual-source qualification strategies.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| China Refining Concentration | -2.2% | North America core, EU regulatory hubs, Japan-Korea cathode chain | Long term (≥ 4 years) |

| Multi-Step Purification Yield Loss | -1.6% | China processing base, North America pilots, EU scale-up sites | Medium term (2–4 years) |

| Ore-to-Chemical Logistics Volatility | -1.2% | South Africa-Gabon export lanes, APAC import corridors, Atlantic battery routes | Medium term (2–4 years) |

| Ex-China Project Execution Risk | -1.8% | U.S. Gulf Coast, Arizona, the Czech Republic, Canada, and Mexico | Long term (≥ 4 years) |

| Feedstock Qualification Variability | -1.0% | Australia, South Africa, Gabon, North America conversion assets | Medium term (2–4 years) |

| Cathode Chemistry Demand Uncertainty | -0.9% | Europe NMC base, U.S. localization chain, China LMFP transition | Short term (≤ 2 years) |

Opportunity

Circular manganese recovery represents a significant long-term growth opportunity, as recycled feedstock volumes remain limited relative to primary HPMSM demand. However, growing battery scrap availability, black-mass processing partnerships, and closed-loop supply agreements are creating new pathways for secondary manganese sulphate production.

The EU Batteries Regulation further supports this trend through mandatory battery traceability requirements and restrictions on battery disposal, strengthening the economic case for manganese recovery. The opportunity is estimated to contribute approximately 1.7 percentage points to future market CAGR.

Producers that secure manufacturing scrap and end-of-life battery materials can potentially reduce raw-material cost volatility by 8–15% and improve EBITDA margins by 250–450 basis points through blended feedstock optimization. If battery recycling scales toward the Critical Raw Materials Act (CRMA) target of 25% recycled material by 2030, capturing even 3–5 ktpa of secondary manganese sulphate equivalent could generate a meaningful recurring revenue stream while supporting OEM demand for lower-carbon battery materials.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Ex-China localization premium | +2.4% | EU, North America core | Short term (≤ 2 years) |

| LMR/LNMO cathode positioning | +3.1% | China, EU, North America, Korea/Japan | Medium term (2–4 years) |

| Circular manganese recovery | +1.7% | EU, North America, Korea | Medium term (2–4 years) |

| Tolling + traceability model | +1.3% | EU, North America | Short term (≤ 2 years) |

| Merchant precursor integration | +2.0% | China, EU, Southeast Asia | Medium term (2–4 years) |

| Strategic project roll-up | +2.6% | EU, North America, and Africa-linked supply chains | Long term (≥ 4 years) |

Drivers

Localization has become a direct demand catalyst because governments are no longer focused only on mining; they are increasingly backing chemical conversion and precursor-grade processing capacity. In the United States, South32’s Clark project received a DOE award of up to $166 million covering 30% of the project cost on a cost-share basis, while other announced projects, such as Element 25’s planned 65,000 t/yr HPMSM facility in Louisiana and South32 Hermosa’s planned 60,000 t/yr HPMSM processing capacity, show that refining-scale ambitions are moving beyond pilot rhetoric.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV battery demand scale-up | +2.8% | APAC core, North America core, EU core | Short term (≤ 2 years) |

| Manganese-rich cathode mix shift | +2.1% | China, Korea, Japan, EU cell hubs | Medium term (2–4 years) |

| Localized refining under industrial policy | +1.9% | North America core, Australia-US corridor, EU projects | Medium term (2–4 years) |

| EU battery traceability and compliance pull | +1.3% | EU core, EEA suppliers, import-dependent Asian refiners | Short term (≤ 2 years) |

| Non-China supply diversification pipeline | +1.7% | U.S., Canada, Czech Republic, Mexico, South Africa, Australia | Medium term (2–4 years) |

| Purification technology and yield improvement | +1.2% | China incumbents, North American pilots, EU converters | Short term (≤ 2 years) |

Restraint

The market’s primary structural restraint is the high concentration of battery-grade manganese sulphate refining in China, which controls more than 85% of global refining capacity and accounts for approximately 95% of HPMSM production in 2024. This dominance exposes Western cathode and precursor supply chains to sourcing dependence, pricing volatility, and policy-driven supply risks.

Limited commercial-scale refining capacity outside China further constrains supply diversification and increases procurement uncertainty for battery manufacturers. The concentration is estimated to reduce the achievable market CAGR by approximately 2.4 percentage points. Even modest disruptions in Chinese export availability can create disproportionate supply pressure in Europe and North America, where alternative capacity remains limited.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| China’s refining dependence | -2.4% | North America, the EU, Japan, and Korea | Medium term (2–4 years) |

| Project permitting delays | -1.9% | EU, US, Canada, Australia | Medium term (2–4 years) |

| Ore logistics bottlenecks | -1.6% | South Africa corridors, Gabon, China-linked APAC | Short term (≤ 2 years) |

| EV cathode demand resets | -1.8% | US, EU, Korea, Japan | Short term (≤ 2 years) |

| Tariff and policy fragmentation | -1.3% | US-China lane, EU import chain, ASEAN reroutes | Short term (≤ 2 years) |

| Cost inflation and qualification drag | -1.5% | Global, especially new Western plants | Long term (≥ 4 years) |

Geopolitical Impact Analysis

The global ultra-high purity manganese sulphate market is highly influenced by geopolitical factors due to its strong link with the lithium-ion battery supply chain. Production is largely concentrated in the Asia Pacific, especially China, which dominates both battery manufacturing and raw material processing. This concentration creates supply chain dependency, making the market sensitive to trade policies, export regulations, and geopolitical tensions.

At the same time, countries like the United States and those in Europe are actively working to develop local battery material supply chains to reduce import dependence and improve energy security. Government support for electric vehicles and clean energy transition is encouraging investment in domestic production of critical battery materials.

However, export restrictions, raw material control, and environmental regulations in key producing regions can impact global supply stability and pricing. Overall, geopolitical factors are driving the market toward regionalization, where countries are focusing on securing and localizing their battery supply chains to ensure long-term stability and resilience.

Regional Analysis

Asia Pacific dominates the global ultra-high purity manganese sulphate market, accounting for the largest share of 54.8%, driven by its strong and well-established lithium-ion battery manufacturing ecosystem. Countries such as China, Japan, and South Korea play a major role in global electric vehicle (EV) battery production and energy storage systems, making the region the central hub for demand.

The availability of raw materials, cost-effective production capabilities, and the strong presence of battery and electronics manufacturers further strengthen its dominance. Rising investments in EV infrastructure and clean energy technologies continue to support long-term market growth in this region.

North America and Europe also hold important positions in the market, supported by increasing focus on electric mobility, renewable energy storage, and sustainable battery material production. These regions are actively investing in building localized supply chains to reduce dependency on imports, especially for critical battery raw materials.

Government support and strict environmental regulations are also encouraging the development of advanced and cleaner production technologies. Latin America and the Middle East & Africa are emerging regions with gradual growth potential. Their development is mainly driven by increasing industrialization, mining activities, and long-term infrastructure expansion, which may support future demand for battery materials.

Key Regions and Countries Covered in this Report

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global ultra-high purity manganese sulphate market is moderately concentrated, with a strong presence of Asia Pacific players due to the region’s dominance in lithium-ion battery and electric vehicle production. Market share is mainly driven by companies with integrated manganese sourcing, high-purity processing capabilities, and long-term supply contracts with battery manufacturers. Growing EV demand is increasing competition and encouraging capacity expansion across key producers.

Market Key Players

- Guizhou Dalong Huicheng New Material

- CITIC Dameng Mining Industries

- Guizhou Redstar Developing

- ISKY Chemicals

- Prince ERACHEM Comilog

- Lantian Chemical

- Guizhou Manganese Mineral Group

- Jost Chemical

- American Elements

- Merck Sigma Aldrich

- Thermo Fisher Scientific

- Xiangtan Electrochemical Scientific

- C4V iM3NY

- Qingdao Haimen Battery Materials

- Changsha Haolin Chemical

- Other companies

Recent Developments

- In 2025, Guizhou Dalong Huicheng New Material achieved commercial-scale production of lithium manganese iron phosphate materials, strengthening its manganese-based battery-material portfolio. The company projected first-quarter output exceeding 4,500 tonnes of trimanganese tetraoxide and approximately 20,000 tonnes of battery-grade manganese sulfate.

- In 2025, CITIC Dameng Mining Industries’ operations under South Manganese Group commissioned a manganese-ingot smelting upgrade with an annual capacity of 300,000 tonnes and a high-manganese precursor project. The precursor project’s first phase added 20,000 tonnes per year of battery-grade trimanganese tetraoxide capacity, while the upgraded process reduced energy consumption by approximately 20%.

- In 2026, Guizhou Redstar developed the environmental approval process for a new high-purity thiourea production project involving an investment of RMB 148.62 million. The project will establish an annual capacity of 20,000 tonnes and replace the company’s existing 10,000-tonne-per-year thiourea production facility.

- In 2025, ISKY Chemicals established ISKY Zinc Nutrition Technology (Malaysia) Sdn. Bhd., expanding its international manufacturing and service footprint in the life-nutrition market. The development complemented ISKY’s existing 150,000-tonne-per-year high-purity manganese sulfate project and its sales network covering more than 80 countries and regions.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 583.6 Bn |

| Forecast Revenue (2035) | US$ 1,083.3 Bn |

| CAGR (2026–2035) | 6.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2025–2035 |

| Forecast Period | 2025–2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Grade (Battery Grade, Industrial Grade, Pharmaceutical and food grade), By Application (Battery cathode materials for lithium ion batteries, Agrochemicals and micronutrient fertilizers, Water treatment and specialty chemicals, Pharmaceuticals and nutrients), By Form (Liquid solution, Crystalline or powder), By End-user (Electric vehicle and energy storage battery, Automotive and transportation OEMs, Pharmaceuticals and healthcare, Agriculture and agrochemicals, Other industrial users) |

| Regional Analysis | North America: The US and Canada; Europe: Germany, France, The UK, Italy, Spain, Russia & CIS, and the Rest of Europe; APAC: China, India, Japan, South Korea, ASEAN, and the Rest of APAC; Latin America: Brazil, Mexico, and Rest of Latin America; Middle East & Africa: GCC, South Africa, and Rest of Middle East & Africa. |

| Competitive Landscape | Guizhou Dalong Huicheng New Material, CITIC Dameng Mining Industries, Guizhou Redstar Developing, ISKY Chemicals, Prince ERACHEM Comilog, Lantian Chemical, Guizhou Manganese Mineral Group, Jost Chemical, American Elements, Merck Sigma Aldrich, Thermo Fisher Scientific, Xiangtan Electrochemical Scientific, C4V iM3NY, Qingdao Haimen Battery Materials, Changsha Haolin Chemical, Other companies |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |